IRDA recently published the Annual Report for FY 2018-19. Let us find out the Health Insurance Incurred Claim Settlement Ratio 2018-19 and how to arrive at the best health insurance companies selection.

What is the meaning of the Incurred Claim Ratio or ICR?

Incurred Claim Ratio or ICR is a ratio of the total value of claims paid or settled to the total premium collected in any given year. This can be calculated as an Incurred Claim Ratio or ICR=(Total Value of Claims Paid/Total Premiums collected)*100.

For example, let us say Company ABC settled the total claim amount of Rs.90 Cr in the year 2018-19. In the same year, it collected Rs.100 Cr as a total premium. In this situation, the incurred ratio stands to be 90%.

This Incurred Claim Ratio is applicable only to non-life insurance companies. For life insurance companies, IRDA publishes Claim Settlement Ratio. I have already written a post on the same. You can refer it at “IRDA Claim Settlement Ratio 2018-19 | Best Life Insurance Company in 2020“.

What to judge from the Incurred Claim Ratio or ICR?

This is one of the criteria to identify the financial health of non-life insurance companies.

# Incurred Claim Ratio or ICR more than 100%

It indicates that for every Rs.100 they collecting as premium, they are paying more than Rs.100 as a claim for a year. In simple terms, your income is Rs.100 but your expenses are Rs.100 or more. So instead of profit, they are into a loss.

# Incurred Claim Ratio or ICR less than 100%

It indicates that for every Rs.100 they collecting as premium, they are paying less than Rs.100 as a claim for a year. Such companies are making a profit as your income is Rs.100 but expenses are less than Rs.100.

What it indicates that less ICR means the company is in profit or eyeing on profit. So either they may insure the less risky individuals or groups (customers rarely come forward for a claim) or rejecting the claims just to profit.

However, rejecting claims only on grounds to profit will not work out for any company. They have to look for reputation, future growth, and regular guidelines. Hence, simply for the sake of profit-making, they can’t deny claims.

In my view, going with companies of high ICR or low ICR is risky. Hence, always choose a company which is in between both these points.

Remember once again, ICR is not the main criterion in selecting health insurance. However, it is one of many criteria.

# Incurred Claim Ratio or ICR less than 40%

This indicates that either the company is charging higher premium rates than its peers and making a considerable profit or the insured individuals are low risks (probability of hospitalization is less).

Difference between Claim Settlement Ratio and Incurred Claim Ratio

Incurred claim ratio applies to general insurance companies. It is a ratio of the total premium collected to the total claim amount paid within a financial year. Whereas, the claim settlement ratio applies to Life Insurance Companies. It is the ratio of claims approved to total claims received.

Health Insurance Incurred Claim Settlement Ratio 2018-19 | Best Health Insurance Companies 2020

Now let us concentrate on IRDA’s Annual Report for 2018-19. We will check the IRDA Incurred Claim Ratio 2016-17 and identify which is the Best Health Insurance Company in 2020 in India.

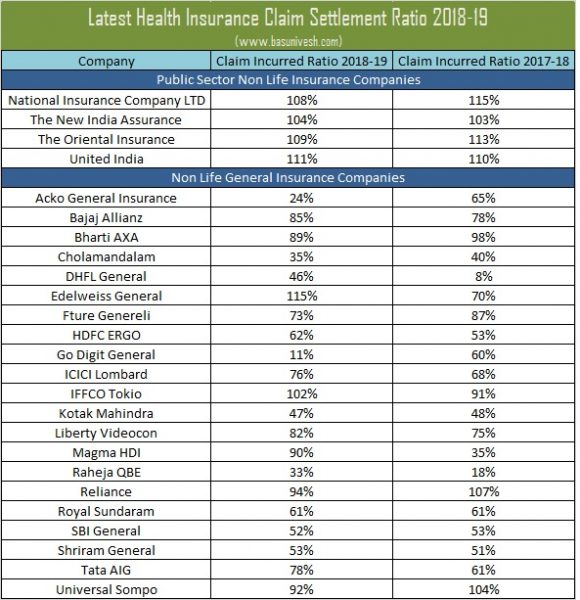

Here, I will divide the health insurance companies into 3 categories. One as public sector companies, second as private companies and the third one as standalone health insurance companies.

