Effective from 18th March 2019, LIC is launching a new plan LIC’s Navjeevan Plan No.853. It is non linked, with profit, endowment plan. Let us see the features and review of this plan.

Why every year LIC will launch the single or limited premium plans from January to March?

If you check the history of LIC’s new plan launch period, you notice that every year LIC launches a new single premium or another type of plans especially during the months of January to March.

The reason is that, during this period around 99% of salaried running behind to search for tax saving investment options. Hence, to garner business from such salaried, every year LIC launch the new plan from January to March.

LIC’s Navjeevan Plan No.853 plan launch in the month of March is one such classic example (even though this time bit lately).

LIC’s Navjeevan Plan No.853 – Features and Eligibility

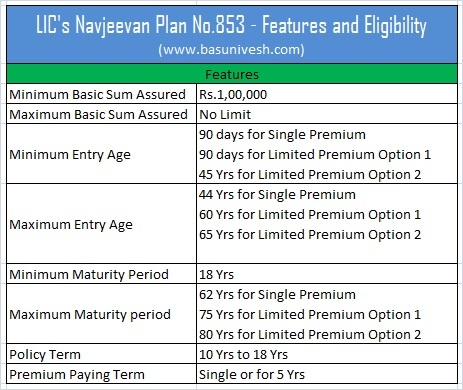

As I said above, LIC’s Navjeevan Plan No.853 is a non linked, with profit, endowment plan. Under this plan, the premium can be paid either as a lump sum (Single Premium) or as a Limited Premium payment option of 5 years. Along with above-mentioned features, below are the special features of this plan

Along with above-mentioned features, below are the special features of this plan

# You can buy this plan both either online or offline.

# If you buy the plan online, then you will get 2% discount in case of Single Premium Payment. However, in case of Limited Premium Payment Option, the discount is 5% on the total premium you pay during 5 years period.

# If your age is less than 8 years, then the commencement of risk will start either one day before the completion of 2 years from the date of commencement of policy or one day before the policy anniversary coinciding immediately following the completion of 8 years of age whichever is earlier.

# This plan offers Accidental Rider and the rider like settlement option rider (both in case of maturity and death benefit).

# In case of limited premium payment option, you can pay it yearly, half-yearly, quarterly or monthly.

# You can avail the paid-up option if you continuously paid 2 years of premium.

# You can surrender the policy at any point of time if you paid a single premium. However, for limited premium payment option, you can surrender it after 2 years completion.

# You can avail the loan under this plan. Under Single Premium, you can avail the loan after 3 months. The maximum loan available is 80% of the Surrender Value. However, under the limited premium payment option, after completion of 2 years, you can avail the loan up to 80% of surrender value (for in force policies) or 70% of surrender value (for paid-up policies).

What are Option 1 and Option 2 in LIC’s Navjeevan Plan No.853?

In the above image, I mentioned, again and again, Option 1 and Option 2. Let me explain to you what these options are in detail.

This Option 1 and Option 2 is applicable only for Limited Premium Paying option but not if you invested as a lump sum. Hence, if you paid as a single premium, then the death sum assured is 10 times of your single premium.

However, if you opted for a limited premium payment, then you have the below options.

# If your age is below 45 years of age.

You will receive the 10 times of your annual premium as a death benefit.

# If your age is above 45 years of age.

In this case, you have two options to choose from.

Option 1-You can choose for 10 times of annualized premium as a death benefit.

Option 2-You can choose for 7 times of annualized premium as a death benefit.

Benefits under LIC’s Navjeevan Plan No.853

Now let us discuss about the benefits available under LIC’s NavJeevan Plan No.853.

A. Maturity Benefit under LIC’s Navjeevan Plan No.853

If the policyholder survives until the policy period, then he will receive the Basic Sum Assured +Loyality Addition.

B. Death Benefit under LIC’s NavJeevan Plan No.853

# If death occurs before the 5 years completion of the policyholder-If death occurs before the commencement of the life risk, then LIC will refund the premiums you paid. However, if death occurs after the commencement of the life risk, then-nominee will receive Sum Assured on Death as a death benefit.

