Today Finance Minister presented the Budget 2016. There was a lot of news, noise and many MAYs around the groups, media, and experts. Now all of them hope silenced 🙂

Let us see the major changes.

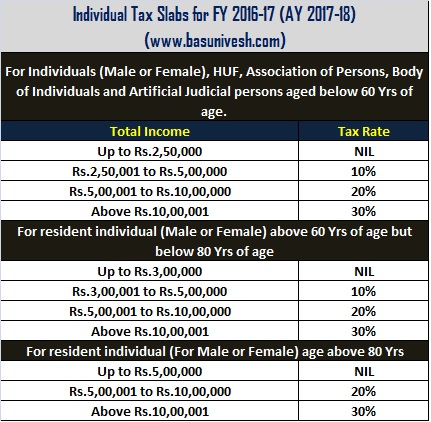

1) There is no Change in your tax slabs and Sec.80C limit.

There is no change in your tax slab. The same tax rate as that of last year will continue. They are as below.

Also, the common man’s favourite tax saving tool Sec.80C limit was also not changed.

2) Health Insurance for Senior Citizens–

A Health Insurance Scheme will be launched for senior citizens whose age is 60 years and above. The sum insured under this scheme will be Rs.1, 00,000 and one can opt a top up of Rs.30, 000 above this Rs.1, 00,000 limits.

This I feel a great social initiative. Because considering the health cost and the probability of being hospitalized is more in case of senior citizens, I felt this was the best initiative.

3) TDS limit for EPF withdrawal raised from current Rs.30,000 to Rs.50,000–

Earlier if you withdraw EPF within 5 years and the amount is less than Rs.30,000 then there will be TDS of 10%. However, this limit now raised to Rs.50,000.

How the TDS will flow in case of EPF withdrawal was explained in my earlier post. Jut go through it. Otherwise, follow the below image.

Finance Minister today proposed to 3,000 stores of generic medicine stores will be opened across the country under Prime Minister’s Jan Aushadhi Yojana.

Promoting the generic medicines by the Government will actually reduce the cost of medicines. This is a one of the best initiative.

4) Start a National Dialysis Services Programme–

Nowadays dialysis cost is so horrible that the kidney failure patients find it difficult to manage it. Hence, Finance Minister proposed start dialysis services in all district hospitals under National Dialysis Services Programme.

5) Government will pay 8.33% of the EPS contribution for 3 years for new employees–

What is this? Usually, in 12% of employer’s contribution 8.33% will go towards EPS. This 8.33% will be payable by Government for the first 3 years of employment. The condition here is that the employee must be NEW in that organization and the salary must be less than Rs.15, 000.

This entire benefit will not be applicable to you. But it is totally beneficial to the EMPLOYER. Because the 8.33% of the contribution is from their pocket, which Government want to incentivize for 3 years. So nothing beneficial to you.

6) Soon you will find ATMs in post offices–

To provide the better access to financial services and especially to bring rural folk into accessing of technology, Government proposed to open ATMs and Micro ATMs in Post Office in next 3 years.

7) Tax Rebate under Sec.87A is raised from Rs.2,000 to Rs.5,000-

Let us first understand what is Sec.87A. This is applicable to below taxpayers.

# This Rebate is available only to RESIDENT INDIVIDUALS (but not to HUF, NRIs, AOP or BOI).

# Your total income must be less than Rs.5,00,000 in a year. (Total Income=Income Under All Heads-Deductions from Sec.80C to Sec.80U).

If above conditions are met, then you can show the rebate of Rs.5,000 from your income.

8) Section 80GG limit raised from Rs.24,000 a year to Rs.60,000 a year–

What is Sec.80GG? I already wrote a post on it long back. You can refer it “Section 80GG Deduction-Get Tax Benefit on rent paid if not getting HRA !!!“. Just I will repeat the eligibility condition as below.

# This section is only applicable to Individual or HUF.

# Tax Payer may be either salaried or a self-employed. However, must not be getting HRA.

# Tax Payer may be either salaried or a self-employed. However, must not be getting HRA.

# Tax Payer himself or spouse/Minor Child/HUF of which he is a member should not own any accommodation at a place where he is doing a job or business

# If Tax Payer owns house at a place other than the place noted above, then the concession in respect of self-occupied property is not claimed by him [Under Section 23 (2) (a) or 23 (4) (a)].Tax Payer has to file a declaration in

#Tax Payer has to file a declaration in Form No.10BA regarding the expenditure incurred by him towards the payment of rent.

If the above five conditions are satisfied, the amount deductible under Section 80GG is LEAST OF THE FOLLOWING.

