Pradhan Mantri Vaya Vandana Yojana (PMVVY) 2020 – 2023 now came up with five major changes. Pradhan Mantri Vaya Vandana Yojana (PMVVY) is now extended up to 31st March 2023. However, the Government changed certain rules with respect to PMVVY. What are those important 5 changes?

Features and Eligibility of Pradhan Mantri Vaya Vandana Yojana (PMVVY) 2020 – 2023

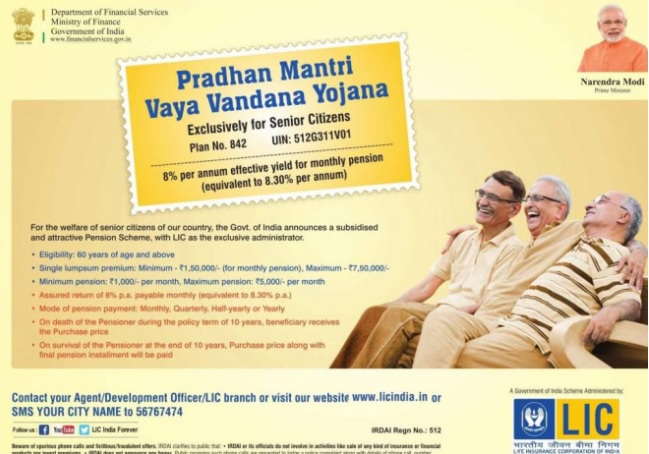

Let us now discuss about the features and eligibility of Pradhan Mantri Vaya Vandana Yojana (PMVVY) 2020- 2023.

Some other features of this product are as below:-

# You can surrender this policy during the policy period under certain exceptional circumstances like pensioner requires money for treatment of any critical/terminal illness of self or spouse. Surrender value payable will be 98% of the purchase price.

# You can avail the loan facility after completion of 3 policy years. The maximum loan payable will be 75% of the purchase price. Interest on the loan will be recovered from the pension amount.

# If the pensioner suicide during the policy period, then his nominee or legal heirs will receive the full purchase price.

# Pension is payable at the end of each period, during the policy term of 10 years, as per the frequency of monthly/ quarterly/ half-yearly/ yearly as chosen by the pensioner at the time of purchase.

# The scheme is exempted from Service Tax/ GST.

# Pradhan Mantri Vaya Vandana Yojana (PMVVY) scheme does not provide tax deduction benefit under section 80C of the Income Tax Act. Returns from this scheme will be taxed as per existing tax laws.

# There is no TDS on this product.

# Pensioner have to submit the Life Certificate on yearly basis through online “Jeevan Pramaan” mode. The pension will be issued after the submission of Life Certificate.

Benefits of Pradhan Mantri Vaya Vandana Yojana

The benefits of this plan are as below.

# During the policy period

The pensioner will receive the monthly, quarterly, half-yearly or yearly pension as he has opted during the time of buying.

# Death Benefits

On the death of the pensioner during the policy term, the Purchase Price will be refunded to the nominee (or legal heirs in absence of nominee).

# Maturity Benefits

If the pensioner survives up to the end of the policy term, Purchase Price and final installment of the pension will be paid to the pensioner.

How to buy Pradhan Mantri Vaya Vandana Yojana (PMVVY) 2020 – 2023?

You can buy a PMVVY scheme from LIC. The scheme is available via both offline and online mode. You can visit the nearest LIC branch or log on to the official website of LIC to purchase this annuity scheme. A policyholder has an option to return the policy within 15 days of the purchase. If the policy is purchased online, the free look period is 30 days.

For offline purchase, you can buy through Cheque/DD.

Pradhan Mantri Vaya Vandana Yojana (PMVVY) 2020 – 2023 – 5 Changes you must know

You now understood the features of Pradhan Mantri Vaya Vandana Yojana (PMVVY) 2020. Let us now see the changes done to the PMVVY.

# PMVVY now available up to 31st March 2023

Actually PMVVY was closed on 31st March 2020 itself. After that Government not extended the date. Now, they have extended the date up to 31st March 2023. Hence, it is available for the investors up to 31st March 2023.

# Interest Rate for FY 2020-21 reduced

Earlier the interest rate on PMVVY was 8%. However, now for FY 2020-21, Government reduced the interest rate to 7.4%.

