Recently I wrote a post regarding best term insurance available in market and claim settlement ratio of Life Insurers. Few felt that they need the same data for Health Insurance Companies too. So let us try to analyze these things from the available IRDA Data.

Note-IRDA released the Annual Report for 2013-14. To know more about the latest Best Health Insurance companies, visit below link.

First of all let us understand the business model of Life and Health Insurance. Both are entirely different businesses when it comes to managing. In Life Insurance your contract with Insurance company is for long term whereas in Health Insurance your contract is on yearly base. So here in health insurance claim settlement we need to consider the yearly premium collection too. That is the reason it felt by many that claim settlement ratio is not so important. But I tried to sum up all the data available from IRDA to arrive at insurance company business.

How many Health Insurance companies are there in India currently?

According to IRDA report 2012-2013, there are 17 Private Insurance companies who do business in General Health Insurance along with Health Insurance, 4 Public Sector biggies and 4 standalone insurance companies who’s core business in only Health Insurance.

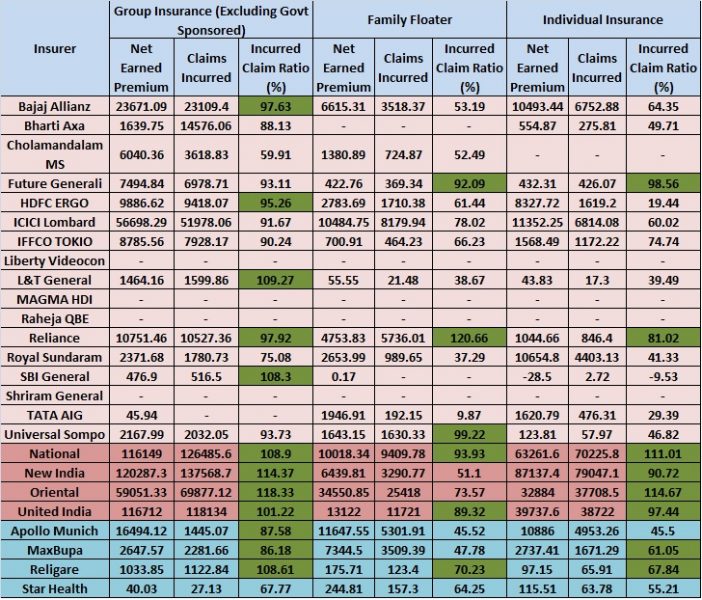

Below is the table which describes the business volume and claim settlement ratio of each individual health insurance companies.

(Note-All figures are in Lakh, data based on IRDA Annual Report 2012-2013)

Here in above sheet I differentiated companies in 3 categories as I said above and coloured differently for each category. Next I considered Group Insurance Schemes (excluding Govt sponsored), Family floater and Individual Health Insurance Schemes.

You notice that in group insurance segment private insurers are aggressive in claim settlement. But when it comes to family floater then general insurance companies and public sector companies are way ahead than standalone health insurance companies. Finally for individual health insurance category again public sector companies are very much aggressive.

Surprising part to me is, standalone companies claim settlement ratio for family floater and individual health insurance policies were low compare to others. This may be due to more scrutiny in settling claims due to their in house TPA.

Hope above table will be helpful for you in choosing a best health insurer.

Hi sir.hope all good at your end.this is MAHESH here,iam about to renew my max bhupa health insurance policy family floater companian with base insured for 7.5 lks to myself,spouse and one daughter (45 ,45 and 18 years subsequently) .today is last date for renewal.premium is 20,917/- per annum.kindly advise me.

Dear Mahesh,

Why a doubt?

hello sir

am mahesh planning to purchase health insurance policy for parents of age 60 ,50 and also brother ,me of age 30 and 25 years which is the best health insurance plan for us please suggest us

Dear Mahesh,

I suggest you to go for senior citizen policies like Star for your father. For your mohter, you and your brother, you can go with HDFC ERGO, Max Bupa or IICI (individual plan).

Is it wise to take any New India assurance mediclaim policy online as their local branch is advising to get it from them to get better support..as per their statement one may get difficulties during claim time..

so , what’s your take on this.. shall i opt for online or Offline?

Dear Deep,

For the claim process, online and offline are the same. It is few guys who create fear inside you.

I would like to take Mediclaim through New India assurance for my Wife & Son (New India Floater policy) so need some solutions which are cited below

1) In my Son’s Birth certificate my wife’s maiden surname is mentioned along with her paternal address as she has not yet changed the same in any of the govt I card like Aadhaar , Voter ID but she has Marriage certificate with my surname and address

2) So, during taking a new policy online which surname & address shall i mention for my wife is it her paternal one or post marriage one

So, incase of any hospitalisation case of my son (hope not required at all) whether relationship of ,y son & wife can be proved based on the basis of birth certificate of my Son.

Dear Deep,

Let her first update by producing the marriage certificate in all records along with using the name as it is in Marriage Certificate.

Hi.. i would like to go for health insurance for my spouse and my baby 1 year..

which one is the best

NEW INDIA FLOATER MEDICLAIM POLICY (SI 5 Lakhs)

Star Health FAMILY HEALTH OPTIMA INSURANCE PLAN (SI 4 Lakhs)

which one has the best chance to get the claim?

Dear Deep,

How you shortlisted these two products?

Dear Basu,

Could you please publish an article or advise on Cancer Insuranec plan.

Whether it is required and what are those available in India.

How to choose the best one And how to choose from, among different companies.

Thanks,

Pradipta Sahoo

Pradipta-I published one already. Refer the same “LIC Cancer Care (Plan 905) – Features, Benefits and Review“.

Sir, First of all God bless you for enlightening the aam admi with your in depth understanding in Health Insurance segment. Very honestly its extremely difficult for common man to decide between the zillions of options to choose from

my questions,

i happened to read the below link, can we rely these stats.

http://www.livemint.com/Object/1XhvIv1t7ce1r1WiQ4BoyJ/mediclaimrating-2017.html

from these reports, i find icici lombard to be a good choice, based on their track record and irda data

please comment

second q to you

i am occasional drinker [ once in a week] and smoker [once in a month]

do i declare these while filling the forms

what if, i declare, will they reject all claims in future related to the above

what if, i dont declare, will they still reject all claims in future related to the above

Please comment

Jestine-You can rely but the decision must be taken with both eyes open. You must declare your habits. If you do not declare, then you give enough room for insurers to find the faults and reject the claim. Why to take the risk?

Hi Basunivesh,

I have a pre -existing psychiatric illness(very minimal) and using tablets for the same.When i approached insurance companies to take medical insurance, theu rejected without issuing the policy stating that because of that illness.

Almost 3 insurance companies rejected the same.Now how to take a medical insurance for me?

Krishna-Hrad to say but only option is to search others.

Hello Basu , I have Apollo Munich optima restore health insurance (3 lac) + top up policy apollo Munich 6 lac for last 4 years.I have claimed insurance in first year for my surgery which they denied indicating it was preexisting condition which was not revealed during application and they add it as permanant exclusion from policy.I want to know should i change my policy now using portability option as 3 yrs are passed post surgery(its shoulder surgery ),or even new policy from other insurance provider will have same clause.Also,what will happen to top up policy if I change the base plan.Thanks for answer in advance

Kunal-It is hard to suggest whether your new insurer will consider this as permanent exclusion or provide some relief of clause with limitation. I think it is better to stick with the existing insurer. Because such surgery is not again repetitive in nature (as per my knowledge).

Dear Basu, my family is health covered under my employers group policy. I intend to retire in couple of years at the age of 50. will I be able to port out from the group policy then? or should I buy another policy separately? thanks. Naresh

Dear Naresh,

Regarding porting, check with your existing insurer. However, I suggest you to buy separate one for you.

Hi Basvaraj,

Finally I zeroed down on MaxBupa. But I am concern of its poor Claim ration. Policybazar website says its overall is just 57%. Should I worry about these figures? Can you please comment guide on market reputation of MaxBupa and latest claim ratio? I copmared it with Star and Apolo.

Nadeem-Claim data is RAW. Hence, if you liked the product, then go ahead.

