When I wrote a post about recent changes in the Employee Provident Fund (EPF), I received so many queries related to Employee Pension Scheme because there is a huge misconception among employees about EPS. Hence, let me write a post on this in detail.

Note-We have deactivated commenting on this post. However, if you have any doubts regarding EPS, then you can raise them in our Basunivesh Forum.

Latest Post–Difference between New Pension Scheme (NPS) and Atal Pension Yojana (APY)

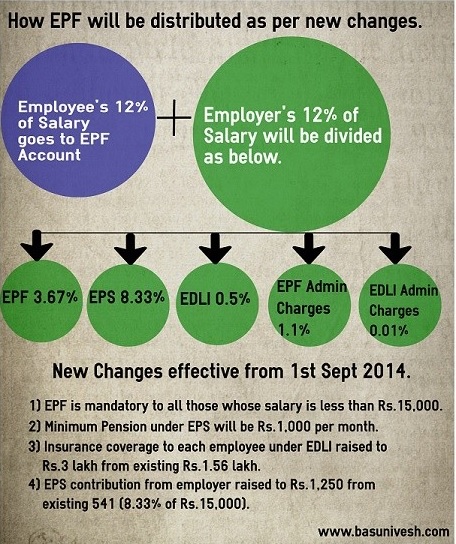

In the below image, I have tried to explain how your’s and employer’s EPF contribution is distributed. Many of EPF members at the first instance do not know that they have a pension scheme and for which their employer is contributing.

You will notice that the major portion of your employer contribution will go towards the Employee Pension Scheme (EPS). However, the majority of employees are ignorant about this.

Few features of these schemes are-

- Employees who are members of EPF will automatically become the members of EPS.

- Along with your employer contribution of 8.33% of your salary, Central Govt. also contributes 1.16% of employees’ monthly salary. Here the meaning of salary means Basic+DA. The rulebook still sticks to the old salary limit of Rs.6, 500 limits for an employer and central government contribution. However, in my view after the new rules, the limit should be raised to Rs.15, 000.

- You will not get any interest on your EPS contribution.

- For calculation purposes, if your service is more than or equal to 6 months, then it will be rounded to next year. If it is less than 6 months, then such fraction of service period is not considered for calculation. For example, suppose you worked for 21 yrs and 7 months. In this case, your service is considered as 22 years. However, if your service is 21 yrs and 2 months, then service will be considered as 21 yrs only.

- Pensioner receives a pension for life long and upon his death will go to spouse and two children below 25 years of age

- Employees are eligible for EPS only if they complete 10 Yrs of service or attain the age of 58 or 50 Yrs of age.

- You will not be eligible to receive more than one pension from EPS.

What is an eligible service for EPS?

As I said above, for calculation purpose, if your service is more than or equal to 6 months, then it will be rounded to next year. If it is less than 6 months, then such fraction of service period is not considered for calculation. For example, suppose you worked for 21 yrs and 7 months. In this case, your service is considered as 22 years. However, if your service is 21 yrs and 2 months, then service will be considered as 21 yrs only.

What is pensionable service for EPS?

The pensionable service is determined by the number of years your employer contributed on behalf of you. If your employer failed to deposit the amount then such months are not considered for calculation of service. Also, in case if an employee completed 58 yrs of age and completed 20 yrs of service or more, his pensionable service will be increased by 2 years for calculation purpose.

What is a pensionable salary for EPS?

It is the last 12 months average salary during contribution period preceding the date of exit from the membership of EPS. In case employee did not receive full payment during that last 12 months, the average of last 12 months full pay drawn by him during the period for which contribution to the EPS was recovered, will be considered for EPS calculation.

In case of such last 12 months, employee hasn’t contributed to EPS, including cases like where the employee has drawn a salary as part of a month, the total salary during the 12 month span will be divided by the actual number of days for which salary has been drawn. The amount so derived will be multiplied by 30 to arrive at an average monthly salary.

When employees get the pension?

a) Superannuation-To avail such pension, you must complete 10 yrs of service and your age must be 58 yrs or above. An employee can continue his job while receiving his monthly pension. However, he cannot be a member of EPS and hence no more fresh contribution to EPS.

b) Early Pension-To avail such pension, you must complete 10 years of service and age between 50 yrs to 58 yrs. To avail such early pension, an employee must not be working.

c) Death of an employee-Employee is eligible for EPS if death occurs as below.

- If death occurs during the service-If at least one-month contribution is done to EPS then his nominee will be eligible to receive the EPS.

- If death occurs while not in service-If death occurs after the service but before attaining the age of 58 years.

In both the cases also employee family eligible for a pension. In case of dead employee having a family, a pension is payable to the spouse and two children below 25 years of age. When a child reaches 25 years of age, the third child below 25 yrs of age will be given a pension and so on.

If the child is disabled, he may get a pension until his death. Only 2 children will receive a pension at a time. In case of an employee not having a family, the pension is payable to single nominated person. If not nominated and having a dependent parent, the pension is payable first to Father and then on father’s death to Mother.

d) Permanently and totally disabled-If an employee is unfit to do his job due to accidental permanent and total disability during a job, then also he is eligible for the pension.

How to calculate the Employee Pension Scheme pension?

There are two methods based on the service you joined. One is for those who joined before 15th November 1995 and another for those who joined after this date.

1) Employees who joined before 15th November 1995-

The pension is calculated separately for Past Service & Pensionable Service

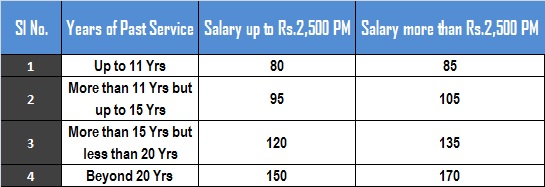

a) Procedure for Calculation of Past Service Pension

- Find out the total past service, i. e. subtract the Date of Joining from 15.11.1995 duly rounding the service in years.

- Find out the salary as of 15.11.1995 as to whether it is up to Rs.2500 or more than Rs.2500.

- Accordingly locate the past service benefit from the table given below.

- Find out the period that had elapsed between 16.11.1995 and the date of exit and based on this period locate the corresponding Table ‘B’ Factor. Date of Exit is Date of attaining 58 years for superannuation/early pension, Date of Death for widow pension and Date of Disablement for Disablement pension.

- Multiply the Past Service Benefit and the Table B factor, which gives the Past.

b) Procedure for calculation of Pensionable Service Pension–

- Find out the Category of the member as to whether he belongs to X, Y or Z Category.

- X – Date of commencement of pension is between 16.11.1995 and 15.11.2000 Y – Date of commencement of pension is between 16.11.2000 and 15.11.2005 Z – Date of commencement of pension on or after 16.11.2005.

- Find out the Pensionable Service and Pensionable Salary of the member and substitute the same in the formula given as below.

(Average Salary X Service)/70

- If the formula pension calculated is less than 335/438/635 respectively, for X, Y, Z categories, then only that minimum pension is to be given.

c) Procedure for the calculation of Total Pension-Add the Past Service Pension and the Formula Pension.

- Add the Past Service Pension and the Formula Pension.

- If the total pension is less than 500/600/800 respectively, for X,Y,Z categories, then that minimum pension shall be the total pension.

- But this total pension is for an eligible service of 24 years or more, and if the eligible service is less than 24 years, then this total pension has to be proportionately reduced subject to a minimum of 265/325/450 depending on X,Y,Z categories (only when the minimum pension is given).

- If the total pension itself is more than the minimum, then the proportionate reduction need not be made even if the eligible service is less than 24 years.

2) Employees who joined after 15th November 1995–

You can directly calculate by inserting the values in the formula as given below.

(Average Salary X Service)/70

You can find the wonderful, detailed calculation of this with an example at HERE or at HERE.

How to apply for the pension?

Once you complete the service of 10 years, then you get the scheme certificate. This scheme certificate can be used to claim your pension either from 58/50 Yrs.

The employee has to include all his past services to arrive at such 10 yrs of service and apply for pension once he attains the age of 58/50. He needs to fill the Form 10D and get attested by that bank manager with photo and other required documents. Submit the form to concerned EPFO.

Whether one can withdraw the EPS amount before 10 years also?

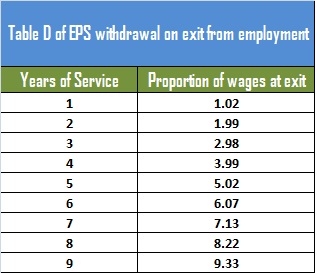

Yes, you can withdraw the contributed EPS amount along with your EPF balance. But the condition is you must not have completed 10 Yrs of service. When you withdraw EPF, then you receive EMPLOYEE+EMPLOYER EPF contribution+Interest earned on this EPF. Along with that, some % of EPS contribution also be paid. This % is determined by Table D of EPS, which is given below. Hence, whatever may be your contribution to EPS, you will get only some % of this based on the number of services and salary.

