LIC is launching a new money back plan LIC Jeevan Shiromani Plan 847 on 19th December 2017. Let us see the features, review, and returns of LIC Jeevan Shiromani Plan 847.

It is a non-linked, with profits, limited premium payment money back plan. LIC is claiming that this plan is designed especially to target the HNIs (High Networth Individuals). This plan also provides you critical illness cover also.

Eligibility of LIC Jeevan Shiromani Plan 847

First, let us see the eligibility condition of LIC Jeevan Shiromani Plan 847.

As LIC is claiming, the minimum sum assured under this plan is Rs.1 Crore. Hence, this is not meant for any ordinary earning individual.

Features of LIC Jeevan Shiromani Plan 847

Along with above-said eligibility conditions, this plan offers the below features.

- Unlike the typical traditional plans of LIC, this plan will be eligible for paid-up immediately after the 1st year completion of policy. For all other policies of LIC, paid up feature will be applicable if you paid the premium for at least 3 years.

- As the policy is eligible for paid up after a year, you are eligible to surrender the policy immediately after the 1st year completion.

- You can avail the loan after a year of the policy.

- Along with inbuilt Critical Illness rider, this plan offers another 3 types of riders and they are Accidental Death and Disability Benefit Rider, Accident benefit rider, New Term Assurance Rider. However, including critical illness rider, you can opt for the maximum of 3 riders ONLY.

- You can pay the premium yearly, half-yearly, quarterly or monthly.

Benefits of LIC Jeevan Shiromani Plan 847

Now let us see the benefits available under LIC Jeevan Shiromani Plan 847.

This plan offers the guaranteed addition. For the first 5 years, the guaranteed addition will be Rs.50 per Rs.1,000 Sum Assured.

From 6th year onward to till POLICY PREMIUM PAYING TERM, this plan offers the guaranteed addition of Rs.55 per Rs.1,000 Sum Assured.

1. Death Benefits of LIC Jeevan Shiromani Plan 847

There are two conditions to pay the death benefits under this plan and they are as below.

a) Death during the first 5 years of policy period

If death occurs during the first 5 years of the policy period, then the benefit is as below.

Sum Assured on death+Guaranteed Addition at Rs.50 per Rs.1,000 Sum Assured.

b) Death from 6th year to policy maturity date

Sum Assured on death+Guaranteed Addition (for first 5 years Guaranteed Addition will be at Rs.50 per Rs.1,000 Sum Assured and from 6th year onward it will be Rs.55 per Rs.1,000 Sum Assured)+Loyalty Addition.

Meaning of “Sum Assured on Death” is defined as HIGHER of the below.

- 10 times of your annual premium (excluding taxes, the extra amount due to underwriter decisions or rider premium)

- 125% of Basic Sum Assured.

- 105% of all the premiums paid as on date of death.

You can also defer the death benefits payable to your nominee in installments rather than a lump sum payment is chosen over the period of 5 yrs, 10 yrs or 15 yrs. This can be exercised by the policyholder during his lifetime only. Based on this, the nominee will receive the death benefits at a deferred period set by the policyholder. Nominee can’t alter this feature. This can be either % of the death benefit or absolute value of money.

The installments will be payable in advance by LIC in the mode the policyholder opted. The interest rate on such payment will be decided by LIC from time to time.

2. Survival benefits of LIC Jeevan Shiromani Plan 847

If policyholder survives to each of the specified duration during the policy term, a fixed % of Basic Sum Assured will be payable. This fixed % is as below.

- For 14 Yrs Policy-30% of Basic Sum Assured on each 10th and 12th policy year.

- For 16 Yrs Policy-35% of Basic Sum Assured on each 12th and 14th policy year.

- For 18 Yrs Policy-40% of Basic Sum Assured on each 14th and 16th policy year.

- For 20 Yrs Policy-45% of Basic Sum Assured on each 16th and 18th policy year.

Like death benefit deferred benefit, this policy offers you to take the survival benefit at the deferred date (postponing the payment receivable). You can receive the survival benefit as per your with along with interest at a later stage of your requirement.

However, you have to defer this survival benefit up to policy maturity only. Before that, you have to receive this benefit along with interest. If you do not take this deferred survival benefit and interest before maturity, death or surrender, then LIC will pay this during maturity, death or surrender time along with interest.

The interest will be yearly compounding but the rate will be fixed by LIC from time to time.

You have to inform this deferred survival benefit receiving option 6 months prior to the actual due date of survival benefit. Otherwise, LIC will pay you the surival benefits as per the due dates.

3. Maturity benefits of LIC Jeevan Shiromani Plan 847

If policyholder survives up to the policy period, then he will receive the below benefits.

- For 14 Yrs Policy-40% of Basic Sum Assured+Guaranteed Addition+Loyalty Addition.

- For 16 Yrs Policy-30% of Basic Sum Assured+Guaranteed Addition+Loyalty Addition.

- For 18 Yrs Policy-20% of Basic Sum Assured+Guaranteed Addition+Loyalty Addition.

- For 20 Yrs Policy-10% of Basic Sum Assured+Guaranteed Addition+Loyalty Addition.

Let me explain the same of both survival benefits and maturity benefits in below sheet for your simple understanding.

Hope the benefits of LIC Jeevan Shiromani Plan 847 may be understood you now easily.

In this plan, you can defer your maturity benefit for future dates in installments. The periods available is for 5 years, 10 years or 15 years. This option can be exercised by policyholder only.

You can choose either % of net maturity amount or absolute value to be payable in installment for the next 5 years, 10 years or 15 years. LIC will pay you in advance of such installments. The installments available are yearly, half-yearly, quarterly or monthly.

The applicable interest on this installment will be declared by LIC from time to time.

The policyholder has to inform LIC 3 months prior to maturity date about this option. During such deferred maturity benefit period, if policyholder wishes to discontinue and interested to commute the remaining installments as a lump sum, then he can opt that.

If the policyholder dies during such deferred maturity benefit period, then the remaining installments will be payable to the nominee. The nominee has no rights to alter this deferred benefit installment option.

4. Inbuilt Critical Illness Benefits of LIC Jeevan Shiromani Plan 847

Along with the above-shared death, survival and maturity benefits, this plan also offers the inbuilt critical illness benefits.

On the first diagnosis of any one of the 15 Critical Illness as specified below, and also if the policy is in force, then the following benefits will be provided.

But before that let us first understand of what are those 15 critical illness which this plan covers. They are as below.

- Cancer of specified severity

- Open chest CABG

- Myocardial infarction

- Kidney failure requiring regular dialysis

- Major organ/bone marrow transplant (as recipient)

- Stroke resulting in permanent symptoms

- Permanent paralysis of limbs

- Multiple sclerosis with persisting symptoms

- Aortic Surgery

- Primary (idiopathic) pulmonary hypertension

- Alzheimer’s disease/dementia

- Blindness

- Third-degree burns

- Open heart replacement or repair of heart valves

- Benign brain tumor

Once you are diagnosed with an above-said illness, then LIC will give you the below benefits.

a) Lump Sum Benefit:–

Inbuilt critical illness benefits equal to 10% of Basic Sum Assured will be payable subject to the following.

- This benefit will be payable after LIC satisfied with the reports with specific deferment period (in respect to specific diseases). The benefit will be payable only once during the policy period.

- A Survival period of 30 days is applicable from the date of diagnosis of critical illness. If death occurs during the 30 days period, then no critical illness benefit will be payable.

- A waiting period of 90 days will apply from the date of commencement of risk or date of revival of risk (whichever is later). However, such waiting period is not applicable for accidental cases.

b) Option to defer the payment of premiums if there is a critical illness claim:-

If LIC accepted the critical illness claim, then you no need to pay the premiums for the next two years. LIC will not charge any interest on such delayed payment. However, if there is a survival benefit dues to be payable to policyholder during this 2 years period, then LIC will pay the survival benefit by DEDUCTING the premiums due.

c) Medical Second Opinion:–

Under this benefit, the policyholder has an option to take the second opinion from the LIC empaneled healthcare providers or through reputed hospitals in India based on the arrangement made by LIC.

Do remember that this facility is available only once during the policy period, for which you no need to pay the cost. The policyholder can take this second opinion immediately after informing LIC about the illness (without bothering about whether his critical illness benefit will be accepted or not).

However, such second opinion not involves any test. If you do the test, then you have to bear the cost of that.

Also, such second opinion is purely based on the facilities and recommendations LIC provide.

