Many of us eager to start early, invest early, ready to invest in BEST products from whatever the lump sum every month available. But we don’t know what are our financial goals, we don’t know the time horizon of the goals and we don’t know the cost of the goals.

Hence, before jumping into investing it is a must for all of us to identify our financial goals. Once you have the clarity about your financial goals, then identifying the asset class and the products are not so tough. Because you know what you want from each rupee you are investing.

From the start of this profession since 6+ years, one thing I understood was that 99.99% of investors don’t know why they are investing, when they need money, and what are their target amount. Instead, among 99.99% of unknown investors, the majority of them are investing to save tax, earn more than Bank FDs or terribly messed with Life Insurance products.

The major requirement of any investing is GOALS. This is where they are messed up with. They don’t know how to identify, they don’t know whether they are NEED or WANT, they don’t know how much they need and when they need.

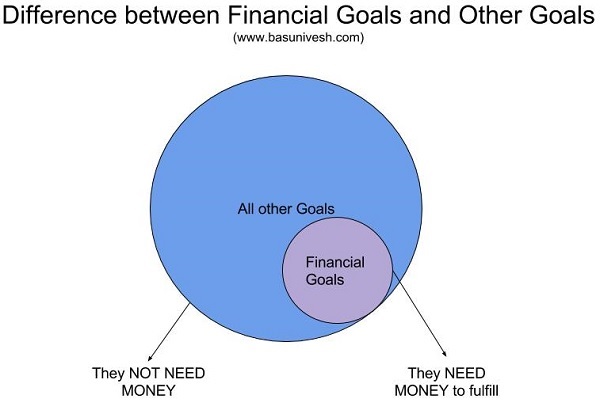

Difference between Financial Goals and Other Goals

How to differentiate between your financial goals and other goals is the biggest doubt for many of us. There are goals like your professional goals, personal goals, financial goals or health goals. Then how to identify which is your financial goal? Let me explain the same with this below image.

You notice that Financial Goals are also the part of your life’s goals. However, the difference between your other goals to financial goals is that in case of other goals you may not need MONEY. But you may need something different like to reach any level of your professional life, you need knowledge update or commitment to learn.

However, in case of financial goals, to meet those goals, you need MONEY.

Difference between NEED and WANT

Now you understood from above image that what are financial goals. But do keep in mind that all goals which require money can’t be tagged as financial goals are wealth creation goals.

Hence, before setting the financial goals, you must understand whether that goal is NEED or WANT. Need is something which is very much required. NEED can’t be postponed or such goals can’t be canceled. For example, goals like your kid’s education or your retirement.

However, there are few goals which are WANT but few feel them as NEED. Goals like vacation, car, BIG HOUSE or international vacation.

I am not saying that you must ONLY have NEED based goals and not enjoy your life. But the priority should be first towards the goals which are very much SURE TO COME in your life.

Hence, list down the goals yourself which are the need and which are want.

Prioritize Financial Goals

Once you listed your financial goals, the next step is to prioritize the financial goals. For example, the emergency fund creation must be your high priority goal than upgrading your car.

Prioritizing your goals makes you understand that what is MOST important for you for your investment.

Time horizon of Financial Goals

Next is to understand the tenure of each financial goals and difference between each goal. Do remember that goals which are less than 5 years are short-term goals. Goals which are more than 5 years to 10 years are medium-term goals. Goals which are more than 10 years goals are long-term goals.

This differentiation is as per my knowledge. However, others may differ from my views.

Cost of Financial Goals in today’s term

The next step is to identify the cost of such goals in today’s term. Why today’s term is because you know the current cost of such goals. Hence, it is for you to identify the goal cost.

If you are unaware of the current cost or the trend of such goal costs, then search for an expert and identify the cost of goals.

Remember one thing that you are just assuming the approximate cost in today’s term. Hence, better to buffer some higher figure than the actual current cost.

Inflation to each Financial Goals

Once you identified the cost of such financial goals, then the next step is to identify the inflation rate applicable to such goals. Remember one thing that inflation rate must not be same for all goals. It varies based on the goal type and the socio-economic scenarios.

