Can PPF make you Crorepati? How to become a crorepati with a PPF? Yes possible by investing and waiting for more than 20 years which is financially not worthy!!

Many of those who share content on how to become a crorepati with PPF are focused on emphasizing the concept of crore, leading them to overlook other crucial financial aspects. This can be highly misleading.

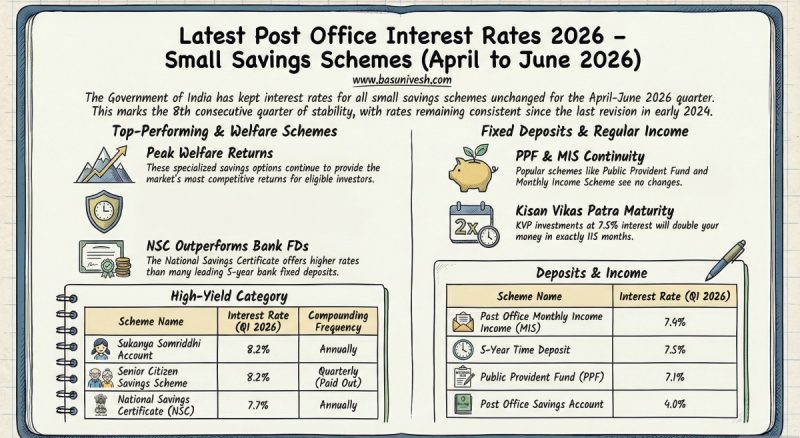

As you all know the maximum contribution one can make in a PPF account is Rs.1,50,000 a year. After 15 years, you can extend it for as many years as you wish in the block of 5 years. However, the interest rate of PPF will change on a quarterly basis. The current rate is 7.1% (Refer to the latest rate at “Post Office Savings Schemes Interest Rates July – Sept 2024“).

If you look into the historical interest rates of PPF, you will come to know the reality. In my earlier post, I mentioned this “Public Provident Fund PPF Interest Rate 2024 (History 1968 – 2024)“

You noticed that earlier it was at 7.5% and then touched the peak of around 80s period of 12% and after that it’s reducing continuously and now at 7.1%.

Therefore, basing our calculations on the assumption that PPF interest will stay consistent and determining whether PPF will lead to us becoming crorepati or not is the primary and most significant flaw in this information.

Another disadvantage of this calculation is that it will require around 20 years to accumulate a crore, given a current interest rate of 7.1% and an annual contribution of Rs.1,50,000 (the maximum permitted). It could take approximately 18 years to accumulate one crore rupees if we consider having two PPF accounts, one for oneself and one for the spouse.

For the sake of simplification, let’s consider an inflation rate of 7% and a 20-year term to reach one crore. In this scenario, the value of Rs.1 Cr after 20 years would be approximately Rs.25 lakh in today’s term. However, if we assume a 6% inflation rate, the current value would be around Rs.31 lakh. Despite us perceiving Rs.1 Cr as a significant amount, inflation diminishes the worth of today’s hypothetical one crore over a span of 20 years.

Many individuals tend to overlook the practicalities when envisioning a sum of one crore. Achieving the one crore milestone is feasible through methods such as maintaining the funds in a savings account (with an interest rate of approximately 3% to 4%), investing in a PPF (for a duration of 20 years), or engaging in the equity market. The crucial factors to consider are the duration required to reach the one crore milestone, the actual value of that sum adjusted for inflation, and whether it holds significance at that particular juncture. Rather than indulging in a vague aspiration for one crore, it is imperative to address these pertinent questions.

Simultaneously, I acknowledge the significance of PPF. It stands as one of the finest debt products available. Nevertheless, my main argument is that, in order to combat inflation and reach your financial objectives, relying solely on PPF is inadequate. Including equity in your portfolio is essential. However, if you are averse to the risks associated with equity, the alternative is to increase your investment, as avoiding risk comes at a cost.

Conclusion – Achieving a target of one crore through PPF may seem appealing, but it comes with interest rate and inflation risks. To mitigate these risks, one could consider taking a calculated risk by investing in equity or increasing investments in PPF. Unfortunately, the annual limit of Rs.1,50,000 for PPF means that reaching the one crore mark will take a considerable amount of time, potentially leading to the devaluation of money.

Basu, Not so fast.

You are forgetting that a couple can achieve this in half time if both are contributing to their respective PPFs.

Take this case in consideration.

Dear Joy,

I can understand that it can be possible at the same time the cost of investment will also double than what I have considered right?

Basavaraj, My long time belief is busted by your analysis.

Dear Pradeep,

Ha ha…I am firm believer of PPF. But relying on this single product is dangerous.