Jeevan Akshay VI is the LIC’s Single Premium Pension Plan. This plan reintroduced from 1st December, 2016 with some changes. Let us see the additional features of it.

Many agents spread rumors that this plan is going to be closed soon. But in reality, LIC revamped the annuity payout, few features of this plan and reintroduced it. As expected, annuity was dropped under this plan to match with falling interest rate.

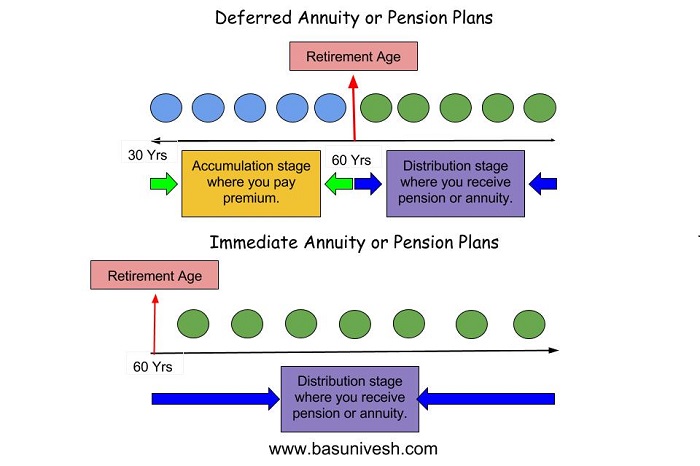

Before proceeding further, let us understand few new words related to pension or annuity plans.

What is the meaning of annuity?

In simple term, you can say it as a Pension, where you will get regular income up to the specified period or conditions. There are two types of annuity.

1) Immediate Annuity-In this case, you invest a lump sum in a product and your pension or annuity starts immediately. Let us say you have around Rs.1 Cr and if you buy immediate annuity plans, then the pension will start immediately from next month.

2) Deferred Annuity-In this case your annuity starts after a certain period. Let us say your current age is 30 years and you are planning to retire at the age of 60 years. If you buy a deferred annuity plan, then you will invest up to your retirement age i.e. up to 60 years of age. After 60 years of retirement, your pension will start.

I tried to explain the same with below illustration as below.

Features of Jeevan Akshay VI – LIC’s Single Premium Pension Plan

LIC’s Jeevan Akshay VI is an immediate annuity plan. This plan is available both in offline and online mode. Click HERE to buy online.

# Minimum Age 30 Yrs.

# Maximum Age 85 Yrs.

# For Offline the minimum purchase price Rs.1,00,000. For online the minimum purchase price is Rs.1,50,000.

# No maximum limit.

# No medical examination required for buying this plan.

# Premium must be payable as a lump sum.

# Pension may be paid either at monthly, quarterly, half-yearly or yearly intervals. It is purely your choice.

# If your purchase price is Rs. 2.50 lakh or more, you will receive the higher amount of annuity due to available incentives. But I have not found what incentives LIC Provides.

# For policies sold online, a rebate of 1% by way of increase in the annuity rate shall also be available.

# No loan facility available under this plan.

# If you are not satisfied with the Terms and Conditions of the policy, you may return the policy within 15 days from the date of receipt of the Policy Bond. On receipt of the policy, LIC will cancel the same and the amount of premium deposited by you will be refunded to you after deducting the charges for stamp duty.

# Nomination is allowed under this plan.

# Assignment of this policy is not allowed.

# Backdating not allowed.

Annuity or Pension Options available in LIC’s Jeevan Akshay VI

- Annuity payable for life at a uniform rate-Once the death occurs the pension holder, then pension ends there itself and the nominee will not receive anything.

- Annuity payable for 5, 10, 15 or 20 years certain and thereafter as long as the annuitant is alive-Once the death occurs the pension holder, then pension ends there itself and the nominee will not receive anything.

- Annuity for life with return of purchase price on death of the annuitant-Once the death occurs the pension holder, then pension ends there itself and the nominee will receive the invested amount.

- Annuity payable for life increasing at a simple rate of 3% p.a. Here the pension will be increased at 3% per year throughout the policy period. Once the death occurs the pension holder, then pension ends there itself and the nominee will not receive anything.