You notice that all the public sector health insurance companies incurred claim settlement ratio is more than 100%. This indicates that they are under the loss.

However, the private sector general insurance companies incurred claim settlement ratio ranges from 24% to 115%.

The average Incurred Claim settlement for public sector is 109.86% At the same time, for private sector health insurance companies it is 76%

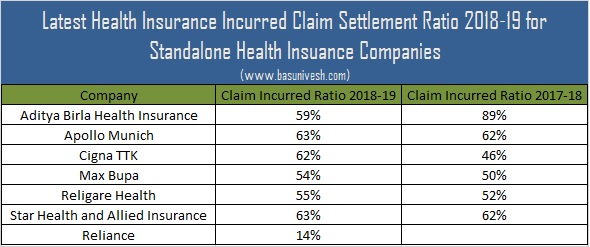

Now let us look at the incurred claim settlement ratio for standalone health insurance companies.

The average incurred claim settlement ratio for standalone health insurance is around 61%. This is a healthy sign.

Best Health Insurance Companies for 2020

Is it wise to choose a product based on the ICR? It is completely wrong. ICR or Incurred Claim Ratio will give an indication of the financial status of companies. Hence, BLINDLY following this ICR for the sake of buying a health insurance product is a MYTH.

Especially in case of buying health insurance, you have to verify the features. Hence, let me give you a glimpse of how to choose the product.

Best Health Insurance in India in 2020 -Checklist to shortlist the product

Let us move forward and identify the points before selecting the health insurance.

# Coverage Amount-Concentrate on Sum Insured and think beyond the current hospitalization expenses. If premium costing you more, then fill the gap with the super top-up plans.

# Day Care Treatment-Many diseases nowadays turned to be day care treatment. Hence, opt for a product which offers you maximum number of day care treatments.

# Buy early-Buying at the earlier age is best than postponing it. We don’t know the health issues. Hence, the insurer may reject your proposal. Hence, always buy immediately and never postpone.

# Understand the cover-Identify the features you want to cover. Covering all NOT POSSIBLE. Hence, try to identify the product which covers many illnesses.

#Individual or Family Floater-Decide whether you want to go for individual or family floater. It is always best to go for an individual if the age of any one member of the family is so high than the others. For example, in a family of 4 the oldest person’s age is 65 years and rest of other 3 members age is less than 50 years, then better to buy an individual plan for that 65 years old individual and rest 3 members can buy a family floater.

Because the premium is fixed based on the age of oldest person also.

# Entry Age and renewable clause-Check the entry age and for how long one can renew it. Usually, nowadays all plans offer you lifetime renewal.

# Identify the company which covers existing diseases at early. Usually, all insurance companies have a waiting period 3-4 years for existing diseases. However, if your concern is to cover the existing diseases, then give first priority to this point.

# Check for room rent capping. Avoid the product which restrict you with room rent capping.

# Check for the co-payment clause. Higher the co-payment means lower the premium for you. Co-payment means how much you also have to pay in a total bill. If the co-payment clause states 20% co-payment, then for all bills claimed, you have to 20% and the rest 80% will be payable by health insurance company.

# Check for exclusions. If you feel the exclusions listed may be uncomfortable to you, then skip that product.

# Check for hospital network availability in your city or town. The cashless hospital benefit is better than producing the bills and waiting for claim settlement.

# Read carefully the wordings of policy brochure. If you have doubts on any feature, then try to clarify it NOW itself.

# Avoid all common features, which companies try to highlight.

# Check for No Claim Bonus company offers.

# Check treatment wise limit if any.

# Check the premium rates. Especially check the rates for older age rates as few insurers jump the rate drastically for older age coverage.

# Finally, if you feel the sum insured you opting is not within your budget, then go for sum insured according to your affordability and opt for a super top up plans.

Hope this much information is enough for you in shortlisting the health insurance product.

Hi Sir,

Can you share your views about future Generali health insurance and it’sustainability because I find this policy covers all my needs…

Can you share lasted data about icr and claim settlement ratio of all health insurance with breakup like for group insurance…floater and individual

Dear Nandini,

I usually stay away from the new entrants. However, if your requirements are meeting with the product, then go ahead. The above data is the latest data what IRDA provided.

Dear Basuraj, How about the Manipal cigna medical insurance company what the claim settlements ration. can you share me pl

Dear Ajay,

The ratio is available in the above post.