- Rs.5, 000 per month;

- 25% of total income of taxpayer for the year; or

- Rent Paid less 10% of total income (Rent Paid-10% of Total Income).

9) NPS 40% withdrawal at the time of retirement from such retirement corpus is tax-free.

Earlier, both the 60% lump sum withdrawal and the 40% annuity both are taxed as per your tax slab at your retirement. Now Government changed it to bit tax-free. Now onward withdrawal up to 40% of the corpus at the time of retirement tax exempt in the case of National Pension Scheme.

However, do remember that remaining taxation of NPS are as usual. Annuity will be taxed as per your tax slab in your retirement.

10) Superannuation Funds and Recognized Provident Funds (including EPF) withdrawal at the time of retirement will be taxed !

Earlier if your service is more than 5 years, then at the time of retirement (58 Years) this whole amount (Employee+Employer contribution+Interst on both) will be tax-free.

Now in interest accrued on your EPF contribution from the contribution period starting 1st Apri, 2016, 40% will be tax-free. Rest is taxed as per your tax slab. Rest 60% on such accrued interest will be taxed as per your tax slab. As usual there is no tax on you and your employer contribution. This is a biggest jolt to all salaried. However, Government given a bit relief that contributions made into EPF after 1st April, 2016 will be taxed as per this new rule. Earlier contribution and interest accrued thereon will be tax-free.

Also, this rule is not applicable to those whose salary (Basic+DA) is less than Rs.15,000.

After lot of confusion Revenue Secretary Hasmukh Adhia, cleared the noise by saying “Small salaried employees with up to Rs. 15,000 per month income will be kept out of purview of proposed taxation of EPF. Only interest accrued on 60 per cent contribution to EPF after April 1, 2016 will be taxed. The principal amount will remain tax exempt,”.

11) Additional interest of Rs.50,000 tax benefits for new home loans–

Earlier any interest payment towards home loans will be available for tax benefit under Sec.24 of IT Act up to Rs.2,00,000 in a financial year. Now this is raised to another Rs.50,000. However, this additional Rs.50,000 tax benefit on interest of home loan will be available for below categories of loans.

# Loan amount must be less than Rs.35 lakh.

# Value of house must not be more than Rs.60 lakh.

# This will be applicable from next financial year.

12) 10% Tax levied if your dividend income is more than Rs.10 lakh per year.

Earlier dividend distribution tax was same irrespective of the how much you receive as dividend. Now Government imposed a limit on this. If your dividend income in a year is more than Rs.10 lakh, then apart from dividend distribution tax, you also be taxed at 10%.

13) TDS of 1% if you buy a car valued more than Rs.10 lakh or on the purchase of goods and service exceeding Rs.2 lakh.

To bring more transparency in financial dealings, Government brings in 1% TDS if you buy a car valued at more than Rs.10 lakh or purchase any goods and service exceeding Rs.2 lakh.

This I think brings in control of black money to certain extent.

14) Security Transaction Tax (STT) raised for options–

When you sell any option contract in Future and Option Market of stock exchange, then seller have to pay the STT tax. This was earlier at 0.017%. But it is now increased to 0.05%.

15) New cess imposed called as Krishi Kalyan Cess-

This additional cess will be applicable to all taxable services. This cess will be utilized for financing initiatives relating to improvement of agriculture and welfare of farmers. The Cess will come into force with effect from 1st June 2016.

16) TDS on NRIs will be reduced if they provide the alternative documents–

Currently, TDS for NRIs is higher than the Indian Residents. However, now if NRIs provide alternative documents, then this will be reduced.

However, how much is to be reduced or what do you mean by “alternative documents” are not yet clear.

17) Redemption of Sovereign Gold Bonds will not be charged for capital gain tax-

To boost the Sovereign Gold Bonds, finance minister today proposed that in case you redeem this bond then there will not be any capital gain tax.

However, if you transfer such bonds, then the long term capital gain tax will be with indexation benefit.

18) Transfer Mutual Fund units in case of merger or consolidation of schemes are free from capital gain tax-

When funds merge or consolidate then such transfer of units will be considered for capital gain tax.

19) Maximum contribution towards superannuation fund or recognized provident fund is restricted to Rs.1.5 lakh for employer.

For employer from now onward the maximum contribution in a year towards superannuation or recognized provident fund is set to maximum of Rs.1.5 lakh a year.

20) Death claim received under NPS is tax-free–

Any death claim received under NPS to nominee is purely tax-free.

21) One-time portability from EPF or Superannuation to NPS is tax-free

Now you can opt for portability from EPF and Superannuation to NPS without any tax hurdles. This is evident now that Government is pushing for NPS rather than EPF.