Hence, judge this rate also wisely. Underestimating inflation may harm you badly. At the same time, considering higher inflation rate may make you to feel fear and may not be possible for you start the goal itself.

Hence, judging the right inflation rate or the nearest inflation rate is the biggest task you have to think.

Once you understand the current cost and inflation to each such goals, then you will arrive at the future value of such goals. Based on this future value you have to now identify the monthly investment requirement.

Asset Allocation to Financial Goals

Once you have the list of goals, prioritized them, know the current values and inflation rates, then the next step is to choose the asset class for each goal.

As per me, if your goal is less than 5 years, then stick to debt only. Here, debt in the sense not ONLY debt funds, it may be FDs, RDs or any other asset which may be secured in nature.

If your goal is a midterm in range like between 6 to 10 years, then the asset allocation between debt and equity should be at 40:60.

If your goal is more than 10 years, then the asset allocation between debt and equity should be 30:70.

Again I am saying, this is not the universal standard. It may vary based on individual planners or individual investors views. However, I follow this way of investment.

Return Expectation from each asset class

Next and the biggest step is the return expectation from each asset class. For equity, you can expect around 10% to 12% return. For debt, you can expect around 7% return expectation.

When your expectations are defined, then there is less probability of deviating or taking knee-jerk reactions to the volatility.

Portfolio Return Expectation for each financial goals

Once you understand how much is your return expectation from each asset class, then the next step is to identify the return expectation from the portfolio.

Let us say you defined the asset allocation of debt:equity as 30:70. Return expectation from debt is 7% and equity is 10%, then the overall portfolio return expectation is as below.

(70% x 10%) + (30% x 7%)=9.1%.

How much to invest?

Once the goals are defined with target amount, asset allocations are done, return expectation from each asset class is defined, then the final step is to identify the amount to invest each month.

There are two ways to do. One is constant monthly investment throughout the goal period. Second is increasing some fixed % each year up to the goal period. Such option is called a step-up option. Decide which suits best to you.

Once you do all these steps on your own and finally arrived at the monthly investment requirement, then the final option is to choose the products.

Now while investing in products, you may think of tax efficient products also so that you may save tax also.

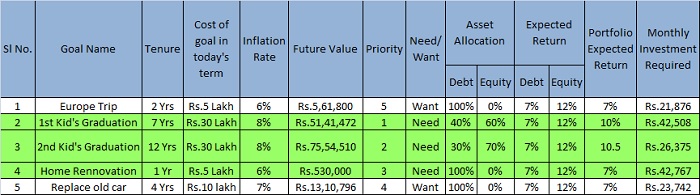

Finally, the work out of all those steps may look like below for you.

Note-The first priority should be to need-based goals and then wants.

Review of investment

Once you started investment, it does not mean that you be silent throughout the goal period. Because you must review whether the assets or products are generating the desired returns or not. If not generating the desired returns, then identify what are the reasons.

Reviewing once in a year is a must. Also, following the asset allocation as pre-defined will makes you protect from the uncertainties.

Conclusion:-I used to repeat this always “ALL PRODUCTS ARE EQUALLY BEST AND WORST”. But it is YOU, who has to choose the asset and product based on your requirements.

Hi,

article is very informative and thanks for sharing it.

I have below questions:

1. For emergency funds, can you share some idea on what basis I should find or how I arrive at cost of emergency fund required for me in today’s scenario? What should be inflation rate?

2. According to me Emergency fund is something which should be ready right away but if it’s not then in how much tenure it should be built?

3. Once the Emergency fund amount is ready where it should be parked? like FD, RD or any other instrument?

Dear Sangram,

1) It should be your household expenses, mandatory expenses like EMI or Insurance premiums and any other such obligatory expenses (like child education fee and all). For an emergency fund, inflation is not required as it is considered based on current expenses. However, you have to increase your emergency fund slowly to match the expenses.

2) Yes. You must have at first.

3) Usually the parking should be where you have instant liquidity option.

Hi,

very informative post, thanks.