Hello Sir,

I bought Apollo Munich Easy Health Insurance plan a year back, paid a premium of INR 4,598. According to age slabs, my premium should increase in 2018. I did not take any claim last year, in spite of that they have increased my premium to INR 5,634. The reason for raise is being told as increase in base rate. Can insurance companies increase base rates of ongoing policies? If it is so, then how can a person plan health insurance, as you never know what will be the premium that you’ll have to pay in coming years!!!

Binny-They can raise based on age slab. However, for what purpose they have to raise on base rate wise? Check with them.

Thankyou for your quick reply, Sir. Upon asking, they said they’ve revised the rates due to hike in medical treatment costs, and supposedly, have added some benefits that are irrelevant.

Binny-If you feel it is useless, then I suggest to use the portability option and move on.

Okay. Thankyou.

Hi Binni

Apollo is a good company but their es are very high. I checking. For my parents…. In 3 yrs they were increasing from 38k to 55 and then in next 4 yra to much higher. Its huge and unjustifiable. I found maxbupa and star and many others much better for similar services.

Thanks for your suggestions Nadeem.

Hi

I am newly married and I want to buy a health insurance for me (30 yrs) and my wife(29 years) . After a week of extensive research we have zeroed on MAX Bupa Health companion and Apollo Munich Optima Restore.

1. Can u please suggest which one is better? and also the reason for the same.

2. What is the optimum cover for the medical insurance?

Thanks

Raj

Raj-1) Both are equally good and bad.

2) It is the sum insured under the policy.

Could you please be a little more elaborate? What is good and bad?

I know the cover is the sum assured, what I am asking is what is the ideal cover one should have for a couple? and how does one decide it?

Raj-Ideal cover depends on your premium paying capacity, the city you live in and the health issues you are facing. Hence, it is hard for me to suggest anything.

You still didnt answer my first question as to what is good and bad in apollo and max?

Raj-Good when you regularly pay premium and bad when you knock for claim. That is the reason they are all into business. So they are equally good and bad.

honestly, you were seriously of no help.. Thanks a lot for not helping and giving all weird answers.

I also read most of your answers in the comments section and understood that you never give proper and relevant answers. Whats the use of having a blog and being this so called ‘FINANCIAL ADVISOR’ when u don’t have or deliberately don’t want to give proper answers to readers questions.. I seriously regret wasting my time!!

Raj-If you are looking for readymade answers, then SORRY this blog is not for YOU. You can find many such experts who BLINDLY give you READYMADE TIPS. But I can’t do such hazardous work. Rest you to decide because at the end it is your MONEY at risk NOT MINE.

haha.. That’s always your comeback isn’t it.You had said the same thing to someone in the comments below earlier also.

BTW I was not expecting any READYMADE TIPS or answers.

What I was expecting is that you advise me about the PROS and CONS for both apollo and max. I am not telling you to choose, that my job. I was just asking you about the plus n minus which either you don’t know or don’t want to share.

Was it that hard to interpret from my first query? All I wanted was genuine piece of advice out of experience or research. Both of which you obviously lack for sure. If you have done some research (which I have seriously started doubting now) then whats the issue in sharing it.

You answers are so absurd that I frankly don’t know what the reader should interpret out of it. which financial advisor replies ‘both are good and bad’ without even stating reasons for the same.

One things for sure, thanks to internet anyone with half baked knowledge like you can come up and write a blog and give such unhelpful and dim-witted so called advice.

Raj-Research will come out when I have data. Without knowing much about you, I can’t do or guide you. You are free to decide my EXPERIENCE and RESEARCH at your own thinking. I don’t want your certification also 🙂 You buy the product, you experience the claims, then you will come to know the meaning of “EQUALLY GOOD AND BAD” 🙂 Till that period ask to someone who can provide you ready made TIPS.

Thanks that you tagged me HALF BAKED. Because how can I be FULL BAKED without knowing the opposite person’s FULL BAKED data? You need ready made answers and my intention is to think on your own because it is you who suffer not me. Rest you decide 🙂

Hi Raj,

I purchased my last term plan based on inputs from Basuvinesh blog on term plan. He patiently provided lot of good advises to me so I was luky on this regard. It was very helpful. Here also the Health Insurance blog is good and providing data which are useful. Still I could think Basu could have provided more accurate answer but it seems he is unwilling for some reasons :). Nevertheless his blogs are good and I am a now a fan of his blogs.

I am also on same page to you, I will share my research till now in case its of any help to you.

Nadeem and Raj-When it comes to zeroing on product, I simply avoid any particular company or product.

Hi Raj,

Even i am looking for a critical plan and a health plan for my parents. With help of Basuvinesh blogs and discussing with companies Sales guys, I zeroed down on Max Bupa (Heath companion variant 1), Apollo Munich and Star out of so many companies. As yours zeroed list and mine is similar so sharing my views, hope you will find useful and Basu will correct us where required ;).

1. Premium: Star is cheapest, I might go with it as their Optima plan is quite cheap with reasonable coverage. Some data collected so far in last 2 days, For 10 lakhs for 63 yrs/58 yrs parents, premium for floater HI is: Apollo= 48k, HDFC Ergo= 53k, Max Bupa= 42k, Religare=42.6k, Star comprehensive = 48k, Star Optima = 27k

2. IRDA data: but with my limited knowledge, IRDA data shows the Premium collected over year is less for Star so seems its not doing so good. Apollo and Max Bupa seems going better in Market in but their ICR is quite less for floater and individual HI. So now I am skeptical

3. Pre-disease: Apollo is good as 3 yrs waiting for pre-disease, Star & Max Bupa has 4 yrs. Max Bupa other variants 2&3 are less i.e. 3 days.

4. Riders: Star & Max Bupa has accidental benefit plus refill. Refill are there in few others also, just check. Apollo has critical rider.

5. Premium renewal revision: I dont like MaxBupa premium revision bracket. They increasing premium every year. I didnt check for Apollo. But Star has bracket wise range where for my 63 yrs old parent, locking for premium increase is 3 yrs. Apollo I didn’t check. Here Star score highest. MaxBupa lowest. Even MaxBUPA 2,3 yrs policy option is coming higher, may be correctly so check for your age brackets.

6. Most important medical test: Some like Apollo mandate test for senior or for lower age they dont need medical test for SI<5 Lakhs. Above they require. Star comprehensive doesnt require any medical test. Star Optima requires. Max Bupa told me they require for higher sum assurance also. BTW, I have nothing to hide and want my parents health reviewed, you may check for your preference.

7. Co-payment : check for this also. Some ask for high. Apollo is good here , they asked me only 15%. MaxBupa has option for 0. Star optima have option for 0 in comprehce but 20% in optima.

8. Cashless Network in my city: Most of them have tieup to similar set of hospitals in my city. Check for yours.

10. Sales quality: Star, Apollo, MaxBUPA very good. Religare worst as they didnt reply to my email form last 4 days.

11. Exclusion: Some of them like MaxBUPA have lot of exclusions.

12. No claim: Star is best as they increase the SI. Apollo is ok, just 5%. MaxBupa says 12.5% but actual its less.

13. Other benefits etc like Maternity I didn’t check as it was for my parents ?… you may like to. Check for caps on Room rents. Policy term is for Life in most cases, but they are anyway going to increase the premium, benefit is not like in Term plan.

BTW, Funny thing is while checking on internet, people are happy and cursing all companies depending on their experience :). So an advisor is right when he say both are good or bad. Hope this helps. Do share your exp also, as it may help people like me also. I will soon purchase one… may be Apollo (benefits) or Star (cheap) or MaxBupa (in between). Again I am not an expert nor willing to write a blog, but just sharing my gathered understanding till now. Its tiring exercise and you can never guarantee of not having bad exp. Just be truthful in filling all details.

Anyway do share which one you finally choose/choosen and the reasons for choosing over other.

Hi Basunivesh,

Firstly i congratulates for this good informative website. I really like it.

Please help me out

I need health insurance for my parents which was previously covered by my previous company at the copay of 20% with no additional premium(Wife, me and parents @2500Rs) but in my new company they are covered with high premium(40000 RS) for 5 lakhs. I am looking for reliable insurers and cost effective.

I am sick of all insurance companies i had gone through insurances policy with high premium and having co pay and long standing preexisting disease for 3/4 years. recently i surfed insurance from PSUs they are price effective and with copay. in this situation i don’t want my parents uncovered when movement from companies. so i decided to take policy from outside and with copay.

