Government announced Interest of PPF KVP NSC SCSS and Sukanya Samriddhi Account and also Post Office Savings Schemes for the period of 1st April to 30th June 2016. There is a huge decrease.

In my last post, I mentioned how the interest rate is now calculated for all Post Office Savings Schemes. This is the big move, which no one expected. Because since long we never faced the interest rate risk in fixed instruments or debt products. Now it is the reality that fixed instruments or debt products are also volatile in nature and associated with risks. Please go through my earlier post of how the interest rate is going to be calculated in future.

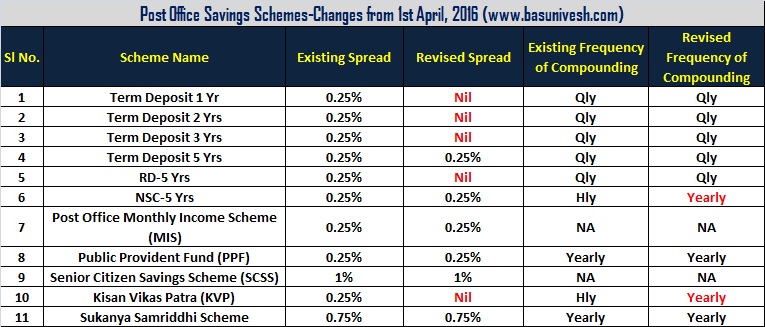

Few highlights of these changes are as below.

- Post Office Savings Schemes rates change on a quarterly base.

- Sukanya Samriddhi Yojana, Senior Citizen Savings Scheme (SCSS) and the Monthly Income Scheme (MIS) enjoys a higher interest rate than other Post Office Savings Schemes.

- The Effective interest rate on National Savings Certificate (NSC) and Kisan Vikas Patra (KVP) reduced.

- Higher liquidity in Public Provident Fund (PPF).

- 1 yr., 2yr., and 3 yr. term deposits, KVPs and 5 yr Recurring Deposits (RD) fetch lesser returns.

The same is explained in below image.

I highlighted the changes in red colour for your better understanding.

Below are the Interest of PPF KVP NSC SCSS and Sukanya Samriddhi Account and other Post Office Savings Schemes. These rates will be applicable from 1st April to 30th June 2016.

Here, I marked in the red colour of whatever the changes from 1st April 2016. Few points you must notice.

# You notice that earlier the interest rate for Term Deposits of 1 Yr, 2 Yrs and 3 Yrs used to be same. Now it is not the case. Also, instead of 5 Yrs Term Deposit, NSC fetch you more return. Because Interest rate for 5 Yrs Term Deposit is 7.9% while for NSC it is 8.1%. But due to compounding effect, the 5 Yrs Term Deposit will actually fetch you more return than the 5 Yrs NSC.

# Earlier KVP (Kisan Vikas Patra) used to double your money in 100 months or 8 Yrs 4 Months. Now KVP double after 110 months or 9 Yrs 2 Months. So almost a year of gap. It is due to change in compounding frequency from half yearly to yearly. Also, due to the drop in interest rate.

# No change in savings account interest rate. So you still enjoy same 4% interest rate.

# Earlier SCSS (Senior Citizen Savings Scheme) used to fetch you highest interest rate. But now both SCSS and Sukanya Samriddhi Scheme offers same interest rate. Because both these schemes are considered as social schemes.

# After SCSS and Sukanya Samriddhi Scheme, 5 Yrs Term Deposit is the scheme which fetch you highest effective return of 8.13%.

Hence, if your idea is not for tax saving, then instead of NSC you can directly go for 5 Yrs Term Deposit.

Whether to invest or not?

No option…The noise of reducing interest rate will be for time being. After that we have to accustom for these changes. But this gives a real shock to many Indians. Because they never felt volatility in their post office scheme. However, now they will see it on a QUARTERLY basis. I still feel PPF and SCSS are best product to invest.

When we consider the real return (return on investment-inflation rate), I feel these post office saving schemes still offering you positive real returns. Just quoting one Facebook group comment here to make you understand on this.

Hope this will cool down many investors 🙂

Hello Sir,

Your Articles are really great and thanks for this good help you are doing.