I am a conservative investor, currently my portfolio allocation is 20% Equity, 80% Debt.

My investment horizon is 10+ years. But still I cannot put all amount at once into equity, to make it 70% of the portfolio right?

I mean what if the current valuations are too high and I may risk losing a lot and if I invest all amount lumpsum now all at once.

How to deal with this issue?

Dear EB,

Conservative but holding 20:80 ratio of debt and equity for 10 years goal??? You have to reduce it to around 50:50. Why you look for valuations when you are doing proper asset allocation and also time horizon is more than 10+ years?

Currently

My allocation to debt is 80%

and allocation to Equity is 20%

That is why I said I am a conservative investor.

Actually, I am worried when I have to invest a large amount of money lumpsum into equity Mutual funds.

More so because the current market valuations are too high and if the market falls, I will be facing big losses in the short term. Which basically means even in 10 years of time, My portfolio return will stay below average.

I am more comfortable with investing in SIP, but cannot take the risk of investing all in one go in equity Mutual funds

Dear EB,

If you are concerned more about such few months or a year volatility, then stay away from equity. It is not meant for you. Also, if you have such fear, then spread your lump sum to around 6-12 months to enter equity.

Thanks 🙂

Hi Basvaraj,

Today i have read some of your articles really they are informative but still i am unable to choose the fund due to number of funds in the market

My Plan is i can invest 1000 per month for 10 years and my age 22, so could you please suggest 2 types of Funds

Thanks & Regards

Pavan Dodda

Dear Pavan,

You can start with equity oriented hybrid funds.

Hello Basu,

I want to create emergency corpus and want to to start SIP in Ultra Short Duration and Low Duration Fund. Can you please suggest 2 (one from each category is better or only one category will suffice?) such funds in which I can put 10K per month to build emergency fund.

Dear Kalyani,

For emergency corpus parking or creation, I suggest you to use Liquid Funds rather than any other types of debt funds.

Thanks Basu for your kind response.

Can you please suggest good 1 or 2 Liquid funds?

Dear Kalyani,

Do you investing in any equity funds? If so, let me know the AMCs names.

I am currently investing in SBI, HDFC, Reliance and ICICI AMC. And planning to take one from Motilal Oswal AMC but not sure yet.

Dear Kalyani,

Use ICICI Pru Liquid Fund.

Thanks Basu for your suggestion.

Hi Basu how are you !

Please can you share whar is the best debt product for NRI as they can not invest in PPF, Appreciate your advise

Investor-Refer my post about Best Debt Funds.

Hi Basavaraj,

The article is very good and throws light on various aspects that need to be addressed while doing financial goal setting. It’s indeed very informative and provides good guidance.

Based on my understanding from the article, I have attempted to work out my financial goals and have a few queries; Here are the details :

Total savings required to be done = Rs. 4 lacs / year (2 lakhs in Equity + 2 lakhs in Debt)

Time horizon = 12 yrs to 17 yrs (except one goal which is 8 years from now)

Plan for Investment in Debt = Rs. 2 lakhs total in Bank FDs / PPF (PPF is nearing maturity)

Plan for investment in equity = Rs. 2 lacs (say, Rs. 17,000/- per month SIP).

Questions :

1) Should I diversify my equity investment into all of the categories i.e. Large Cap, Mid-cap, Balanced and Small-cap?

2) If so, how much % investment into each category fund?

I am yet to begin building my portfolio and hence seeking your advise.

Best Regards

DR

DR-1) You have to.

2) You have no clarity with respect to goals. Hence, hard to guide properly.

Great article, Basavaraj. Can you please share your Excel file?

Sunand-Sure, I will in my continued second post. Please wait for next article.

Hi

I would like to know the inflation rate for purchasing flats/villas etc.Is there any way we can guess/calculate this according to city we live?

Vishnu-You can refer THIS.

Hi

I have started investing in last year. As of now my money is parked in the following instruments

ELSS (Franklin India Taxshied Direct Growth) : 100000 . (An SIP of 10000 is currently running till march 2018.)

