The biggest goal of an individual’s financial life is to plan for Retirement. Hence, the financial industry came up with so many FANCY Retirement Calculators. You just have to input the data and within few minutes you end up with desired numbers to achieve the retirement goal.

Is Retirement Planning is so easy? Whether we must trust these calculators and start investing? Let us go into some side effects of such retirement calculators.

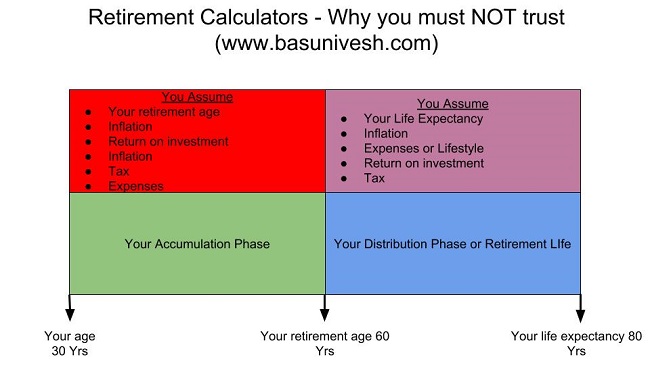

When someone plan for retirement, then there are basically two stages. One is the accumulation stage and another is the distribution stage.

During the accumulation stage, you start investing to accumulate the retirement corpus. This invest is again based on the time horizon of the goal and the asset allocation you prefer.

During the distribution stage, you start to withdraw from such accumulated corpus (which you accumulated while you are working) for your retirement life. Both these periods of accumulation and distribution stages are definitely long term.

Let us first understand what are all the data you need to input in such retirement calculators to arrive at the required investment towards retirement goal.

- Your current age

- Your retirement age

- Your life expectancy

- Your current monthly expenses

- Expenses which you have to consider during retirement age

- Inflation rate during the accumulation phase

- Inflation rate during the distribution phase

- Returns on investment during the accumulation phase

- Returns on investment during the distribution phase

- Taxation during the accumulation phase

- Taxation during the distribution phase.

- Certain retirement investments which you have to link to retirement goals like NPS or EPF.

Let me show the same in a graphical way.

You notice that the complete retirement calculators depend on so many ASSUMPTIONS!! If one assumption goes wrong, then your retirement life will be a CURSE.

Retirement Calculators – Why you must NOT trust

Let us discuss one by one like how such assumptions may be disastrous for your retirement life.

# Retirement Age

Assumed that you are going to continue your working life up to 55 years or 60 years. But what if suddenly there is a financial crash in your industry and due to which you completely out of job?

What if your health unable to protect you to work for so long year of 55 years or 60 years of age? You have to end up your profession and forcibly start retirement life at the earliest.

Assume that you both mentioned above things are going well up to your retirement age. However, due to stiff professional competition, your employer may feel that you are unfit as you grow older. Because an employer may feel that cheap, young energetic and up to date knowledgeable guy can easily handle the task, then what is the point in employing you?

So never think that even though you planned to work up to the age of 55 years to 60 years, but be ready for early retirement. Also, remember that EARLY RETIREMENT in many cases is a CURSE (especially when it is unplanned).

# Inflation

During the calculation of retirement, we consider inflation during your accumulation phase and also during the distribution phase. However, the inflation number what you enter may be average and AVERAGE NOT APPLY TO INDIVIDUAL.

It may be higher or lower. If the inflation is higher than the actual inflation what you go through, then it is fine. But what if the inflation is lower than the actual inflation?

You have to sacrifice your retirement life in many ways.

# Expenses

Many of us are in a wrong belief that expenses will come down during our retirement life as we do not spend on our travel, lifestyle expenses or some other expenses which we usually experience when we are young.

But the reality may change drastically. What if you have serious health issues during your retirement days? What if your kids turn to be your LIABILITY due to their job loss or maybe for some other reasons?

Spending may increase due to such uncertain realities which you hve to face during retirement age. Also, you have no other option to compensate such spendings by again joining job.

Hence, never be in a wrong belief that expenses will actually decrease during your retirement age.