I am 27 yrs old and i am investing Rs.1000 in each of the below mentioned Mutual funds via SIP and planning to continue it for another 10 to 15 years.

Sundram select midcap-Gr – Nov 2015

Reliance small cap fund-Gr – Dec 2015

Franklin India smaller companies fund-Reg-Gr – Nov 2016

DSP BR small cap fund-Reg-Gr – Nov 2016

HDFC MidCap Opp Fund-Gr – Nov 2016

Right now my investment is 100% in Equity and planning to invest 5000 more in ELSS/Debt funds.

My portfolio suggests to invest 30% in Debt and 70% in Equity. could you suggest me some good ELSS and Debt funds. and also suggest me whether i can go for opening a PPF account.

Awaiting for you reply.

Thanks in advance.

Regards,

Sathya

Dear Sathya,

Who suggested these funds to you? Why so many small cap funds? Who suggested you 30:70 ratio?

I have chosen those funds on my own by referring in net. i have read, it has to 30:70 ratio for the mutual funds if the investment is above 10 years. whether i will lose with these funds having in my portfolio and how can i make i correct? could you please suggest?

Dear Sathya,

Keep one thing in mind, no fund will perform BEST forever. You have to be patience.

Thank you for the reply sir.

I invested money in SCSS account in IDBI bank as well in post office and SBI.

I filled 15H forms and hence no TDS is applied in P.O. and SBI for any quater.However IDBI deducts TDS from interest payable on 31 March and reverse it after my request application.Manager of IDBI told me that as interest is paid on 1st working day of April TDS is deducted.

Can you clarify this discrepancy ?

Abhaykumar-Yes, they are right.

please tell the interest calculation for NSC of 5 yrs – is it same 8.70 % (2017 year Rate) for all next 05 years or different for each years as per respective interest rate of that year.

Thanks & regards,

sunil kadam

email- [email protected]

Sunil-It will be fixed throughout the period at the rate which is applicable while you investing

Hi Basu,

Hope you will be fine.

Please advise that is there any TDS Deduction in KVP.

Thanks

Aswad-TDS (Tax Deducted at Source) will not apply for Kisan Vikas Patra or KVP.

I have invested one lakh under KVP (post office) , but now i need to cancel with in month, is this possible , the change am planing because of TDS to pay for the intrest. Pls advise what i can do to come out of this KVP.

Narasoji-Do you feel avoiding TDS means avoiding TAX??

Hi Basavaraj, Not exactly, I thought KVP is good for me ( my salary is 40K) to show the tax exemption under 80C and no tax will deduct on the interest i get from this plan after maturity (TDS) but now i got to know there is no tax saving with this KVP, now want to exit from this to look for better plan to invest. (last week only opend this KVP in post office)

Narasoji-You are allowed to withdraw it after 30 months ONLY.

if I withdraw after 30 months will be get the interest on my investment or , Can i transfer this KVP to my brother ?

Narasoji-Yes, you will get interest up to 30 months. No, you can’t transfer it to your brother.

Hi Basu,

I have been investing money monthly 1000/- each in below funds.

1) HDFC mid-cap growth –Direct

2) HDFC Balanced fund-Direct

3) ICICI pru chip large cap -Direct

I do not have knowledge in share market, but i would like to start invest in share market/stock exchange.

Please suggest me

Karthik-Without knowing the goals and timeframe, it is hard for me to guide.

Hello Basu,

I opened SSA in SBI, I added account to beneficiary so that I can make online contribution from my savings account , but to my surprise I found receipt which is generated is ppf receipt? From bank I got normal passbook not the pink SSA passbook! Can you please tell is it normal?

Ankit-You have to contact the bank. I am not aware of how they are managing this account.

I confirmed with SBI Bank, they treat SSA transaction as PPF transaction. So online receipt which is generated will be a PPF receipt. But passbook will show it is a SSA account.

Ankit-I think they not yet set up the system to generate SSA receipt.

Hi basu, Finally I feel that I have found a knowledgable, relaible person who can actually help. Please help me with this issue.

I am 26, 1st month in my job, in 30% tax bracket. parents are dependent on me. father doesn’t have taxable income(no epf, no ppf, no pension, no savings). they are fully dependent on me.