# If death occurs after the 5 years completion of the policyholder-Sum Assured along with Loyalty Addition will be payable to the nominee.

Meaning of Sum Assured on death

# For Single Premium Policies-Higher of the below will be payable

- Basic Sum Assured

- 10 times of Single Premium

# For Limited Period Premium Payment Policies-Higher of the below will be payable.

- Basic Sum Assured

- 10 times of Annual Premium (If Option 1 has opted) OR 7 times of Annual Premium (If Option 2 has opted).

LIC’s Navjeevan Plan No.853 Return Calculation

Now let us consider an example to understand the return calculation. I have considered the Life Assured age as 45 Yrs, Sum Assured Rs.5,00,000 and chosen the Option 1. Now the results are as below. You notice that the returns hover around 5% to 6%. Now it is your turn to decide whether it is suitable for you or not.

You notice that the returns hover around 5% to 6%. Now it is your turn to decide whether it is suitable for you or not.

LIC’s Navjeevan Plan No.853 – Should you invest?

# It is a typical financial year end product launch by LIC to garner the business from the employees who are looking for TAX SAVING options by hook or crook. Hence, no such surprise.

# When you look at features, LIC wisely made it a SINGLE premium and LIMITED period regular premium plan, where the premium payment option restricted to 5 years ONLY. The reason is to benefit these individuals who are in a desperate mode to save tax.

# LIC offering this plan in both ONLINE and offline mode. Hence, if someone really fan of this product, then I suggest going for an ONLINE mode where you will get around 2% discount on single premium and 5% discount on regular premium plan.

# When you check at above return calculation, you noticed that the returns are around 5% to 6%. Hence, do you feel it is worth to invest for such a long period and expecting around 5% to 6% returns?

# Many agents may say there is Life Insurance Coverage also. But to make them aware, nowadays even LIC itself offering term insurance at the damn cheap rate (forget about private players), then it is of no use to consider such Insurance+Investment product.

# I am stressing once again the basic funda of investment. Never combine your investment and insurance need. Also, never invest in a product just for the sake of TAX SAVING. The investment must help you to achieve your FINANCIAL GOALS but not the AGENTS FINANCIAL GOALS. Because for a single premium, the agent will earn 2% commission and for regular premium, a 1st-year commission is 14% (inclusive of first year 40% bonus commission) and subsequent years 5%.

Finally, beware of such products where such products neither suffice your Life Insurance needs (the ideal Life Insurance coverage should be around 15 to 20 times of your yearly income) nor it will give you a decent return (even fail to beat the returns of products like PPF).

Hence, there is nothing NAV (NEW) nor JEEVAN (LIFE) to have this product as your choice 🙂

dear sir

i am 35 year old and i have 2 small children of 2 years and 1 yer . i want to save fr their future education to go abroad. i have never liked LIC returns. can u suggest some plans currently i am only making fds

Dear Mehak,

You did right that you not touched LIC plans. However, it is hard for me to guide blindly.

Sir I don’t have understand of policy can you please deatails of policy deatails upload that you tube ,this policy is fake or real

Dear Anil,

If you can’t understand the features, then read once again. If you still have certain doubts, then you can ask me.

If the taxation aspect of the returns are not taken into consideration, I feel the analysis are incomplete. Please compare after cosidering the same. At present we are required to pay LTCG tax on equities too.

Dear Dilip,

Do you compare this plan with EQUITY? I consider this plan as a debt product. In that, I feel PPF is way ahead than this plan for return and taxation purpose.

Good Info. Thanks for sharing.

Dear Sir.

I am a 53 year old employee in automobile company

My retirement age is 60

Every month I left with 50k as excess over my all expenses

I have 50 K every month in MF SIP

I have PPF for my Son and Daughter 1.5 L per annum each

I want to have 50 k per month pension after 60 till 75 through usage of 50k left over excess monthly

Pl suggest a investment area

Dear Dinesh,

Accumulate the same through Mutual Funds in the ratio of 60:40 in debt to equity. Slowly come out from equity before the goal is around 3-4 years away.