- Annuity for life with a provision of 50% of the annuity payable to spouse during his/her lifetime on death of the annuitant.

- Annuity for life with a provision of 100% of the annuity payable to spouse during his/her lifetime on death of the annuitant.

- Annuity for life with a provision of 100% of the annuity payable to spouse during his/ her lifetime on death of the annuitant. The purchase price will be returned on the death of last survivor.

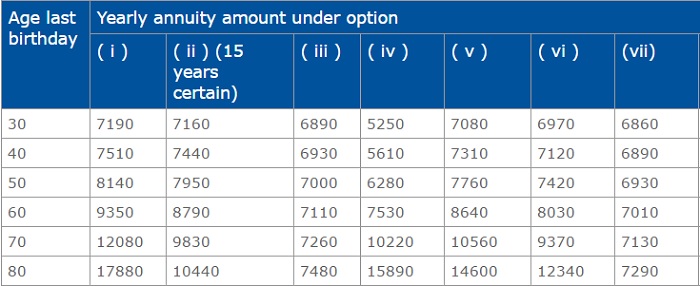

How much pension you receive from LIC’s Jeevan Akshay Plan?

Effective from 1st December, 2016 LIC reduced the annuity rate of this plan. In below image, I showed you the earlier annuity rates.

In below image, I will show you the Jeevan Akshay VI annuity rates applicable effective from 1st December, 2016.

Notice the difference. LIC reduced the annuity rates to match with the current falling interest trend.

For your age and the options you want to choose, you can calculate the premium HERE.

Jeevan Akshay VI – LIC’s Single Premium Pension Plan changes from 1st December, 2016

What are the changes that were made to earlier plan? Earlier you are not allowed to surrender in this plan. Now it is allowed. But there are few conditions to it.

# Annuity rates were dropped drastically to match the falling interest rates. I already showed the earlier rates to current rates in above images.

# Surrender is allowed after the completion of a policy period.

# Surrender is allowed for the annuity options where you have the option of “Annuity with return of purchase price”. Therefore, from above annuity options, only the options 3rd (Annuity for life with return of purchase price on death of the annuitant) and option 7th (Annuity for life with a provision of 100% of the annuity payable to spouse during his/ her lifetime on death of the annuitant. The purchase price will be returned on the death of last survivor.)

# If the annuitant is shifting to another country permanently as evidenced in their visa or citizenship documents. The surrender value payable shall depend on the age (last birthday) of the policyholder at the time of surrender of the policy.

# If the annuitant is diagnosed as suffering from any of the following critical illnesses:

- Cancer of specified severity

- Myocardial infarction

- Open Chest CABG

- Open Heart Replacement or Repair of Heart Valves

- Kidney Failure requiring regular dialysis

- Stroke resulting in Permanent Symptoms

- Major Organ/Bone Marrow Transplant

- Permanent Paralysis of Limbs

- Motor Neurone Disease with Permanent Symptoms

- Multiple Sclerosis with Persisting Symptoms

- Angioplasty

- Benign Brain Tumor

- Blindness

- Deafness

- End-stage Lung failure

- End stage liver failure

- Loss of speech

- Loss of Limbs

- Major Head Trauma

- Primary(Idiopathic)Pulmonary Hypertension

- Third Degree Burns

Long back I wrote a post on this plan (LIC’s first online plan “Jeevan Akshay-VI”-Review). However, I thought to write it once again after the new changes done to this plan.

Whether LIC’s Jeevan Akshay VI is the best pension plan in India?

This is the immediate pension plan. Therefore, once you accumulate the retirement corpus then you can think of this plan. This plan offers FIXED pension based on the option you opted.

If you accumulated enough retirement corpus, then you can think of buying this plan as it offers FIXED returns. Whether the interest rate falls or goes up, you no need to bother.

The biggest concern is, this product will not take care of inflation. LIC provided the 3% inflation-adjusted pension payment in one of the above annuity option. But in my view, 3% is not at all enough when the real inflation rate is more than 7%.

