Do you believe it? Two third of adults over worldwide are financially illiterate. Shocking but the reality. This is the data from Standard & Poor’s Ratings Services Global Financial Literacy Survey of more than 150,000 adults in 148 countries in 2014.

This shocking revelation is not only from developing countries but also from developed countries. The country-level financial literacy ranges from 71% to 13%.

What are the parameters considered to arrive at literacy level?

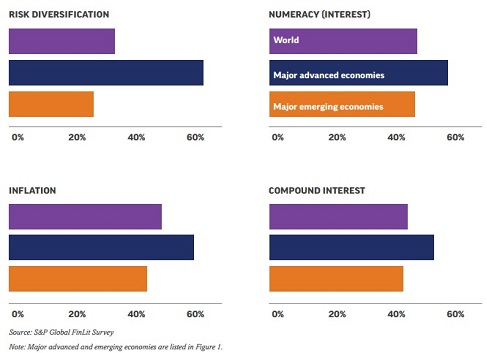

- Risk Diversification-Let us say you have Rs.1,00,000 to invest. How will you invest? Whether you put all money in one asset class or put it in different?

- Inflation-“Suppose over the next 10 years the prices of the things you buy double. If your income also doubles, will you be able to buy less than you can buy today, the same as you can buy today, or more than you can buy today? “

- Numerical (Interest)-Suppose you have to borrow Rs.100. Which is the lower amount to pay back-Rs.105 or Rs.100+3% interest?

- Compound Interest-“Suppose you put money in the bank for two years and the bank agrees to add 15 percent per year to your account. Will the bank add more money to your account the second year than it did the first year, or will it add the same amount of money both years? “

Based on above questions, a person is said to be literate, when he or she correctly answers at least 3 out of 4 questions. Based on this, around 33% are ONLY literate and rest of them are considered as illiterate.

Below are some interesting findings of this survey.

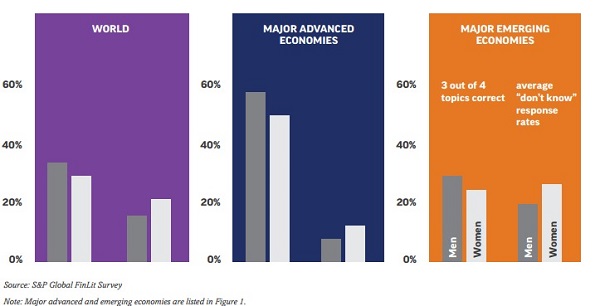

- On average, 55 percent of adults in the major advanced economies–Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States–are financially literate. But even across these countries, financial literacy rates range widely, from 37 percent in Italy to 68 percent in Canada.

- BRICS (Brazil, the Russian Federation, India, China, and South Africa)—on average, 28 percent of adults are financially literate. Disparities exist among these countries, too, with rates ranging from 24 percent in India to 42 percent in South Africa.

- Higher GDP countries have higher financial literacy.

- However, education, consumer protection and shape of financial literacy are major factors.

- Inflation and numeracy are the most understood topics worldwide.

- Knowledge of risk and diversification is lowest. The same is explained in below chart.

- People who faced the reality in their life are more understandable about the concepts like inflation.

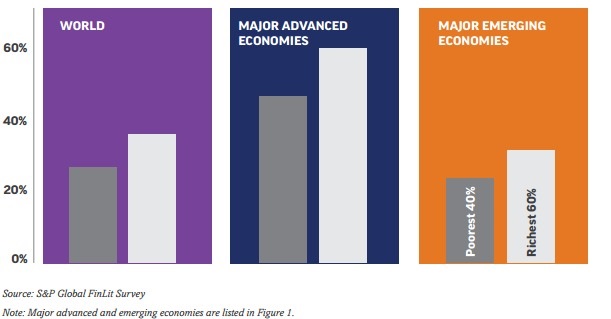

- Lower financial literacy among women and the poor.

- Financial literacy grows with age but later decline ( adults age 65 plus have the lowest financial literacy rates of any age group).

- Financial literacy grows with income.

- Adults who lack in accounting also lack in financial skills.

- Credit is more common rich countries than poor.

- Credit cards are gaining popularity. But sadly how interest is calculated or interest concept is totally low.

- In this report, India stands at 24% financial literacy.

The complete details is available at “Standard & Poor’s Ratings Services Global Financial Literacy Survey“.

Dear Mr. Basavaraj,

First of all I would like to thank you for your wonderful posts, sharing / advice to people like us.

And I am fully agree on this article

I need your valuable advice on

1) Child Education

2) Medical Insurance

3) Life Security ( Increase Wealth)

4) Term Insurance

Firstly I would like share about myself, I and my wife both are working professional, and we have son of 10 years.

Today I am keen to looking for Investment/securing the future. On the above said points

1) Child Education: – It is most important thing which I need to act, as he is now 10 Years old need big amount for his graduation.

2) Medical Insurance: – I am looking for medical insurance plan/company for the family i.e. me, my wife and son for long term, as its required later stage of age.

3) Life Security: – I have one long term policy (Jeevan Saral from LIC) and currently paying 72000 Rs P/A. Need your advice on planning of SIP, Mutual Funds ( I am not having basic knowledge on that or funds type).Appreciate you if you please elaborate more on this. I can invest approximate Rs. 25000 to 30000 PM. Also looking for life insurance for family members.

4) Term Insurance: – Please suggest on the part of Term Insurance, I am looking for at least 1 cr for individual of us.

Today I am reading your article on Jeevan Shikhar : – Which is very good and saved me ?

Also please suggest on Jeevan Saral, I bought this policy 4 years ago.

With Warm Regards

Vishal-Financial planning can’t be done in comment section. If we do like this, then it is more harmful to you than me 🙂

Great Post and Agree With you that Around 100% of population only 2-4% are literate about financial inches and rest 98% are just depending on brokers or cheap consultant even after they are charging them huge amount and even in return they are not getting their excepted results ….

Nice post about S&P survey.

Although I think number of questions could be little more (around 10) so that we could have got better picture (or still worse?). However, it might have been designed by S&P so that all candidates could complete it.

Findings of the survey are on the expected lines. However, couple of findings are interesting. One is financial literacy improves with age but falls after crossing 65 and people who lack in accounting also lack in financial skills.

In case of India, one has to concede that financial literacy is abysmally low. I have seen many people who do not know how to calculate compound interest. They do not pay heed to inflation while making investment decisions forget about Risk diversification.Hence, any LIC agent can fool them by inducing them to buy pathetic traditional plans like endowment and money back plans where one neither gets insurance cover nor inflation beating return. Ads of LIC boasting 40 crore odd existing policies in India is a proof. I hope the condition will improve in years to come

Thank you for sharing

RiteshM-Pleasure to read your views 🙂

Thanks.

One more thing. If we apply these results to our country, we can safely conclude that 3 out of 4 Indian adults are financially illiterate.

Shocking but true for a country aiming to become financial hub of the world.!!!!!

RiteshM-True 🙂