22) Pre-Construction period for taxation purpose raised from 3 years to 5 years-

Earlier to claim tax benefits on home loan of a Self-occupied Property, the construction has to be completed within 3 years from the end of the Financial Year in which the capital (home loan) borrowed.

Now it is raised to 5 years. This change will be effective from 1st April. 2017.

23) Date of Agreement is the date of transfer for immovable property-

It is clear that the date of agreement is the date of transfer of immovable property, but not the date of registration of immovable property.

24) Threshold limit for audit for professionals raised from current Rs.25 lakh to Rs.1 Cr.-

If you are professional and your income is Rs.25 lakh in a year, then you must audit it according to Sec.44AB. Now this limit is raised to Rs.1 Cr.

25) Reduction in service tax for Single Premium Annuity policies-

Finance Minister proposed to reduce the service tax on single premium annuity insurance policies from existing 3.5% to 1.4% of the premium paid.

Hi Basu,

I heard that FM is going to introduce a 0.5% cess for the welfare of beggars in our country, he is planning to announce this in April.

Will this be on Income tax or the taxable services?

Pradeep-I am not sure about this. Let us wait and watch for one more CESS 🙂

Hi Basavraj,

I want to manage my portfolio for FY 2016-17.

Could you please guide me to invest in tax saving plans and insurance plans (Term plan).

Arun-I don’t know your financial goals. So how can I guide you? Tax saving and insurance plans (You mean to say insurance+investment products), comes into picture at later stage.

Dear Sir,

I did not understand point no 21 “One-time portability from EPF or Superannuation to NPS is tax-free”. Actually i am hearing it for the first time, would like to know following things on the same.

Can we transfer some amount from EPF to NPS account?

If yes, Would it be beneficial and what is the process of doing it?

Thanks and Regards

Abhijit Dalvi

Abhijit-The move is to promote NPS. It is not partial. You have to move completely from EPF to NPS. However, we have to get some more clarification. Wait for that.

Hi Basavaraj ,

i have been following your blog since a while, thank you very much for sharing detailed information on various topics. your posts clarified so many doubts.

I am a software engineer, my total experience is 5 years, currently i am working in my 3rd company, i have transferred my EPF amount from 1st company to second company and again from the second to third.

my questions are.

1) an individual can withdraw amount post completion of 5 years, since my first company’s PF account is meeting this criteria, am i eligible to with draw money from it? since that contribution (1st company’s) is already landed in my current(3rd) company’s PF account, how can that be with drawn?

2)every time i transferred money to new company’s PF account , i’ve observed that only my contribution+ employer contribution is being transferred to the new one not the contribution towards pension fund, where is that money going? how can i get that?

please help.

thank you in advance

Venkatesh-1) But if you are in job, then you can’t withdraw EPF. Also, read latest withdrawal rules “4 EPF withdrawal changes effective from Feb 2016“.

2) No need to worry. Your EPS followed your EPF.

Dear Sir,

What about the NPS tax benefits for the FY 2016-17? whether the deduction under 80 CCD-1B ( Additional benefit of Rs. 50K is over and above the benefits under 80C) is existing or Not?

Raj-It will continue as usual.

After budget declaration, got to read one good article. Thanks Basu Ji. I’ve one CAN account with CAMS. Now via mfuonline portal, I can invest/redeem/SIP in mutual funds from the comfort of my home! Now I want to open a demat account for online share trading. How to open it? And what are my options? Like in MF, CAMS or KARVY option’s there.

Suggest me the option which has minimum or no brokerage for opening/maintaining that account. I strongly wish to see one full article on that also in future.

Raju-Please read my earlier post “Best Demat and Trading Account in India-How to chose it?“.

Dear sir,

I have a doubt regarding the rise in car prices..will the taxes of infrastructure cess and luxury taxes in budget 2016 17 be effective from april 1 or immediately??The car dealer now asks for an enhanced amount immediately…kindly guide

anesh-Budget changes will come into effect from 1st April, 2016. He is misguiding you.

explain Home loan and interest benefit of this budget for govt. servants and income assessment

Appu-There is no such special benefits in case of Government servants. The tax benefits are same as that of regular assessee.

I can’t believe that Government can touch anything(EPF) to get taxes from everywhere. We keep paying tax on the income which already got taxed. This can only make more blackmoney and more Swiss bank holders.

Next year, both birth tax and death tax can be included.

Karthik-Let us not hope that much bad thing to happen 🙂

Hi

Regarding point 10, does it apply for PPF accounts as well?

Thanks

Sorry, i got my answer after reading below comments and responses.

Thanks

Raghu-Thanks 🙂

RAghu-There is no change in PPF rules.