I selected two PSU which are cost effective PNB -oriental and Andhra bank arogadhaan and only confused with shall i go for family floater for parents or family floater for parents and spouse and me.

as

1. my wife have one individual policy from (apollo munich).

2. my wife company had covered me and my wife for 5 lakhs with copay.(apollo munich)

3. In my company my wife and me are covered with copay of 20% and 5%.(apollo munich)

I don’t have any seperate policy apart from my company and wife’s company. also I had check the insurer claim ratio is very high for PSU’s. Do they really settle the claim or straight forward reject as the rumors from private insurers.

Please suggest me the best option.

I will high appreciate your efforts towards my help!

Its urgent as year is coming to close and i have to decide before 28th dec.

Thanks

Rajmani

Rajmani-You are going with the insurance which provided by tied with banks. Not sure how long they run the show. Instead, buy the health insurance from general insurer or standalone health insurance providers. Better to separate your parents from your family. If you combine, then it cost you more.

I am planning to buy a new health insurance policy for my family.

i am 34 my wife 32, elder daughter 10 and youngest daughter 6 year old, I have plan sum insured amount of Rs. 5 lac.

So kindly give your valuable suggestion for which policy best for my family with avg. Premium (up to 15000/-) & having good claim settlement record in IRDA.

Thanks

Ravindra-In my view you can look for Apollo, Religare, New India or National.

Thanks sir,….

Thank you very much

My name is Atul, Age 31Yrs, i want buy family health insurance – Rs 3 lakhs . kindly suggest which is the best company & plan.

Thanks

Atul-Please refer above post and chose the one which suitable for you.

Which is best between star health and national insurance

Atul-I will never name any particular company.

I am 27 years old male, with history of ankle fracture 3 years back (post operated) and history of shoulder dislocation and fracture humerus (post operated) 3 months back. History of epilepsy, on medication for 3 months. My ankle is prone to develop arthritis changes and I might require arthroscopic debridement of ankle or even ankle replacement in coming 5-10 years. I want to have a health insurance with sum 7.5-10 lacs, no cap on room. The plan should cover the surgeries I mentioned, after 3-4 years. My sole aim of taking a plan is to cover these surgeries, so I want to know specifically if at all the above mentioned surgeries will be included in the plans. I would also like to know if there is any health plan that covers cost of lab investigations on OPD basis as well.

Thanking you,

Dr Rahul Chawla

Rahul-But sole AIM of all insurers is to insure the person who is not prone to any expenses in future as it is loss to their business.

I might require surgery, not necessary that I would..may be after 5 years..may be after 10 years..depending on condition at that time…so wanted to opt for a plan that includes the above mentioned surgery after 4 years. Any suggestion regarding plans to opt for?

Rahul-I can’t point anyone insurer or product. But it is purely depends on insurance company. Check first with few public sector companies.

Could you please delete above both of the comments in the form of questions I asked. Apprensive that the medical history could be an issue afterwards in the policy I m taking. Thanks in advance 🙂

Rahul-Don’t worry. There are many Rahul’s for that particular company.

Is icici lombard insurance company is good. I would like to do Complete health insurance policy

RAghu-You can go ahead if plan features matching and also premium is affordable to you.

Your answers are politically correct. In short no benefit to readers.

Kumar-Pleasure 🙂

Hi Basavraj, Thank you for your work in providing clarification and help to people. I want to buy family floater for myself (32 years) and my wife (28 years). My questions are-

1. Should I choose standalone insurer like Apollo, Max Bupa etc. or Public insurer? Which one is better in terms of claim settlement?

2. Does premium increase after every year? or some age group like when I cross 35 years age?

3. Does premium increase if I claim in any one year?

Shailendra-1) I slightly inclined towards standalone.

2) Premium increases based on age group.

3) NO.

Thanks for quick response. Some more questions-

1. I see that ICR is way higher for public insurer. Does that mean they do not just work for profit and reject fewer claims?or they may be wrong in term of their planning and end up paying more?

2. I could not find genuine information on CSR for various insurer. Do you know latest CSR for Apollo, max Bupa, Oriental, United India Assurance? Is there a consolidate list?

3. I want to take insurance for sum approx 25L. When I look at various comparison websites, only Apollo and Max Bupa provides insurance for such high amount. Does that mean only standalone insurer provides high amount insurance?

Shailendra-1) Don’t rely too much on ICR. Who knows that public sector companies may NOT REJECT YOUR CLAIM? Look for feature, affordability and comfort with company and go ahead.

2) Refer my latest post “Best Health Insurance Company in India-Based on IRDA 2014-15 Incurred Ratio“.

3) Never believe such portals. They are INDIRECT AGENT, they show which profit to them.

Dear Sir,

Please advise a good medi claim policy {Family Floater} for me. I am 49 years and my wife is 38 years old. And my son is 12 years old. We don’t have any health issues. The coverage would be 3 lakhs.

Ajai-They are already listed above.

Hi Sir,

I have taken Oriental Family floater policy 2 years back. All my family members(myself+wife+son+father+mother) are included in this plan. Recently they have increased the premium amount from 13K to 24K. I opted this plan because it was providing 5 Lac rupees cover for all the members in Rs 13K.

1. Is this plan good for my family protection or I should look for some other?

2. Is their any information about the maximum renewable age, I tried to find but couldn’t found the same?

I have bought this insurance through medimanage. I have opted for TPA service. Apart from this I have opted for Rs 2 Lac corporate insurance more for my parents by paying Rs 16K . Correct me if I have planned anything wrong.

Thank you in advance!

Ankush-First check why the premium increased to almost double.

Hello Basavaraj Tonagatti,

I’m intending to buy a health insurance for my parents ( Age : 55 Yrs old).

Can you suggest if going with Standalone Companies or Public Sector would be right ? And reasons behind it.

Thanks

Saket-Better public sector companies.

Hello Sir

I have a ULIP Policy, ICICI prudential health saver family floater policy. I am 37, my wife is 31 and we have a girl child of 5 years. Do i need to look for another policy? In that case what is ur opinion abour Religares, Care Insurance policy? Please opine

Pavithran-Your requirement is health or life insurance?

Hi Basvaraj,

I’m finalizing on health insurance plan for my family (myself, husband and 1 kid). I’m confused with Star, Max Bupa and ICICI Lombard.

From you expertise, what do you suggest?

I’m taking this plan for tax saver and to cover family’s usual medical expense (claimable).

Anila-What is confusing you?

Hellow Sir,

I am Working As Medical Representative Normally I’m Driving On Bike 6-8 Hr In Different Places. So, I Required Easy Claim Settlement Regarding Different Types Of Policies Such As 1) Health Insurance Policy (In Which Medi Claimed )And 2) Life Insurance (Natural Or Accidental Death Benefit Policy) For Me Which Protect My Wife, Daughter & Mummy.

Devendra-All three are must but dont combine all three. Buy separately and especially for life insurance buy ONLY term insurance.

Thanking You For Replying My Comment But Which One Best Company For Health Insurance As Well As Life Insurance, Please Help Me Regarding Quires.

Devendra-All are equally GOOD AND BAD.

Thanking Sir Again Replying My Quries But Regarding This Two Insurance Company i.e Apollo Munich & TATA Aig Which One Is Best.

Devendra-I may be biased, but I am towards Apollo.

Hello Sir,

I was comparing the premium charts of Religare care and optima restore for 10 lac SA. I could see that the premium go very high in Optima restore during old age. Can i assume that 30-35 years later also same premium “trend” would be around for Religare and Apollo, considering both are there in market then too.

As of now i am inclined towards Apollo Munich, but this premium “trend” is making me consider Religare.

1) What would be your suggestion about this?

2) I remember reading that you prefer companies that use TPA for claim settlement, what could be the reason behind this preference?

3) After going through the policy wordings of normal health insurance and Super tops, I feel if i have the corpus to take care of the deductible(eg 5 lac), then i should opt for a super top up of 10 lac instead of a normal health insurance. The premiums are really low and the features are quite similar. Do you share this view?

And i must say that your blog has given a good insight about many topics.

Regards

Anoop-As far as the premium chat is there, they can’t increase as and when they wish. I never said that to go with companies which have their TPA service. Hope you misunderstood it. If you afford Rs.5 lakh then go ahead. But you can insure that Rs.5 lakh also wisely. Just buying a base plan of Rs.5 lakh. Rest is left with you.