1. In which scheme I can invest to provide them a steady income every month/quarter?

2. How much Do I have to invest to get 10K/month for them?

3. Is axis income fund(G) and DSP income oppportunity fund (G) good options or MIS/SCSS?

TIA

Saikat-Why you need constant income? If your parents depend on you then whether you invested in one’s emergencies like life, health and accidental isnruance?

Hi Basu,

I need your help regarding my father’s investment, he was retired at March 2015 at age 58 but govt. of India & ITI (sick psu) giving his retirement fund by 2nd week of May 2016. His total corpus is 29 lacs (23 lacs as PF & 6 lacs from gratuity).As his age is 59 so he is not eligible Senior Citizen scheme.

I would be grateful please provide investment tips so he could get monthly income.

Some of the concerns & inputs are as follows:

a) As interest are decreases sharply and in future chances are there chances of more cuts, so he doesn’t wants to take risk now he needs safe and monthly income from interest.

b) Monthly expenses he needed atleast 30k per month. (25k for expenses & 5k for saving).

c) Other source income are

1) Getting pension Rs 2400 per month.

2) Getting Rent 5000 per month.

Some of the queries are:

1) Where to invest and what is best option to get the better interest return?

2) Our focus is more for senior citizen scheme available in market as interest rate is higher than and after 6 months he would be in senior citizen category as of now we think to invest in bank FD, Is it is a right decision?

3) Like MIS in post office/banks is Mutual Fund MIP is good to invest and as compared to bank/post office which gives higher return in short term and do this scheme giving monthly interest.

4) Investing in Non-Convertible Debentures (NCD), is this investment give better monthly income. (I don’t know anything about it just heard from someone)

5) Where to invest 5k in MF via SIP or 3k in MF and 2k in banks.

Fund selected: HDFC or Tata Balanced Fund

6) How much money to put for emergency fund 1.5 lacs or more please suggest?

Request you to please provide your input on the above query and which will help us to create a path for next upcoming few years. You had always guide me every time when i needed thanks for support :), as requested in below post of mine the day has come for which i am waiting for so long.

Thanks,

Shalabh

Shalabh-1) Nothing is safe now.

2) Better decision to go for SCSS once he will be eligible.

3) Mutual Fund MIPs comes with bit of equity exposure and monthly income is not fixed.

4) Riskier as company ratings may fall and end up in default risk. Hence, try to avoid such NCD. To extent you can invest in secured NCDs but not unsecured.

5) Without knowing timeframe it is hard for me to guide.

6) Ideally it should be 6-12 months of household expenses. If it is for your father, include additional surplus as health emergencies.

Hi Basu,

Thanks for your input it was really helpful.

For point 2) any other options apart from SCSS.

For point 5 ) time limit is 5 years and looking for balanced fund.

Thank you so much sir.

Thanks,

Shalabh

Shalabh-If your expectation is constant cash flow from investment, then stick to SCSS only. If your timeframe is just 5 years, then stay away from any equity funds.

Thanks Basu 🙂

Hi Basu,

I request you to kindly share your thought on your blog regarding senior citizen, so they could get better investment return, as in India we had a bigger section of people rely only on interest after their retirement and we know interest rate will fluctuate in the future.

I had seen lots of people in your blog are raising their concerns on senior citizen scheme as they are now worried about the returns after interest rate cut.

I request you please provide us some useful information about them & explore the different options for investment and there risk factor.

Thanks,

Shalabh

Shalabh-I understand your concern and thanks for providing inputs. Definitely I will write a post on this.

Thanks Basu looking forward for your post.

Is it correct that the deposits made in Senior Citizens Savings Scheme on or before 31/03/2016 will earn 9.3 % for next five years and proposed quarterly revision in interest rate is not applicable to the deposits made before its April 2016?

Kundapur-YES, you are right.

What happens to the investment that was done in SCSS before April first?????????. Will they get 9.3% or 8.6% in future??? Kindly reply.

Rajesh-No doubt, it will fetch you 9.3% return.

Sir, does it mean if I invest an amount before 31st march in SCSS I would get the return of 9.3% for next five years (i.e till maturity) or will it change as per revision similar to PPF??

PKpadhy-It will be 9.3%.