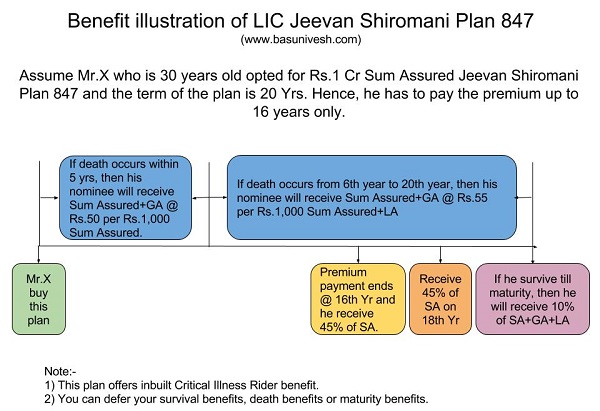

Let me explain the benefit illustration with below image.

What returns we can expect from LIC Jeevan Shiromani Plan 847?

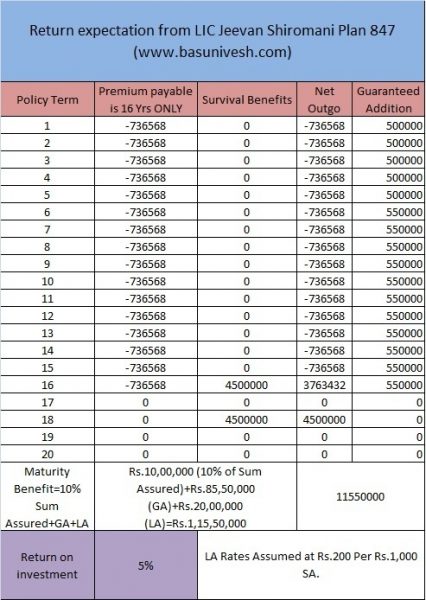

Let us consider that Mr.X whose age is 30 years opted for Rs.1 Cr LIC Jeevan Shiromani Plan 847 and term of the policy is 20 years, then we can expect the returns as below.

You notice that Mr.X will pay the premium up to 16 years only. However, he receives the survival benefit of Rs.45 Lakh on 16th year and 18th year. On maturity, he will receive remaining 10% of Sum Assured+GA+LA.

I considered the LA rate as Rs.200 per Rs.1,000 Sum Assured. Few may argue that this too less by comparing other plans which NOT offers you guaranteed addition. If you check the LA rate of Jeevan Shree (which offers GA like this plan) with the LA rates of other plans, then you notice that LA rate of Jeevan Shree is too less than other plans.

Hence, considering this trend of LIC, I considered the fair value of Rs.200 as LA for calculation. You notice that return on this investment is just around 5%.

Review of LIC Jeevan Shiromani Plan 847

# This plan is not for all. Because the minimum sum assured under this plan is Rs.1 Cr. Hence, if you afford around Rs.5 lakh to Rs.10 Lakh premium then you can opt for this plan.

# The new feature what I saw under this plan is that this plan is eligible for paid up, surrender and loan immediately after one-year completion of the policy period. Usually, LIC plans eligible for paid up and surrender after 3 years. However, LIC reduced this to one year for this plan. In my view, LIC reduced this to one year to make sure that LIQUIDITY must not be an issue.

# This plan offers an inbuilt critical illness cover. However, do remember that getting a claim from critical illness is not so easy and hence you must understand the pros and cons of such critical illness rider benefits. Only 15 illness are covered under this plan. However, if you go for standalone critical illness insurance, then you get around 20 illness are covered (available in the market). Hence, I don’t think this is an additional great benefit. Refer my post on this topic (Best Critical illness policy in India – Comparison Table).

# GUARANTEED Addition is an EYE CATCHING feature of this plan. But the biggest catch this time by LIC is that this GUARANTEED addition is available up to your premium paying term. After that, your invested money will not earn a SINGLE RUPEE. Also, do remember that such yearly accumulated guaranteed addition will not earn a single rupee on it. LIC just keeps this with it and pay you at surrender, death claim or at maturity. Hence, never enter into this plan with the hope that GUARANTEED means the BEST PLAN.

# If death occurs within 5 years of the policy period, then your nominee will receive SA+GA @ Rs.50 per Rs.1,000 SA. However, if death occurs after 5th year to policy period, then your nominee will receive SA+GA @ Rs.55 per Rs.1,000 SA. Hence, the probability of your nominee receive during the first 5 years is less.

# LIC now started to offer to defer the survival benefit, death benefit and maturity benefits to its plans. However, choosing such options blindly without knowing the interest rate offered by LIC is like a BIGEST mistake. Because, if death occurs, then-nominee has no rights to change these options. The nominee has to continue with the option which policyholder selected. Hence, be careful while exercising this option.

# Coming to returns part, you noticed from above illustration that this policy will give you around 5% to 6% returns. Hence, in no way it is even beat the current inflation rate. Hence, it is waste if you invest for such a long period but get a return which around 5% to 6% returns.

Instead, if go for term life insurance and invest the same in PPF (yearly maximum limit is Rs.1.5 lakh) (forget about equity products), then you may earn more than this plan.

Conclusion:-There is nothing new in this plan other than offering to HNIs (setting minimum sum assured as Rs.1 Cr), deferring your survival, death and maturity benefits, inbuilt critical illness rider and eligibility for paid up and surrender within a year.

Rest of all features looks like TYPICAL LIC MONEY BACK PLAN. Nothing new to run behind this product and invest. However, if you feel 5% to 6% returns BEST for you by investing such a long period, then definitely GO AHEAD!! Else simply skip this product. Because in my view, this is meant for agents to garner huge business from a single plan selling.

See everyone thinks before investing his money. I know returns are 5-6%. But they are Pre-tax returns. People investing in this Plan are HNI’s. They are in 30% slab. Post Tax Returns Come around 9% which is fairly good. Always calculate Pre-tax and Post Tax Returns. Moreover come out of negativity with Lic. Jeevan Sheromani is getting good response from market. You can fool a person for a small premium but you surely cannot fool a person in case of Jeevan Sheromani where minimum premium comes around 7 lakhs per annum. Get out of all negativity regarding lic. Market will judge it’s products. Stop spreading negativity all around the world.

Gopal-So as per you 9% pre-tax return is BEST for long-term HNIs (whom you claim NONE can cheat them)?? 🙂

In today’s market Interest Rates are falling.Nothing is Guaranteed in Today’s Market. In such a scenario Lic is talking of Guarantee in Case of Jeevan Sheromani and Jeevan Umang.

The HNI buying this policy will surely need a ppt presentation. He will ask his Doubts. If He finds good in the product He will buy it.

See Lic is not a business of Cheating, It is a business of Relationship Building.

CFP’s only focus on internal rate of return and develop a negative mindset towards Lic.

But I must say you nowadays my CFP’s are Lic DO’s.

There are two ways to create estate,

Save and Create or

Create and Save

insurance is the only way where you create the estate(I.e. Sum Assured) first,and then start saving for it.

Rest let the Market Decide.

Gopal-Whether HNIs need PPT or satisfy, that is left with you (agents force), I can’t enter into that and I am not sure why you are sharing this sales pitch here. Not only CFPs, but all those invest must concentrate on IRR. But sadly agent force not ready to sell INSURANCE but INSURANCE+INVESTMENT. What is guaranteed in this plan? The first 5 years GA right? Later on anything guaranteed? I don’t have a negative mindset about LIC, I still support LICs Term Life Insurance or Jeevan Akshay. But any agent force support these two plans and sell to clients? They NOT, because the lure for commission makes them to stop selling these actual products.

If CFPs joining LIC, then I too have to follow and accept LIC wholeheartedly??

Estate can be created not by SAVE and CREATE but by INVEST and CREATE. When it comes to investment, each of us has rights to know how much we get. The money we earn is not of any politicians or agents. No more emotional drama when it comes to money matters whether it is LIC or any other Government investment product.

Dear Gopal,

I would not want to discuss about the returns and stuff. What I would like you to explain is why LIC is not offering these plans online or even a purchase at LIC office option?

In today’s world everything from vegetables to medicines to consumer goods to to MFs to life, health, auto insurance are offered online.

I am not saying purchase from agents should be done away with, but why not provide additional options like Online to buy these products?

All it takes is to provide all policy information online and a simple application to fill online and submit. These products don’t need any extra effort from a third person at all.

Please explain just this for me and the curious crowd out here.

Lic is offering e-term plan, jeevan Akshay,Pradhan Mantri Vaya Vandana Yojana, and Cancer Care Online.

Why It’s not offering other products online is out of my control.

You may write to lic India regarding this.