Liquid Fund (HDFC Liquid Fund Direct Growth) : 150000

Savings Bank HDFC :130000

Holds’ 2 credit card : 150000 credit balance per month.

I’m earning monthly around 45000 and job is stable.Since I come from a upper middle class family, i have enough financial backup

in case of an emergency too.

My monthly expenses comes around 15000 per month including rent and everything.

As of now im yet to marry , and there is not much goals to accomplish currently. May be i will get married in 2 years.

So my current goal is maximum wealth creation.

In 2018 , im planning to continue invest in ELSS (around 120000 as SIP of 10000 each month).

1) Do i need to change from Franklin to any other fund for ELSS?

I dont see any chances of redeeming my Liquid funds soon.

2) Ideally i would like to limit my savings balance to a max of Rs 50000.Surplus cash above that can be invested in proper investments (Min 3 months to Max 1 year)

Please suggest me exact investment type for this.

Vishnu-Goal must have proper time horizon, expectation and the quantum of money required to achieve that goal. If these are not clear, then it is hard for me to guide BLINDLY.

Investment horizon : 1 Year

Goal : For Secondary emergency fund

Risk Profile : Moderate

Monthly : 10000 can be invested.

Vishnu-Use Liquid Funds.

I am investing in ICICI PRUDENTIAL NIFTY NEXT 50 every month with every dip for future purpose. My aim is to accumulate 100000 Units. Is it the right approach?

I hope after 10 to 15 years NAV touch 100 Rs. and after that, I will put the money in a Debt fund

Amit-Right or wrong depends on your time horizon and asset allocation you are following.

Thanks Basavaraj, What’s your opinion on Next fifty Index fund

Amit-I am more inclined towards active funds than index funds.

Dear Basu can u list out the benefits and demerits in investing in registered chit fund companies.

Rahul-Long back I wrote a post. Please refer “The Chit Fund Act 1982-Understand the law first“.

Basavaraj,

I have created my first goal for pooling the emergency fund with the information you provided in the post. Could you help me calculate the monthly investment required amount both with and without step-up option. I can increase 10% every consecutive year in case of step-up option.

Sl no goal name tenure cost of goal in today’s term inflation rate future value priority need/want asset allocation expected return portfolio expected return monthly investment required

debt equity debt equity

1 emergency fund 3 270000 6% 321575 1 need 100% 0% 7% 12% 7% ??

Vignesh-Use either simple compounding formula or online available step up compounding formula to arrive at the values.

hi Vignesh – does it mean that you need emergency fund after 3 years?

In my Personal opinion, one should keep the Emergency Fund in a way that it can be accessed even in the midnight hour. Preferably, e-FD/e-RD etc.

Shishir-The first priority should be for emergency goal. But he want to accumulate within 3 years. Let him workout with numbers and come back.

Thanks Basavaraj/Shishir. I checked for the calculators online. I would require to invest Rs. 7310/- monthly with step up 10% annually (or) Rs. 8010/- monthly without step up assuming 7% annual returns to achieve my emergency fund goal in 3 years.

But the liquid mutual funds like reliance treasury plan for direct growth gives approx 7.4% returns for 3 year period and that too they offer liquidity. Why should I go for debt fund? Instead can I invest in this liquid fund?

Vignesh-Liquid Funds are also considered as debt funds. Also, you can try Arbitrage Funds.

However, keeping other suggestion aside and to answer your query, per my calculator the MI req. is approx. 8000/-.

Hello BasuNivesh,

I’d like to invest in equity mutual funds for minimum 15 long years with 5k per month,can you please suggest which equity mutual fund is better for it?

Sathish-Refer my post “Top 10 Best SIP Mutual Funds to invest in India in 2018″.

Hi Basunivesh,

Are pension plans really good for oldage people??IF, so please mention few pension plans currently in india.

If not, please suggest some good plans to get a stable monthly income of 50 K per month for old people, as senior citizens savings scheme and other are taxable as well as they have limit upto 15 lacs ,with 15 lacs it is impossible to get pension or interest of 50K per month since we are planning for a peaceful life for parents..

