Sovereign Gold Bond Scheme 2021 Series I is available for subscription from 17th May 2021 to 21st May 2021. Should you invest in these bonds? Who can consider investing in such bonds?

Note:-Before reading further, first understand whether your investment in Gold is for your own usage or as an investment. If for investment, then read my post before proceeding to this post “Gold Price of Rs.18.75 in 1925 to Rs.47000 in 2020 – Should you invest?“.

This is the first series of FY 2021-22. You can refer my earlier post to understand the complete calendar for this FY at “Sovereign Gold Bond Scheme 2021-22 – Calendar“.

This Gold Bonds scheme was launched in November 2015. The government launched this scheme to reduce the demand for physical gold. Indians buy around 300 tons of gold every year. This is to be imported from outside countries. Let us see the silent features of this scheme.

The Bonds shall be issued in the form of Government of India Stock in accordance with section 3 of the Government Securities Act, 2006. The investors will be issued a Holding Certificate (Form C). The Bonds shall be eligible for conversion into de-mat form.

Features of Sovereign Gold Bond Scheme 2021 Series I

Let us understand the features of Sovereign Gold Bond Scheme 2021 Series I in detail at first. Let me explain the same using the below image.

# Dates to subscribe

Sovereign Gold Bond Scheme 2021 Series I will be open for subscription from 17th May 2021 to 21st May 2021. The Bonds will be issued on 25th May 2021.

# Who can invest?

Resident Indian entities including individuals (in his capacity as such individual, or on behalf of a minor child, or jointly with any other individual.), HUFs, Trusts, Universities, and Charitable Institutions can invest in such bonds.

Hence, NRIs are not allowed to participate in the Sovereign Gold Bond Scheme 2021 Series I.

# Tenure of the Bond

The tenor of the Bond will be for a period of 8 years with exit option from 5th year to be exercised on the interest payment dates.

Hence, after the 5 years onward you can redeem it on 6th, 7th or at maturity of 8th year. Before that, you can’t redeem.

RBI/depository shall inform the investor of the date of maturity of the Bond one month before its maturity.

# Minimum and Maximum investment

You have to purchase a minimum of 1 gram of gold. The maximum amount subscribed by an entity will not be more than 4 kgs per person per fiscal year (April-March) for individuals and HUF and 20 kg for trusts and similar entities notified by the government from time to time per fiscal year (April – March).

In the case of joint holding, the investment limit of 4 kgs will be applied to the first applicant only. The annual ceiling will include bonds subscribed under different tranches during initial issuance by the Government and those purchased from the secondary market.

The ceiling on investment will not include the holdings as collateral by banks and other Financial Institutions.

#Interest Rate

You will receive a fixed interest rate of 2.50% per annum payable semi-annually on the nominal value. Such interest rate is on the value of money you invested initially but not on the bond value as on date of interest payout.

Interest will be credited directly to your account which you shared while investing.

# Issue Price

The nominal value of the Bonds shall be fixed in Indian Rupees fixed on the basis of a simple average of the closing price of gold of 999 purity published by the India Bullion and Jewellers Association Limited for the last 3 working days of the week preceding the subscription period. The issue price of the Gold Bonds will be Rs 50 per gram less than the nominal value to those investors applying online and the payment against the application is made through digital mode. The issue price of Sovereign Gold Bond Scheme 2021 Series I is at Rs.4,777 per gram.

# Payment Option

Payment shall be accepted in Indian Rupees through cash up to a maximum of Rs.20,000/- or Demand Drafts or Cheque or Electronic banking. Where payment is made through cheque or demand draft, the same shall be drawn in favor of receiving an office.

# Issuance Form

The Gold bonds will be issued as Government of India Stock under GS Act, 2006. The investors will be issued a Holding Certificate for the same. The Bonds are eligible for conversion into Demat form.

# Where to buy Sovereign Gold Bond Scheme 2021 Series I?

Bonds will be sold through banks, Stock Holding Corporation of India Limited (SHCIL), designated Post Offices (as may be notified) and recognized stock exchanges viz., National Stock Exchange of India Limited and Bombay Stock Exchange, either directly or through agents.

Click HERE to find out the list of banks to buy Sovereign Gold Bond Scheme 2021 Series I and List of Post Offices to buy Sovereign Gold Bond Scheme 2021 Series I.

# Loan against Bonds

The Bonds may be used as collateral for loans. The Loan to Value ratio will be as applicable to ordinary gold loan mandated by the RBI from time to time. The lien on the Bonds shall be marked in the depository by the authorized banks. The loan against SGBs would be subject to the decision of the lending bank/institution, and cannot be inferred as a matter of right by the SGB holder.

# Liquidity of the Bond

As I pointed above, after 5th year onwards you can redeem the bond on 6th or 7th year. However, the bond is available to sell in the secondary market (stock exchange) on a date as notified by the RBI.