This is calculated as below.

Wages as on the date of exit X Corresponding Table ‘D’ factor. Here wages means Basic Salary+DA for EPS at the time of withdrawal. Therefore, suppose your salary is Rs.15,000 at the time of withdrawing and you completed 7 years, then you receive the EPS of Rs.1,06,950 (Rs.15,000*7.13). This is the amount you get, irrespective of your actual contribution to EPS. You have to submit the Form 10C along with other forms of EPF withdrawal to your HR.

Note-I found that still EPFO not updated the manual as per the new changes. Hence, I am unable to find the corresponding values for calculation. Whenever it is updated then I do changes here also.

Note-We have deactivated commenting on this post. However, if you have any doubts regarding EPS, then you can raise them in our Basunivesh Forum.

Hi, My name is Murali, now I am working in Pvt. concern past 11 years and now pension scheme activated with my account. Now I plan to start a business and completely close to my PF and Pension scheme also. I don’t know the procedure to close my Pension scheme. My age is 32 years.How to surrender my Pension scheme certificate and how can get the amount? Somebody says the pension scheme amount not pay to you before the age of 53 years. because of i have doubt , I don’t know how many years of we are live ? If my saving amount not used to me in my critical situation, what is the use ?

Murali-Please refer above post. The age is not 53 years. But between 50-58 years of age.

My service 12 years .

PF deduct from my salary 1004 /- monthly & 1004 /- pay by company total rs 2008 /-

How we can get full amout

Please confirm process .

Amar-How can I get full amount means?

Hi,

My father has took VRS in 2005. Now they don’t have any another income source. So they can withdraw the EPS ( Pension ) amount?

Please let me known.

Shishir-It depends on above rules. Please refer.

Hi,

My father has completed more than 20 yrs service. So can they get amount.

Shishir-Yes.

Thank you so much.

Can you please tell me the Procedure for that.

Shishir-Please contact the concerned EPFO.

hello sir,

I worked for Company 1 for 6 yrs. The company maintained EPF and EPS through RPFC.

I then moved to company 2. This company has exempt trust for EPF and EPS is through RPFC. I filled form 13 for transfer and PF is transferred and shown on 2nd company’s internal portal. How to know status of EPS.

Question 1: I raised grievance with RPFC of company 2 for eps status and they are asking for Annexure K. Whom do I get annexure k from. RPFC of company 2 sent mail to RPFC of company 1 but no response. I raised grievance with RPFC of company 1, they replied annexure k already sent in 2014 to registered mail id but I never received it.

Question 2: I have now resigned and moving to company 3. If I fill form 13 through company 3 will details of EPS from company 1 and EPS from company 2 both get transferred to RPFC of company 3.

What should I do in this mess, transfer or withdraw. The passbook on UAN portal also does not show anything to me it just says “Passbook not available as pertain to exempted establishment (i.e. Trust)”

Please help.

Alice-Raise the issue with EPFO Grievance Portal online.

I have worked in a company for 3 years and then started my own business. I claimed the EPF amount but Pension Contribution (Rs 25900) is still pending. What is the procedure to claim it and will I get the whole amount?

Thanks

Vivek-You have to submit forms for withdrawal.

Hi Basavaraj,

I am Rajesh, I have served in a multinational company for 12 years. I quit the job on 2009 and started some own business. now I am thinking to withdraw the EPS amount. My current age is 45. Can I withdraw my EPS?

Rajesh-You can.

Mr. Basabraj Tonagatti,

May I comment some thing on the clarifications given by you under EPS, 1995 as there is much material to be deleted and be added or rectified.

Secondly may I further clarify the queries raised by the public and replied by you as I observed that the

queries are not properly replied and put in confusion . there is also a language problem in your clarification, I think that can not be rectified at this stage

Katoch-If your intention is to help people genuinely, then you are always welcome 🙂

My pension and arrears were sent to the bank for credit. There was 48000 RS as recovery amount in arrear. After deducting this 48000, my arrear was 96000. Bank added both 48000 and 96000, applied hold on 144000 and my main balance went debit 48000. I approached them on which they told that there is some recovery. I credited the account with 50000 so the main balance now was now credit 2000. They are now telling that the EPFO office has applied the hold due to recovery. I want to know can EPFO office control the bank account. Who will now remove the hold? There is no recovery as such and all documents are submitted.

RAvindra-I don’t about EPFO. But surely bank is playing with you.

Sir,

Our organization named international development enterprises( India) and I have contributed to pension scheme from my PF account Rs. 116526/- as per the EPF pass book balance is confirmed. I have contributed pension from 1999 april and my PF account no. is DL/22204/187 in south Delhi. now I am age of 53 perhaps our organisation may continue maximum up to three years. can you tell me on my pension contribution amount how much I will be eligible for getting pension per month. The figure is always enchanting me for certainty.

Regards

Debadas Pattnaik

Debadas-It is hard to say at this point.

Plz sir, any perceptiveness? what ever may be the amount but should I cherish a hope of Rs. 2000/- per month. I have already given the assured sum and time of service. So whats hardness to calculate the same. Plz give us some amount of hope for monthly pension . We don’t want exact amount to be received. but any perception?

Regards

Debadas Pattnaik

My full pension is Rs.1099/-. I have completed 58 years on 20/05/2015.

From 1/12/2008 till date I was paid Rs.826/- ie., @4% per year for 6 years (early pension) 24% was deducted.

The arrears due is as follows:

20/5/2009 to 19/05/2010 for 12 months @ Rs.44/- per month = Rs. 528

20/5/2010 to 19/05/2011 for 12 months @ Rs.88/- per month = Rs.1,056

20/5/2011 to 19/05/2012 for 12 months @ Rs.132/- per month = Rs. 1,584

20/5/2012 to 19/05/2013 for 12 months @ Rs.176/- per month = Rs. 2,112

20/5/2013 to 19/05/2014 for 12 months @ Rs.220/- per month = Rs. 2,640

20/5/2014 to 19/05/2015 for 12 months @ Rs.264/- per month =Rs. 3,168

—————–

Rs.11,088

20/05/2015 to 30/06/2016 for 13 months @ Rs.273/- per month Rs. 3,549

——————-

Total arrears payable as on 30/06/2016 Rs.14,637

——–

Am I right ? in claiming the arrears ?

Madhusudhan-Cross check with EPFO.

Hi how to transfer widow pension scheme 1000 directly to the bank account?what is the procedure to do that?

Charan-Contact EPFO.

Dear Mr. Basavaraj,

In my previous company they having PF Trust, and EPS they maintaining through government only.

I left pre. org on 31st July 2016 after working of 6 years. I withdrawn my PF amount, and EPS amount is still pending, Currently I joined another company. Can I withdrawn my EPS amount too? If yes then How? or is it require to transfer in new organization? (They are not maintaining trust)

Please suggest.

Thanks In advance.

Rajesh-Better to transfer.

Thanks for your quick response.

But as required some amount presently.

So is it possible to withdraw EPS too.

If yes pls suggest.

Thanks

Rajesh-NO.

Hi Basavaraj Tonagatti,

I do have a query regarding my tenure,

I started my job from apr-2006, my pf account created on May-2006.

My contribution made from (you can say May-2006)

Organization I

1. May-2006 – Sep-2008 (29 Months)

2. From Sep-2008 – Jul-2011 (I was out of india, under the same organization and no contribution made during this period) (2 Years 10 Months around)

3. Aug-2008 – June-2015 (47 Months)

Organization II

1. Oct-2015 – Till Now (Still serving)

I did my pf transafer from my first org. to my Second Org. In comment of my pf transfer it stating like (09 Years, 02 Months, 02 Days). So my query is am I eligible for scheme certificate after 3-4 months (Since as of now I already served around 9 months in my current organization) ?

Second query is untill when my pension part will be deducted from the emplyee share…?

Galvin-You will be eligible. But do you want to start your retirement? If not, then why you want the pension certificate now? EPF and EPS will be as long as you work and meant for long term wealth creation for your old age.

Thanks a lot, but I am not seeing any benefit for continuing eps for next 10-20 years….what I will get only 5k or 6k, I will get more in epf interest rate instead of eps return…………..I m thinking that if I get scheme certificate then I believe the deduction of eps part from the employer share will stop…. and the whole amount will be credited in epf balance…… I m not sure about it…..but if it happens like that then I will get more return than eps……what do you think on this ?