# Yearly change in the interest rate

Earlier, it was not such a practice to revise the interest rate of PMVVY on yearly basis. However, now the Government changed this rule. From now onwards, it will be changed on a yearly basis.

Do remember that suppose if you pruchased during the FY 2020-21 then the current 7.4% interest is applicable for you for throughout the 10 years period. The change in interest rate on yearly basis is applicable to the new buyers only.

Hence, existing buyers will enjoy the interest rate for next 10 years which is at the time of purchase.

# Minimum investment required is revised

The minimum investment has also been revised to Rs.1,56,658 for a pension of Rs.12,000/- per annum and Rs.1,62,162/- for getting a minimum pension amount of Rs.1000/- per month under the scheme.

It was earlier Rs.1,44,578 to avail a yearly pension of Rs.12,000 and Rs.1,50,000 for getting a minimum pension amount of Rs.1,000 per month.

It is all because of reduced interest rate from 8% to 7.4%.

# Interest Rate is linked to SCSS and Finance Minister will decide the interest rate

Annual reset of the assured rate of interest with effect from April 1st of the financial year in line with the revised rate of returns of Senior Citizens Saving Scheme (SCSS) up to a ceiling of 7.75% with a fresh appraisal of the scheme on breach of this threshold at any point.

Delegating the authority to Finance Minister to approve the annual reset rate of return at the beginning of every financial year.

Review of Pradhan Mantri Vaya Vandana Yojana (PMVVY) 2020 – 2023

Considering the current trend, even though there are few negatives, but this product is worth to consider for senior citizens.

# No Tax Benefits-I may say this product as one more failure. Senior Citizens desperately looking for tax benefits or tax relief when they receive the pension. However, this product fails to meet that expectation.

# Liquidity-As one grows older, uncertainties related to health or other issues pop up. Hence, one must invest in a highly liquid product. However, in this case, liquidity is available in exceptional cases. Hence, it fails to understand the requirement of senior citizens.

# Inflation– This plan will give you the same equal monthly pension. But who will take care of raising inflation in terms of health issues or the cost of living?

# Maximum Ceiling-The The maximum pension one can avail under this plan is Rs.9,250 a month and the maximum investable amount is Rs.15,00,000. This means that one can’t sustain by depending on this product itself. It is hard for an individual to survive with meager Rs.9,250 per month pension.

# Returns-The only eye-catching in this product is a 7.4% guaranteed pension. But tax and inflation will eat this 7.4% return and in the end, you may have to survive with the negative real return. However, if one compares with FDs, then this product may be eye-catching.

# You can go ahead IF-You can go ahead and invest in this plan IF you are not concerned about your taxation, inflation, or not aware of other products like tax-free bonds or other debt products. Simple, straight forward, backed by Government and managed by LIC are the positives of this product.

# No Age-based purchase-Unlike Jeevan Shanti, which is also LIC’s immediate annuity plan, in this plan the purchase price is fixed. It is not dependent on your age.

Conclusion:-Considering the current falling interest rates and scary debt funds, it is a product made for senior citizens. I suggest you to go ahead and utilize this product to the maximum.

Our recent posts:-

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

Death of insured on 26july 2022 but recd pension or interest on 23sep2022 but it’s calculated till death date who will pay 2 months interest? Can I claim or complain to redressal authorities.

Dear Shivakumar,

It may be due to procedural delay.

Can I have both PMVVY and SCSS both together exceeding 15 lakhs?

Dear Animesh,

Yes.

Can I retired State/Central/Defence employee receiving service pension join the PMVVY ?

Dear Padmanabhan,

Yes, he can.

Hi,

While submitting application for pmvvy, it asks for aadhar, bank details and address and finally a payment button shows. Does this mean we don’t have to submit any document thereafter. Also, is the policy document sent in email? . Can you please help with this query.

Dear Sib,

It is the KYC process and once done means over. They usually send it through physical mode.

Can the original bond of PMVVY scheme be submitted at any branch of LIC at the time of redemption or only to the branch of issue? During 10 years the policy holder can change his place of residence many times and will live far away from the place of issue.

Similarly, can details of change of nominee, bank, life certificate etc also be given at any branch of LIC in India?

Dear Rangarajan,

Currently, it is to the said branch. In future, we don’t how friendly the LIC will turn.