Hence, you have two options. Either you can redeem it at 6th or 7th year or sell it secondary market after the notification of RBI.

Do remember that the redemption price will be in Indian Rupees based on the previous week’s (Monday-Friday) simple average of the closing price of gold of 999 purity published by IBJA.

# Nomination

You can nominate or change the nominee at any point of time by using Form D and Form E. An individual Non – resident Indian may get the security transferred in his name on account of his being a nominee of a deceased investor provided that:

- the Non-Resident investor shall need to hold the security till early redemption or till maturity; and

- the interest and maturity proceeds of the investment shall not be repatriable.

# Transferability

The Bonds shall be transferable by execution of an Instrument of transfer as in Form ‘F’, in accordance with the provisions of the Government Securities Act, 2006 (38 of 2006) and the Government Securities Regulations, 2007, published in part 6, Section 4 of the Gazette of India dated December 1, 2007.

How to redeem Sovereign Gold Bond Scheme 2021 Series I?

As I explained above, you have an option to redeem only on 6th, 7th and 8th year (automatic and end of bond tenure). Hence, there are two methods one can redeem Sovereign Gold Bonds. Explaining both as below.

# At the maturity of the 8th year-The investor will be informed one month before maturity regarding the ensuing maturity of the bond. On the completion of the 8th year, both interest and redemption proceeds will be credited to the bank account provided by the customer at the time of buying the bond.

In case there are changes in any details, such as account number, email ids, then the investor must intimate the bank/SHCIL/PO promptly.

# Redemption before maturity-If you planned to redeem before maturity i.e 8th year, then you can exercise this option on 6th or 7th year.

You have to approach the concerned bank/SHCIL offices/Post Office/agent 30 days before the coupon payment date. Request for premature redemption can only be entertained if the investor approaches the concerned bank/post office at least one day before the coupon payment date. The proceeds will be credited to the customer’s bank account provided at the time of applying for the bond.

Sovereign Gold Bond Scheme 2021 Series I Taxation

There are three aspects of taxation. Let us see one by one.

1) Interest Income-The semi-annual interest income will be taxable income for you. Hence, For someone in the 10%, 20%, or 30% tax bracket, the post-tax return comes to 2.25%, 2% and 1.75% respectively. This income you have to show under the head of “Income from Other Sources” and have to pay the tax accordingly (exactly like your Bank FDs).

2) Redemption of Bond-As I said above, after the 5th year onward you are eligible to redeem it on 6th,7th and 8th year (last year). Let us assume at the time of investment, the bond price is Rs.2,500 and at the time of redemption, the bond price is Rs.3,000. Then you will end up with a profit of Rs.500. Such capital gain arising due to redemption by an individual is exempted from tax.

3) Selling in the secondary market of Stock Exchange-There is one more taxation that may arise. Let us assume you buy today the Sovereign Gold Bond Scheme 2021 Series I and selling it in the stock exchange after a year or so. In such a situation, any profit or loss from such a transaction will be considered as a capital gain.

Hence, if these bonds are sold in the secondary market before maturity, then there are two possibilities.

# Before 3 years-If you sell the bonds within three years and if there is any capital gain, such capital gain will be taxed as per your tax slab.

# After 3 years-If you sell the bonds after 3 years but before maturity, then such capital gain will be taxed at 20% with indexation.

There is no concept of TDS. Hence, it is the responsibility of investors to pay the tax as per the rules mentioned above.

Whom to approach for service related issues?

The issuing banks/SHCIL offices/Post Offices/agents through which these securities have been purchased will provide other customer services such as change of address, early redemption, nomination, grievance redressal, transfer applications etc.

Along with this, a dedicated e-mail has been created by the Reserve Bank of India to receive queries from members of public on Sovereign Gold Bonds. Investors can mail their queries to this email id. Below is the e-mail id

RBI Email Id in case of Sovereign Gold Bonds-[email protected]

Sovereign Gold Bond Scheme 2021 Series I – Should you invest?

Before proceeding further just check it the current market price of past issues.

You noticed that only two issues are trading below the current series offer price. Hence, I think if you really wish to buy, then buying this series is the best option than buying from secondary market.

Advantages of Sovereign Gold Bond Scheme 2021 Series I

# After the GST entry, this Sovereign Gold Bond may be advantageous over physical Gold coins or bars. This product will not come under GST taxation. However, in the case of Gold coins and bars, earlier the VAT was at 1% to 1.2%, which is now raised to 3%.

# If your main purpose is to invest in gold, then apart from physical form, investing in ETF or in Gold Funds, this seems to be a better option. Because you no need to worry about physical safekeeping, no fund charges (like ETF or Gold Funds) and the Demat account is not mandatory.