Hi This is tushar mittal

I am looking for a health insurance policy for myself (25yrs) , my father (51yrs) and my mother (46yrs, hypertension and surgical history of uterus removal).

Where should i go public companies or private companies.

being a public companies does it take long time to settle the claims..

Can you please suggest me a good policy.. lesser caps and good settlement ratio?

Tushar-Separate your insurance with your parents. For your parents you may check with public sector companies and for you private sectors like Apollo, MaxBupa or Religare.

Hi Sir,

I want to buy a health insurance for my mom age 53. She has a medical history 5 years ago on that time she undergo for a surgery. She was suffered from TB along with plural effusion. I want a good health policy for her, so that at the time of claim rejection should be none. Please suggest me a good health policy for her, Recently Coverfox suggested me a health insurance of oriental. Your suggestion required for the health plan. I think Religare offer a good plan, please suggest if I should go with Religare or any other else

Thanks in Advance

Karan

Karan-Considering her age, I suggest you to go for Oriental. I may be bit biased towards public sector companies. But claims may be easy.

Please Suggest, If I am considering The New India Assurance health insurance or Oriental Health Insurance is best, please also suggest me about SBI general Health insurance

Karan-To me, all are BEST.

dear sir,

I have working as LIC agent since 6 years now I take General insuranc eagency,which company suited for me.

Anil-I am not expert to guide you on that.

Sir,

I have purchased a family floater policy of 5 lakh from star health and already my company has provided a medi claim policy of 3 lakh for my family, now I want to know what are the ways to use this both for claim settlement.

Anjan-First try to use corporate insurance, then your own.

Sir,

If the claim amount has exceeds the sum insured in case of corporate insurance in that case can I claim the balance amount from my own? if yes then how? please advise considering both the case i.e cashless and without cashless treatment.

Anjan-Yes, you can claim the remaining from your own insurance. But you have to share the bills with two insurers.

I am 27, residing in Varanasi, looking for a heath policy if 5L.

Have shortlisted ICICI Lombard, and L&T Ins. Which one to go for?

Vishnu-For me, both are BEST.

Hi,

I need to buy an medical insurance for my mother who is 59 years old she doesn’t have any existing condition. My advisor is suggest L&T health insurance. I am not sure how they are ? Can anyone give me a feedback.

Thanks

Som

Som-If the features matches of L&T, then go ahead.

Hi basavaraj ji,

I am Truptesh Darji, age 29. I want family floater for me & my wife. I have compared few of the plans.

1. Bharti AXA Smart Health Basic.

2. Religare Care.

3. Cignattk ProHealth Protect SB02.

4. Mexbupa Health Companion.

Which one is best among these?

Truptesh-1st, 2nd and 4th.

go with max bupa you also get maternity benefit after 2 year .

Parthsingh-Check the requirement of reader and then comment.

Respected Sir, I want to purchase health insurance policy for my son who is 20. Shall I go for Apollo optima restore or religare care with NCB super. Why Religare premium is 50%less than Apollo optima restore ?

Mahender-If plan features matching you then go ahead with Apollo. Setting premium is entirely insurance company’s decision. No one can question it.

Basu,

I currently have 2 floater policies with Apollo Munich (Optima Restore) policies. One is for me (46 yrs) and my son (16 yrs) and the other policy is for my wife (42 yrs) and my daughter (11). We took this policy for 10 Lakhs each and since we have not made any claims since the last 3 years we took this policy, out Bonus now is 100% and hence each policy is worth 20 lakhs each now.

However I have always been worried about Optima restore because of the Bonus being reduced by 50% after a claim year.

Now my financial advisor is advising me to take similar 2 floater policies with Max Bupa with 5 Lakhs each and add a floater of 20 or 30 lakhs (basically 2 policies for 5 lakhs individual limit for 2 people and another floater for each policy). He is suggesting Max Bupa Gold for me. While this plan is a little more expensive, I like the fact that there is no loading charges and also no bonus reduction. In addition, with portability, I assume there will be no waiting period also.

Can you pls advise me if this is the right move to make ?

Shankar-Stick to Apollo.

Thanks for your response Basu. Based on your advise, I have gone ahead and renewed my policy with Apollo. However, I wanted to know from you your thoughts on why you chose Apollo over BUPA. Is it because of Claim settlement or Customer service or market feedback or something else? I would be interested to know the factor.

Also, when I initially took the apollo policy in 2012, there was a loading factor of 19.83% that apollo charged me because of existing health conditions for me. I was fine with this. However after 3 years, inspite of no claims from my side, they have been increasing the loading factor along with my age. Now my loading factor stands @ 21,83% and is 2% more than what I paid when I initially took the policy. Not sure how more this is going to increase for me in the future. Would you still recommend me to stick to Apollo for the next 1 or 2 years also ? Pls let me know your thoughts.

I wanted details of Health insurance and Not Mediclaim policies. What we want is how Life insurance companies who launch different health plans are different from those who specifically working in health insurance ……and not General and health.

Manual-Read my earlier post on the same of LIC’s product “Jeevan Arogya-Do you know this LIC’s Health or Medical Insurance Policy?“.

I want to buy a health policy which is best through bank or direct from the agent/company.

Sanjeev-It depends on the features you are looking for. How can I say?

Direct is better than banks. For our experience people have been facing a few settlement issues with policies tied with banks. You can go for floater plan for your family . If you want PSU go for New India Assurance or National . If you are looking for private companies HDFC Ergo or Max Bupa are good.

There are various options like Individual , Floater combinations etc , so its good to know understand and then buy the plan of your choice

Hi Mr. Basu,

Nice article however I have a different opinion to judge companies on their incurred claim ration. Higher incurred claim ratio means the company is in loss. That is the reason usually insurance companies load your premium when they incur a higher loss (even though you do not have any claims in previous years). Thus it becomes very tough for a client to continue the policy with loaded premium (specially when companies load premium when one files big claims). In my opinion claims reported vs settled can be one of the good parameter to check while buying any health insurance. Apart from it time taken to process cashless / reimbursement claims is another very good aspect to check while buying health insurance for your family.

While buying insurance I should also understand that everything is not covered in the policy. There are certain exclusion & waiting periods in the policy on certain diseases.

Regards

Dhiraj Rana

Training Manager in a Health Insurance Company

Dhiraj-But according to IRDA rules, because of their loss with claim settlement in certain cases, they can’t load the premium as their wish. It is purely abolished long back.

Hi Basu,

Thanks for the great information.

I’m looking to get myself, wife, son, parents & parents-in-law insured in a new single floater policy. 3 of the 4 parents are between 61-65 years of age and have pre-existing hypertension (nothing else major). We do have currently ongoing age old policies from different insurance companies but all individual ones and with not so significant sum assured. Getting each one topped-up may not be as good as to opt instead for a single floater policy. Hence, looking for same.

Could you suggest a good option ?

Star health appears good for senior citizens, but recent public reviews and low claim ratios worry me a bit. What’s your take on this ?

Thanks ahead,

Ankit

Ankit-Please refer my earlier post “Best Health Insurance Company in India-Based on IRDA 2014-15 Incurred Ratio“.

Thanks. Could you also suggest few good options for the floater policy I’m looking for (to cover all senior citizens along with primary family) ?

for folks in family beyond 60 pls continue the existing plan. As they have previous history of hyper tension they may not get a new cover and even if they do it will come with waiting periods. For you 3 you can get cover with floater plan or heartbeat gold pan from Max Bupa

Even after informing the Agent all about the diseases they have not informed the company and provided me the insurance . Next year before renewal I revalided the same and norticed that the agent had fooled me and he hasnt provided any supporting document which could help Star in declining the claim. On top when I addressed this this is the reply given by the company . They tell al lthe mistakes are customers and agents dosent have any role in this . This is how they ash away . So never go with a company which is already predecided to be with fraud agent and cheat customers

Dear Sir/Madam,

RE:- Policy no P/* Policy. Senior Citizen Red Carpet Policy

We acknowledge your representation regarding the issue in incorporating PED in the above mentioned policy.

In this connection, we would like to inform you that it is the responsibility of every customer to disclose all the previous medical history in the proposal form and our intermediary assist only to fill up the form.