In country like India there is much of the population uninsured, we need agents to spread insurance among them.

Moreover ground reality is this uninsured population do not believe in term insurance, they what something back at maturity. Its their mentality.

In case of term insurance you need proof of earning. Do really all the population have proof of earnings? Much of the population is working in unorganized sector and even don’t know the meaning of itr.

So by your term insurance theory we will be unable to provide them insurance (due to lack of income proof).

So are they to be kept uninsured?

insurance is not for only when you die.

How many Indian wives are really financially literate to handle 1 crore amount of term insurance they would get on unfortunate death of their husbands.

Insurance must also be bought for certainties of life like child education, child marriage, and a happy retirement.

Do not put all your eggs in one basket(I.e. Equities)

Have a balanced portfolio with insurance getting its due share.

Gopal-“we need agents to spread insurance among them.”-Are you (or agents) spreading INSURANCE or INSURANCE+INVESTMENT to garner their commission?

Buying PURE Life Insurance does not mean TERM INSURANCE ONLY. If you are so concerned about poor people’s insurance need, then why not you spread PMJJBY, which offers Rs.2 lakh Life Insurance with cheaper rate than LIC’s mortality charge? Do PMJJY requires income proof?

Do not put all your eggs in one basket-Who saying you to PUT? It is your assumption that those who oppose your LIC products are really suggesting to put money in equity 🙂

The problem with agents fraternity is that when someone question returns, they jump to insurance part and when someone stresses about the importance of insurance, then they jump into the social cause as if they are the agents of social welfare and doing the work at free of cost. Investment never be done with BLIND social cause or heartly but must be done with both eyes wide open. Never push such products for the sake of your % of commission.

For your kind information I always make sure that the person I am dealing with is Insured under Pradhan Mantri Suraksha Bima Yojana, Pradhan Mantri Jeevan Jyoti Bima Yojana,and Atal Pension Yojana. I myself took many to Bank to Enroll them under these schemes. Have I got Any commission out of it?

See I am not talking about pushing a product for the sake of commission.

I myself took many people to Bank to open their ppf account too.

I don’t think the person buying Jeevan Sheromani buys it for agents welfare.

Investment must be done with both eyes wide open accepted.

But you can take term insurance and one of the lic plan as a investment in debt category.

In all Lic plans you get return at 6-7%at maturity.

But what if you die in between the policy term? Person paying 500rs a month if dies immediately still gets 2 lakhs in accidental case.

Moreover do you think the nominees of the poor people covered under Pmjjby and Pmsby will get the claim amount hassle free?

It is must to report to concerned bank within 30 days of the accident.

Many nominees of these poor people do not know even how to fill the claim form also.

Lic agents are promoting cancer care product and that’s the need of hour.

See who is saying that lic agents are doing social service at free of cost?

We buy clothes and owner of the shop gets commission(profit) out of it.

So as per Insurance Act agents are entitled to commission for the work they do. They are moreover prohibited from giving any rebate from their commission amounts to the policy holders.

I know some agents do offer rebates to their policy holders(though it’s unlawful).

Lic agents get only 0.1% commission in sale of pradhan Mantri vaya vandana Yojana I.e just 150 rs for 150000 sale.

Still pradhan Mantri vaya vandana Yojana has great collection.

Would it be just still to blame agent fraternity for the lure of commission.

See agents also have homes, family. They are certainly selling the product for the customer benefit.You just want they should do this work without commission. But remember commission voucher is paid to agent by lic not customer moreover they are forbidden to give any rebate.

There are many people in rural areas with no adequate banking facilities. Banks are overburdened with works like crop loan etc and are reluctant to even open their ppf accounts(as you know the reason they get no commission for opening ppf accounts).

I myself saw how reluctant banks are to even Enroll the customer under Pmjjby, Pmsby,and Atal Pension Yojana.

In such a scenario If any agent is pushing a lic product(though according to you for % of commission )I dont find anything wrong in it.

He needs money for his survival. Why do we expect them to do this work without commission. He comes to collect the renewal premium at home though the premium amount may be as low as 3000 per year I.e. He gets only 150rs out of it. In that too he gives the customer free lic dairy which costs him 50rs every year.

Its not correct to blame the entire agent fraternity for the wrongs committed by few.

Gopal-Thanks for your lengthy answer 🙂

“Moreover do you think the nominees of the poor people covered under Pmjjby and Pmsby will get the claim amount hassle free?”-Why not you help in this regard also if you are concerned so much about poor?

“See agents also have homes, family. They are certainly selling the product for the customer benefit.You just want they should do this work without commission. But remember commission voucher is paid to agent by lic not customer moreover they are forbidden to give any rebate.”-Who are against their income? I am against their strategy where they HIDE or use social cause to sell product by throwing in air the concept of Insurance.

So banks are reluctant to push PMJJBY, then we can insure them with wrong products?

May I know the LIC agents average survival period in the industry? How many agents actually work as full-time agents to serve their clients?

Wow, I just asked one question and that with acceptance that agents are okay but why not online or even selling policies at LIC offices.

You have given me answers like people from unorganised sectors need insurance, they dont have income proofs, etc, etc.

Do you know whats the policy premium for an endowment plan? I know for afact that for a 30 year old a 5 lac cover will need him to pay 40,000 per annum.

Do you think a low wage earner with 10-15,000 can afford to pay 3,000 premium every month and for what? 4-5% return? I don’t even want to debate with people who don’t have common sense.

And who are you to decide that housewives don’t deserve to get a 1 crore insurance money if their husband expires just because she is financially illiterate?

All you agent fraternities sell these products only because they are financially illiterate. And you people sell these to even house wives and children.

First ask LIC to sell insurance to only earners in a family. Only they need insurance and not a 5 year old kid or a 70 year old senior citizen.

The biggest joke you said is, insurance must be bought for certainties like marriage, education, etc. Let me tell you, marriage and education can be achieved only if you are alive and by savings and investments or even a loan but no one gives a loan to your family if you die which is why you buy insurance.

Insurance is for uncertainties. If someone says there will not be a single motor accident in the world would we ever buy an insurance for our vehicles?

I read all the comments in discussion, it seems basu is very much impressed by equity market.

Basu, as coin has two sides equity also has same.

Please educate investors with both worst case returns and best case returns and let them decide if they are ready to risk.

If you speak about insurance educate clients by claim settlement ratio.

If you speak about debt fund educate clients about debt returns vs risks and how it is different compared to ppf, nsc without taking risks

You felt pity on knowledge of so many people, there is an example where a 34 year old person asks for investment advice and you suggest debt and equity without doing need/risk appetite/comittment analysis.

Don’t feel pity basu share the truth and unbiased reviews.

Have a look at real estate too, argument is not a solution but war of egos

Amol-If you read my Old Articles, then you will find the information about claim settlement ratio, debt funds and their risks, best and worst cases of equity. 34 Years person asked me about investment means I might have suggested him debt and equity with proper asset allocation. If you read my posts about equity funds, then you will come to know what I wrote.

I feel pity to those who feel EQUITY IS BEST or DEBT ONLY BEST on this earth. I am unbiased as I don’t have commission income from both 🙂

Dear all, please suggest me the best investment options… I am 34 years old and have one child 8 months old and planning to settle abroad but I feel I should invest in india so that regularly if I invest which would help my kids in their future studies, marriage and settlement.

Prabh-Use Equity and Debt in ratio of 70:30.

Mutual funds which give negative returns in 10 years

1. ICICI PRUDENTIAL CORPORATE BOND FUND GROWTH gave annualised return (-)14.17% in 10 years . means if u invest 1 Lakh in 2007 then its value in 2017 will be 21697 with a loss of 78303.

2. ICICI PRUDENTIAL CORPORATE BOND FUND B GROWTH (OC) gave annualised return (-)14.02% in 10 years . means if u invest 1 Lakh in 2007 then its value in 2017 will be 22079 with a loss of 77921.

3. DSP BLACKROCK WORLD GOLD FUND GROWTH gave annualised return (-)1.33% in 10 years . means if u invest 1 Lakh in 2007 then its value in 2017 will be 87468 with a loss of 12532.