Dear Basu,

Since they have revised the interest rates of PPF ,is it good to invest more amount in PPF,your advice ???

Sethurajan-Considering this as debt product and the tax benefits, I suggest you to invest in this product.

what bout if someone invest today in sr citizen scheme ( before 1 april) ,it is also affected by rate change in every qtr or if we start same on or after 1 aprilwill bear the risk of qtry rate change pls comment as my banker told me if i invest today than it will be not afftected by qtr future rate flactualtion

Sir , as govt will review small savings schemes rates quaterly. I want to know about post office monthly income scheme (MIS) which is 5 years.

If i invest in MIS in April 2016 , i will get 7.8% for 5 years tenure or till June and next quarter July to September according to new revised rates as declared by govt.

Kindly clarify.

TechGuy-It changes on quarterly base. Exactly like earlier PPF used to be on yearly base.

Dear Basu,

Thanks for excellent article so far. I need your recommendation for investment. My age is 33. I can invest 3 lakhs per annum for next 20 years

and happy to take moderate risk. Please suggest me good investment options.

I am currently investing 1.5 lakhs per annum in PPF.I dont have any insurance or LIC policies. As I mentioned I do investment only in PPF hence

expecting advise from you other than PPF.

Thanks

Prasanna-First buy online term insurance to the tune of 15-20 times of your yearly income. Second, whether this Rs.3 lakh is apart from Rs.1.5 lakh PPF investment or it is part of it? Please clear my doubt to guide you in better way.

Dear Basu,

The 3 lakhs rupees is in additional to the existing my PPF investment. I have term insurance with my organisation which cover 10 times of my annual package and medical insurance for 7 lakhs, both this insurance are not valid if I quit the job.

Thanks

Prasanna

Prasanna-I suggest you to use equity and debt in ratio of 70:30. Equity funds are listed at my post “Top 10 Best SIP Mutual Funds to invest in India in 2016“.

Not an impressive response., but thanks.

Prasanna-Everything can’t be handheld. You have to understand the limitation of commenting and responding. I can’t do the financial planning with mere two lines sharing from your end. I think you got answer to what you asked. My intention is not to give you readymade answer. But make you to think on it. At the end of the day you have to learn and start investing on your OWN.

As the nation is developing, the interest rates on this types of products definitely reduces. It is expected.

If you see in any developed country, we need to pay money to the banks, if we want to save money in the banks.

The nation is developing meanings, inflation rate should be low, interest on this type of products will also be low.

Mani-A reality which we all have to adjust 🙂 Thanks for your positive views.

Is this applicable to previous deposits done? One of my friend did the KVP for X amount for 8.7% in this month, POST OFFICE assured him amount will get doubled by 8 years 2 months.

Ravi-No change in his earlier deposits. No need to worry.

Dear basu,

“Super like” ? your approach

“?” Character is auto printed when I posted above my comment with special emogy.

Please ignore question mark character.

Anup-It’s alright 🙂

Anup-I already aired my view.

But in reality we are not seeing any impact of reduced inflation.. Our expenses are still the same/more when the inflation was in double digits.

According to me there is no real economics behind inflation, its just a myth.

And this govt has started to dig its own grave much before next elections.

Raghu-Inflation is not MYTH, but the way it is calculated is YES…a BIG MYTH. Don’t blame it on this Government. Because even if other party also at ruling, they have to do this long pending change. We just have to accept it.

Govt should at least keep PPF& senior citizen savings scheme unchanged. The former is one of the most popular and lakhs of small investors have deposited their hard earned money in it while the latter is a social scheme. Unlike govt employees who have generous pension & medical help post retirement, the senior citizens have only such schemes like SCSS, for earning regular income in their sunset years.

Sreekumar-Forget about keeping the rate same, but from now onward it changes on quarterly base. This is hard to digest those senior citizens who are completely dependent on such schemes.

Dear Basu,

* For Senior citizens

What should be the approach of investment ?

Dear Basu- Any input ??

Anup-If the corpus is suffice to survive with debt category investments like LIC’s Jeevan Suraksha or SCSS, then no need to take headache and invest it right away. However, the corpus is not suffice, then we have to use bucket theory to build a corpus (Pattu created a calculator for it).

Basu- Great. Thank you.