Informing orally to the agent/SM is not sufficient and the declaration of the previous medical history has to be mentioned in the proposal. The proposer has to verify the proposal before signing.

At the time of taking our policy which is on..20*, you have not disclosed the medical history in the proposal form which amounts to non-disclosure of material facts leads to the violation of principle of utmost good faith and making the insurance contract voidable.

We, based on your request vide telecom, advising you to submit the entire medical documents regarding the ailment which is to be incorporate as PED

By evaluating the risk element, we will communicate you. Be extra cautious when you are planning to go with Star. I suggest you to take insurance with other companies .

kksclt-I say it that your ignorance or belief on agent is the biggest mistake. As per rule, they are correct.

Hello Sir,

As regards family floater mediclaim shall I go for Bajaj Allianz Ins. Co. or Nationalised Bank tied up Ins. co. Please advice.

Anil-Don’t go with the insurer tied with banks. But of standalone.

Maxbupa’s family floater is very good. Depending on your budget there are options of health companion and heartbeat gold

HELLOOO,,,I M From delhi age 21. i am searching for health insurense..which company i choose …wt about RELIGARE.

Sanchay-Read my latest post “Best Health Insurance Company in India-Based on IRDA 2014-15 Incurred Ratio“.

Frd never buy your health insurance from 3 companies Religare,royal Sundram and star health .rest other companies are good u can go ahead .I’m telling you from my experience and rest choice is yours

Vishal-How can you have health insurance from all these three companies. I head an individual will have only with one company. Why you split your health insurance among all these worst (according to you) companies?

Hi

would you like to share your experience for Star health as I am planning to buy for Star

Swapnil-It is cheapest. But with heavy co-payment clause.

i took apollo munich family floter restore plan health nsurance ,but settelment ratio is very low ,what can i do for future .please give me your mobile no ,mail id

Amirtharaj-Continue the same insurance, No need to worry.

Can an insurance company like max bupa (health companion plan)reject your policy issuance if you say that the insured person(my mom) has little symptons of artritis (RA) ? Currently arthiris is not major but doctor has suggested for physiotherapy. I am ok if they cover that after 3 years of waiting period but they said they cannot issue policy because of RA. My father has BP takes regular BP pills.

Can you please suggest a suitable plan for ,my parents age 58 which can cover above disease ? I am ok with waiting period . Sum insured minimum 5 lakhs , City Pune

Riyal-It is purely insurance company call for rejection of proposal. We can’t say anything on that. Check with Star or Apollo.

But what if companies mention on their sties to accept all the pre-existing diseases after waiting period. But, actually they don’t. I think all these companies need to clarify on there exclusions part.

Ankit-The wide definition is enough to reject the claim. Hence, be careful while entering.

Hi,

I am looking for health insurance for my parents both aged 58 to be covered under section 80 D.

My father takes BP pills regularly. Plz suggest a good insurance plan for sum insured 5 lakhs

Univesh-Refer my earlier post “Best Senior Citizen Health Insurance in India-Product Comparison“.

Hi ,

My parents have yet to cross 60 for Senior Citizen plan.

I just talked to a policy bazaar agent , they suggested for Max Bupa Health Companion

Star Health Optima and Religare Care .

Which one is good ? please suggest

Thanks.

Lalit-All THREE.

Hi Basu,

Is it good to buy directly from Max Bupa or third party like policy bazaar , bank bazaar or medimanage ?

Univesh-I feel to go through the agent of your nearby area than these online portals. Because he may be handy in case of claims.

How is bharti AXA as a company? Do you think they will be able to scale up in India? Which is the best GI online site to book a policy

Nolen-It is good old company. Regarding their scalability, I can’t say anything. To book a policy? Can you elaborate more?

hello my name is vikesh barla residing at port blair andaman nicobar island . i am new in mutual fund .please give some information regarding how to invest in franklin india high growth compnies fund through sip .how to invest online through direct plan . what are the forms are required to be fill . whom to approach

Vikesh-You claim to be new and don’t know anything, but mentioning the particular fund. Let me know how you selected this fund and for what purpose.

Hi Sir,

Could you please suggest a suitable family floater for for around 10 lacs coverage ? My age is 39, wife-31 and kid is 3 yrs.Wish to take the plan in Calcutta but it should be covered all India.None of us, till date have any existing ailment.Looking for a policy which is reasonable in premium and having no copayment and good coverage of cash less treatemen of maximum diseases and other anciliary facilities.

Thank you in anticipation.

Best Regards,

Parijat

Parijat-Usually all insurance companies offer cashless benefit across India. You can check with Star,Apollo or public sector companies.

Thanks

Hello Basavaraju,

I am a 56 years old with no health problems. I have taken Good health plan from New India Assurance company. Many people are advising to shift to Star Health or IFFCO. Please advise since when I become old claim settlement is important to me.

Rama-Continue the same.

Thanks, I will continue

Hey Sir

I m vaibhav , 22years of age .Just started my job.Would like to know which company offers best health insurance for an individual…..was thinking about HDFC ERGO.

Vaibhav-Then go ahead with HDFC.

Hello Basavaraj Sir. I greatly appreciate your writings that I’ve been following for a while. Your knowledge has really helped me in not falling into an unknown trap in the name of health insurance. I’d be very grateful if you could help me in the final leg of choosing my health insurance plan.

I’m 34 yrs. old female residing in Delhi. These are the policies I’ve shortlisted for myself, listed according to preference with reasons –

1. Max Bupa Health Companion – for 100% recharge benefit, no room rent capping, covers physiotherapy and AYUSH benefit too, no deduction in NCB even in claimed years, covers all daycare procedures. (but premium increases every year and concerned about their claim settlement ratio)

2. HDFC Ergo Regain – for 100% restore benefit, no room rent capping, covers physiotherapy and AYUSH benefit too. pre/post is 60/90 days.

3. Apollo Munich Optima Restore – for 100% restore benefit, no room rent capping, high NCB @ 50%, pre/post is 60/180 days. (but doesn’t cover physiotherapy, Ayush benefit expenses).

Please help me choose the best one.

Thankyou Sir.

Binny.

Binny-I know MaxBupa costlier than others you listed. But if you feel Physiotherapy and Ayush benefits are MUST, then stick to it. Otherwise, my choice will be Apollo.

Its late, but I still want to thank you for your advice. I, eventually settled with Apollo Munich Easy Health. Thanks a lot for the good work you’re doing for others Sir. Be blessed!!!

Binny-This is great to know 🙂

Hello Basavraj,

Appreciate you as a policy advisor. I would like to go for family floater policy & short listed United India Insurance & New India Insurance.

Could you pls. let me know, with which company from above I should go for insurance ?

I am living at Baroda, Gujarat.

Rajesh-Both are good. Chose the one which you feel comfortable.

Hi Basav,

Want to take a family floater health insurance for me n my spouse & we are planning for child.

Need your suggestion regarding two health insurance :

a) National Parivar Mediclaim Plus – Premium is little bit higher.

b) L & T Medisure classic – a new player in market, hence worrying for the service.

Also please suggest if any other family floater option is there with more or same benefits & cheaper premium.

Thanks,

Subhajit.

Subhajit-Go with National Insurance (if features matching you. Look at Religare Care also.

Hi Sir,

Its a very good blog.I want to take accidental insurance ,health insuramce and critical illness for me and my wife.And

health insuramce and critical illness to my mother.

My age is 36,wife age is 27 and mother age is 65.I am looking good insurance.Suggest me good insurance company.I am looking for 5 lack Sum insured.its should cover Ayush ayurvedic tratment.

Vishal-You can chose health insurance by referring above post and below comments. Regarding accidental insurance, read my earlier post “Best Accidental Insurance Policy in India-How to choose them?“.

Sir, I’m living at Kolkata. I’m looking for a family floater policy (Me-35, Wife -35 & Son-05 years) for a sum of 5 Lacs with renewal upto 80 yrs. Interested in non private companies like National & United India but in confusion abt their CAPP ings & co payment. Pls suggest what policy should i opt/?

Ujjwal-Almost all companies these have capping and co-payment cluase (especially from public sector companies). So go ahead with the one, which you feel comfortable.