The second biggest concern is taxation. The pension you receive from this plan is added to your income and taxed as per your tax slab. Therefore, if your agent lure you that this plan offers more than 7% returns, the post-tax return reduce further.

Many spread rumors that this is the BEST retirement product. But in my view, it fails to give you the post-tax real returns. However, I must admit that if someone is looking for a constant stream of income (without bothering about taxation and inflation), then you must go ahead.

Please explain details of LIC of India plan. Table 803 issued in 2010. Investment plan.

Dear Syed,

What details you want?

if i want to remove my cash from jeevan akshay akshay 6 policy how can i remove……

Dear Prakash,

Please be in touch with the home branch.

Hello Basu,

Hope you are doing well.

This is regarding Immediate annuity with return of purchase price plan(Plan C). As for an NRI, if they opted for this plan, TDS will be deducted directly from annuity/Pension amount rest we will get in our bank account.

Can we file tax return to get back the amount deducted as TDS ? Please mention the detail.

Looking for positve response from yourside.

Thank You

Mayank-Yes, you can file ITR and get it back if your tax payment is less than what they deducted.

Lock in period is death for Jeevan Akshay VI ? Basavaraj please comment on this/

Rajeev-Refer my above post. There is no such lock-in. But you are not allowed to withdraw or close this plan easily. Refer the conditions set for closure.

Same thing , If we are unable to withdraw or close this plan easily.Why People are purchasing it.

Rajeev-Because they need a secured monthly return.

Sir,

Is this plan still available? LIC website lists this plan under “Withdrawn products” – https://licindia.in/Products/Pension-Plans/jeevan_akshay. Also, is this the best immediate annuity plan available in India?

Jalakrut-It is relaunched and available now also. Please check HERE.

send details for single time payment and immediate pension scheme

Mani-The details are available in above post.

Hello, I am interested in taking this policy. I’m 37 years old. I want to invest 54 lakhs and take an immediate annuity with option of return on purchase price upon death. The online payment seems a little complicated as they are only accepting net transfer and there is hardly any help. Can you please explain how much is the monthly annuity payout if I take this policy off-line compared to online?

Ram-May I know what prompted you to choose this plan at this age?

Bank FD interest rates are falling day by day and future repo rates are sure to fall. So I am rolling the dice and taking a change. I work in a private sector so I think I better secure my future with at least 20% of my income from pension source

Ram-How you assume that FUTURE REPO RATES fall? Do remember that return from this plan is taxable income for you like salary income.

My wife and I are 26 and 29 yrs old, currently no child and both are working in software industry. We have corporate insurance of 3L sum insured each. Should we also take family health insurance which include us and my child in future? if yes, please suggest plan.

Thanks

Kumar-Yes, having own health insurance is a must.

Thanks,

Which one will be better individual or family plan?

Could you please suggest few plan?

Kumar-You have to go for family floater plans. Refer my earlier post, which may help you in shortlisting the product “IRDA Incurred Claim Ratio 2015-16 | Best Health Insurance Company in 2017“.

People are talking about LIC Jeevan Akshay and Fixed Deposits for retirement planning. However, very few paying heed to SWP of Mutual Funds.

Provided one is ready to stay in stock market for long term via Mutual Fund, one can easily invest a major portion of investment in 2-3 mutual fund schemes. One can choose Equity balanced fund and start withdrawing at 7% – 8% per year. Equity funds have a lock in period of 1 year for getting tax exemption. Hence, after 1 year a person can get steady monthly income that too tax free (since it is redemption of units) and original corpus would also increase significantly (assuming mutual fund would generate higher return than above-mentioned 7%-8% )

This way a person can take care of both tax liability and capital appreciation.

Sir,I have a query to you

1.Is SCSS scheme for once in life for maximum period of 8 years(15 lakh) with extension or I can reinvest as a same person after 8 years over?

Pratik-Refer my post regarding SCSS at “Post Office Senior Citizen Scheme (SCSS)-Benefits and Interest Rate“.