4. JM BASIC FUND GROWTH gave annualised return 0.03% in 10 years . means if u invest 1 Lakh in 2007 then its value in 2017 will be 100300 with a Profit of only Rs. 300 in 10 years

5 UTI TOP 100 FUND GROWTH gave annualised return 1% in 10 years . means if u invest 1 Lakh in 2007 then its value in 2017 will be 110462 with a profit of only 10462 in 10 years

Lalit-First update your knowledge of HOW MANY TYPES OF MUTUAL FUNDS are there. Second thing, you don’t knwo the difference between ANNUALIZED RETURN TO CAGR. Third thing, you are comparing your PRODUCTS (which are mainly debt) with GOLD and EQUITY. I simply thought to laugh about your knowledge and feel pity on those who invest based on your suggestions. Now regarding your fund returns, I am not sure from where you are picking the data and spreading it. The right returns are as of below as on 1st Feb 2018 (ValueResearchonline). You really need a basic understanding of how interest return calculated and what are MUTUAL FUNDS 🙂

1) ICICI PRUDENTIAL CORPORATE BOND FUND GROWTH-10 years returns 8.02%

2) JM BASIC FUND GROWTH 10 years returns 0.57%.

3) UTI TOP 100 FUND GROWTH- 10 years return 8.64%.

https://www.fundsupermart.co.in/main/fundinfo/worst_Funds.svdo

sorry to say basu sir

but my data is correct and u can check from above site

This data is updated till 1st Feb 2018

Next time i send data of top 10 negative return generater mutuaf fund in the period of 5 years. I am a government officer and not an agent . I know the value of money and how much hard work we have to do to earn it.

U can cross check the figures of return calculated from Financial Calculater app. Annualised return percentage is given there. Why should we need to know how many types of MF there? Are we giving exam for MF? Our target is to earn money , save for future and if possible mutiply it. But never loss it by playing gamble like mutual fund.

Lalit-I feel pity about your knowledge. First check which is the BEST way to calculate the return (Annualized or CAGR).

“Why should we need to know how many types of MF there? Are we giving exam for MF? Our target is to earn money , save for future and if possible mutiply it. But never loss it by playing gamble like mutual fund.”-GREAT GYAAN. NOW I REST MY CASE 🙂 WHY SHOULD I KNOW ABOUT THE TYPES OF MF!! BECAUSE IT IS YOUR MONEY INVOLVED. IF YOU DON’T WANT TO KNOW, THEN THE RISK TO YOUR MONEY OR INVESTMENT GOES HIGHER AND HIGHER. BLIND INVESTMENT IS DANGEROUS AND FEELING YOU AS PROFESSIONAL AND THE MENTALITY OF WHY SHOULD I LEARN FEELS ME SORRY!!

Now u r coming on the correct track. As u said its ur money and it my be in danger if u invest in MF. Also chances are there to get negative return from above date . Also MF house with leading brands may also give negative returns . So moral of the story its a gamble and please accept it.

LALIT-NOW YOU ARE ON RIGHT TRACK 🙂 I have not said IT IS DANGER IF YOU INVEST IN MF but I said if you don’t know anything then first learn and then invest. If you are not ready to learn then it is your problem but not mine problem. Because money involved is YOUR’s but not MINE. Investment is nothing but managing risk rather than what you are thinking!!

If you are not ready to learn the basics of investments, then even investing in Bank FDs may be dangerous to you. If you not understood this also, then it is completely YOUR PROBLEM or your behavior problem but not mine 🙂

Yes you are right basu sir

Investment in MF is management risk. And means we can lose mpney by taking risk or we can gain also. So isnt it a gamble. There government created scheme for safeguard of people of India. So its better to onvest in government scheme instead of gambling on MF Bazar

Lalit-As per you, which is safe even the money you are keeping in your SAVINGS ACCOUNT?? If you feel Bank FDs or even for the sake of savings accounts are safe, then why people cribbing about the PAY-IN option of latest Govt Bill? Just read and let me know your views 🙂

Lots of people are approaching me for investment. Lots of people have invrsted in my office and amount is above 25 lakh each. They dont wish to continue with MF and bank . They are now investing in PPF , NSC ,5 TD .

according to these people , mutual fund is the wosrst from the past experience of 25 years . They prefer

1. PLI if they are eligible like Doctor Lawyer C A and NSE BSE listed company employess and govt semi govt employees.

2 . 5 TD

3. NSC

4. KVP

Lalit-LONG LIVE YOU AND YOUR INVESTORS!! 🙂

Lalit-Sure sure 🙂 You can send a monthly report. We discuss on that!!

THIS IS THE SITUATION IN ALL OVER INDIA. AFTER THE ARRIVAL OF MODI GOVERNMENT , THE INVESTMENT IN POSTAL LIFE INSURANCE AND 5TD HAS INCREAD. PEOPLE DIVERTED FROM BANK AND MF TO POSTAL LIFE INSURANCE ,5TD ,KVP,NTHIS IS THE SITUATION IN ALL OVER INDIA. AFTER THE ARRIVAL OF MODI GOVERNMENT , THE INVESTMENT IN POSTAL LIFE INSURANCE AND 5TD HAS INCREAD. PEOPLE DIVERTED FROM BANK AND MF TO POSTAL LIFE INSURANCE ,5TD ,KVP,NSC

Sad to know so many people you know diverted their money from MFs to PLI after Modi came to power. Because after Modi took over, stock markets have rallied 50-60% which has reflected in the MF that has given me 25% annualized returns.

I truly feel sorry for you and your fellow investors who have missed the bus.

Good luck with that 7 or 8% returns in PLI.

Meanwhile Basu only says if anyone is happy with 7% returns over 20 year period they can continue what they are doing. His lessons are for people like me who want to earn 12-15% returns over a long period that can beat inflation and create wealth. Whats good for you is not necessarily good for many others.

And I read India’s roads are killing machines, so don’t step out to risk your life. Stay home and stay safe.

Pradeep-I can only say one sentence about Mr.Lalit “I feel pity about his knowledge”.

Lalit-Long live your Post Office, YOUR DATA (which is completely wrong in all sense from your understanding your annualized to CAGR, types of MF and your claim of an increase in investment in post office schemes post Modi era) and YOUR AGENCY!!

Lalit-Can you explain to me which is the best way to calculate returns? Annualized or CAGR? What is the difference between two? Which standard your regulator (hoping you are representing some insurance company) or other regulators in India follow?

If you don’t know, then update your knowledge and then come up for discussion. We definitely discuss. WHY SHOULD I LEARN attitude may be LOSS to you than ME!!

Incorrect data.

I am going to write to ICICI Pru AMC telling their their fund data has been wrongly put up by the above website.

Let us compare using Financial Calculator

If u invest 5350 monthly for 15 years in RD with current rate of interest 6.9% then you may get 1684980 and no tax rebate and no insurance.

If u invest 5350 monthly for 15 years in PPF with current rate of interest 7.6% then you may get 1759405 with tax rebate under 80C and no insurance.

Now if u invest 5350 monthly for 15 years in Postal Life Insurance (PLI) of government of India run by post office then you get 1870000 with appx interest rate 8.3% and additional benefit of tax rebate under 80C and Life insurance.

Top mutual fund gave us 13% return in 10 years. If we deduct taxes and other charges then this return was about 10% but with simple rate .

suppose we invested 100000 in so called top mutual fund(if we dreamt and win a jackpot) then we get net amount 200000 after 10 years after deducting all taxes and charges. So they say u get 13% but actually its simple 10% and in compound interest language its just 7.3%.

Kindly correct me.

Half cooked illogical calculation for Mutual Fund does not reflect the true returns.

What taxes and charges are you talking about that reduces 13% returns to 10%for MFs?

Even if the returns is only 10% it is not simple interest, it is the CAGR (Compounded Annual Growth Rate) after expenses are accounted for. MF returns are always shown in CAGR.

So taking away all the faulty calculation, MF actually returns 13% CAGR (as per your return assumption) and potentially more.

Now compare this with others.

Pradeep-Sadly he don’t know what is Compounding, IRR and XIRR and how MF returns actually has to be shown as per guidelines. So let us wait for his knowledge updates for further discussion 🙂

Explained! Why we lose money in Mutual Fund

— By Kaushlendra Singh Sengar |Aug 27, 2017 04:01 am

We have always considered mutual funds to be the safest bet in investment gamble, but Kaushlendra Singh Sengar says every venture has its own shortcomings, and we need to know them

“I wish to invest in mutual fund, as my first investment,” my friend told me. My immediate question to him was, why? And he replied, “It’s secure and safe and my money will be managed by professionals, and I don’t have to worry much.”

Was he really right? Do we never lose money in mutual funds? Is it 100% fool proof investment available in the critical financial world? If it was really that great as an investment vehicle, wouldn’t everyone put their hard-earned cash in mutual funds rather than putting it in saving account or fixed deposit?

But looking at the benefits of mutual funds – it being professionally managed, benefits of diversification which ultimately minimizes risk coupled with requirement of low amount to invest along with tax advantage – it looks like a favourable investment option for every class of investors.