#Returns

Yesterday I had a meeting with my fee-only client. He is 21 years old, last month he joined to the job and his CTC is Rs.25 lakh. When I started to discuss about goals and stressed about retirement and asset allocation, his question was that why not go 100% into equity rather than the boring asset allocation as his goal is more than 30+ years away.

My simple answer to this young guy is that he might have seen the fancy returns generated by equity from 2014 to 2018. However, if we neglect the market crashes like the one of 2008, then within a few days, whatever he accumulated may vanish.

You notice that many of these calculators consider the average returns which we have to expect from our investment during the accumulation phase and also distribution phase.

How realistic are these with the actual humpy dumpy market? If you face the crash like 2008 or the stagnant returns of few years from the equity market, then it takes many many years to recover and reach to the level of returns you entered while calculating.

Hence, entering average return expectation is fine but never believe that this will happen with you.

# Taxation

In the Indian perspective, many of our tax rules are dependent on political parties. They float the rules and also change the rules to lure certain section of people.

Equity investment was tax-free up to the last financial year. However, due to changes in the Budget 2018, suddenly there is an LTCG tax on equity investments also.

Same way, in case of EPF also, earlier interest earned from non-contributory EPF was tax-free (if your EPF account is more than 5 years). However, now interest is taxable income from such non-contributory EPF accounts.

Along with such changes, we have to experience the constant changes in Indian tax slabs. If such changes are conducive to our retirement then no issues. However, if they are not, then we have to bear the tax cost.

Remember, the tax may also take away some percentage of your retirement corpus. Hence, keep an eye on such changes.

# Life Expectancy

We assume that we may not live like what our parents. There may be reasons to believe in such things. It may be due to our sedentary lifestyle, eating habits or stress.

However, due to medical advance, we may outlive our expected life expectancy. In such a situation, our retirement corpus may dry up soon. There may be many reasons to outlive our expected life expectancy. Such a situation is horrible than any other points which I explained in the above post.

How to plan for our retirement goal?

Now we understood the limitation of retirement calculators. Then how one should plan for retirement goal? Do we completely neglect these calculators?

My simple suggestions to this are that you noticed we consider many many assumptions when we arrive at our retirement corpus. As I said above, if anyone assumption went wrong, then your retirement life will be a MESS. Hence, assume that such calculators showing you to invest monthly Rs.10,000, then don’t try to restrict your investment only to Rs.10,000. If you can afford more than that, then try to infuse more money towards this goal.

Another way out is to play with such a retirement calculator by REDUCING your working age and returns. Otherwise, INCREASE inflation, life expectancy, expenses or tax liability.

Consider your retirement goal as the FIRST PRIORITY than any other goals of your life.

Hello Sir,

You have well explained the assumptions and details but there is something called balancing retirement portfolio which I feel should be added, as one reach near retirement should consider moving out of equity oriented funds to debt ones irrespective achieved the target goal or not, else wealth accumulated over period of time may be vanished in case of crash like 2008 ?

As you pointed it correctly there are many factors which play out how well planned plan may also not work in ones favour.

Thanks

Raj

Dear Raj,

That portfolio allocation is a different chapter. Here, my intention is to highlight the drawbacks of retirement calculators.

Very good information….got many insights keep educating us this way

Dear Satish,

Pleasure 🙂

Hi Basu,

Your advise for a best retirement plan for a 42 year old working in a private concern

Currently I have an SIP running for 2500*4 in HDFC hybrid equity and HDFC mid cap.

Please advise on this.

Dear Ajith,

Create your own retirement corpus rather than running behind these pension or retirement plans.

Dear Basu,

Could you advise how to create one..

Dear Ajith,

Create by first identifying the time horizon of the goal, do asset allocation between debt and equity and finally start investing based on that.

Interesting article. But I guess it is kinda self understood that these calculators (or any kind of financial planning calculators) will only be indicative. Also even these calculations should be revisited every year and refined in light of new information. Still thanks for sharing your views.

Dear Anand,

Thanks for your views. But here my point is that retirement calculation is based on so many assumptions. Hence, don’t be in wrong belief that everything is fine once you start investing.

Thanks Basu.

I requested you for writing an article on this few months back. I shall go through it in details and fire some questions :).

Regards,

-Santosh

Dear Santosh,

I am waiting to answer your doubts.