There are certain changes to Health Insurance Tax Benefits 2018-19 (AY 2019-20) after the Budget 2018. Many of us have health insurance either from our employer or on our own. However, we forget to claim a few tax benefits. Hence, let us understand these changes in detail.

We all know the importance of health insurance in today’s costly medical hospitalization. Hence, it is imperative for many of us to buy health insurance. Otherwise, your one hospitalization of few days may dry up your whole emergency corpus.

Who can claim Health Insurance Tax Benefits under Sec.80D?

If you are paying the premium against health insurance in the name of below-mentioned family members, then you can avail the Health Insurance Tax Benefits under Sec.80D.

- Self

- Spouse

- Your Parents (Dependent or not dependent)

- Dependent children

Budget 2018 – Health Insurance Tax Benefits 2018-19 (AY 2019-20) changes

As I mentioned earlier in Budget 2018, Government made some changes to Health Insurance Tax Benefits. Hence, first let us revamp those changes.

# The maximum tax deduction limit for senior citizens under Section.80D of IT Act was raised to Rs.50,000 from the existing Rs.30,000.

# As of FY 2017-18, Very Senior Citizens (who are above 80 years of age), can claim a deduction of up to Rs.30,000 incurred towards medical expenditure, in case they don’t have health insurance. However, in the Budget 2018, it has been increased to Rs.50,000. Even individuals who pay premiums for their dependent senior citizen’s parents can claim the additional deduction on health insurance premium (or) medical expenditure

# In case of single premium health insurance policies having cover of more than one year, the deduction is allowed on a proportionate basis for the number of years for which health insurance cover is provided, subject to the specified monetary limit under Sec.80D.

Assume that your health insurance yearly premium is Rs.50,000. However, if you go for a two-year premium paying in advance, then the health insurance company is offering you the discount of Rs.3,000 i.e. for two years it the premium will be Rs.47,000.

Earlier, you are allowed to claim the deduction under Sec.80D in the financial year in which you paid the premium and that also as per the specified limits of Sec.80D. However, from FY 2018-19, you can claim the tax benefits under Sec.80D proportionately for two years. It means for the first year you can claim Rs.23,500 and next year another Rs.23,500.

Health Insurance Tax Benefits 2018-19 (AY 2019-20)

Now let us discuss more about Health Insurance Tax Benefits 2018-19 (AY 2019-20).

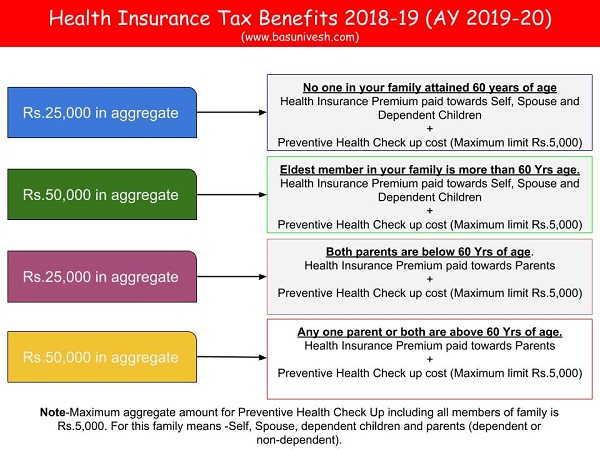

Health insurance premium paid for Self, Spouse or dependent children is tax deductible up to Rs.25,000. However, if any one of the persons mentioned above (Self, Spouse or dependent children) is a senior citizen and Mediclaim Insurance premium is paid for such senior citizen then the deduction amount will be Rs.50,000 from FY 2018-19 (AY 2019-20).

Same way, health insurance premium paid towards parents is eligible for deduction up to Rs.25,000 under Sec.80D. However, if any one of your parents is senior citizens (above 60 years of age), then the limit is Rs.50,000.

For senior citizens above the age of 60 years, who are not eligible to take health insurance, the deduction is allowed for Rs 50,000 towards medical expenditure.

Let me tabulate the same as below.

As I said above, along with above said benefits, very Senior Citizens (who are above 80 years of age), can claim a deduction of up to Rs.30,000 incurred towards medical expenditure, in case they don’t have health insurance. However, in the Budget 2018, it has been increased to Rs.50,000.

Budget 2018 – Standard Deduction in-lieu of Medical Allowance

Earlier you used to get a medical allowance of up to Rs.15,000 as an exempted benefit. To claim this benefit you have to submit the medical bills. However, effective from FY 2018-19, a standard deduction of Rs.40,000 in lieu of travel, medical expense reimbursement, and other allowances are available for salaried employees and pensioners.

To claim this standard deduction, there is no need to submit medical bills to your employer.

Irrespective of the amount of taxable salary you will be entitled to get a deduction of Rs.40,000 or taxable salary, whichever is less.

