HDFC Bank offering a special deposit for senior citizens naming it as HDFC Senior Citizen CARE FD. HDFC Senior Citizen CARE FD Vs SBI WeCare FD Vs Senior Citizens Savings Scheme (SCSS) – Which is the best?

A few days back I wrote an article comparing SBI WeCare FD with Senior Citizen Savings Scheme (SCSS). You can refer the same at “SBI WeCare Deposit Vs Senior Citizens Savings Scheme (SCSS) – Which is the best?“.

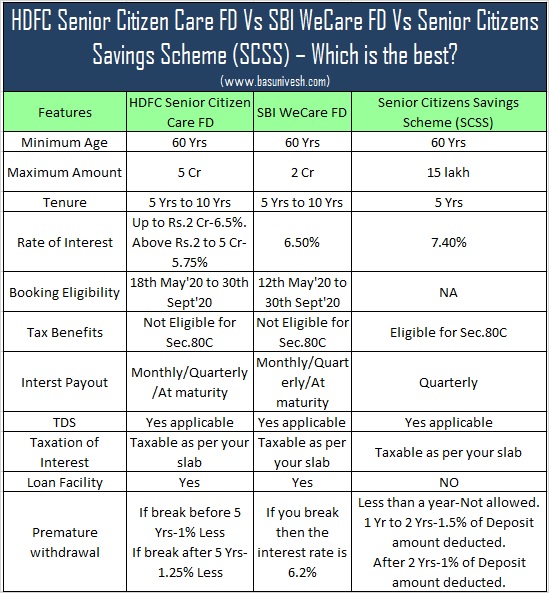

Banks are offering these special rates as they are flooded with liquid cash and also considering the situations due to Covid-19. But it does not mean you have to BLINDLY go for such FDs. Because there are few thigns which you have to consider before buying these FDs. Like what is your requirement, liquidity, premature closure rules, interest rates offering or taxation issues.

HDFC Senior Citizen CARE FD Vs SBI WeCare FD Vs Senior Citizens Savings Scheme (SCSS) – Which is the best?

Effective from 18th May’20 to 30th Sept’20, HDFC Bank offers a special senior citizen CARE FD. The features are almost the same as SBI WeCare FD.

You noticed that in many cases both SBI WeCare and HDFC Senior Citizen CARE deposits are the same. However, the SCSS still holds good and the best choice for you.

The premature withdrawal rules are easy in the case of SCSS. However, in the case of HDFC FD, you end up earning less of almost 1% from the current 6.5%. Hence, even if we compare both SBI and HDFC FD, my choice is SBI FD over the HDFC FD.

Conclusion:-After comparing HDFC Senior Citizen CARE FD Vs SBI WeCare FD Vs Senior Citizens Savings Scheme (SCSS), obviously SCSS is the best choice. The only negativity with respect to SCSS is the maximum limitation of Rs.15 lakh. Choose the one which is best suitable for your requirement.

Refer our latest posts:-

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

Dear Sir,

Can I nominate my only child who is presently studying in the USA on a student F1 Visa, and maybe a NRI by now, in a SCSS (Senior Citizen Savings Scheme) that I plan to open.

I believe nomination is now mandatory and I have no other person to nominate.

Some banks are suggesting that I cannot nominate my NRI son.

I find this restrictive.As I have only one child ,there is no one else who I can nominate.

Surprisingly private sector banks have this restrictive nomination clause printed on their SCSS form ,while post office and public sector banks do not.

Please look into this restrictive clause and correct it. A father should be allowed to nominate his son. If not,then this will be against Natural Justice.

Please advice me.

Thank you,

CA.Sanjay Agarwal

Dear Sanjay,

I have replied to your email.

I am 70 yrs ( DOB : 05.07.1950 ) & my wife is 65 yrs ( DOB : 04.02.1955 ) of age . Is there any health policy available for us ?

Dear Rupak,

Check with Star, MaxBupa and HDFC ERGO.

Dear Sir,

Two questions :

(1) Can a person stagger his investment into SCSS over a period of say 5 years or even 10 years. The point here is that since there is 80-C rebate allowable for this investment, therefore if I make total investment of Rs. 15 lakhs in one go, then, I will be able to utilize 80-C benefit only upto Rs. 1.5 lakhs and rest is of no use. But, if I am allowed to either stagger my investment, say, @ Rs.1.5 lakh per year or if I can open separate accounts every year, then it is very good from tax and 80-C benefit point of view.

(2) Whether the rate of interest, currently at 7.4% is fixed till the end of the scheme period or the rate of interest is open to change/review by GoI at some frequency.

Dear Kamal,

If you stagger in such way, then to park this total Rs.15 lakh, you have to do it for 10 years. Where you keep the remaining Rs.13,50,000? We have always such a mindset to save tax by hook or crook. At the end, we are in big trouble. Neither gain nor profit. Don’t think too much.

No, it is fixed for the entire period for you.

Ha ha. Liked the comment “save tax by hook or crook”.

In fact, staggering the investment over a ten year period would be foolish also. You never know whether the scheme itself would exist or not.

Just an idea came to mind and therefore asked for clarification.

Thank you so much for the clarification.

Dear Kamal,

There is no harm in discussing ideas 🙂

Really I am your fan and ardent follower. I have one question on PMVVY i.e.

What about people who have purchased it prior to march ,2020 @8%, Will their rate be reduced? If so it’s breach of trust.

Dear Rajinder,

They will get 8% fixed.

Hi Basavaraj,

Your comparisons as and on new schemes/products is really useful. This assists us to make better decisions.

Thanks and keep up the good work. I do read most of your articles and learn with every article.

Thanks

Hemanth

Dear Hemanth,

Pleasure 🙂