Galvin-Do you feel by getting scheme certificate your contribution to EPS will stop automatically from the existing EPF? Check the rules.

Galvin-The problem is, you can’t stop from employer EPS contribution.

Hi,

I have worked for 2 years and 9 months. If I submit form 10C on closure of PF account and the total amount contributed towards EPS till date is Rs.32,005 by the employer, but my current basic pay is Rs.19,000 will I receive 19,000*2.98 = Rs.56,620 towards EPS even though my employer hasn’t contributed as much till date. If not how do I calculate the amount I’ll receive towards EPS. I’m closing my PF account because I have to move outside the country.

Thanks in advance.

Naman-It is based on Table D.

Dear sir,

I was working with wipro infotech, I left job and then i withdraw my e.p.f . as I got my p.f. check 45 days before but, i didn’t recieve my E.P.S money so, how much time it will take to clear.

Avinendra-Check with local EPFO.

Hello Sir,

After working for 4.5 years and changing my job I had withdrawn my EPF. I got around 3 lakhs in two separated transaction, in 2010.

Now in the current company I have already worked for 6 years.

1. So how my ‘total no of years’ be calculated? is it 6 years or 10.5 years?

2. At the time of did I get the EPS amount also? If so, can I repay all my money with penalty and interest so that my number of years be increased so that I cna get maximum pension?

Please guide.

Manoj-1) 6 Yrs. 2) You can’t do so.

Sir, i have transfer my pf in current PF account but i have received only my pf part where as pension part is still pending and i havent received,so please advice me whether this amount i will get..?

Deepak-Wait for a week. If you not received then raise the issue with regional EPFO.

Hi Basa,

I had opted PF transfer while switched over to next company, And EPF amount was transferred to current company but EPS amount is not transferred.

Note: Previous company maintains PF in EPO but current company has trust to handle PF.

Could you please assist me on how to get transfer EPS amount from previous to current company?

Senthil-It too transferred. If you have doubt, then contact regional EPFO.

Hi,

I withdrew my full EPF and EPS in the year 2015 and my service period was only three years. The EPFO deducted income tax on EPF but not on EPS.

Can you confirm, if I have to pay income tax on EPS as well. If it is exempted, under what head can it be shown (u/s section 10 of income tax)

Thanks,

Raghu

Raghu-It is not exempted income. YOu have to show it as salary income.

Hi Sir,

Thank you for your response. I believe you are referring to EPF which is taxable. I want to know about EPS which was also refunded by the EPFO but not taxed. I found the following section in IT act section 10:

Payment from approved superannuation fund in specified circumstances and subject to certain limits [Section 10(13)]

Approved superannuation fund means superannuation fund which is approved by the Commissioner of Income-tax. Tax treatment of such fund is as follows:

? Employer’s contribution is exempt from tax, however, from assessment year 2010-11 employer’s contribution in excess of Rs. 1,50,000 per annum is charged to tax as perquisite. Employee’s contribution qualifies for deduction under section 80C and interest on accumulated balance is not liable to tax.

*Payments made from the fund are exempt from tax under section 10(13) in following cases:

? Payment on death of beneficiary; or

? Payment to employee in lieu of, or in commutation of an annuity on his retirement at or

after the specified age or on his becoming incapable prior to such retirement; or

? Payment by way of refund of contributions on the death of a beneficiary; or

? Payment to employee by way of refund of his contributions on leaving the service in connection with which the fund is established otherwise than by retirement at or after a specified age or on his becoming incapacitated prior to such retirement; or

? Payment to employee by way of transfer to his account under a pension scheme referred to in section 80CCD.

Can you confirm if I am correct.

Thanks,

Vaibhav

Vaibhav-EPS is taxable. You are quoting EPF rules and superannuation fund rules.

Hi sir I worked with company for 3years and 6 months. I submit a application to withdraw my eps one and half month ago but havn’t got any money or reply from them.can you please tell me how long it will take. And how much i will get like full amount which is showing in my EPS or any percentage??

Thanks & Regards

Gurjot Singh

Gurjot-You can wait for another 15-20 days, then raise the issue with local EPFO.

I contributed to EPS account for 13 months only and after that stopped contributing to EPS due to 58 yrs of age but still contributing to EPF account. Am I eligible for applying for pension? If not, then should I withdraw my contribution as no interest is provided on EPS. I am still active member of EPF. Thanks & Regards. B.R. Chaudhary

Chaudhary-If you completed 58 years of age, then you can apply for EPS.

I have worked for company for last 3yrs and 8 months, so my table amount will be as for 3yrs (2.99) or 4 Yrs (3.98)

Pradeep-4

Hi

i have worked with an Co. for 1 year 1 day where the PF is maintained by such Co. via creating trust.

where my basic is more then 15000 still co. deposited 8% in EPS maintained at EPFO and remaining 4% in PF at own trust.

at the time of leaving organisation i filed PF withdrawal form with EPS 10-C, resultant PF balance in my account maintained under trust is processed but EPS balance is not processed as asking for UAN where the UAN No. is not updated to me.

further in an communication with organisation giving a reason that in the absence of UAN the refund of EPS was not processed by concern regional EPSO office.

where communication with EPSO office responded that your employer should have your UAN and should produce the same while submitting any withdrawal form with office.

the query is EPSO office is provide response that at given EPS No. no contribution is made by mentioned company and we are not holding any balance in given no.

now how to process the withdrawal of EPS and how to get UAN.

Hitesh-In that case it is your employer who should be liable to pay. Show them the reply of EPF. If they still not budge, then complain against employer with EPFO.

Hi Sir,

I have withdraw my whole PF amount in April-2016 and no Pension (10 C) form has been submitted at that time. Can I withdraw Pension now by submitting only 10 C form.

I have completed 8 years of services and after UAN its completed 4 years.

Please advise how can I proceed to withdraw my Pension amount.

Supriya-Yes, you can withdraw. Contact your employer or regional EPFO.

Thank you so much for your valuable advise.

Hi,

I have worked with ABC company from 2011-2015 . I have a UAN number and PF account linked which I have withdrawn. When I joined new company XYZ, I don’t know what there procedure were.. they have provided a new UAN. Now I have 2 UAN (obviously with different contact number). I want to know is it the right process? and what will happen with my old UAN? Will it get automatically closed or is there any way I can link previous mobile number to my new mobile number. Please advise.

Regards,

Priyanka

Priyanka-One must have only ONE UAN. But it happened accidentaly. So try to retain the new one for future. For new UAN, make sure all your KYC details are upto date.

Yep, All KYC details are upto date. Now what about my old UAN. I tried to link my phone number with new UAN but as it was already registered with old UAN, I am unable to update it. Can I request to close the old UAN ?

Priyanka-Better you close either old or new. But retain only one UAN.

Hello sir,

Mene 1.5 year job ki he,

Mera total pf deduct 17,000 huva he,

Mene last 3 month se resign kits he,

Ab mujhe 17000 ka double 34000 pura Paisa milega ya aadha Paisa pension me chala jayega?

Dhaval-It is not double. But depends on total accumulated amount. Check your balance.

Hi ,

I have a question , I started working from July-2006 and stopped working at March-2014.

After I resigned I didn’t withdraw my PF amount to avail pension scheme. I thought on July 2016 I’ll complete 10 years to get the eligibility for pension.But, as I read above my contribution/employer contribution ended on March-2104.

So, please clarify me will I be eligible for pension?. Another question I have is if I withdraw my amount will there be any conditions? like tax/not able to withdraw full amount.

Please help me to decide .

Thanks,

Shabana.

Shabana-Your EPS not completed 10 years of contribution. However, you can withdraw and the payable will be based on Table D.

Hi,

My Mother in law used to get pension as a widower of my father in law. She passed away recently, and their children want to close the bank account. They have been told to go to the EPS office and complete the formalities. Can you please help understand what formalities needs to be done?

KD-I am not aware of formalities. Plese contact regional EPFO.

I have worked in a company for 2 years 2 months and now have joined a new company, i have transferred my EPF to new company and is reflecting in new passbook, as i am continuing to work in my new organization, can i withdraw EPS as EPF is already transferred?

Vishwas-No, you can’t.

I had worked in Pvt Ltd. Company from 01.02.1996 to 31.12.2006. The tenure of service was 11 years + pensionable service was 11 + 1 year Bonus & pensionable salary Rs. 4273/= as per Scheme Certificate sent to me by EPFO. Now I need to withdraw early pension as I attained the age of 50 yrs.

Now kindly advise me how much I get the early pension.