Hi,

I wanted to insure my mother who is 54 years of age for around 5 lakhs policy. She takes regular medication for hypertension but she is mostly healthy otherwise. Can you please suggest which is the best policy I should consider for her. We live in Goa in a city named Vasco. I wanted to take some policy within 15k and having minimum period to cover pre existing diseases with good reputation of covering during emergencies.

Adul-Whether anyone financially dependent her? If so then try your luck for buying term insurance. Otherwise, insurance is not required to her.

I want to go for health insurance for following members:

self (51 years)

mother(71 years – diabetic)

wife (43 years)

sister (43 years)

daughter(19 years)

Which one to opt? Family floater or individual

Krishnamurthy-Better to separate your mother and sister. Include you, wife and daughter in family floater.

Dear Sir,

I wish to take a Oriental family floater policy(Proposer will be me) for my parents completed age 59 (Father) and mother(56). My age is 30 yrs completed unmarried.

Budget : around 30k pa.

Medical history of father : daily medicines for BP, thyroid and acidity. Cataract operation done already on each eye. Thankfully Never admitted suddenly

Medical history of mother : daily medicines for BP, thyroid and acidity. Cataract operation done already on one eye. Thankfully Never admitted suddenly

Medical history of myself : admitted for jaundice in Feb -2012(claimed through group insurance of college). Admitted for appendicitis in May 2005(No claim made as I had no insurance).

My queries are as follows. Do reply to each query.

1. Which shud I take family floater or individual for my parents? Considering my parents age and history.

2. Oriental doesn’t have a medical check up till the age of 60.Do I need to disclose the medicine and hospitalization history of my parents and mine while filling online?

3. How much should be the sum assured?if I take family floater or individual?

4. Can I add later my wife, child later?

5. If I get admitted suddenly for some illness( not pre-existing) after 1 year, will the claim be accepted?

Ronak-1) Family floater (for your parents ONLY). 2) Yes, better to disclose. 3) It is hard to say (as I don’t know the city you stay and other details). But ideally it is better to have more than Rs.5,00,000. 4) You buy an individual separate plan. After marriage switch to the family floater. Separate your parents insurance from your’s. 5) Yes, if it is not due to an existing disease.

Dear Basavaraj,

I would like to get your thoughts on Future Generali – Future Health Suraksha plan. This looks like a good plan with very competitive premiums. I was researching on plans for my parents aged 57 and 47 and was thinking of finalizing Apollo Easy Health or Tata AIG Mediprime until i stumbled on this on your blog. I saw the claim incurred ratio and took a further look into the policies.

Any cons you see with Future Generali? Please share your comments. Thanks in advance!

PS: Appreciate the time you take out to respond to folks like us and put your thoughts on so many subjects out there. Few of them are a real eye opener 🙂

Singh-Plan looks good. However, if your entry is above 55 years then the maximum cover they offer is Rs.5 lakh.

Thanks for your reply!

I am considering it as the cover I am looking for is under 5 lakhs only.

Dear Singh,

Did you end up buying from Future generali ? how is the experience with them? and any idea about their claim settlements?

Thanks Basavaraj for the response for the earlier query!

I have another question – My mother recently turned 66. I had applied for Medical Insurance with Star ( Medi Classic) which they rejected. She takes medicine for Asthma. What are the alternatives I have? Is there a chance to get insurance from L&T or Oriental?

Paryushan-I am not sure, but check with insurers of you mentioned.

I would like to purchase one Individual Health Policy for my Son aged 22 years 6 months. He is presently studying. Which is better – New India Assurance or United India or Oriental Insurance or National Insurance or Any Private but Reliable Company with guaranteed and timely response.

Thanks!

Sen-Before selecting the insurance company, first look at what are your requirements. In my view public sectors are good. You can go ahead.

Hi Basavaraj,

I am looking for insurance for my in-laws, ages – ( 62 & 63 yrs ). There is no preexisting illness. I was considering L&T medical insurance Medisure Classic family floater, SI 4 lakh because of its features but I am not able to get any figures on its Claim Settlement Ratio and the feedback on its service.

Please suggest if L&T is a good choice or should I consider alternatives. Oriental is another insurer from PSU, I was considering.

Also,Please suggest if I should go for a family floater policy Or with individual policies of 2-3 lac each.

Thanks,

Paryushan

Paryushan-Please go ahead. For me, both companies are good. Better to go with family floater with life-long coverage (if possible).

Hi,

I am 35 years old and currently Diabetic. My father is planning to take a Health Insurance policy for me. We are living in Hyderabad. Can you please suggest me any good plans that are suitable for me. We are hoping to have a policy with least premium and reasonable coverage.

With thanks,

VKishore

Kishore-Check with Star.

Thank you Basavaraj

Sir,

Myself 39 years, have hypertension. My wife 35 years have cholesterol and scoliosis. 6 year old kid. We would like family floater plan.

I can afford premium upto Rs.20000/- per annum. I need life long cover.

My questions are:

1. How much amount of insurance coverage should I opt for

2. Should i go for family floater from more than one companies. Will it be beneficial

3. Private companies or public companies

4. What all medical check ups needed.

Sam-1) Ideally it should be equal to your yearly income. But there is no such standard formula regarding how much to buy.

2) Stick to one company.

3) Both are same. Before that understand your requirement.

4) It depends on insurance company you opt.

Thank You sir for your valid time.

Sir, myself(47), spouse(44),son (16) & daughter (14) having mediclaim 2007 from New India Assurance for 2,2,1 &1 lakh respectively since 2005. Now i am looking for a best family floater for 5 Lakhs. I have done a claim for my self in November 2015 for URTI.

Can you help me which is the best family floater without room rent cap. I can afford the premium upto 20K. My policy is going to expire on 16th January 2016. Before that i want to port the same to some other good company .

I gone through STAR, RELIGARE, CIGNA TTK, UNITED INDIA, BUT Getting totally confused which to be used. Please help.

Jacob-Why not with New India only?

Hi Mr Basu. Genuinely appreciate your efforts through this blog.

Existing Scenario : I am a 36yr old doctor residing at Mumbai and my wife’s the same age. My parents are aged 68 and 67 years.

My parents are covered under my brother’s company by a group insurance for SI of Rs 5lacs by Oriental Insurance Co.

I have a ULHP from ICICI Prudential for 5 lacs (with moderate risk- Balancer fund) and

my wife has the same SI of 5lacs from National Insurance.

Mother – Has hypertension, Diabetes and Lupus. Other family members have no major illness

Requirement : I want to increase the SI to Rs 10lacs each

We plan to have a baby soon

Queries:

1. Is it wise for me to continue in ULHP or should I shift (port out)to pure health insurance? My annual premium is pretty steep at Rs 15000.

2. As my mother has pre-existing illnesses, I was considering Star Red Carpet as the waiting period is 1 year as against 3-4 years elsewhere but there is clause for copayment (30% for non- pre-existing and 50% for pre-existing illness). Can you please suggest a better option?

3. For my father, I thought of Religare / Star.

4. Should I take super top- up family floater for parents to reduce premium?

5. As me and my wife have diff companies with diff policy renewal dates, I was told by Coverfox.com that I cannot take a floater top-up plan..So I must take individual super top ups.How do I add my children in future?

6. Are govt companies like National prompt like pvt companies or else, one has to extend hospitalization till the cashless claim is processed..

Please give me your valuable opinion at the earliest.

Regards.

Kumar-I think, it is the repeat comment and I already replied to it. Please check my reply.

Dear Sir

Please advise a good Health insurance policy for me 55 years ( preexisting conditions Hypertension and diabetic 2 ) my mother 70 years (preexisting conditions Hypertension and diabetic 2) wife 48 years and a son 22 years coverage between 7 lakh to 7.5 lakh. Should I go for family floater or individual -plan. please give your valubale advise

Nadee-Opt individual plan for your mother (It is hard to get the insurance for her age, but try your luck). In your case go with family floater. My choice will be public sector companies and in private Apollo, Max or Religare.

Dear Sir,

My mother age is 59 and she is fit n fine. I wish to buy a health insurance scheme for her to counter the unforseen medical problems. Please suggest the best.

Vijay-You can go with any public sector companies. In private, I prefer Star, Apollo or Max.

Hello Sir,

I have gone through the above schedule and discussion tags, comparing Incurred claim ratio b/w apollo, max bupa, religare, star , future generali and universal sompo I concluded religare, star, future generali and universal sompo has much better ratio than other.