Despite such fascinating edges which mutual fund has over other investments, investors may tend to lose money even in them. But the question arises why? How? When a fund is being managed by the best financial minds of the markets, who keep a track of every nitty grittiest of the stock, coupled with functional advantages of the fund, then how do we lose our money?

Thorns of money tree

If we come across any individual who has lost money in mutual fund, he seldom looks back at the reason; rather he will close that door of investment opportunity for him. So, we are still at very nascent phase of investment industry. If we lose, we don’t look back and question why, we rather shy away our eyes from that option and forget about it. This is why we make mistakes. So, before investing into anything, we must know all the pros and cons of the investment options. We all are generally aware of the fruits of the investment tree but not the thorns. Let’s know the thorns of mutual fund, which makes us, lose our hard-earned moolah.

Return expectation, time horizon, individual goal are the first steps before you put your money into anything. Here lies the trap; we don’t know our purpose and duration of investment, which makes the basis of our investment. Investment goal needs to be sorted at first instance. So, when we don’t know what we need, we end up choosing the wrong product, thus ending up in wrong box. If one doesn’t have any minimum time frame, and just wish to save, the duration should be in line with the product. Basic rule which need to be followed is five years and three years for equity and income fund, respectively.

Home done well

One of the biggest challenges is to pick out of numerous numbers of mutual funds in the market. There are around 40-45 major mutual funds operating in the market with total schemes of 10,689, with total asset under management as on June 2017, at almost Rs 19,51,492.21 crore. This makes further choosing the right mutual fund a difficult task for retail investors.

Many investors put their money in mutual fund because despite being unaware of how the stock market operates, they may wish to encash on the opportunity. They think mutual fund is a lesser risky option. But we must understand where is ultimately a mutual fund manager is investing? He doesn’t put the investor’s money in fixed deposit or recurring or may be a saving account which gives us a guaranteed return. A mutual fund manager ultimately puts his money into the stock market. Every individual knows that stock market is prone to all kind of risks – be it economical, political or global. In recent months, return on mutual funds like Reliance midcap and small cap fund (G), L&T emerging business fund and many others has given negative return. Mutual fund is also prone to various risks which the stocks are prone to, in which the fund managers have vested their funds.

We invest after looking at the past performance, but past performance doesn’t guarantee any future income. A mutual fund manager is driving a car without a reverse gear, that is, he can only buy shares and not short sell, and neither can he exit the market. This is one major flaw, even at the weakling, manager has to buy. And only an investor can ask him to exit from a particular share, this is where investor fails to make proper exit from the market and that pull his investments down.

Fund managers have inflow of fund; they can’t keep the money within the house. So even if the markets conditions are unfavourable, a manager has to put in money in some or other stock, thus making a bad investment decision.

Though mutual fund is lucrative, it has its own flaws which tend to pull down the returns. So, an investor must read the document carefully before investing.

(Kaushlendra Singh Sengar is the Founder & CEO of Advisorymandi.com)

http://www.freepressjournal.in/finance/explained-why-we-lose-money-in-mutual-fund/1127520

Lalit-Great sharing 🙂 “A mutual fund manager ultimately puts his money into the stock market.”-But sadly author has hindsight that Mutual Funds=Stock Market Investment. He does not know how to manage the risk by investing properly with proper asset allocation. Mutual Funds does not mean STOCK MARKET. There is other types of assets which also comes under mutual funds like debt funds. If you don’t know how to manage the risk, then even the money you keep in your savings account is also RISKY.

Truth about LIC. Fantastic article.

https://www.equitymaster.com/diary/detail.asp?date=04/21/2016&story=2&title=Why-Its-Best-to-Stay-Away-from-Buying-LIC-Policies

Pradeep-Now they keep silent 🙂

Return on safe investment is as below

LIC 5% – 6%

RD 6.9%

PPF 7.6%

PLI 8.3%

Let us compare using Financial Calculator

If u invest 5350 monthly for 15 years in RD with current rate of interest 6.9% then you may get 1684980 and no tax rebate and no insurance.

If u invest 5350 monthly for 15 years in PPF with current rate of interest 7.6% then you may get 1759405 with tax rebate under 80C and no insurance.

Now if u invest 5350 monthly for 15 years in Postal Life Insurance (PLI) of government of India run by post office then you get 1870000 with appx interest rate 8.3% and additional benefit of tax rebate under 80C and Life insurance. Means if u are in 30% bracket then u can save total tax in 15 years upto 288900 which total return may go upto 1900000 with insurance of 10 lakh.

Atrocious calculations. Any plan that has a life insurance component in it will be dependent on the age of the holder. They calculate your premium based on your age for a given sum assured. Returns will then vary accordingly. Bonus to be paid out is not written in any document to be shown assured.

FD and RD will pay the same interest for people of all ages.

Also these interest rates will vary every 3 months for next 15 years. Why would someone lock 6.9% for next 15 years?

Its funny to write return % and then do calculations for these. People would be mentally retarded to take you post seriously.

Lalit-I think you are unable to understand the concept of long term investment, real return, inflation and the damn cheap rates of Life Insurance (Term Life Insurance). It is not your fault but the fault of your profession, which forcing you to defend your product as BEST on this earth 🙂

Premium rate is same for any age group. and it is same since 1884 in Postal Life Insurance. Oldest plan of India by government for the security of people of India. So according to my opinion one should must invest for safe and higher return without any risk. Because mutual fund agent will never comment on worst mutual funds who gave negative return over a long period of 10 years . They only admire the top MF and attract the customer. So be safe and avoid any misguid by MF agents or LIC agents. Just invest ur hard earned money in best schemes like PPF and PLI . 80% MF house performed below averagr over the last 10 years . only 5% crossed over 10% return in a period of 10 years. So its like betting ur money. If u r lucky then its jackpot. Otherwise ALLAH MALIKPremium rate is same for any age group. and it is same since 1884 in Postal Life Insurance. Oldest plan of India by government for the security of people of India. So according to my opinion one should must invest for safe and higher return without any risk. Because mutual fund agent will never comment on worst mutual funds who gave negative return over a long period of 10 years . They only admire the top MF and attract the customer. So be safe and avoid any misguid by MF agents or LIC agents. Just invest ur hard earned money in best schemes like PPF and PLI . 80% MF house performed below averagr over the last 10 years . only 5% crossed over 10% return in a period of 10 years. So its like betting ur money. If u r lucky then its jackpot. Otherwise ALLAH MALIK.

Lalit-Can a common man buy such product? Mutual Funds (again you are thinking of ONLY EQUITY) is a not a product like invest today and forget for rest of the life. You must review it once in a year. If you are not capable of doing so, then it is your fault but not the MF product fault 🙂

“80% MF house performed below averagr over the last 10 years . only 5% crossed over 10% return in a period of 10 years”-Can YOU PROVE FROM YOUR DATA?? I am eager to learn your claims now!!

So as per you ONLY PLI AGENTS ARE GOD WHO ALWAYS SAY TRUTH!! Funny but unable to digest your level of knowledge. Anyhow, leave it. First share your claim of 80% MF performed below average CLAIM, then we discuss further.

Lalit-So as per you 13% returns of MF is not compounded or IRR return but a simple return. Please update your knowledge about SEBI and AMFI guidelines about the procedure to show returns in MF industry. Also, as per you all MF are taxable and hence it reduces return part. Please update your knowledge about 13% return of what you are quoting for XYZ fund is simple or Compound. Also, let me know the 13% fund, which you quoted is equity fund or debt fund. Also, update yourself what are the taxation rules of equity and debt funds.

Come up with your answers. Then we discuss further 🙂

Now LIC agents need to scout for only 5 to 6 “HNI Bakras” during the year to achieve MDRT !!!

Ritesh-Exactly 🙂

Hey, Very useful article!

Thanks for sharing!

Marketinsider-Pleasure 🙂

Sir,

How good is LIC jeevan kabhi plan for a 23 year old fresh graduate engineer…?

Vijay-I never heard such plan. Check LIC portal, there also you not find such plan. Beware of such agent’s created plans.

No plan is there named as jeevan kabhi

In this early age buy one term plan ,and invest money in midcap based funds as in early age u can take a bit of risk

This plan is Very good for you

Anil-May I know HOW?

One point to note is that not only LIC but all insurance companies misguide people with endowment/moneyback/pension plans. Agents will quote any nonsense to get commission – do your own homework.