Please suggest me.

Soumitra-It is explained above.

Hi,

I worked for a period of 5 yrs 4 months. I’ve applied for claim and got EPS amount Rs 43955 but as per information I searched in Google table D, the formula for calculating EPS is last basic salary * 5.02

My basic salary was 24000, so I expected 24000 * 5.02 but what I got is less than that. Could you please clarify?

Thanks

Ravikiran

Ravikiran-If you have doubt, then raise the issue with EPFO.

For EPS withdrawal calculation purpose the basic is considered as 15000 max.

Kavish-It is explained above.

Hi Sir,

I’m trying to generate my UAN number but its showing the UAN number is already generated for the updated mobile number. Can you please guide how i can go further.

Regards,

Reshma

Reshma-Check with your employer whether the UAN generated or not.

Hi,

I worked for 10 months in private company. How do we know whether I am a member of EPS? When I checked my balance at EPFO website, I received SMS which only stated 2 components: EE, ER.

Eklavya-You are the member of EPS. If you have doubt, then check with EPFO or your employer.

Hi,

My brother joined one MNC on Aug 04, 2008 and died on September 07, 2008

The company was registered with EPFO and has deposited 4640 as his one month pf. The company was also registered in EDLI scheme

We have now filed claim from employer which they have also agreed

Can you please let us know how much EDLI amount and pension will be provided? Whether the pension my parents will get start from September 2008?

Thanks

Manish Kumar

Manish-Refer above post for pension and EDLI will be Rs.6 lakh.

Hi…I tried understanding but could not get through…..can you pls let me know the pension amount…just and idea…because it is very confusing….also I guess the EDLI limit is only 1.35 lakh

Pls explain

Thanks

Manish

Manish-Do you feel for just one month of salary contribution one will get pension? NO…I am not sure how much was EDLI in 2008. Please check with his employer or regional EPFO.

One month of contribution is required for pension eligibility. Just wanted to know bout the calculation

Manish-I don’t think so.

I resigned form my last job, I got refunded my EPF ( my contribution + partial Employer Contribution) . Remaining of the Employer contribution is went to EPS account.

I counted the total amount is deposit to EPS is 36000 Rs. I was with that job for 7 year and 2 month. how can i apply to get my EPS refund back , and how much approx I will get. should I need to wait till I grow 58Year or else.

Thanks

Raju-You have to apply for EPS withdrawal separately by filling necessary forms.

Dear Sir,

I am working in a private company since 01/12/2006 at vapi gujarat

I want to know that there is mistake in my name and date of birth my name spell is pragnesh but in epfo it is prgnesh (missing letter “a” and my date of year is 1982 but at epfo it’s 1992, and in all documents (KYC) adhar card / pan card / bank account submitted it is correct.

so I want to know that need to change at epfo? creates problem at time of withdrawal? and if yes what is the procedure for that.

Thank you

Regards,

Pragnesh

Pragnesh-Better to change and you can do that through your employer.

You should tell your employer to fill form 5 and submit a photocopy of a valid ID Proof of yours. Then they will change in the portal

I have withdrawn my PF but I received the Pension certificate from the organization

I served for 10 years . After resignation from previous company I joined another company now want to transfer my pension amount to current company. what I have to do regarding this

Sameer-Quote the same EPF number.

1.For EPS withdraw (before 10 years) , basic pay or net pay will calculate. for ex. my salary 20k. basic 7k. year of exp 2. than for eps withdraw, 20000*1.99 or 7000*1.99?

2, How rounding works. for ex, 1.3 year will calculate as 2 or 1?

Karthikeyan-1) Basic. 2) only months will be rounded but not years.

How months will be rounded?. For example 1 year and 4 months who will round?

Karthi-In that case it is 1 year.

Hello Mr. Tonagatti,

I have served six organisations in past 14 years. I transferred my P.F amount from my first organisation having served for 3 years 9 months to my second organisation in 2006 however I am not sure if the Pension amount also got transferred. I say that because after serving the second organisation for 2 years and 8 months I requested for withdrawal of PF as well as pension amount. I received Rs.19500/ as my pension amount which if I go by Rs.541/ PM deduction,accounts for 3 years only whereas it should have been at least for 6.5 years i.e. 42000/ I wrote to EPS and they said that this is full and final amount. My query is as following

1. Can I do something now to get my pension fund from year 2002 to 2006

2. Will there be any tax deduction if I withdraw my PF after 5 years of commencement of PF account.

3. What do i do about small EPS contributions during my service in different organisations after 2006 as some of them are as small as 10 months

Thanking you in anticipation of reply

Regards

Gurpreet Singh Chani

Gurpreet-1) Yes.

2) NO.

3) Better to transfer to current EPF (if you are currently working).

One of our client has withdrawn PF in F.Y 15-16,before 5yrs. The amt withdrawn by him is taxable for the F.Y 15-16 (except EE’s Cntribution which will be Exempt from tax)

We had taken EE’s contribution under 80C as deduction in Previous Years do we need to revise Previous Year’s ITR.

Thanks

Pritesh-Yes.

Hello,

I have worked for 4.5 years in a company(A) from July 2011 to Dec 2015,and then moved to other company(B) in Jan 2016.Here are my questions

1. I had issue with UAN mapping because of DOB mismatch.So, my current employer(B) created new UAN. I placed request for PF transfer.In this case will my EPS amount be transferred into new PF account of new UAN

2. Can i withdraw my EPS amount now, after transfer.

3.What is to be submitted and where for EPS withdrawal.?

4. What is my service period considered as?Is it 0 years since its new UAN and New PF account after transfer? Or my earlier service period is considered and hence it is 5 Years.

Regards,

Swetha

Swetha-1) I doubt. Because UAN is already attached with old EPF. Creating new UAN was unnecessary.

2) NO.

3) You can’t.

4) Since earlier service.

I had EPS with my last to last employer and my last employer did not have any EPS provision and hence the EPS fund is lying with my 2nd last employer. Now in my current organisation, they again have the EPS facility. So is it viable to get the EPS transfer from my 2nd last employer and continue as my basic salary has hiked or else withdraw from there and start afresh EPS fund here. my service in 2nd last employer was 4.5 years with 10 months in last employer and just joined new employer.

Will I get benefit in transferring or withdrawing the fund and restarting here. If needs to be transferred then please guide how can I.. Thanks

Mukesh-It is BEST to transfer.

sir,my uncle died in 2001,from there my grand father receiving his pension.every year he has submitting life certificate but now pension stopped from January,..where should we contact ?

Vinai-EPF Office.

Dear Sir,

I have been working in an Indian company since 4 years(including 1 year as trainee). Now I got an offer from a gulf company(there is no contribution of EPF as I see in offer ) will soon join there. I checked in the EPFO website the company’s part of contribution is comprised both a fraction part for EPF and remaining part for EPS.

Now my questions are:

1)when I will be able to withdraw the money?

2)If I withdraw then I can able to withdraw all or a part of it. If it will be a part then which one EPF or EPS?

3) In case If I don’t want wish to withdraw and I leave it as a deposit money, then will there be any problem for claiming the account in future as I now fear if I able to withdraw it will be spended in some expenses anyhow.

please guide.

Regards,

Gurpreet

Gurpreet-1) Immediately. 2) You can withdraw full EPF and part of EPS. 3) Your account stops earning any interest after 3 years. Hence, better to withdraw.

Dear Sir,

I have completed 4 years 11 months and 25 days of service with my company and I am resigning the job due to some factors. I have seen my EPF balance as Employee Contribution (A) + Employer Contribution(B) + Pension Contribution(C). After 60 days of unemployment,

1. Am I able to with draw at least A + B without taxation?

2. Do I get interest on (A+B)? What is that interest Percentage if any?

3. When can I withdraw C? Is it after 10 years only even if I am unemployed? If before that, then only portion of current amount shown in e-Passbook can be withdrawn?

Hope your reply.

Thanks

PFQuery-1) Yes, but not without taxation. Even you can withdraw C (but partially based on your service).

2) Yes, it depends on yearly rate of interest.

3) Now..you can withdraw. But partially.

Sir, I have received the scheme certificate for service of 10 years from my previous employer eight years back and now i am working in a new company for 10 years. Total years of my service is about 20 years. I am preserving my original scheme certificate with me and not surrendered to my present employer. How can I take the pension scheme benefits for my total tenure of service at the age of 58 or leaving if i leave the company before the age of 58?.. Can I submit the original scheme certificate to the present employer to add my past services along with present services period?. Please advise….

Murugan-Yes, you have to submit the same to current employer.

Is there any way to check the my EPS balance online ?