I am retired,68. For my essential monthly expense, I have FDs in two banks. Bit extra money in hand, I approached LIC. Agent gave me Jeevan akshay VI scheme brochure, and I chose the most risky(risk calculated) one, which gives me a return of 10.5% or above, BUT..that is, as long as I am alive. Once kick the bucket..no corpus..no interest nothing. Where I fell in love with the scheme is when I was told, no tax on interest. But that was a professional lie.. Still, don’t you think, its wise to take juice out, when the fund tangible?…………..??????

John-You are still in the illusion that this plan offers you 10.5% returns (irrespective of whatever the option you select). Second thing is, you can opt for ONLINE, then why you took it OFFLINE? The monthly pension you receive from this scheme is taxable income to you. Also, surrender is allowed only with few options, not for all.

Dear Sir,

I am 40 years male, unmarried with No EMI or any loans. Would like to invest, but have no clue about it. Need your suggestion on the same.

I thought of investing in some retirement/pension plans to have regular income after my retirement. What about investing in Single premium Annuity pension plan and fixed deposit…?

Which plans are best for the above two options…? your other financial suggestions also will be much appreciated. Looking forward your valuable reply here or at my mail id provided.

Thanks

Gopal

Gopal-Currently you are working or not? From when you need this retirement monthly income?

Sir – currently i am working. i may need this regular income in next 5 years, that is when i reach 45 years.

Gopal-Then use Postal MIS.

Sir –

I am an NRI. cant use postal MIS. I thought of retiring from professional work by 45 years, that is in next 5 years, so thought of investing something for regular monthly income.

I may plan to involve in some social activities or some other work for nominal salary after 45 years in India.

Please suggest accordingly, sorry if i ask more from you.

Regards

Gopal

Gopal-It is hard to suggest a single product which suits your retirement. Because I am not aware about your financial life. But you can check the above product for it’s suitability. However, you said your constant monthly requirement is only for 5 years. Hence, I recommended MIS.

Dear sir,

My father has retired with lumpsum retirement benefit.So,I want to invest some amount in lici pension plan.So,as per latest news that govt. announced VPVY 2017 is coming months.Therefore,if I invest money to Jeevan Akshay plan then it will not possible for opening a new account for new scheme.So,my question is that should i wait a month for new lucrative lici new pension scheme or i invest it to old jeevan akshay scheme??As far as i know that interest rate would be much higher with the upcoming scheme.and if i opened in jeevan akshay as per new pattern changes on dec of 2016 then which option i.e. out of 10 option which one is prefer to apply for monthly pension for my father with 100% given to my mom and after that purchase value return to me????

Pratik-I replied to your FB message.

Hi

Was told current interest of 6.7% for jeevan akshay 6 wud change again after March 31st. Is it true. Kindly confirm.

Really appreciate u taking time to help others.

Tks

Shirine-As of now, there is no such confirmation. Hence, I consider such news as rumors.

Logically, they might change the annuity rates again as FD rates fall, Shireen – say by Dec’17 or Mar’18 etc – finally it’s all speculation (like in shares 🙂

Meanwhile, the agents will continue to cry ‘fox’ ‘fox’ & that this plan is going to disappear or give lesser returns soon etc (it’s their work as agents, anyway – always best to use our common sense) – I’ve been hearing this personnaly from a friend agent since 2012.

However, I have been checking out this plan on LIC site from 2007 – that’s a whole 10years in my sight alone & rates have dipped along with FD rates but plan has not gone away – experts can comment based on more data & experience, of course – this is a layperson point of view.

As per me, it’s not the greatest plan alive, to panic anyway 🙂 – but yes, if you are a traditional minded ‘FD person’, LIC JA VI makes a lot more sense as FDs are max 10years contracts you have with banks whereas JA VI is a lifetime contract with LIC – in that way, interest rate they offer is protected! Of course forgetting inflation & all such alone it can be said so.

Back to the topic, yes, since they fixed these annuity returns, FD rates have further gone down, so logically they might revise their rates sometime in next one year or so – speculatively, again! Basis of speculation:

In 2012 when 10year FD rates were 9.5% (max at IDBI), LIC JA VI was giving ~5.8% starting annuity on Option4 @ 3pc incr, to take an e.g., based on what I recollect

In late 2016 when 10year FD rates were 7% & falling they are giving ~5.6% starting annuity on Option4 @ 3pc incr (just for an e.g. – rates of every option has proportionately fallen) that continues now

Today 10year FD rates are 6.5% and still going south, like, its already hit 6% in some banks.