In fact, people have to open their eyes while investing in any asset – be it stock,MF,real estate,gold or insurance – do not go by what is marketed to you verbally by any stakeholder – read the fine print before any investment.

Shrikant-It is rampant in insurance industry.

How MF distributors earn their commission

Distributors continue to be paid upfront fees and trail fees

Mint

Kayezad E. Adajania

After the capital markets regulator, Securities and Exchange Board of India (Sebi), abolished entry loads with effect from August 2009, it made it mandatory for mutual fund (MF) distributors to disclose the fee that they earn from MFs. Also, as a result, distributors were also asked to charge their customers directly.

In the meanwhile, distributors still continue to be paid upfront fees and trail fees, which now forms one part of distributor’s earnings. The other part, of course, is the fee they charge you—the investor.

But about the fees that your agent earns from MFs, wouldn’t you like to know how they earn commissions? This is not about how much they get paid individually, but it helps to understand how MFs deal with their distributors.

Upfront and trail

Let’s get the basics out of the way first. Equity schemes charge as much as 2.75% (limits were enhanced in 2012, up from the earlier 2.50%) every year to its unitholders; debt funds charge up to about 2.50%. As the scheme’s size goes up, the expense ratio comes down. Let’s say your equity fund’s expense ratio is 2%. Of this, say, the fund puts aside 25 basis points (bps) for custody charges, registrar and transfer charges and audit fees. A basis point is one-hundredth of a percentage point.

This leaves 1.75%, of which, say, your fund gives some portion to agents as commission and keeps the rest as its own income, also known as asset management company (AMC) fees. Assume your fund decides to give about 0.75% as upfront fees and 0.50% as trail fees. While your MF pays upfront fees to distributors at the time that he gets fresh investments, it pays trail fees to distributors for as long as you stay invested. What remains (50 bps) is your AMC’s own income.

In reality, your fund house pays different commission to different distributors. Pricing also varies from product to product. Dhruv Mehta, chairman, Foundation of Independent Financial Advisors (FIFA), one of India’s largest distributor associations, says: “Products that have the potential to generate higher returns also pay higher commissions. Also, higher the volatility, higher will be the commissions because such products are also difficult to explain to the investor; more effort goes by the distributor to explain its nuances.”

As a ballpark, fund industry officials say that equity funds pay 75-100 bps as upfront commission and another about 0.50% as trail fees. Debt funds pay 50-75 bps as upfront charges and about 40-50 bps as trail fees.

“Fees paid to distributors from the ‘beyond top 15 cities’ are higher than what distributors get in the top 15 cities”, says Kalpen Parekh, chief executive officer, IDFC Asset Management Co Ltd.

title=

Get paid as per category

Higher the business a distributor gets, higher are his or her rewards. Typically, banks and national distributors get paid the most because of the sheer volume of investments that they get, but many independent financial advisers (IFAs) who have grown their businesses in recent years have also seen a rise in their fees and commissions.

Fund houses, then, classify these distributors in categories. For instance, Reliance Capital Asset Management Co. (AMC) Ltd classifies its distributors as silver, gold and platinum with silver being the lowest category and platinum being the highest. “We look at their existing assets under management with our fund house. But that’s just one aspect. We also look at their potential, among a few other things,” says Sundeep Sikka, chief executive officer, Reliance Capital AMC. DSP BlackRock Investment Managers Ltd classifies its distributors as “retail” (at the base level) and then going up to “preferred”, “premium” and finally “key relationships” that typically have the largest national distributors and bank distributors.

Your fund house then prepares various commission structures for each of these categories; higher a distributor’s category, more the commission he stands to gain.

Focus and other schemes

Sometimes, fund houses focus on garnering inflows in few and select existing schemes. Such schemes could be small-sized and the fund house may want to grow them in size. The fund house then makes such schemes as its focus schemes. “Here, the fund, typically, pays something extra, say, 25 bps extra upfront, in addition to the usual upfront fees it pays,” says Hanoz P. Patel, founder and director, Power Pusher Financial Services, one of Mumbai’s largest distributors of financial products.

For instance, a brokerage chart that we looked at for the April to June 2013 quarter prepared for a bunch of distributors of Reliance Capital AMC shows that the fund house has earmarked three of its schemes—Reliance Top 200 Fund, Reliance Regular Savings Fund–Balanced and Reliance Savings Fund–Debt—as its focused schemes. At the moment, these schemes pay an upfront commission of 1.75% to this bunch of distributors, no trail fees in the first year and 85 bps per annum trail fees from second year onwards. The rest of its schemes pay 85 bps as upfront fees and then 50 bps per annum from the first year onwards as trail fees.

Focused schemes need not necessarily be those whose corpuses fund houses want to increase. They could also be well performing schemes within a fund house. For instance, Birla Sun Life AMC classifies its large and well performing equity schemes as “designated equity schemes A” and the rest of them as “designated equity schemes B”.

SIP commissions

One way of paying distributor commissions on systematic investment plans (SIPs) is the same as fund houses pay for lump sum investments. Pay the distributor upfront charges every month, as and when the inflows come followed by the trail fees at the end of every year.

But commissions in SIPs get tweaked slightly. “It takes more effort on the distributor’s part to convince investors to invest in an SIP. Also, the investment amounts are typically small, in the range of Rs.1,500 to Rs.3,000. So by just paying a brokerage to him, it might not help him make his ends meet,” says Ajit Menon, head (sales) and co-head (marketing), DSP BlackRock Investment Managers Ltd.

So in addition to the usual upfront charges, some funds houses pay a flat charge per application. Fund officials say that typically some fund houses pay Rs.50 per application if it is a one-year SIP, Rs.100 for a three-year SIP, Rs.150 for a five-year SIP and Rs.200 for a 10-year SIP. These are merely approximate amounts; your fund house may or may not pay such flat charges.

There’s a third mode of payment and that works like this: in addition to the upfront and trail fees, some fund houses pay an additional bonus incentive to distributors. For instance, if 1% is the upfront fee, the MF may choose to pay an additional incentive of 25 bps on all monthly incentives. But there is a small difference. Unlike the usual upfront commission that gets paid after every instalment comes in, MFs bunch up all the months’ special incentives and pay the distributors upfront when the SIP gets registered.

Here’s an example: assume you enrol for a three-year SIP and commit to invest Rs.2,000 every month. Assume your fund pays the distributor an upfront commission of 1% every month (after the instalment comes in on a month-on-month basis) and another 0.25% special upfront commission. This means, that your agent will earn a total of Rs.720 (Rs.2,000 x Rs.20/month x 36 months) as upfront commission and Rs.180 as a special commission throughout the SIP tenor. This Rs.180 gets paid upfront to the distributor when the SIP starts. If the investor leaves prematurely, the advance special commission is recovered back from the distributor

Special situation

Usually, equity funds fetch more commissions to distributors than debt funds but sometimes it could be the other way around. For instance, so far in 2013, fund houses have been busy selling their debt funds to capitalize on the falling interest rates.

Between April and June 2013, for instance, L&T AMC is paying a higher upfront fee (1.50%) to select distributors for selling L&T Triple Ace Bond as against 50 bps upfront fee that it is paying to the same set of distributors for selling any of its diversified equity schemes. Several such examples can be found in the market, where commissions paid to debt funds is as much or even higher than what equity funds fetch. “Falling interest rates are good news for debt funds and fund houses want to showcase their income funds to be able to attract inflows. Same is the case with government securities funds. They get aggressive in selling them and hence a higher commission,” says Shashank Joshi, a Mumbai-based distributor.

The recent high commissions paid on Rajiv Gandhi Equity Savings schemes is another example because it was a new product and fund houses wanted to popularize it.

Full trail model

Some fund houses such as Franklin Templeton Investments Ltd and Canara Robeco AMC have started to offer the option to its distributors to opt for a full-trail model. This means only trail fees and not upfront fees at all. “These are smart distributors and financial planners who know that their customers will stay invested. These distributors aren’t interested in churning their investors’ money. So they prefer to wait out longer and keep earning trail fees,” says Amit Trivedi, CEO, Karmayog Knowledge Academy, a Mumbai-based MF training institute.

Since the distributor doesn’t earn upfront fees, the trail fees are generally higher, for as long as the investor stays invested. Trivedi says that distributors who are new in their businesses and who possibly struggle with their cash flows prefer to get upfront commission and a little bit of trail. But established distributors and financial planners who are interested in “building their business” opt for a trail model.

Trail fees, fund officials claim, are also charged by those who largely charge a fee from their investors. With entry loads abolished, fund industry officials and distributors say a trail model benefits all—fund houses, distributors and investors. While investors are nudged to stay invested for a longer tenor, distributors’ earnings go up in the long run and fund houses get sticky money.