Mainul-Sadly NO.

Sir, I got my PF amount from Fortis PF Trust (Delhi) on 18th May, But still I have not received my EPS amount .

But for my other colleagues, they received that EPS amount just a while after they received their PF amount..

what may be the reason for the delay..

looking forward for your replay and advice in this regard..

Sai-Either approach the employer or the EPFO.

Hi Basavaraj ,

I have a query about the staement written in the post i.e. ” Employees are eligible for EPS only if they complete 10 Yrs of service or attain the age of 58 or 50 Yrs of age”.

My question is ” Is it the condition that we have to work continously for 10 years in single organisation for getting eligible for EPS Benefit or it is transferred in the same manner like EPF.

Please reply.

Thanks,

Yatin

Yatin-It is total tenure of employment but not within single employer.

Thanks for the reply. But did not understand. Please elobrate, the confusion is that I have changed 2 companies and just want to know that the amount deducted by both the companies as EPS will be paid to me or not and how can I check my balance of EPS online.

Thanks in the advance.

Yatin-Your total tenure with both companies are considered for EPS tenure.

THANKS 🙂

Is there any way to check the balance online?

Respected Sir,

As per ur suggestion ,I want to put complaints regarding my issues. If u have any suggestions/(s), Please suggest.

Here is my compliant.

I,am a employee of above Establishment since last 16 years as a full time em employee .My employer not paying salary to all employees including me since June 2013 due to what reasons know him/them best.So, obviously PF also not deducting from June 2013 and depositing to EPFO.

I ,want to know from your side the following information.

(1) Is it mandatory on the part of Establishment to pay the contribution on regular basis and/or under which circumstances should be relaxed and up-to what extent?

(2) Is this Illegal?Please Reply in detail.

(3)What will status of our /my Account after non-payment of contribution by Establishment after continuously last 36 Months? Will it becomes inoperative?

(4) Interest on the amount up-to May 2013 will be deposited in our/my Account by EPFO or not? If yes,then up-to what?

(5)What are the powers to EPFO to give relief in such case/(s)?

Please Reply this as early as possible since compilation of 36 months are at the edge of this month,to avoid further complication from your side.

Kadam-Please go ahead.

Dear Sir,

I had switched companies multiple times and had withdrawn my PF. I haven’t done PF transfer. EPS also withdrawn. From the above set of comments I am able to see that only part of EPS would have been credited. If yes

1) Would I be able to get the remaining EPS anytime in future?

2) Is it 10 years in one company to be completed to get the complete EPS? or is it total experience

3) The PF accounts is always new with every companies since I used to withdraw them all the time.

Appreciate your clarification here. Many thanks in advance.

Janardhan-1) NO, 2) Yes 10 years of EPF contribution to that particular account. 3) It is your fault. It is not NEW for every company. You can transfer and use the same EPF account.

MY employer had not pay contribution since last 36 months due to the financial problems.Will my account cease/inoperative?will interest gets or not? please reply,Sirji.

Kadam-Raise the issue immediately with EPFO. It is illegal to stop depositing EPF.

thank you ,sirji.

Dear Mr. Basavaraj,

I had worked in a organisation for 9 yrs 2mths and wish to withdraw by PF. Will I get my complete pension amount???

Firozi-It must be 9 years and 6 months minimum.

Sir, so if I withdraw the PF now what will be the amount which I will receive?

Firozi-Check with EPFO.

Hi Basavaraj,

After transfer my PF from my previous company to current company through form 13, I can see my contributed and company contributed amount of previous company is added into my current company PF account. But can’t see any amount added in my EPS section. So, is it transfer along EPF or I have to raise concern for the same? If need to raise concern, then what should be my approach and to whom?

Please suggest..

Thanks,

Bimalendu

Bimalendu-It will transfer along with EPF.

Thanks Basavaraj for you quick reply. So, you mean to say that it already transferred along with my EPF, but the EPS amount not showing my current company EPS section, is it?

Thanks,

Bimalendu N

Bimalendu-Yes.

Thank you Basavaraj!

Sir,

I have the same Case as above guy. Why EPs is nit shown in transfer amount of EPF ?

Gaurav-I am not sure, you have to raise the issue with EPFO.

Hi I have a manufacturing unit where around 50 employees, staff and workers/machine operators are employeed.

Many of them have employment upto 10 years and some are between 5 to 10 years. Since the govt announced that the PF scheme will be converted to pension scheme, the employees want to withdraw their PF. Since many of them have already withdrawn 80% for house etc, it is difficult to do it now. They are asking for accepting their resignation and be in our employment after a break or thru contractor.

What is the real picture? Is the PF fund totally going to be converted in Pension? Can the employee not withdraw their PF now? Should we take their resignation to get their PF amount in their account?

Pl guide !

RS-I replied to your FB message.

I am a member of EPF since 1990 and in Nov 2015 I completed 58 years. Still I am working in the same company and since Nov 2015, the company is contributing only to PF and not ESP. Now What is next step I should do? Should I apply for pension now or after taking retirement? In case I should apply for pension, how to go about? – Thanks in advance

Venkateshwaran-They can’t contribute only to EPF by stopping to EPS. Check the facts.

Thank you so much Basavaraj for your reply. Its really very helpful.

So i understand 10 years in EPS does not require continuous contribution for 10 years. Its also accept break between it. Am i correct? And if i stay in my current company for more than 10 years then there is no option to withdraw. And in that case pension is the only option.

Another query. i contributed 26000 to EPS in 3.8 years . So what is the formula to calculate withdrawal amount.

Manjari-Yes, your understanding about tenure of EPS is correct. There is no formula for 4 years. If you want to withdraw, then it be payable as per Table D.

Thanks Basavaraj. find those answers which was searching from a long time.

Hi Basavaraj,

Previously i was working in Tech Mahindra and worked for 4 Years and 8 months. But within that time i was in UK onsite deputation for 1 year and me or my employer did not contributed anything to EPF and EPS. Now i joined Cognizant and already transferred EPF. But what should i do with EPS? if i transfer EPS then how this 10 years will get calculated? is it continuous 10 years required in same company or it means only 10*12=120 months of EPS contribution whatever the employer is and breaks in contribution.

Another question. What is benificial? if i took the scheme certificate of EPS and transfer it or if i withdraw it and invest as FD.

Manjari-It is your actual contributory period to EPS but not your employment with your employer. Better to withdraw and invest.

Basavaraj ji,

I had left my previous organization in Jan 2014 after 7yrs employment there. My [F ws withdrawn and settled in next 3-4 months time.

Now 2months I got a letter that the EPS settlement is in process and it has been submitted to RPFC.

It was submitted as per the acknowledgement NOVEMBER 2015.

They sked me to check on line EPFO site. but there is no records on settlement as of now though its reflecting online as a group of employees.

So my query is : How much time does it take for this settlement? Do I need to do anything?

Thanks and Regards

Rajesh

Rajesh-If you not received amount, then raise the issue with EPFO.

Basavaraj ji, So can I raise it online ,or do I have to go in person to any EPFO office?

Rajesh-Raise it online.

Recently i applied for withdraw of my PF amount on 01.05.2016.

My total PF amount is (employee share+Employer share + pension contribution) (5644+1726+3918=11288) but i received only Rs.7730/- on 27.05.2016.

please tell me when i receive my remaining balance of (Rs.3558/-).

Uday-Whether your calculation also involves full EPS balance? If so, then you will get EPS withdrawal based on Table D but not fully. If still you have concern, then you can contact EPFO.

Dear sir

please clarify my doubt regarding EPS. I have worked with a company for 8 yrs and 10 moths now i resigned from there on apr 10 th 2016 .When can i withdraw my epf amount .While cheking with UAN portal my balance is (Employee+employer+EPS contribution) is (121434+51264+55154) respectively my basic salary was

10431.please tell me the EPS amount that can be claimed…

Vinod-It is based on Table D.

My EPF account was with HCL Trust and Pension was with LOCAL PF office in Delhi. Now after switching job to new employer I got my EPF amount transferred but not EPS. For EPS HCL says that

I need to fill form 13 with my present employer

Present employer submits the form with current EPF office

Current PF office sends the form to old PF office

OLD pf office will then issue the transfer of my EPS to new EPF office….

I had earlier filled two copies of form 13 with my present employer, one for pf and other for pension transfer. But they had sent both the copies to my previous employer. So I got my PF amount transferred but not pension.

Should I again fill form 13 with present employer for transferring Pension ?

Adil-I think it is also transferred but not reflecting. Raise the issue with EPFO.