I want to take an family floater policy for me and my husband. Kindly suggest which company policy should we opt for?

Also please tell me if there is any policy which covers maternity expense also and how about if we go for national and united insurance.

Kamini-In my view you can go ahead with Apollo, MaxBupa, Religare or Star.

Sir,

I am working in a private company . i want my family to be covered with health insurance and it should be long term .

a family is about – wife 31 years , two daughters – 3 year and 9 year and father – 63 years and mother 51 years

we are confused and kindly suggest some good health insurance for our family

Sundar-First separate your parents from your family. Buy them separate senior citizen health insurance plans and for you typical family floater. I suggest public sector companies for your parents and for you Star, Apollo, MaxBupa or Religare.

HI Basavaraj,

1. Is there any specific reason for recommending public companies for senior citizens (father 63 yrs and mother 58 yrs)?

2. Any recommendation of public sector companies with good services?

Nadeem-1) Claims may be easier and also the pricing of hospitals will be bit lesser than if you own private sector health insurance.

2) Only few there in this sector. I can’t name any specific.

Hi Basavaraj,

I am planning to take a Health Insurance policy for my parents both aged round 58-59 years. I have considered to buy Apollo Munich Optima Restore policy considering the benefits they offer. But after going through this article by IRDA on the claim incurred ratio, I am considering National Insurance Company too since their claim incurred ratio looks to be on a higher side which is important factor for me to consider as they are close to 60 years of age. But this report published by IRDA doesnt indicate the ‘Claim Settlement Ratio’ which gives info about claims processed Vs Claims submitted. I wanted to check this ratio of both Apollo and National Insurance and accordingly decide which one to go ahead with. Do you have this info? If yes, please provide and also suggest me which one to go ahead with among the above mentioned options by me.

Regards,

Sailesh

Sailesh-In case of health insurance it is claim incurred but not claim settled. Hence, neither I have that data nor IRDA.

DEAR sir,i am a 46 year old, my wife is 45 years, and 2 child.1st child is 13 years,2nd child is 8 years.

pl.sujjest me which company health policy is best for me.also advise me floater is best or individual is best.

thanks for your help in advance.

best regrds

gupta

Dhanunjaa-Chosse family floater. You can go with public sector companies or in private Apollo, Star, MaxBupa or Religare.

I am 60 years old and have pre-existing heart disease and taking medicines (no heart attack, stent etc). Based on the search, I found the following policies found attractive.

a) Star Health Cardiac Care; b)Star Senior Citizen Red Carpet.

My questions are:

1)Star Health Care is meant for some one already suffered by an heart attack. This is not the case for me. Can I buy it or go for Senior Citizen Red Carpet?

2) The policy premium of above policies are higher and there are limitations in coverage, therefore, I want to stop it after 4 years. Hence, I buy another policy now covering me and my wife (both ) in addition to the above mentioned policy. It means I will be covered by two policies for 4 years. Ultimately, me and my wife will be covered with lesser yearly premium and better coverage terms after 4 years. Is it correct planning, any legal issue in it?

Thank you

Thangaraju-1) Yes go for senior citizen red carpet.

2)Yes, go for floater than individual.

HI,

My Father & Mother are 52 & 47 respectively.

They are taking medicines for Thyroid. I have my Company policy cover for Parents Wife & myself for 5 Lakhs.

I am looking to buy Floater for parents for 4-5 lakhs. They are in Nagpur.

Please check if you can suggest :

1) Floater or individual for Parents

2) 4 lakhs or 5 lakhs

3) Good Health insurance company & plan

4) Buy from Agent (like coverfox,etc) Direct from company is good

I have compared many companies but not able to come to conclusion.

Regards,

Rohit

Rohit-If they have some health issues then it is hard for them to get insurance. I suggest to buy separate family floater for both of them. Check with public sector companies. If none of them come to your help within your budget, then I suggest to opt for super top up options.

Thanks. But I said they dont have any health issue. Only Doctor has suggested to take medicines for Thyroid. Otherwise they are completely fine.

And all the companies like ICICI, Bajaj, Apollo, Religare, HDFC . ready to give policy.

Just i need your support to know which company is preferable.

Dear Sir,

I want to know about the Cigna-TTK Healthcare Plane ? What is your comment about Cigna-TTK ? I want to e take a 5 lacks policy for me, my wife and our child .. Please share your comment…

regards

Debajit Sarma

Debajit-I am not sure about their service as they are new entrant.

Hi Basavaraj

Thank You very much for this article. It helped me better understand the health insurance ecosystem.

I had an individual Bharti Axa basic health plan with Rs. 2 lac sum insured which expired on 29 september 2015 after three continuous renewal. I got married in June this month and thought of going for a suitable family floater plan. After searching for several polices, I found Universal Sompo individual essential to have the most benefits (including maternity and convalescence benefits) and lowest premiums. However, I am concerned with regards to the claim settlement track record of the company as it is not a well known company in India. Would you recommend going for Universal Sompo?

Also is it possible to shift from one company (group floater) to other so that I don’t have to serve the waiting period again.

Neerajt-What about converting the existing policy into family floater?

Hi Basavaraj, the claim settlement for individual insurance was eye opener, which was amazing analysis. I am looking a health insurance for my mother who is 61 and perfectly healthy with no pre-existing condition, so i don’t want to spend much on premium for 3 lac coverage. Can u suggest public and private insurance which is under 15 k per year?

sanathan-Check with public sector companies and in private, check with Star, Apollo, Maxbupa or Religare.

Hi Bro,

I wanted to buy a Health Insurance policy, I Shortlisted 3 Companies

Max, Apollo , Religare.

Plz suggest which one is best in term of claim settlement,

only one difference i found in max, will increase premium every year.

and my my second question is i also wanted to buy super top up, so i can go with L&T or Not.

Kindly suggest

Thanks in Advance.

Aditya-To me all are GOOD. Better to have super top up with the insurance company where you have basic plan.

Hello Sir,

Feeling great to find you here to get resolved my queries about Health Insurance.

I have a medi claim policy of New India, with sum assured of 1 Lakh. Rs., by last six years. Eight months back, I had gone through a hip replacement surgery (Left Leg) & I am perfectly fit & fine now. For this I got a full claim of 1 lakh Rs. as the total bill was 2.85 lakhs. Now I want to get insured for about 5 Lkhs. but as per New India rules I can not increase the sum assured for next 2 years as insurance has been claimed this year. So I want to shift to another insurance company for multiple reasons as follows.

1) The New India premium is costly than other private insurance companies.

2) If I wait for two years, then It will take 2 + 4 total 6 years to get eligible for getting insured for PREEXISTING diseases.

3) It’s good to get all processing through online, nowadays, instead of chasing policy agent.

4) Today I am 44 yrs 7 months. If I shift to other insurance company I will be saving myself going through medical tests as it is mandatory after 45 yrs for some companies.

Considering all this what is the best insurance, in your opinion, for me. Sometimes I feel that I may have to go for knee replacement (for right leg), in next 4 -5 years. I just want to get eligible for availing this claim benefit before that. Apart from this I don’t have any other health related issues.

I was just thinking of Apollo, Star or HDFC Euro.

Is any one of them fits best for me?

Your opinion will be of great help. Please comment.

Tanks & regards

Atul

P. S. : Is it true that in case of preexisting disease you can’t buy insurance online?

Atul-What I suggest is, let the current health insurance be continued and buy the new one with declaration of current health issue. What will happen in this case is, your future knee replacement cost will be reimbursed with existing insurance if the claim is within a 4-5 years. If the period is beyond that, then you get the full benefit from old and new insurance. Because all insurance companies issue you a policy with a condition of waiting period. Hence, you may feel hard to get reimbursement for your immediate medical cost.

Check with existing insurer about the super top up facility available or not. If it is, then go for top up or super top up facility with same insurer. This may relieve your headache and also cost. There is no such rule that with pre-existing diseases you can’t buy insurance online. You can buy it but with exclusions.