Considering 10year FDs is the nearest competition for LIC JA VI plans have (good idea of theirs, targetting the ultra orthodox middle class sense of secure investments in India), yes, there’s a probably that the annuity might further be set downward. When? All’s possible is to guess. If you have some insiders in higher positions in LIC, check what are in the related memos that are floating over their desks (not the stuff they use to market their products to customers, but real official decision stuff!). Just kidding:-) your guess is as good as mine!

Summary is that if the plan appears attractive to you now, based on whatever parameters & life goals & sense of peace goals you have, good chance that it’ll still be attractive even after they bring it down would be a good guess too 🙂 – finally, again, entirely your call!

I need to generate regular steady income for my parents. Which option is better. SWP from equity mutual fund. Lic annuity plan. Or combination of both. Please advise.

Ravi-Hard to say but if you not worrying about taxation and concentration is only on FIXED income, then better to stick to this plan.

Thank you. With rising health care costs one critical illness can cause bankruptcy in old age. To counter this threat I plan to invest in multi bagger stocks which have the potential give 10x returns like Idfc bank do you agree with this. Strategy I don’t health insurance is reliable in old age with pre existing conditions

Ravi-The same multi-bagger stocks ruin your principle if the market starts to fall. Do you have the guts to sustain such loss? Take risk but calculated risk. The so-called multi-bagger stocks are meant for TRADERS who love when you buy and sell. For funding of health emergencies, investing in stocks is the disaster. Rest you have to decide. Equity will give good return BUT WHEN? Is it when you need money for your father’s hospitalization? No…but in long run and that too if your holding period is more than 5+ years. Never rely on these so called experts cum brokers.

Very good review

I’m 34 yrs old and my wife is 30 yrs with 3yr kid can I take this policy on my wife’s name for long term investment and among seven options which one would suit me can you suggest a bit confused

Rahul-Is she in need of monthly income?

Hi Basu,

I am looking for a child insurance/education plan to support my child for his future needs irrespective of my presence.

I am 35 year old and have a 2yr old son.

Also please let me know your best take on the above along with Pension plans as requested by others.

This will be of great help to people like us who do not have much idea on these.

Thanks & Regards

Sirisha

Srisha-Never run behind any child or pension plans. First, buy term insurance to the tune of around 15-20 times of your yearly income. Then based on the time horizon of goals, start to invest in mutual funds. Refer my posts for the same “Top 10 Best SIP Mutual Funds to invest in India in 2017” and “Top and Best Debt Mutual Funds in India for 2017“.

Thanks a lot Basu for the much needed advice.

Sirisha-Pleasure 🙂

Dear sir

We respect your awesome movement to create real financial knowledge even to learned people like me,

will soon seek your advice for personal finance coaching

Regards

Basavarajaiah-Sure.

The article was very helpful. Can you also share your views about HDFC Life Assured Pension Plan. Was going through the features here – https://goo.gl/YGUayA

Jai-It is a ULIP plan and we are fond of the words ASSURED or GUARANTEED, but how much and whether it is suffice or not we never estimate. Also, this is not immediate annuity plan to compare that product with this LIC’s product.

Dear Basu Ji,

I really like to read your post and blogs.

I had arequest if you can post comparision between top 5 Immediate anuuity plan presently in india in detail.

Thank you.

Mayank-Thanks for your tips. Sure..I will come with this post soon.

Hi ,

Somedays back you suggested me this one for investment, is there any other plan in market competitive to this one?

regards,

Dnyanesh

Dnyanesh-I still suggest if you are not worrying about inflation and tax.

thanks, but if we worry about tax? is there any other way?

inflation i am not worry, but don’t want to pay tax on earned or getting money.

Dnyanesh-But to be frank inflation is the dangerous enemy than tax which we common people never estimate. Rest you decide on your own.