Hence, let us say a person has worked for few days (or) months and his salary was just Rs.30,000 for a financial year, then he will be entitled to a deduction equal to salary, which is Rs.30,000. Because it is less than the standard deduction of Rs.40,000.

If his salary in a financial year is Rs.3,00,000, then he can claim the standard deduction of Rs.40,000. Because in this case the salary is more than the standard deduction.

Few points before you avail Health Insurance Tax Benefits 2018-19 (AY 2019-20)

# The premium amount should be paid in non-cash mode only. If you paid the premium through cash mode, then you are not allowed to claim the deduction under Sec.80D.

# Meaning of Dependent Children in case of a male is that you can claim tax benefit on health insurance premium paid towards your male children up to 25 years of age (if he is unemployed). However, if he is above 18 years of age and employed, then you are not allowed to claim the tax benefits towards the premium paid on health insurance of such children.

# Meaning of Dependent Children in case of a female is that you can claim tax benefits on health insurance premium paid towards your female children up to her marriage and unemployed.

# You can’t claim the tax benefits if you paid the premium towards your in-law’s health insurance premium. However, your spouse can claim the tax benefits by paying the premium towards his/her parents (your in-laws).

# You have to claim the tax benefits towards the premium you paid but not towards the service tax or GST you paid.

# If you have purchased the life insurance policy with aCritical Illness rider, then Tax deductions on premiums paid towards such critical illness rider can be claimed under Sec.80D.

Hope now you got the clarity on what are the Health Insurance Tax Benefits 2018-19 (AY 2019-20).

Refer our other posts related to Health Insurance:-

- GST Rates on Life Insurance, Health Insurance and Car Insurance Premium

- Health Insurance by Banks – Should you buy?

- Multiple health insurance policies -How to claim from all?

- Top Up Health Insurance Plan & Super Top Health Insurance Plan-What are they?

- IRDA Incurred Claim Ratio 2016-17 | Best Health Insurance Company in 2018

This might be off topic, is travel insurance premium tax deductible?

Dear Vineeth,

Sadly NO.

I really like the way you have explained this complex stuff. I appreciate it.

Hi Basu, I am 38 yrs old and availing a health insurance policy i.e. Heartbit Silver since 2012 with a SI of 3Lacs for me and wife age 32 Yrs and premium is around 14K .I tried to renew my policy to Family First with 1Lac indv and 15Lac shared SI but Maxbupa is denying to upgrade the policy citing reasons of previous case history of claim for stomach ulcers ,so can I go for a portability option to increase my SI,please suggest what action should I take?

Thanks,

Vinit

Dear Vinit,

Why not go for super top-up policies to increase your sum assured?

I have corp group policy where i am paying premium of 40K for my parents & parent in-laws. Additionally, I have a family floater policy for which i pay premium of 35K. How much I can claim as deduction. My parents & in-laws are above 60years.

Please elaborate. I am really confused.

Dear Sunil,

You can’t claim on in-laws premium. However, you can claim benefits for you and your parents as I explained above.

If health insurance policy premium one time payment for life time coverage then how to claim on proportional basis,?.if it is for 3 years we can divide premium by 3 and then claim.if it is for lifetime how to do it?

Dear Srinivasan,

Do any health insurance product provide this option of payment of one time and coverage for LIFETIME? Please let me know.

1. Is it possible to have multiYear ( more than 1year) health insurance ? My agent tells me it has to be yearly……

2. Which is better – Family floater mediclaim or mediclaim 2012…for family of three persons ( husband/wife/son)?

Dear Nil,

1) Yes, you can have so.

2) Family floater.

As a sr citizen abkve 60,i am not eligible for health insursnce. I am also a pensioner. Can i avail upto 50,ooo towards medical expenses in addition to stanfatd deduction of

40, 000. B. D. BAWEJA.

Dear Baweja,

Medical expenses under which section you are referring?

A very informative piece of advice. I would like to know which are the economical and best health insurance available for a family.

Dear Ratan,

BEST and ECONOMICAL not go hand in hand.

Dear Basu,

Awesome information across the blog, thanks for all your hard work. I have a quick question. I see that taking extra rider for critical illness is not recommended along with a term plan and also you mentioned that separate Health Insurance plan only for Critical Illness may not be a good choice due to its complex nature. So besides office provided health insurance if we take an additional family floater ( me + wife + daughter) of 20 lakhs, does it makes sense? In that case what is the backup plan for super critical illness like cancer (cost 40+ lakhs) etc?

Dear Sanjay,

Beside your employer-provided health insurance, you must own a family health insurance, However, if your family have a history of critical illness, then better to opt separate critical illness cover.

I like your way of work.

please guide me how I associate with you for future benefits.

Dear Harsh,

I am not sure what you are looking from me. Can you elaborate more?

I like ur all articles.. Thank u for enriching our knowledge.

Dear Nirav,

Pleasure 🙂