Jaitley has just made himself a mortal enemy of 6 crore middle class and lower middle class EPF subscribers. Its a dangerous idea to fiddle with the tax structure of a 5 decade old tax-free govt fund. Its also unfair to tax senior citizens’ retirement corpus esp. when they have paid taxes all their life and there isn’t any social security pension unlike euorpe and US.

The political backlash can be severe. Hope trade unions and the middle class protest vociferously and reverse this retrograde move by the Finance mismanager.

Ram-Let us hope for the best. I know it is bit harsh.

Basu, many thanks for for your expert comments, really enjoying reading your post, very simple and easy to understand, thank you keep posting.

Dear Basavaraj,

My comments is regarding point #10 related to 60% of all PF deposits after April 2016 being taxed.

Lets assume some one is getting 1 crore after retirement. 60% of which is 60 lakhs will be taxed @ say, 30%-slab will result in a tax of 18 lakhs + Edu.cess extra. Total money in hand will reduce to less than 82 lakh for rest of his life.This is huge and so painful to salaried class. Is this correct?

I contribute towards Voluntary PF till this year. Now , i wish to do away with this and feel like paying to my home loan principal with this . What are other options available ? Please share your views on this.

regards,

Suresh

Suresh-Your understanding is perfect. The Government move is simple that they want to align both EPF and NPS in same way. So slowly moving towards NPS. But sadly forgetting that how badly it impacts in long run. Other options depends on your requirement and when and for what purpose you need that amount and all. I can’t suggest blindly.

Also another point, by the time the current generation who are in there 30’s reach there retirement age ie 58yrs i am sure there will be lot of changes in tax slabs.

Having said that i don’t understand why government is forcing people to buy Annuity plans after retirement both in case of NPS and now in EPF…

If promoting annuity plans was there real intention, they could have provided additional benefits for ppl who opt for annuity schemes rather than threatening them by taxing the corpus on withdrawal, so that people voluntarily would have put there money on annuity plans

Raghu-The real intention is different. It is combining NPF and EPF.

I was reading somewhere looks like tax liability will be more if govt considers taxing 60% of interest amount. Can you clarify which is better taxing 60% of employee contribution or taxing interest earned on 60% of employee contributiom?

Wow there is so much confusion.. RIP EPFO

Raghu-Wait for few more days. No need to jump into any conclusion.

Hi Basu,

V good one; you nailed it! I shared this to link on fb page. Pls let me know if you have objection, I’ll remove it. Thanks.

Teja-Not at all. In fact I am happy if you share it 🙂

Dear Sir,

I have question on Point 10: Superannuation Funds and Recognized Provident Funds (including EPF) withdrawal at the time of retirement will be taxed:

My father is retiring in 2016- Nov so will his entire EPF fund / Superannuation/Gratuity fund will be taxed or only his contribution from April 2016 till Nov 2016 minus 40% will be taxed.

Means for example his EPF balance as of now is 5 lakh and from April till Nov he will be contributing 1 lakh then tax will be imposed on only 60k or entire 5lakh + 1 lakh – 40% i.e on 3.6 lakh

I hope i have put my question correctly.

Thanks

Shekhar

Shekhar-Please read the updated post once again.

Hi Basavraj,

On line 21

21) One-time portability from EPF or Superannuation to NPS is tax-free.

Is it possible to port from superannuation to NPS, Previously I opted for superannuation and now moved to NPS. I checked with HDFC Securities who manages NPS, they said that its not possible

Deepak-From Superannuation to NPS is not possible as of NOW.

what changes(maturity taxation?) will be on ppf after union budget 2016?

Uttam-There is no change. There is a huge confusion of many about EPF and PPF. But keep it mind that this budget not touched anything related to PPF.

But we can expect taxation on PPF too, soon, that was a key point in the Economic Survey

Srmenon-Cool…let us wait till next year budget 🙂

138. In case of superannuation funds and recognized provident funds, including EPF, the same norm of 40% of corpus to be tax free will apply in respect of corpus created out of contributions made after 1.4.2016.

–> This is from FM’s Budget Speech. ( and Recognized Provident Funds, including EPF).. This probably implies PPF also.

Can you please clarify ?

Karthik-PPF is not annuity product nor the pension product. It is purely different product. Don’t confuse yourself between EPF and PPF. Just Govt cleared that there is no change in PPF rules ( It is as per what I expected). So hope the doubt is cleared now.

Yes… Thanks for the clarification…

I am an employee of west bengal govt.Here we are to contribute compulsorily minimum 6% of basic pay towards GPF.Will it be in same taxation as that of EPF?