Dear sir, pls confirm one thing.. after my releiving from my organisation.i received two credits in my account in next three montha. one is pf settlement and another provident fund…pls confirm if this is pf and eps ..or eps is supposed to be creduted later. Also pls confirm form 10 c is used for Eps withdrawal?

Ranjana-I don’t think it is EPS.

Sir,

I submitted my scheme certificate to new employer. How I know the existing employer linked the scheme certificate to the existing PF account.

UAN 100262639631

Surendran-You can check with online or else directly contact EPFO.

Use your UAN number and registered password to login to UAN portal and check whether your new PF account is tagged to your UAN number or not. If it is tagged then check whether your old PF account amount is credited to the new one or not. If not credited then use the transfer claim option in UAN portal and initiate the PF transfer from old pf account to new pf account

I have linked the Old Employer once i received your message. it is linked with my present UAN. Thats why i doubted. Now what will be my service period? will it be 9 years or 1.5 years?

Waiting for your revert

Thanks for clarifying my doubts sir.

Respected Sir,

My self Dhaval, I have completed service 9 Year 5/6 Months my joining date was 1st May 2005 & resigned date 31st Oct 2013, am i eligible for Pension scheme ?

Please guide if i do not wish benefit of Pension Scheme.

As 10year not completed i am not eligible so, Hence, May i eligible for full settlement ?

Dhaval-Refer eligibility service rules mentioned above.

Bhagyalakshmi-Whether you withdrawn EPS also from your first EPF?

Then what will be my service period.

When I tried to link through UAN it is linked ans the status states it is active. why this conflicts?

Bhagyalakshmi-The old EPF account once you withdrawn and not linked to current one means how can the current EPF will reflect the old history of your job?

I have a query on EPF.

Totally i have 9 years of service.

My first organization which i had worked for 7.5 Years has a PF Trust.While releiving from there i did a PF Withdrawal and got the complete settlement then.I did not do a PF transfer that time.

My second organization for which i am working for last 1.5 years comes under EPFO.

Now i have applied for a PF withdrawal for the prepayment of home loan which needs minimum of 10 years of service.For me i have 12 years of service and have association with EPF.

But my application got rejected saying i have only 1.5 years of service.

Is it correct?

DO i need to do anything from my previous employer to link my older PF account to the new one , eventhough i have done complete settlement that time. Is it possible to link it now , so that i can take the PF withdrawal.

Expecting your answer on this.

Bhagyalakshmi-Old account is closed once you withdrawn the amount. Hence, you can’t link that.

Hi Basavaraj,

I have a PF account for which i can check balance in EPFO website.But i am not sure if I have my EPS account as well(pension account).

How to check if I have a EPS account as well,and if i have EPS account how can i check the balance in EPS account.

Also if my EPS account is still not opened how can i open it.

Thanks for the information 🙂

Rajdeep-This I answered in our FB chat.

Hi Basavaraj,

I have a query on EPF.

Totally i have 12 years of service.

My first organization which i had worked for 7.5 Years has a PF Trust.While releiving from there i did a PF Withdrawal and got the complete settlement then.I did not do a PF transfer that time.

My second organization for which i am working for last 4.5 years comes under EPFO.

Now i have applied for a PF withdrawal for the prepayment of home loan which needs minimum of 10 years of service.For me i have 12 years of service and have association with EPF.

But my application got rejected saying i have only 4.5 years of service.

Is it correct?

DO i need to do anything from my previous employer to link my older PF account to the new one , eventhough i have done complete settlement that time.

Expecting your answer on this.

Thanks,

Vijayasree

Vijayasree-Yes, they are correct. Because your first EPF account no more linked to second EPF account.

Hi Basavaraj,

Thanks for the reply.

Is it possible to link it now , so that i can take the PF withdrawal.

Regards,

Vijayasree

Vijayasree-It is of no use and they will not link.

Ok .Thanku so much for the clarifications.

Dear sir,

I worked 1n a firm less than six month. so i can withdraw my EPS.

RAvi-NO.

Hi Basvaraj,

Do you know why PF passbook does not reflect any “Interest” for the last financial year?

If I see my passbook, it had been credited in March every year but this time it has not been updated till now. There were also rumors that this year PF body will give bonus instead of interest.

Please share if you have any insight to this issue.

Thanks in advance.

Gaurav-I am not sure about this. But usually they update it by April every year.

Thanks for your complete guide.

I am contributing to EPS since June 2001 but I don’t get any proof for that from the EPFO. How will I prove my length of contribution(Service) during the time of Pension. We only get yearly PF contribution slip. What about the EPS. Please do the needful. How to solve long pending grievances with EPFO. Thanks.

Yogesh-Check once again, you will also find EPS.

I have worked in 1st organisation from June 2001 to july 2007. Then I left the 1st organisation & joined 2nd (another) organisation from July 2007 to May 2015. During my service in 2nd organisation I transferred my PF from 1st organisation to 2nd organisation in the year 2008. Then Once again I left the 2nd organisation & join 3rd (another) organisation from may 2015 and continuing till date. Now I have transferred my Total PF(PF of 1st & 2nd Organisation) from my 2nd organisation to my present(3rd) organisation. The total amount (1st & 2nd organisation) for PF is transferred but for EPS service length mentioned in annexure-K is reflecting only period of 2nd organisation i.e from july 2007 to may 2015. However for EPS I need to produce total service length continuing from ist organisation i.e from June 2001 to may 2015. Further I do not have any evidence of annexure -K of my 1 st job.

Please suggest me how to generate record for my service length continue from June 2001 to till date for the purpose of EPS.

Yogesh-The EPF contributions are enough proof of your service.

Thanks

But still the question remains how I will prove my total length of service if it is not reflected on papers available with me.

Please guide.

Do we have any online facility for it.

Yogesh-Raise the issue with EPFO.

Hi Sir,

I have got a total of 8 years and 9 months of IT experience. So far i have worked with 4 companies within 8.9 years.

When i switch from my 2nd to 3rd company, my 2nd employer didnt transfer the EPS amount to my 3rd company EPS account? However they did transferred the EPF amount.

Also, please advise do i need to transfer the EPS amount along with my EPF amount whenever i switch over to another company?

Am i eligible for the EPS?

Thanks,

Srini

Srinivasan-If EPF is transferred, then EPS was also be. Check once again with concerned EPFO.

Srinivasan- In general EPS is not transferred. When you transfer from your old account, your contribution & employer’s contribution towards PF is transferred but not the pension component. Only thing which matters is your duration of employment which is mentioned in your passbook.

As far as eligibility is concerned, you can avail pension if you have contributed to pension fund for at least 9 years & 6 months.

Dear sir

please guides

i have worked 5 year and 7 month

my basic was is Rs 8750 ( from last 11 month )

i have submitted form 10 c and i got 34076 in my account (which is same as eps shown in e passbook )

but as per table D calculation

8750*6.07 = 53211

please suggest what to do get difference amount

Jay-You will not get that difference amount.

please tell me as per table d i am eligible for Rs 53000 and i get less amount so why i can’t get

please guide

Jay-May be some calculation difference between you and EPF. Contact EPFO for the same.

Thanks

please provide the any link where i can ask same

my pf account with chennai office TN/MAS

Jay-Contact Chennai Office.

Hi, Thank you for the article. I applied for withdrawal of EPF & EPS (i had to submit the form 15G even if the withdrawal amount was more than 3 L). I received the amount in 3 weeks, however the pension part is very less.

I have worked in the organisation for 3 years and as per the article and other articles i read the EPS money i should get back is 2.98*15000 = Rs. 44700. Even if tax is deducted on this it should be ~40K. I received only 27K. Am i missing something?

Also, is there a way to know how much tax was deducted against the EPF amount that i received? In short, is there a way to know the calculation?

Sheetal-If you submitted the Form 15G, then they not deduct the tax. You received less EPS based on Table D calculation.

HI Basavaraj Tonagatti how to eps amount transfer if Company’s Operation shutdown at regional office SO cutting down their employee BEFORE SIX MONTH?

Nisav-You can transfer along with EPF.

Thanx sir for your reply but i don’t want to job at anywhere i want to do my own business so i want to withdrawn my whole pf amount.. so please suggest what i do in that situation…?

Nisav-You can withdraw.

COMPANY CLOSED THEIR REGIONAL OPERATION SO MY 6 MONTH NOT COMPLETED IN JOB SO HOW CAN I WITHDRAW MY PENSION SCHEME FUND (WITHOUT REJECTION OF 10C) WITHOUT TRANSFER….. PLEASE SUGGEST IF ANY SOLUTION….

Nisav-Try your luck with regional EPFO.