Rajan-I am promoting HERE DIRECT MUTUAL FUNDS, then what is the necessary to share this GYAN HERE? 🙂

I love the fact that you have shared an article that discusses statistics about whats paid to distributors, etc by MFs.

This article is possible only because Fund Houses are transparent with their expenses and the SEBI is doing a fine job regulating them.

And you know what? I don’t care about distributors, I invest in Direct plans in MF.

Now I want you to show such an article about LIC policies. I want to know what is the exact commission for each policy, whats the mortality charge every year, what other charges are being taken by LIC, how much of my money is actually invested who is the investment manager and most importantly where is it invested and finally what are the returns does it yields.

LIC is the biggest fraudulent organisation in India. I can prove it right here. I have asked a simple question to many agents here and got no answer. Lets see if you can answer me on the below question.

LIC promised 40% more bonus this year due to high profits. But if you compare last year’s bonuses with this year there is no change at all.

You can read the news below.

http://www.livemint.com/Money/H1lQrcBZVXFDYdm473hLNI/LIC-to-pay-40-more-dividend-bonus-in-201617.html

The most Trustworthy org as per you is the biggest cheater and fraud going around. Challenge you to try proving me wrong.

Pradeep-Don’t worry, he will now raise the different issue to divert it (by copy-pasting).

Great Article Basavaraj! You have hit the nail!

Few years ago an agent tried to sell me the traditional endowment plan. I asked for the returns. He could not respond to all my queries and asked me to become an agent. I accepted the idea thinking that the first year commission of 20-30% and then 5% Y-o-Y for next 15-20 years would be a good Total return for my own policy.

However after getting deep into the plans and understanding its returns I found that NONE of the traditional endowment plans (Insurance plus Investment) in India suffice the need of a person who seeks financial independence for his/her loved one plus returns on investment.

The very first purpose of any GOOD insurance plan MUST be to ENSURE that if the “Earning Member (Yes policy must be on the name of Earning member only. I have seen agents asking to take life insurance for non-earning spouses as well)” of the family is no more, his/her dependents can live a smooth financial life after him/her.

For all LIC FANS and its promoters let us discuss about this particular policy only in little more details.

A person who is buying this policy for S.A of Rs 1 Crore and paying annual premium of Approx Rs. 7.36 Lakh must be earning at least 15 Lakh (Assuming after all household expenses, child education, travel expenses, person uses entire saving to pay the policy premium).

So if a person who spends Rs. 7.5 Lakh annually for his/her lifestyle, the Risk cover of Rs 1 Crore would never be sufficient for his family.

Rather person can buy a Term Insurance of Rs 3 Crores with few Critical Illness riders by paying an annual premium of not more than Rs. 25,000 per annum (30 Years Healthy Person).

With this Term insurance, person has secured his life (Financially ?) by paying an annual premium of Rs. 25K and getting a much higher Life Cover.

Now the remaining amount 7,36,000 – 25,000 = 7,11,000 can be invested in any good secured plans, which will give at least 8% tax free returns, for next 20 years (By paying only 16 Installments initially for 16 years and then keeping the maturity amount for another 4 years at same interest rate to complete 20 years).

This investment @8 would grow to Rs 3.16 Crore plus ( Yes Three Crores) in 20 years which is far greater than the Total Returns of Rs 2.25 Crore ( Considering all money back in 16th and 18th year and its interest earned for next 4 and 2 years respectively). And as I said earlier you get huge amount of Life Cover i.e. 3 Crore compared to just 1 Crore given by this policy.

So the people who are shouting here that, Pure Term Insurance plans don’t give anything on Maturity, must look into the numbers above.

Write back here, in case you need more detailed explanation for above calculations.

Arun-Well articulated and thanks for sharing your views. The sad part is that those who are LIFE INSURANCE agents not accepting that PURE TERM LIFE INSURANCE is a MUST. But as per them a product which combines LIFE INSURANCE+INVESTMENT is the ONLY LIFE INSURANCE PRODUCT, which can secure one’s life but not term life insurance. Hence, one must not buy term life insurance!!

There are two reasons.

1. Many who becomes agents by passing an simple exam sometimes themselves does not know what is “Term Insurance” and what are its benefits. As it is never taught to them by their supervisors.

2. Even if someone knows he/she will not tell this to their clients, comparing the earning potential in terms of commission with the traditional policy (25% for first year i.e. 1.84 Lakh in first year and 36800/- every year for next 15 years) which is much larger then the commission earned with the “Term Insurance” Policy ( mere Rs. 1250/- only ) or no commission as these policies are available online easily.

Arun-Completely agree.

Hi Basu Sir,

Happy to see a lot of people are aware of facts nowadays and LIC agents in the forum are disappeared.

Happy also to see that a healthy discussion is going on.

All are expressing nice reviews. Full credit to your blog. It has made them understand the importance of term life insurance and also investments.

regards

RAJESH PAI

Rajesh-Yes, this time really a healthy discussion even from one or two agents. I always welcome such healthy discussion. Above, that as you said, people are slowly understanding the products in a better way and staying away from such products.

perhaps discussion will never stop , we still don’t understand behaviour of clients under different circumstances … even if client accepts Term Plan be it from any Company ….after some period many are not interested to continue with Term plan …financial decision mostly are emotional rather practical … I am also an agent … tried every client to understand importance of Term plan … in the end they prefer to buy other plans and that is also from another agent,Here I loose much needed business.

Financial Planners do calculate very smartly but fail to understand behavioural science, which now is accepted even by world

Let every person decide on his own behaviour and knowlege.

Both are right

Sunil-Now let us discuss on behavioral finance. If you are handled with the task of selling a product and if you are selling the RIGHT plan to client based on his or her need, and if you still fail to sell, then it is not client’s problem but something in YOU. If Term Plans are so untouchable by public, then why there is so much rush towards quoting competitive price by insurance companies? Why LIC was forced to launch online term plan to compete?

Now, regarding your view that majority of them will discontinue, do you have data from LIC or from other insurance companies to validate your point?

It is your task as an agent to change the behavior of a client and that is why LIC pay you the hefty commission.

Sunil & Basavaraj – When an Agent is genuine from his bottom of his heart and looking only to serve the needs of his/her Client, then the Agent will certainly promote term insurance. However, the situation is contrary. In reality, the genuineness is missing. Let’s take a hypothetical condition that all insurance companies start paying commissions only for selling term insurance and the commissions for the other plans such as endowment, money back, etc. are stooped, do you still think the same guidance by Agents would prevail ? Don’t you think the situation would totally reverse? :)…

This will never happen, companies will not give more commission to term insurance

Pathanapani-Insurance companies have to run their business. Hence, they float such plans and first they make agents scapegoat and indirectly to individual buyers.

Arun,

You have taken pain and effort in providing detailed explanation. Forgot about agents. For rest, it is not that they do not understand nor realize the calculations and difference and the loss. This mind set had been there for many decades that what ever goes out of our hands should be doubled or more, but should not get lost. So this mind set makes people to still take insurance + investment and they are okay for the 5-6% returns even after 20 or 25 years. You mentioned one important point, for me also agents asked me to put insurance on my wife’s name, when I asked questions, they told anything can happen to anyone and we will get money. So as long as they are okay to lose their money we should leave it. For genuine advise seeking people, still suggestions can be given

Yes Sudhakar, Its people mindset because of which so many endowment plans have been sold in past.

However, many a times, its wrong presentation of Total Returns to a perspective buyer who has just started a job and wants to save taxes.

Most of the Return calculation tables for these policies would show that a person who falls in 30% tax bracket will save Rs 30 Tax buy paying Rs 100 as premium and hence effective investment of Rs 70/- is growing to Rs 200/- to 250/- in 20 years.

However buyers forget that there are already many such instruments (80C) in the Market to save income tax such as

1. Employee Provident Fund (EPF)

2. Public Provident Fund (PPF in Post Office). Now a days few banks are also offering this as online investment in PPF instead of traditional post office.

3. Voluntary Provident Fund (VPF) – Additional PF deducted apart from Regular EPF.

4. Tax Saving ELSS (Mutual Funds)

5. Sukanya Samriddhi

6. Home Loan Principal

7. Child Education Fee Paid in Schools

Moreover people need to understand that Maximum Limit for 80C is mere Rs. 1.5 Lakh and most of this limit can be fulfilled by above mentioned instruments. So tax saving should not be a driving factor for any Insurance policy.