Sir,

i am searching for health insurence policy.. every insurence companies telling same befits and approximately same premium cost..

but when i read the reviews regarding their companies many people wrote very badly..

i am totally confused to take policy…

star, L&T, relighare,appolo all are apoke to me and told their benefits,.. but customers who already took their policy saying that there are many claiming issues. if i raise same point with policy employees they are saying it is not like that..

what shoould i do?? on what basis i can select health insurence policy???

please sir.. give me suggestion…

thank youu

Chand-When you check the reviews, dig in deep and find for what purpose they rejected the claim. In many cases, especially in India, people think of health insurance only before they find any such health issues which costing them. They look for health insurance and end result is rejection. At the same time, many in wrong belief that for whatever claim, insurance company is there to pay the dues. It is not like that. You must understand how it works and what are exclusions. If your claim is right one, then forget about insurance company, even GOD can’t protect them in paying.

Hi Basu,

I appreciate this blog, it’s quite helpful.

I am looking for Health Insurance for my mother who has recently undergone Spinal surgery. I have approached Apollo Munich, they said they cant offer her policy due to Spinal surgery and similar response from ICICI Lombard. Based on discussion so far, Bajaj Allianz and Max Bupa look promising, with 2 years waiting period.

I know we don’t have much choice due to her pre-existing condition, but wanted to check with you if you can suggest any other Health Insurance provider who offer Insurance for people with Pre-existing condition.

Regards,

Priyank

Priyank-Better to go with any one of two with the condition of waiting period. Check with public sector companies too. They may be generous to some extent.

Dear Basavraj Ji, I am thinking of taking religare heath insurance family floater policy for 25 lacs. Do suggest me is choosing Religare is a right decision now and also for future in case there is a requirement.

Thanks

Anil N

Anil-I personally own this policy.

Plz don’t buy with Religare .u will repent in future.plz take from any other company

John-May I know your bad experience on the same?

I am looking for a health insurance policy for my grandmother who is 74 years old. She doesn’t have an existing insurance policy. She has no pre-existing diseases as far as my knowledge goes. I would like to have a cover of about 3-3.5 lakhs for her. I would still like to have her go through a pre-insurance medical test just to confirm she has no ailments which can result in a claim being rejected in future. Researching online I could only find offerings from private insurance companies. I am not quite sure which one to go for and what their claim settlement track record is like in individual insurance policies(especially policies for the elderly). If possible I would prefer the lowest co-payment possible and not an insanely high premium(Not more than 25-30k ideally).

Could you suggest which would be the best option to go for?

Gurdit-Check with National, New India or United.

which health insurance company is better? relicare or appolo munich or bharti axa.. please help me

Mayank-To be all SAME 🙂

dear sir which company is better from these companies in the basis of network kospitals , service, clam ratio , biggest company in india and with out tpa

please send reply

thanks N.Sreenivasulu

ANDHRAPRADESH & Telangana States

Sreenivas-Among which companies?

Apollo Munich, Cignattk, Maxbupa, Riligare and Star health

Dear sir which health insurance company is better from these companies like Apollo Munich, Cignattk, Maxbupa, Riligare and Star health on basic information of claims ratio, services, network hospitals, good product for people and low premium but maximum which is better company from sreenivasulu

Sreenivasulu-Your expectation is high and there is no such company which we can say PERFECT.

As for tell maximum, but not 100 percentage give rank from these companies like Apollo Munich, Cignattk, Maxbupa, Riligare and Star health give rank for above component as your information

Sreenivasulu-Apollo, MaxBupa, Religare, Star and Cigna.

hi Basavaraj,

hope you are doing well , my name is ram tiwari and i am 35 years old i want want to take a 3 lac health insurance policy foe me my wife and my son , please inform me about the best plan available . I have checked with HDFC ergo and Max bupa but i am confused please help, thank you

Ram-What is your confusion?

hi Basavaraj,

hope you are doing well , my name is ram tiwari and i am 35 years old i want want to take a 3 lac health insurance policy foe me my wife and my son , please inform me about the best plan available . I have checked with HDFC ergo and Max bupa but I am confused in choosing the insurance company ? which company should i go with HDFC ergo or Max Bupa ? please reply in selecting one, please suggest, thank you in advance!

Ram-What is the confusion?

Hello Basu

I have a medical policy from bank group insurance through Universal samphoo

covered 4 lakhs and now three continious year without claim over . this is family floater policy. now i am eligible for pre exhisting disease .

when I buy this policy, after 3 months I met with BP and start takikng BP medicine and my wife after one year taking BP and thyroid medicine ( .25 ) as per Dr advice . The policy was without medical checkup . My age is 52 and my wife age is 50 and my daughter age is 22 apart medicine there is No health issue. During the second year I was hospitalised with Dengue fever there was problem ( Delay ) with claim settlement. I have to wait for full day in the hospital.

1. My question is I want to raise SI amount for another 3-4 lakhs due to costly medical expences with less premium

the same company will do it or not

2. After 55 years there is Co-payment of 20% . But I want a policy without co-payment suggest good insurance company with less premium Because in this policy the premium is 9k

3. My worried is whether the insurance company will do my insurance or not

Sir you are requested to suggest me

thank You

Praveen-1) This being a group insurance, I suggest to raise your doubts with bank. Because I don’t know the details of plan. 2) I don’t think they allow you to continue with less co-payment. 3) Check with bank.

sir

can I buy super top up plan

If yes than what is super top up plan

and which health service provider is good PSU or Private

Praveen-Recently I wrote a post on this, please go this post “Top Up Health Insurance Plan & Super Top Health Insurance Plan-What are they?“.

Hi Sir,

Hope you are doing well.

I have Dedicated health insurance policy (DHS) of 4 Lakhs. i got this policy through my current company. its a cashless insurance policy and it will expire in a month. i would like to renewal but our company is planning to proceed with a different company insurance policy. i spoke with DHS customer care people that i am interested to continue the policy and they said its should be done through my current company only. But my current company was not interested to go with that policy. i dont now the reasons. but we really like that policy. is there any possibility to continue the policy or else do let me know the best policy for me and my wife and parents. I am planning to take health insurance for my family and that should be Cash less medicalim policy. Please suggest.

Looking forward to hear from you soon

Chaitanya-There is no such product or company called DEDICATED HEALTH INSURANCE POLICY. Yes, it is purely your employer’s call to continue or go with new insurance company. Also, you can not single handedly continue this policy on your own. Because your policy comes under Group Insurance. If apart from your employer insurance, you want to have your own then check with Star, Apollo, MaxBupa, National, Religare.

Hi Basavaraj,

Thank you very much for sharing your knowledge here. I have spent some time on researching a new policy for my parents.

Can you help me in finding an answer to below mentioned questions?

Background:

Father – 59 years (Paralysed 15 years back) but has been fit since his paralysis stroke.

Mother: 53- Fit

I was thinking to buy insurance for my parents for a family floater plant. Since most of the companies claim that they could insure people with pre-existing diseases, I knocked doors of all the private companies including Max Buppa, Star Health, bajaj, ICICI Leombard, HDFC Egro etc. The strage thing about all these private clowns is that they say and write something but mean something. I called everyone and ,after hearing that father haa paralysis stroke, 15 years back everyone has denied me an insurance.

The worst is bajaj who never replies to e-mails and I wish they had any courtesy, if at all.

Now, I have moved on to private. After visiting National health Insuarce’s offce, they recommed that you buy an insurance policy through banks and that would be without a medical check up so they could avoid paper work and we could avoid medical tests though I am fine getting medical tests so that we get it right.

Can you explain what are consequences if we buy a health insuarnce floater policy through bank-say Bank of India? I know that the policy would bbe actually given by National Health Insurance.

Are there any downsides of buying through bank? What are they?

Having gone through stats, Public Health Insurance Companies seem to be reasonable whilst claiming back. What would you recommend?

Though I don’t have much choice for my father, would you recommend buying a separate policy for my mother from private company?

Which of the public companies out of 4 is the best in terms of services or claim setllements?

I would appreciate if you can help me and would be more than happy to pay any consultancy charges to you for sharing your knowledge.

Many thanks,

Yaman

Yaman-Sad to hear about your stories. But again public sector Nation Health played a trick here. When you buy a regular health insurance from them and claim arrives, in that case they may be under loss. Just to avoid this, they recommended a group insurance offered by a bank. By doing this, even if claim arises then their loss is less. Please check the plan features offered by bank. If it really suites to you then go ahead. My suggestion is to separate your mother from father insurance policy. Buy the insurance for your mother from private or public sector companies of your choice. In my view, all public and private sector companies are equally good and bad.