Hello,

I have query on the EPS withdrawal from my previous company.

In Apr-2013, I changed my company and didn’t transfer my PF. With previous company I was having experience of 5 year 8 month and withdrawn my PF in 2013 itself.But I didn’t withdraw the EPS. Am I eligible to withdraw the EPS from my previous company? What is the process for the same.

Waiting for your kind reply.

Thanks

Pradeep

Pradeep-You are allowed to transfer ONLY.

This Blog really helps! Thanks a lot for the very detailed explanation about EPS, Mr. Basavaraj!

Hi Basavraj,

Very detailed and enlightening article. While we all know about EPF, knowledge about EPS is very limited, even to professionals. Thanks a lot for this article.

I have a query. The pension amount calculation as given, will the same amount be given year after year, or there is a provision for increase in pension amount based on inflation or DA announced by governement,

Thanks

Sandeep Gupta

Sandeep-It will be same.

Dear Sir ,

I have withdraw the whole amount from EPF but the amount credited in bank twice and occurs a difference of 954 rs from the whole amount mentioned in the passbook (PF contribution and Pension contribution ) . I would like to know is there any surcharges for the withdrawal /any service charge .Please reply

Thanking You

Tijo Kurian

Tijo-There is no surcharge. Check the same with EPFO.

Thanks for your Prompt reply

Sir,

I have withdrawl pf and epf from my all 3 previous organisation from 1993 to 2008 period. Since 2008 i am working. My query as below ( 93 to 96, 96 to 99, 99 to 2006, 2008 to continue )

1) Is it require to add my 3 previous company to epfindia online web site. Will I get its benefit in pention.

2) How I can add/ register this three organisation in epfindia online portal

3) How can I know my previous PF number

4) Some body says that inspite withdrawl both pf and epf, some amount left in account. Pl. clarify

Patel-First understand that PF and EPF in your case is same but not different. Regarding merging and creating online accounts, if you already withdrawn the amount, then why you are looking at them again?

Hi ,

I submitted withdrawal form for PF and EPS form 10C on july 2015 at the time of leaving my Company after 9 yrs 8 months of experience.

I got my PF amount .But for EPS , i checked the eps site and it shows msg that claim ID has been approved for payment through cheque and is under process for the past three months. Pls confirm when i will be receiving the funds. Also pls advice will i get full amount or pension per month. Pls confirm how can i escalate the matter.

Any help in this will be appreciated.

Ranjanna-You have to check with EPFO for delay. You will get the amount based on Table D.

Thanks for prompt reply. Pls confirm the epfo contact details or email id.

Ranjana-They are available at EPFO portal.

Dear sir, pls confirm one thing.. after my releiving from my organisation.i received two credits in my account in next three montha. one is pf settlement and another provident fund…pls confirm if this is pf and eps ..or eps is supposed to be creduted later. Also pls confirm form 10 c is used for Eps withdrawal?

Ranjana-I don’t think it is EPS.

ThNks sir. Form 10c is used for eps withdrawal.pls confirm

Ranjana-Refer this post for the same “EPF (Employees’ Provident Fund) Forms-Simplified“.

Hi ,

I submitted withdrawal form for PF and EPS in Aug 2015 at the time of leaving my Company after 4 years of experience.

I got my PF amount .But for EPS , one month back i got two messages from EPFO office stating that Claim Form 13 has been processed .Second message stating that claim ID has been approved for payment through cheque and is under process.Today after sending a mail for the status , they replied that EPS a/c was already transferred to new account , your claim form 10C has been rejected.

What does that mean ??? EPS amount has been transferred to my new PF account No ?? And if yes , how can i verify the same as well as how can i check the balance in my PF account .

Any help in this will be appreciated.

Thanks

Neha

Neha-If you not applied for transfer, then how can the transfer happened? Please clarify this issue.

Thanks for your reply.

Will check with the PF Team

I have completed 10y of service, am over 50y old but below 58y, unemployed since 3 years. I want to claim my pension. I am single and live with my mother. My father is no more. My brother is my nominee. Do I need to submit any documents about my parents and brother along with form 10d?

Amarnath-Not required.

I was earlier serving with a Company who had granted exemption from EPF and had their own PF. Now the Company has credited all my contribution with interest to EPFO in recent time. So question of transferring my PF from the Company to another Company was not possible due to the circumstance of closure of the Company. After that I had started new job with another Company where EPF scheme was there and I had started the EPF with new PF No.

My querry is as below:

I have withdrawn my PF through Form No.19. But at the time of subm,itting the Form No.19, my HR was not aware to submit form 10C for EPS withdrawal with form No.19. Now I got my PF withdrawal. Now I have submitted the EPS withdrawal Form No.10C after getting the PF contribution. I have got message from the EPFO that your Form No.10C is received and sent for process. But after that message, 7 days is passed but still 7 days is passed for this message,no message of regarding my claim is received from EPFO not any amount is credited to my Bank A/c.

Now I want to know that whether I will get the EPS or not. I have completed only 2 years and 6 months service with PF contribution and attained 58 years of age on 18-3-2016.

Gunvant-Yes, but not fully.

Hi Basavaraj,

My mother had provident fund, she passed away in service period but she completed 20 years service, her organization has its own trust to maintain epf. l got her provident fund and eldi but not received any part of eps. I am 30 year old, l know it is only upto 25 years to get pension. but I hear about capital return on eps, what is that.?? Can I eligible to get my mother’s pension fund.??? Please clarify me..

Regards.

Jomon-Yes, check with her employer or concerned EPFO.

I am member of PF Pension Scheme I Complete of 10 year of my job . my age is 54 year. I have no job at a time. I want to pension.

then what I do for get pension. please guide me

Sudhir-Please refer above post completely.

I have worked in my previous organization between 10-Oct-2011 to 26-Jun-2015 (3 years 8 months) and after moved to different Company from 29-Jun-2015

Actually I have transferred my PF, including of all mentioned above , except EPS .

My previous organization has own trust , but they advised EPS will be maintaining from RPFO Bangalore.

So please advise, is it possible to transfer of EPS amount , or how to claim that later.

Renganathan-I think your EPS also transferred. Check it perfectly.

hello Basavaraj Tonagatti,

I claimed for my PF amount. I got NEFT transfer for Pension contribution.and more then 10 days passed away after that still my PF amout is not tranferred.

Can you please suggest what to do now.

Thanks in advance

Raj Patel (Ahmedabad)

Raj-Raise the issue with EPFO Grievance Cell.

Sir,

I resigned from my last company after 18 years of service on 24.08.2015. My total experience is 30 years. I completed 50 years on 19.05.2015. I have a few queries:

1. How do I know my accumulated pension amount? Which website or portal will give me this information? My PF number is TN/AMB/039991/000053.

2. I have got my PF, gratuity & superannuation amount, but my last employer says that I will get only a pension certificate and not pension till I become 58. But as per your post, I fulfill the criteria (50 years age & 30 years service). What should I do to get my pension?

3. If I get pension now, will it be taxed? What is your advice to me regarding premature withdrawal? Should I wait too 58?

Thanks in advance

Regards

Sriram R

Sriram-1) It will be reflecting in your passbook. If not, then contact EPFO.

2) Approach the EPFO directly with the pension certificate.

3) Yes.

Dear sir i didn’t getting my original pension epfo still deducting my computed pension after completion the time they told there is no rule to correct the computed pension in 1995

So please explain me about this

Bhanwaru-I am not getting your doubt.

I WANT TO KNOW CAN I WITHDRAW MY EPF AFTER 8 YEARS WITHOUT CONTINUATION

Sivakumar-If you are unemployed, then definitely yes.

Dear Mr Basavaraj Tonagatti,

Can you kindly explain the current status under the Employees Pension Scheme 1995 relating to the following 2 options:

1.Option for Commutation of Pension

2. Option for Return of Capital

Thanks and Regards,

Sumant Sharma

Sumant-Both the options already explained above. There is no change to it.

Hi Basavaraj,

I’ve have been working in a private company since September 10, 2004. In a month or 2 I’m planning to quit this job and take a break….and assuming that I will not be working in a corporate setup anymore. My query is that now that I have crossed the 10 year bracket, can I withdraw my pension amount along with my provident fund or will I need to wait till 58 years to withdraw my pension scheme. Kindly provide your advice on the same at the earliest.

Thanks!

Vibha

Vibha-You can withdraw EPF but EPS will provide pension.

Hi Basavaraj,

I have completed 11 years in pf account, and I am not going to work any more.

My question is can I get both EPF and EPS, please advise.

Thanks

Tom

Thomas-YES.