# In this Sovereign Gold Bond Issue FY 2021-22, the additional benefit apart from the typical physical or paper gold investment is that the annual interest payment on the money you invested.

Hence, there are two types of income possibilities. One is interest income from the investment and second is price appreciation (if we are positive on gold). Hence, along with price appreciation, you will receive interest income also.

But do remember that such interest income is taxable. Also, to avoid tax, you have to redeem it only on 6th, 7th or 8th year. If you sell in the secondary market, then such gain or loss will be taxed as per capital tax gain rules.

# There is no TDS from the gain. Hence, you no need to worry about TDS part like Bank FDs.

# A sovereign guarantee of the Government of India will feel you SAFE.

Disadvantages of Sovereign Gold Bond Scheme 2021 Series I

# If you are planning to invest for your physical usage after 8 years, then simply stay away from this. Because Gold is an asset, which gives you volatility like the stock market but the returns of your debt products like Bank FDs or PPF.

# The key point to understand is also that the interest income of 2.5% is on the initial bond purchase amount but not the yearly bond value. Hence, let us say you invested Rs.2,500, then they pay interest of 2.5% on Rs.2,500 only even though the price of gold moved up and the value of such investment is Rs.3,000.

# Liquidity is the biggest concern. Your money will be locked for 5 years. Also, redemption is available only once a year after 5th year.

In case you want to liquidate in a secondary market, then it is hard to find the right price and capital gain tax may ruin your investment.

# Sovereign guarantee of the Government of India may feel you secure. But the redemption amount is purely based on the price movement of the gold. Hence, if there is a fall in gold price, then you will get that discounted price only. The only guarantee here is 2.5% return on your invested amount and NO DEFAULT RISK.

Conclusion:- Invest in Sovereign Gold Bond Scheme 2021 Series I if your main purpose is to accumulate physical gold after 8 years or so. However, if your purpose is to have an exposure to gold in your investment portfolio, then better to stay away. As they are illiquid in nature, it is hard for you to sell while doing the rebalancing activity. Instead, go for highly tradable Gold ETF or Gold Funds are better options.

REMEMBER, GOLD IS AN ASSET CLASS WHICH MAY GIVE YOU RETURNS OF DEBT PRODUCT BUT VOLATILITY LIKE EQUITY MARKET-Hence, do you need this asset as an investment in your portfolio?

Latest Posts:-

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

- 5 Important Investing Truths Most Investors Ignore

- Retirement Is Personal — Stop Comparing Net Worth and Move On

- EGR: The Gold Investment 99% of Indians Have Never Heard Of

- New Income Tax Act 2025: What Changed for You from April 2026?

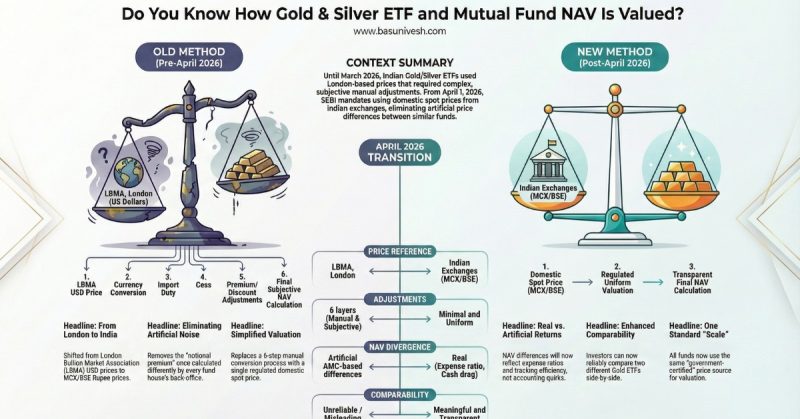

- Do You Know How Gold & Silver ETF and Mutual Fund NAV Is Valued?

See your conclusion in the above article:

…….Conclusion:- Invest in Sovereign Gold Bond Scheme 2021 Series I if your main purpose is to accumulate physical gold after 8 years or so……..

Your point is not clear.

SGB’s at the time of redemption is paid out only by cash; so where is the question of accumulating gold after 8 years?

If you mean buying gold using redemption money, then one can accumulate noble metals at any time and not necessarily at the time of SGB maturity.

Please clarify your point.

Thanks

Dear Swamy,

Yes, SGB will pay you in cash. Here, my point is that if you need it after 8 years, then accumulate it through SGB not with physical gold itself. Because safekeeping gold for 8 years is always a headache.

Hello Basuji,

I have 2 Question-

Q1 – If I subscribe to SGB online & Hold the same in Certificate Form (Non-Demat), how can I trade same ?

Q2 – Can one get his/her Physical Bond listed in his/her Demat Account after purchase ?

Dear Vaibhav,

1) To sell, you must have a Demat account as trading will take place in the secondary market.

2) Yes.