Recently RBI announced to launch Inflation Indexed National Saving Securities (IINSS-C) which are entirely a new product to Indian retail investors or to Bank FD savvy investors. So let us look at its features and feasibility.

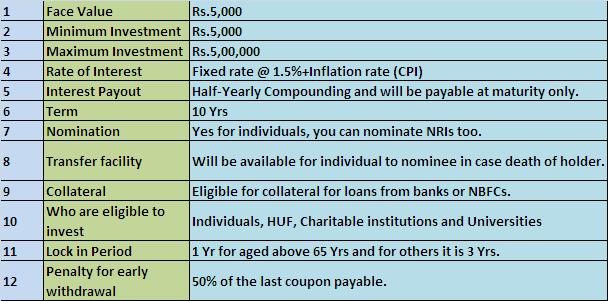

These bonds will be available for retail investors from the second half of Dec 2013. Banks are eligible for sale these bonds. So there is no hurdle for retail investors for investment. In this bond interest will not be fixed. Also interest will consists of two parts. One is fixed rate @ 1.5% above CPI and another is inflation rate based on CPI (Consumer Price Index). So suppose CPI inflation is at 10% then this bond will fetch you 11.5% return (fixed rate (1.5%)+CPI rate (10%)=11.5%.)

Inflation according to RBI will be considered as “final combined CPI will be used as reference CPI with a lag of three months (i.e. final combined CPI for September 2013 would be reference CPI for all days of December 2013). In case of change in the base year, the base splicing method will be used.”. Hope few may get confused as of now (even me too), but you may presume that this inflation rate will be somewhere between WPI (Wholesale Price Index) and actual CPI.

Previously RBI started issuing inflation indexed bonds based on WPI (whole sale price index). But in reality our day to day inflation is much closer to CPI. So to make more attractive RBI come up with CPI based bonds. Below are the few features of the said bond.

Who can invest?

Well, considering the current high inflation rate this bond may look attractive and may actually fetch you more than Bank FDs. But in reality interest rate will be always fluctuating and when the inflation rate comes down then the same bond may lose its sheen. But this is one among the safest investment avenue. So for those who are totally risk averse may definitely look for it.

Also bear in mind that there will be lock in for this bond. Hence based on your requirement invest. In case of early withdrawal there is a penalty clause of 50% of the last coupon payable. If we consider the current CPI rate at 10% then the actual return of this bond will be 11.5% which is more than any Bank FD rate. Also as compounding being half yearly it will give more yield than this above quoted 11.5% at the end.

Regarding taxation, I am still confused. Because few claiming it as a interest is yearly taxable like NSC but no TDS. But few claiming that it will be taxed as per capital gains tax rules like with indexation 20% and without indexation 10%. If it is a second case then it will be attractive. Let us see in future about the tax treatment of the same.

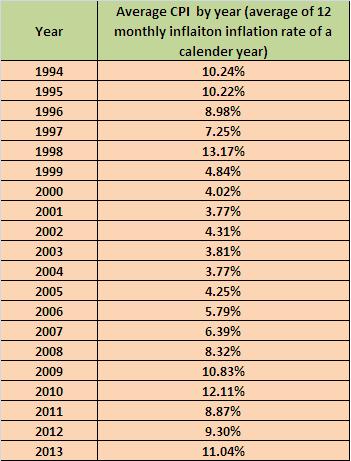

Below is the last 10 year average CPI date, which I think will give you some idea how the inflation is moving year on year (Source: inflation.eu).

So to simplify about this bond-Safety, interest rate will be floating based on CPI, high yield when inflation is higher, low liquidity and better tax advantage than bank FDs.

Hello Sir,

Is it a good option to invest in it? As the return amount is taxable.

I’m little confuse on like this product which return is taxable that means it saying like FD with higher return % and at last we get lesser. How we decide to choose like this product.

Thanks,

Anshu-If your requirement meets this plan then go ahead.

Hi Basu !

IIFL is going to launch a Home Bonds on 12th December ’13 on 12.15% interest p.a. can you give me some tips on that..

It looks good but i need your opinion..

is it good to buy ?

Parthiv-Yield they show as 12.15% but the interest rate is 11.52% also this is taxable. It does not mean that no TDS means no tax. But I need to verify in detail. Also if it matches your financial goal then you can try.

Hi Basu !

IIFL is going to launch a Home Bonds on 12th December ’13 on 12.15% interest p.a. can you give me some tips on that..

It looks good but i need your opinion..

is it good to buy ?

Please inform whether interest for the 3rd year will calculated on the basis of cumulative CPI index from 1st year or each year interest will be calculated on each year CPI separately.

Sarawagi-Each year interest will separate based on the CPI.

I may be getting into too much of detail at this stage. But would like to know more about taxation part of it. If I have a 3 year FD with cumulative option, then although interest is paid at the end of 3 years, every year i need to pay tax on the accrued interest. Bank sends a letter with this accrued interest details. Will I get the same from this IINSS as well? Since my AY 2008-09 tax returns have still not been sorted by income tax dept for not showing accrued interest, I am a bit picky here. It is difficult for us to calculate it since we will not know the exact CPI number.

Bhushan-It is yet to launch product with only few fine prints available to know. So I am unable to comment at this stage. I think they will send as is the case with FDs. But not sure.