Further people needs to be educated that Similar to Term Insurance there are mortality Charges in traditional endowment policies which are never shown to clients and these are definitely higher than the Pure Term Insurance.

In term of Numbers, for a Term Insurance plan of Sum Assured Rs 1 Crore. approx. ANNUAL premium would be just Rs 10,000/- and in case of survival person won’t get anything on maturity. However in Endowment plans for same Sum Assured (Rs 1 Crore) the premium would be at least Rs 5 Lakh. Our of these 5 Lakh a hefty amount would be taken out as Mortality Charges and final returns on maturity would be much less than the “Term Insurance + Any other Invesment explained above”.

Only point People need to understand that in case of Endowment Plan insurance charges are hidden whereas in Term Insurance its clearly visible.

So if an agent explain this to their client with proper numbers on a sheet, I am sure nobody would deny Term Insurance.

You are 100 percent correct. Especially for people with salary cap of 10 Lacs and more, the normal PF, Housing loan Principal and PPF will exceed 1.5 Lacs. At some point we need to pay tax to government if we wish or not. Initially LIC plans were targeted mainly for Income tax and additional canvasing of lump sum and unfortunately this is still continuing. If you ask me people can opt for simple 50 L term insurance which will be hardly less money as premium. Few week end cinema is mall itself will cost 5 K per family. So people do not think from broader perspective.

But I hope this will start changing from now.

Sudhakar-But LIC plans mainly target sub Rs.10 lakh income individuals and also who are eager to SAVE tax. This is the reality and this how many get turned scapegoat.

Worst part about these policies is that it meets neither Insurance needs nor Investment.

Sum Assured is never sufficient because of hefty premium which a person can’t pay.

A person who earns Rs 10 lakh generally will go for S.A. of Rs. 20 lakh for which he would pay at least 1 lakh annual premium.

Here neither this S.A is sufficient nor the returns on investment which generally falls in the range of 5%-6%.

Plans are shown in a such a way that a person would never know the exact maturity amount. Thanks to assumed Annual Bonus and Loyalty bonus which are never clear.

An agent would show a rosy picture to buyer and get him trapped.

Arun-Yes and such selling is called as a social cause in nation-building.

Have spoken plenty about the agents and the people mindset.

Lets talk about the beast LIC itself and the word TRUST that everyone associates with them.

Take old Jeevan Anand policy that was in force from 2002 to 2013 or 14.

For 20 year term, The bonus declared in 2004-05 was 43/1000 and this year it is 45/1000. Basically the bonus has increased by 4% over a 13 year period while the value of rupee has reduced by 50%.

Also India has gone through 2 bull markets and a period of high interest rate cycle (nearly 12%) all of which would have boosted LIC’s returns including this year which their chairman has acknowledged with 40% more profits and promised to pay that as additional bonus.

Only that they have not done it. They keep paying same bonus year after year.

So how trustworthy an organisation is LIC?

How long can they keep saying they are govt org but continue to cheat people?

Basically govt has used LIC for its benefits, when they were not able to raise money they simply used LIC’s money.

Also LIC being govt org, their operations are very inefficient which mean lots of cost running it. This does not include agent cost which is fully funded by customers.

As far agents, just look at the Ads run by LIC on TV, they show the agents can earn sitting at home rather than work hard encouraging people to become LIC agents. How pathetic.

All of this eats into the returns and what we get is peanuts in the end.

So my opinion is people should shun LIC for what it is rather than embrace it in the name of TRUST.

When will people realise this?

Pradeep-This is what I am trying to say, each and every central Government uses LIC whenever they need money. Offer the sale of their stake in Public Sector Companies and force LIC to buy the holding. This is happening since long. But it does not mean I blindly trust LIC and risk my money.

When I am investing, then it is MY MONEY which matters to me rather than what LIC do for society or generate the employment to the country. If I am so generous, then I am happy to donate money to LIC rather than buy their product.

Frankly you can’t compare LIC product with mutual fund because in mutual fund you are investing whole amount into share market ,no liability on the part of fund manager to make guaranteed payment, as mutual fund returns are subject to market risk. Today mutual fund look Rosy because market at its peak ,crossed 33000. When modi govt cane into power in 2014 , sensex was at 17000 ,today is 33000. So growth is almost more than 100%. In life insurance traditional product ,first you have to ensure 100% return of capital means risk cover then you have to invest fund in govt securities which should be safe and assured returns.check mutual fund returns in 2008 to 2011,all the returns are in negative. Second ppf might offering returns a@ 8.40 but it’s not assured for next 10 years or 15 years or 20 years . Can any fund manager write on stamp paper that current returns will be guaranteed for next 10 years??

Now this LIC Jeevan shiromani product is offering benefits as 1) 125% more risk cover means 1.25 crore sum assured + guaranteed bonus on death for amount of 1 crore 2) 5 lac every year for first five years and 5.5 lacs for next till premium paying term for sum+ loyalty additions assured of 1 crore.3) money back minimum 30%. On 10th ,12th years means 30 lacs payble for term of 14 years ,35% on every 12 & 14th years for term of 16 years, 40% on every 14 & 16 the years for term of 18 years ,45% on 16th & 18Th years for term of 20 years 3) in built critical illness – for 15 specific diseases – 10% for means 10 lacs payble for 1 crore sum assured 4) option to defer the sb payment any time and can take with interest.5) loan 90% of premium is availability after one years 6) death or maturity can be taken in next 5 or 10 or 15 years with interest either yearly or half yearly or quarterly or monthly option. 7 ) as per calculation minimum guaranteed maturity amount is payble under term of 14 years-1 crore 75 lacs, for 16 years 1 crore 86 lacs , for 18 years it’s almost 2 crore , and term more than 20 years 2 crore 10 lacs which is guaranteed even after 20 years. So never compare LIC product with mutual funds. we know that those who are selling mutual funds always target LIC because LIC only gives guaranteed bonus ,first risk cover.

Rajan-Well articulated to give the seeds of GUARANTEE at the cost of savings account interest by LIC products. Today market may be ROSY (as per you), but the investors like me who invested more than 10 years back, it does not matter even if the market fall to 50% from current level. I still be happy with my 12% expected tax-free return. Hence, if you don’t know, you are not confident of how to invest or learn, then it is your problem. It does not mean we must all invest in so-called GUARANTEED product and burn our future financial life by satisfying NEGATIVE REAL RETURN.

When the Term Life Insurance and Critical Illness products are available at damn cheap rate by insurers (including YOUR OWN LIC), then why I have to stuck to this product???

LIC NOT GIVES GUARANTEED BONUS but only few products offers GUARANTEED ADDITION, but at what COST???? Keeping money in a savings account is better than buying such crap (by properly buying term plan).

Never try to COMBINE INVESTMENT WITH INSURANCE. When someone point at you INSURANCE coverage, you people JUMP AT INVESTMENT and GUARANTEE and whenever point low return, then sudden you jump at inbuilt INSURANCE.

We only ask people yo check mutual fund returns from 2008-2011.. people will get answer..all were in negative..I know your are mutual fund seller ..where you get four types of commission which people are not aware..

You only try to sell your product. Which is understandable..but please tell people how much commission you are earning in mutual fund..there are four type of commission..tell truth…we are eager to know..how much you are earning commission on mutual fund…

Dear Rajan, I believe many are taking this discussion personally, which should not be the case. Point here is what is good for an individual when it comes to investment of one’s hard earned money. I am an individual salaries person, and by my experience understand various products.

Here no one is imposing to by Mutual Funds or any Policy but trying to compare and show the facts with appropriate numbers which an aware person can understand and take informative decision.

By the way, as said earlier, apart from Mutual Funds, there are many other safe products which would give better returns then any endowment policies.

And for Mutual Funds itself, I do invest in it and don’t pay a single Rupee as Commission to any broker.

Kindly google about Direct Mutual Fund category where a person can by directly from an AMC (Asset Management Company) instead of buying through any brokerage firm. Compare the EXPENSE RATIO of two type of Funds Direct Fund and Regular Fund. You will understand the in Direct expense ratio would be somewhere between 1 and 1.5 whereas in Regular it would be between 2 and 3. The difference is called Commission.

Moreover there is no need to go for only Mutual Fund if you want low but safe returns.

One can choose Term Insurance and any safe Investment (PPF, EPF, VPF, Sukanya Samaridhi, Banks RD). With these you would get a very High Life Cover and much batter returns on your investment than endowment policies.

Its all, one wish and not an old belief to understand various investment instruments available in market and then take an informed decision.

Disclaimer : I am an individual investor and not associate to anyone in any form.