Please suggest how to get 50K per month as pension in india

Srikanth-Sadly all such pension plans are taxable in the hand of retiree. If you are looking for stable income, then can check LIC’s Jeevan Akshay VI.

Hi Basu,

Nice to see your blogs. My in-laws are 65+ and are looking for the steady income source. They have some real estate investment which they are planning to liquidate sometime but that will depend on buyer availability etc.

They are looking for a monthly income of around 40k, which product and how much investment would be good.

I myself is well versed with financial product/risk and invested completely in equity. But which products would be good for them. They have not invested much in equity/mutual fund before but are willing to try.

They are doctors hence monthly income source is reducing hence they are looking for some replacement.

As per my understanding, they will have more funds when there real estate sell are done … hence I feel they can take little bit risk and put in the balanced mutual fund ( rather than liquid fund or pradhan mantra pension yojana etc ) What is your suggestion ? what are the schemes ?

I know sometimes SW (systematic withdrawal) will eat into principal but considering availability of funds through real estate exit.. would that be good investment

Thanks

Pankaj-Hard to guide anything with mere few lines of sharing. However, if they are primarily dependent on this income, then I don’t think balanced funds a good choice. Use complete debt products which offers fixed income to them.

Very informative post sir. Thanks…

Hi Mr. Joshi,

I would suggest combo of post office SR. Citizen scheme (15L+15L) + monthly income scheme(9.0L) and a debt mf. SR. Citizen scheme + MISS will ensure at least 20-25K pm for next 5 years. Rest they can invest in mf with varying return.

Further there is PNVY pension scheme of lic which ensures 5k pm for next 10yr. By investing (7.5L +7.5L)in the scheme you will ensure 10K pm.

Roughly you will earn 30-35k pm for next 10 years.

Hope your problem is addressed

Hi Basu,

I am using my EPF & VPF as my debt components and recently increased my VPF contribution to re balance my portfolio(Eq:Debt –>65:35), but latter I came to know that the EPF interest rates will be reduced for this year and authorities are planning to invest 15 per cent of its corpus in equities through exchange-traded funds. So this is again going like hybrid allocation in my opinion.

Kindly advise is it still okay to hold EPF/VPF as my debt components? or do you suggest any other alternate pure debt component ?

Hari-Hold and consider as Debt only.

Thanks Basu!

Hi Basu – Can you provide the Formula that you used? I am getting a higher number, when I entered the value as per your excel image.

Shishir-Is the value is too much different? Let me know the values you considered so that I too can try and answer.

Basu – There is no big difference, I am using Excel formulas.

As per your 1st e.g. “Europe Trip”, with ‘FV’ formula in Excel, I get future value as 563,580. and with ‘PMT’ formula I get monthly SIP amount as 21,945.

Do you also use Excel based Formula?

Shishir-I used financial calculator and that may be reason for slight difference

Thanks Basu – I have created my own Excel with this and mapped it with my current investments. It gives a fair !dea about the Gaps and action required to fill them.

Shishir-Great to know.

@Shishir – Can you share formula used for “Monthly investment required” ?

Vijayendran-It is nothing but compounding formula which is available in excel or there are many such calculators online.

Vijayendra – I used PMT function in Excel to calculate that.

Very good article ! Long way to go bro !

How did u arrive at monthly Installment

Manav-When you know the time, future value, expected return, then easily you can calculate the monthly installment.

Can you please share the XL template!

Anjan-I will update soon. But it is easy and you can personalize and create on your own also.

Thank you Basavaraj

very good information sir , thank you so much

Ganesh-Pleasure 🙂

Excellent. Why the inflation is different for various goals?

Saurabh-The inflation of education is different than the inflation rate of your car price. Hence, better to consider the inflation rate based on the goal.

Thank you.. Can you upload the excel file? or provide a Google Spreadsheet link, it will be useful for all of us.

Saurabh-Let me create one and share with you all. I just made an image using excel sheet. Let me create the detailed sheet.

Thank you .. appreciate your efforts