Is it not cheating of gullible salaried people of the country to entice them to “Invest” in such instruments, that too by the “Government company”?

LIC coming up with such pathetic plans year after year which neither covers adequate risk nor inflation beating returns. Do “policy holders” know that they are getting poorer by buying LIC policy?

Dear Ritesh,

It is sad that LIC the oldest insurer forget the real cause of LIFE INSURANCE.

In Who is the good financial Planner means, Who oppose the LIC is not good that person is the best financial planner.

Why not checking the all other aspects of the plan.

What is the premium you are going save by investing a single premium in this plan to get 10 times of annual income? For 50 lakhs sum assured term we need to pay latest 20K per annul right?

What is the benefit portion of Pre tax using U/S 80C that also consider and Major benefit is TAX savings on maturity is very impotent. Even MF need to pay 10% tax on LTCG

Major thing it is a peace of mind to buy a LIC product with guaranteed returns.

LIC past experience on Jeevan sharee LA is good so in future LIC may generate good returns we can expect the MOre LA and also more returns.

Product will not suitable who are ready to take rsik in equity and this is good for who want to save tax and also get guaranteed returns with good life cover.

we are not recommending to invest all clients savings surplus in this kind of products, but small portion of allocation they can invest for short term

Dear Srinivasa,

I am not opposing certain plans of LIC like LIC’s Online Term Insurance, LIC’s online Jeevan Akshay VI and LIC’s PMVVY 🙂 But as an agent fraternity (I feel you too), can you canvas this product to your clients to buy them online (as they buy online, then they get additional benefit)?

Do you feel nowadays filling the gap of Sec.80C is a big thing? With EPF, PPF, kids tuition fee, Term Life Insurance premium, one can easily fill the gap of Sec.80C. Hence, don’t propagate that this is the ONLY product which will be eligible for Sec.80C benefit.

LIC’s LA for Jeevan Shree is good, but how much and whether the benefits of LIC’s Jeevan Shree and this plan features are same??

I am not saying that ONE MUST take equity. It is up to them to invest in equity or debt. But why not the products like PPF??

Basu ji..I saved my hard earned money. Yes it’s just a tax saving lat minute tool. But can u suggest good LIC plan. Also, which Term Insurance ( online ) is really very good, reliable and Cheap Too. Is lic term insurance good one.

Dear Ammy,

Never combine INSURANCE with INVESTMENt. Regarding the term life insurance products, refer my latest post “Top 5 Best Term Insurance Plans in India 2019“.

Hello Sir,

Once again thanks a ton, for providing your valuable views on Financial products, also for Educating people in simple way n words.

Dear Vinay,

Pleasure 🙂

whether the policy is covered under 80 c

Dear Ramakrishna,

YES.

Hi Basu sir, Really nice and educative article. I have never seen you being biased and always give your unbiased analysis. Keeping giving us information about such products. Thanks a lot

Dear Sat,

Thanks for your kind words 🙂

Nice information Sir. Thanks. Can you please suggest one good investment plan which should have a guaranteed return after 10 yrs. i want to invest for my child education.

Dear Chinmaya,

Sadly there is no such GUARANTEED plan for your 10+ years investment period.

Dear Basu Please suggest good Saving for long term for family pension from best financial institute…

Dear Arun,

Be specific with your requirement, is it for saving or INVESTMENT? Long term means how many years? Which as per you is the BEST FINANCIAL INSTITUTE?

if there is no guaranteed plan with you he can invest in LIC nav jeevan plan for regular payment option for 5 years. He will get 10 times life cover and guaranteed sum assured and also a LA as u mentioned above, mainly he will get the tax benfit in both 80C and maturity. what else we want to invest

Dear Srinivasa,

What is GUARANTEED in LIC PLAN? Only the Sum Assured right? Then why not LIC’s online Term Plan? LA or BONUS are not GUARANTEED. Hence, don’t misguide people.