Sir, If I invest in PM Vaya Vandana Yojana Rs 15 lacs at a particular branch of LIC, at the end of 10 years, should I surrender the original bond at the same branch or to any branch of LIC in India? Because 10 years are a long period and I may not be living at the place of issue of the policy.

Can I likewise contact any branch of LIC for change of bank details or change of nominations etc. please clarify. Thanks

Dear Rangarajan,

Currently, it is to the said branch. In future, we don’t how friendly the LIC will turn.

Hello Sir,

1.My mother has FD in the bank where her annuity for PMVVY gets credited. Does she need to submit two separate 15H form one for FD and another for PMVVY?

2.Kindly guide about point no.19 in 15H for PMVVY:

a) Identification number :

b) Nature of income

c) Section under which tax is deductible

Regards

Dear Susmita,

Yes, you have to submit two Form 15H.

Hello Sir,

Thanks for your reply.

2.Kindly guide about point no.19 in 15H for PMVVY:

a) Identification number :

b) Nature of income

c) Section under which tax is deductible

Waiting for your valuable reply.

Regards

Dear Susmita,

Please refer my Youtube video in this regard.

Hello Sir,

Could you please send me the link. I could not find any video of yours regarding 15H fill up for PMVVY in particular.

It will be very kind of you , if you just tell me the Section under which tax is deductible , at least.

Regards

Dear Susmita,

Form 15H filling is same for all products and the form not change based on the product. Refer the link (https://youtu.be/sHZOEb0iV-s).

Hello Sir,

1. If I transfer money to my mother’s account and she invest that amount along with additional amount in PMVVY, does this money transfer attract any tax? PMVVY pension amount is taxable that I know, but does this daughter to mother money transfer attract any tax?

2. My mother, a senior citizen, does not have more than 3L income annually, and does not submit IT return. This year if she purchase PMVVY policy, does she need to submit IT return this year? If yes, does she need to continue submitting IT return?

3. If her annual income exceeds 3L but remains under 5L, does she need to submit IT return?

Kindly advice.

Regards

NB: Every time I am submitting comment it disappears after page refresh, and I have to again post it. Kindly look into the matter.

Dear Susmita,

1) The best option is to have a gift deed between you and your mother (in a plain paper). Once you gift that to her, whatever the tax liability is there, it is on her head. This way, you can reduce the tax liability.

2) and 3) It is better to file ITR.

Hello Sir,

Kindly let me know

1 )whether one has to pay GST on PMVVY premium amount?

2) For example if someone wants to buy PMVVY policy of 5lacs, does she need to pay additional GST over this 5lacs?

Regards

Dear Susmita,

Yes, you have to pay the GST.

Basu Sir – Small correction, you have typed NOT instead of NOW in “Let us NOT discuss about the features and eligibility of Pradhan Mantri Vaya Vandana Yojana (PMVVY) 2020- 2023.”

Dear Balaji,

Thanks for the suggestion. Yes, updated.

Hello,

If i invest in Pradhan Mantri Vaya Vandana Yojana (PMVVY) today (on 21st May 2020), rate of interest will be fixed for complete policy term of 10 years (which is 7.40% for Monthly Pension)?

Please confirm.

Dear Vivek,

Fixed for you.

It means that under PMVVY, you get 7.4% interest and under SCSS, you get 7.75%. Both are fundamentally inadequate and tax inefficient and inflation neutral or negative over an extended time period. Further, since in both the cases, the rate of interest is open to review/change every year, so technically, your ‘investment/contribution’ is tied whereas the returns are not fixed but variable. And in the falling rate scenario, no wonder, interest would drastically reduce over the next many years.

Dear Kamal,

In current scenario, who is giving you 7.4% and 7.75% (even if we consider the pre-tax)? Above that, they have secured product. Hence, for those who are looking for safety, constant stream of income and best returns in current scenario, these are the best.

Do remember that if you invest today, then your return on investment is fixed.

Thanks a the update ?..whether the limit of investment has been extended from earlier 15 lakh or not?

Dear Priyajit,

It is Rs.15,00,000. There is no change in that.

In article you mentioned maximum ceiling is 7.5Lakh right

Dear Vidya,

Sorry, I forgot to edit. The initial limit when it was launched was Rs.7.5 lakh and later increased to Rs.15 lakh.

Thanks for the update..was waiting for it & no wonder u r first one to cover after it got published in financial express. Just one query, r they charging GST on premium unlike erstwhile?

Dear Priyajit,

NO GST.