Hi Basavraj,

I have an Insurance cover of 5 Lac from my employer. I wish to increase the cover to 10/15 Lac. Should I go for a Super Top-up plan of lets say 10/15 Lacs with 5 Lac deductible. Please suggest.

Dear Anshum,

As the base cover is from employer and uncertainty always there, I suggest your own base plan and super top up.

Dear Basavraj,

Thanks a lot. Can you please suggest whether I should go for Optima restore 10 Lac base plan or 5 Lac Base + 20 Lac Super Top-up. Both have similar premium. In fact I do not understand why the premium is charged low in Super Top Up compared to increase in Base Plan. Is there any difference in facilities.

Dear Anshuman,

Go for 5 lakh base+Rs.20 lakh super top up.

Hi sir,

I have a coperate family floater plan for 5 lakh. For which I pay 14000 premium.

I am planning to buy a family plan for my family apart from the coperate plan. Is this a good idea

Dear Avinash,

It is not only a good idea but the BEST idea.

WHICH IS BEST HEALTH INSURENSE

Dear Vikas,

Refer above post properly.

Sir I am having Star family health Optima policy. I am paying premium as per zone 3, as it is my hometown but I am living in zone 1 Delhi. Do I will face any problem during claim.

Dear Rajiv,

I don’t think so.

its does not matter, where are you living.

Please check the below plan and let me know what you think. Thanks again.

I am 35 years old. Combined income with husband is 2 lakh. Investment are like below. Need to generate wealth of 3 cr by next 25 years.

Investing in 10,000 schemes in each scheme.

Kotak Emerging Equity Scheme – Mid Cap

Reliance small cap – small cap –

Parag parikh long term equity – multi cap

SBI bluechip – large cap

Aditya birla sunlife front line equity -large cap

Started SIP 9 years back and stopped 2 yrs back Reliance Value Fund. Since I got 9% return for now waiting to transfer or redeem.

Also, doing the below investment

1 lakh in NPS – one time10,000/month in PPF50,000 a year in NPS 5,000 per month in RD

2 lakh in post office month scheme – one time

Have 2,00,000 FD for emergency. Have enough health and life insurance.

Please advice on my financial state right now and advice changes. Appreciate the help.

Dear Richa,

Financial Planning guidance can’t be done with mere few lines of your sharing. It is more harmful for you than me.

Dear sir, my age 42, wife 35and son 8 , looking for family health Insurance for 5-7.5 lac coverage, please suggest a plan. Thanks n regards Arunava.

Dear Arunava,

Refer my post “Top 5 Best Health Insurance Plans in India 2020“.

Hi Basavaraj,

My friend is looking for a health insurance but he is confused if he should go with private or public sector policy… reason is he worried is because he had smoking history 5 years ago. However he doesn’t smoke now and do not have any heath issues could you please suggest which type (Public / Private) policy he should go with? he is thinking going with public sector policy will be safer. but he is not sure. Please help with your suggestion.

Dear Anugrah,

If you are hiding the facts, then whether it is PUBLIC sector or PRIVATE sector, both are RISKY. Choose the product based on your requirement than defining like public or private sector.

No, i am not hiding any fact. i personally availed health insurance benefit from both companies, public and private sector for me and my one family member in my two previous companies under corporate insurance policy. our concern here is which once is more better for a person who had smoking / drinking history considering he / she doesn’t have any existing health issue.

Dear Anugrah,

All are equally good and bad.

What about star health insurance ?

Dear Arun,

Refer above post properly.

Hello. How is Acko and Digit able to keep the ICR at 24 and 11% respectively?

Dear Leshan,

There may be two reasons. One is that their customers are young enough where the probability of hospitalization is rare. Because of which they are able to be under such a profit. The second one maybe rejection. Hard to say as the data will not specify the reasons.

I have my mediclaim floater policy in New India Assurance with SA 3Lakhs for 7 years.I want to port to Star Health now.Will it be wise for me .Please suggest.

Dear Pradip,

Why you felt to part it?

I want to port from New India to Star Insurance co. because later company gives 25% bonus of sum assured in case of no claim year.

Dear Pradip,

Stay away from such fancy offers.

Isn’t there any advantage in this offer? Please explain….

Dear Pradip,

Nothing such.