Thank you very Much

This question to Mr.Basavaraj,

Sir, I worked in a company for 10 yrs and received pension scheme certificate in 2006,i will attain 58 in 2024 and the pension starts from there. Pensionable salary is ?6500.My doubt is now I am working in another company last 6 years where the PF A/c become different ,shall I attach it to my previous scheme certificate A/c to get revised pensionable salary scheme certificate? so that the amount will increase?my current salary is ?1 lac per month

Thiruppathy-Yes, you can do it. Try to transfer earlier EPF account to new one.

I am 37 and served in a Pvt company for 12 years. I plan to quit and start something on my own. In this case is it wise to withdraw the EPS or wait till i turn 58 and then utilise the Pension scheme.

Naveen-Better to withdraw.

Thank You Basavaraj

Hi, My Employer is contributing INR 15000/- towards EPS. So, if I work for say 36 years will my monthly pension be 15000 x 36 / 70 or will it be limited by minimum pensionable salary (INR 6500) and calculation will be made like 6500 x 36 / 70 even when I am contributing higher. This is what I found on all the online calculators available. Kindly confirm.

Gaurav-In the above post, I already explained the above scenario.

Hi Basvaraj,

You have explained it as…..

***************************************************

2) Employees who joined after 15th November 1995–

You can directly calculate by inserting the values in the formula as given below.

(Average Salary X Service)/70

***************************************************

So my pension after 35 years of service shall be 15000 X 35/70= 7500/- pm

but when I use a calculator from the link you have provided it limits the monthly salary to 6500

and calculates as 6500 X 35/70 even when I contributed 15000 every year.

So I am still in a fix… which formula shall I use!!!

Gaurav-The revised minimum salary limit is now Rs.15,000 but not Rs.6,500.

Thanks Basvaraj 🙂

I have recently changed my job. My previous company had its own provident fund and was registered with the regional provident fund commissioner. Both the employer and employee contribution was deducted and taken towards provident fund account. No amount was apportioned towards pension scheme. My tenure in the previous company was 4 years 3 months.

Post the job change, my new employer has the following scheme with respect to provident fund.

There is an option provided by the employer whereby the employee is free to choose either 15,000 or actual basic salary (higher than 15,000) for the calculation for provident fund. With respect to the employer contribution of 12% of basic salary, 8.33% shall be taken towards pension and the balance 3.67% shall be taken towards provident fund. My tenure in the new job is around 3 months. The Company would deposit the money with the government towards provident fund.

The following are my queries w.r.t provident fund:

1. I want to transfer the previous company’s accumulated PF balance to the new company. On completion of 5 years of service (tenure considering both the previous as well as the current employer), I wish to withdraw the money. Are there any conditions towards withdrawal and what are the tax implications of withdrawal.

2. I want to invest a higher amount in provident fund and not restrict the basic salary to INR 15,000 per month as provided by the statute. If I go for a higher deduction, is it compulsory that the employer should contribute 8.33% of the basic salary towards pension scheme. Can I not transfer the entire amount to provident fund?

3. How can one withdraw the amount lying in the pension scheme. I also understand that I have to complete 10 years in service. Though the previous company did not have any pension scheme, will the tenure there be considered for the 10 years consideration.

Thanks for the help.

Ankit-1) You can withdraw for a special purpose. Refer my earlier post “All about EPF (Employee Provident Fund) advance withdrawal“.

Thanks for the response. What about the response to question 2 and 3.

IF employee has completed more than 10 years in service and then retires ,is withdrwal of amount allowed using form 10c.

Mukta-No, only eligible for pension.

Isnt it unjust? As there is no interest on EPS I end up getting peanuts as pension.

If I am allowed to withdraw I can invest it for better returns.

How come no one has raised any objection? Are those worker-unions sleeping?

Mukta-Do you feel worker unions free of politics?

when this rule came into effect? I am sure left parties were part of govt. at that time.Still if enough awareness is created there is scope for petition in court

Mukta-this rule exists since long. There is scope, but the question is who will?

PLEASE GUIDE ME FOR MY BELOW METTER.

I WAS WORKING WITH PRIVATE FIRM IN RAJKOT.

MY JOINING DATE IN THIS FIRM IS 01.05.2006

AND LEAVE THE JOB 22.02.2016.

PERIOD: 9 YEAR 9 MONTH 21 DAYS

I AM ALREADY ENTER PENSION SCHEME???

CAN I FILL PF 19 FORM AND 10 – C FORM WITH ACCEPTANCE FOR PARA RULE 8 A) FOR ACCEPT SCHEME CERTIFICATE?

CAN BETTER ME FOR ACCEPT SCHEME CERTIFICATE FOR 8. A)

PLEASE ADVICE ME FOR FILL THE PF FORM BEFORE 30 APRIL 2016 .

PLEASE REPLY FASTLY FOR ME ,AND ALSO BENEFIT FOR SCHEME CERTIFIACTE?

Manish-Yes, you are eligible for pension.

Thank you very much Sir

Now please advice me, after 58 year I will receive my all pension amount with interest in my bank account

Please advice

Manish-Yes.

Hi sir, I worked with a company for 4 years. While termination my basic was 13112. EPF is around 120000. Pls advice what shud be my EPS that I can withdraw along with my EPF. Thanks.

N-Check with EPFO portal online or contact EPFO directly. How can I say this?

it is vey informative , thank you basavaraj to educate public in epf and eps related matters

Information in the site is very useful. I have some query kindly help.

I left job as a teacher and EPS on 31/03/16. My EPFRO is in Mumbai. I have 13 yrs of service and my age is 53. I am applying for reduced pension. It will be with effect from what date.?

I wanted to draw pension from other states EPFO. Hw can I do it.

Kindly guide me.

Vasudevan-Effective date will be from when you apply. Regarding the getting of pension from other states, I am not sure it is possible. Check with EPFO.

Dear Sir,

I was joined a private firm on 13/12/1990 in Delhi after than i have left the firm on 14/08/2001. please advice me can i get pension scheme benefit. But during the service period i was on leave almost 06 Month in service time in same time my PF contribution not deposit in PF department during leave period.

please advice me how can i get pension scheme benefit ?

Anil-Yes, you are eligible.

if i have another pension scheme, will i be eligible for eps pension

SRP-Another pension scheme means?

Hi,

I have just changed my employer and want to transfer the EPF from previous to current employer, but want to withdraw the EPS amount. One of my friend has done the same thing by sending Form 10 C (EPS withdrawal) and Form 13 (EPF transfer) to the previous employer.

Please confirm about the same.

Manpreet-There is no such system to track. So your friend might withdrawn. But to be frank it is not allowed legally.

I have worked for 3.5 years in 1st organization and withdrawn PF +EPS.

and worked for second organization for 4 years and now with 3rd one for last 2 yrs

Both 2nd,3rd organization have their own pf trusts. I have raised PF transfer. and the PF gets transferred from 2nd to 3rd,I don’t know whether EPS gets transferred or not.

1. In my current company website, contribution to PF is showing as 6 yrs. ,can I be confident that my EPS transferred.

2.Can we withdraw EPS amount while continuing in present job? i am not interested in pension scheme.

3. now in corporate world ,salaries are more. contributing 15000 per annum from 1st year onwards till service ends. on 8 % interest also it would end up large amount by we reach 58 yrs.

if we start career at 25 ,continue till 58 .We contribute for 33 yrs . EPS accumulated amount is around 23 lac( at 8% interest )

but we may just receive (15000*33)/70=7071 per month . 84857 per year.

but for 23 lac ,at 8% interest we can get 1,84,000 per annum.

the EPS scheme might be helpful who contributes less in beginning and reached 15,000 by end of service.

Why EPS is not linked to the amount contributed? it’s just linked service period and last year salary.

Subba-1) YES. 2) No, you can’t. 3) It is the rule.

Dear Sir,

please guide me for below matter .i was working in private firm .I AM JOINING OFR THIS FIRM 01/03/2007 AND LEAVE THE JOB 01/08/2015. CAN I FILL PF 19 FORM AND 10 – C FORM WITH ACCEPTANCE FOR PARA RULE 8 A) FOR ACCEPT SCHEME CERTIFICATE ?

CAN BETTER ME FOR ACCEPT SCHEME CERTIFICATE FOR 8. A)

PLEASE ADVICE ME FOR FILL THE PF FORM BEFORE 21 APRIL 2016 .

PLEASE REPLY FASTLY FOR ME ,AND ALSO BENEFIT FOR SCHEME CERTIFIACTE ?

Jitendra-Scheme certificate will come into picture when you completed minimum 10 years of service. In your case it is not.

Hi Basavaraj,