In this post, I am sharing the RBI Repo Rate History from 2000 to 2026 (the latest change of 8th April 2026). Whenever you are watching business news channels, you might have come across the word called as Repo Rate or Reverse Repo Rate.

Latest RBI Repo Rate Updates – On 8th April 2026, RBI left the repo rate unchanged. Hence, the current repo rate is 5.25%.

Let us first try to understand what the Repo Rate.

As you may be aware RBI is a regulator of the Indian banking system. The two most important functions of RBI are – to control the supply of money in the economy and to control the cost of credit (lending rate).

RBI always monitors these two functions as they directly impact the inflation and growth of the nation. Repo and Reverse Repo rates are the two tools that RBI uses to curtail inflation and thereby support the economic growth of the country.

What is the Repo Rate?

When we need the money then usually we approach the bank. Banks usually lend us by charging certain interest. This is called the cost of lending.

Same way when banks need money, they approach RBI. The rate at which they borrow money from RBI is called as Repo Rate. For such borrowing, banks have to pledge certain government securities. For example, if the repo rate is 5%, and the bank takes a loan of Rs.1,000 from RBI, then the bank will pay interest of Rs.50 to RBI.

The long form of the repo rate is “Repurchase Rate”. Usually, these loans are for overnight (1 day).

A higher repo rate means a higher cost of borrowing for the short-term needs of the banks. Based on this, banks usually charge the rate of interest for us.

If banks are unable to repay, then the RBI can sell these pledged Government Securities in the open market and recover the amount.

What is the Reverse Repo Rate?

When you have the money you usually deposit it with the bank. In return, the bank will give you some interest on such FDs, right? In the same way, whenever banks have surplus money, they deposit the extra money with the RBI for which they earn interest at a rate known as the Reverse Repo Rate. For this deposit, the RBI provides collateral in the form of Government Securities.

A long form of Reverse Repo Rate is “Reverse Repurchase Option”. This is also of a one-day tenure.

We can explain the same using the image below for your better understanding.

Why will RBI change Repo and Reverse Repo Rates?

Whenever the RBI increases the repo rate, banks have to pay more interest to borrow the money. In return, banks will charge a higher interest rate to their customers. As borrowing costs for us increased means we hesitate to take the loan. Because of this, people spend less.

As there is less demand for goods and services, the price of the goods and services will fall. Thereby inflation rate will decrease.

So in simple terms, to control inflation, RBI will increase the repo and reverse repo rates.

However, if inflation is low, then it means that there is less demand for goods and services. To promote spending and increase demand, RBI will decrease the repo and reverse repo rates. As interest rates decrease for the banks, banks will start to offer us loans at a lower rate. Thereby people start borrowing the money and start to spend.

Hence, as and when there is a need to decrease or increase inflation, RBI will change the repo or reverse repo rates.

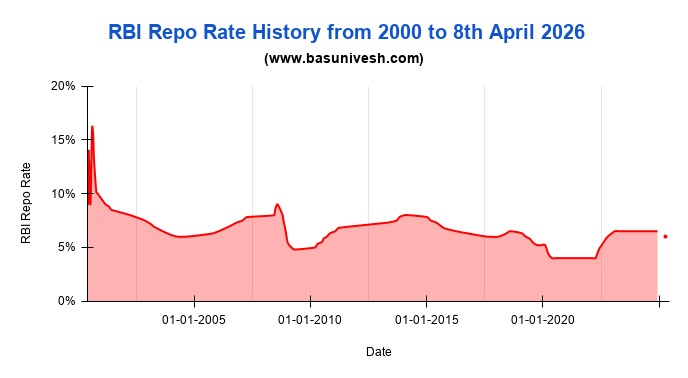

RBI Repo Rate History from 2000 to 2026

Let me now share the RBI Repo Rate history from the year 2000 to 2026. The below chart is prepared based on the data available from 5th June 2000 to 8th April 2026

If you notice the above chart, you will find that history was more horrific with a higher repo rate than what it is today. The respective numbers are as below.

RBI Repo Rate History from 2000 to 8th April 2026

| Date | RBI Repo Rate |

| 08-04-2026 | 5.25% |

| 06-02-2026 | 5.25% |

| 05-12-2025 | 5.25% |

| 01–10-2025 | 5.5% |

| 06-06-2025 | 5.5% |

| 09-04-2025 | 6% |

| 07-02-2025 | 6.25% |

| 06-12-2024 | 6.50% |

| 08-10-2024 | 6.50% |

| 08-08-2024 | 6.50% |

| 07-06-2024 | 6.50% |

| 06-04-2024 | 6.50% |

| 08-02-2024 | 6.50% |

| 08-12-2023 | 6.50% |

| 06-10-2023 | 6.50% |

| 10-08-2023 | 6.50% |

| 08-06-2023 | 6.50% |

| 06-04-2023 | 6.50% |

| 08-02-2023 | 6.50% |

| 07-12-2022 | 6.25% |

| 30-09-2022 | 5.90% |

| 05-08-2022 | 5.40% |

| 08-06-2022 | 4.90% |

| 04-05-2022 | 4.40% |

| 08-04-2022 | 4.00% |

| 10-02-2022 | 4.00% |

| 08-12-2021 | 4.00% |

| 09-10-2021 | 4.00% |

| 06-08-2021 | 4.00% |

| 04-06-2021 | 4.00% |

| 07-04-2021 | 4.00% |

| 05-02-2021 | 4.00% |

| 04-12-2020 | 4.00% |

| 09-10-2020 | 4.00% |

| 06-08-2020 | 4.00% |

| 22-05-2020 | 4.00% |

| 27-03-2020 | 4.40% |

| 06-02-2020 | 5.20% |

| 05-12-2019 | 5.20% |

| 04-10-2019 | 5.20% |

| 07-08-2019 | 5.40% |

| 06-06-2019 | 5.80% |

| 04-04-2019 | 6.00% |

| 07-02-2019 | 6.30% |

| 01-08-2018 | 6.50% |

| 06-06-2018 | 6.30% |

| 07-02-2018 | 6.00% |

| 02-08-2017 | 6.00% |

| 04-10-2016 | 6.30% |

| 05-04-2016 | 6.50% |

| 29-09-2015 | 6.80% |

| 02-06-2015 | 7.30% |

| 04-03-2015 | 7.50% |

| 15-01-2015 | 7.80% |

| 28-01-2014 | 8.00% |

| 29-10-2013 | 7.80% |

| 20-09-2013 | 7.50% |

| 03-05-2013 | 7.30% |

| 17-03-2011 | 6.80% |

| 25-01-2011 | 6.50% |

| 02-11-2010 | 6.30% |

| 16-09-2010 | 6.00% |

| 27-07-2010 | 5.80% |

| 02-07-2010 | 5.50% |

| 20-04-2010 | 5.30% |

| 19-03-2010 | 5.00% |

| 21-04-2009 | 4.80% |

| 05-03-2009 | 5.00% |

| 05-01-2009 | 5.50% |

| 08-12-2008 | 6.50% |

| 03-11-2008 | 7.50% |

| 20-10-2008 | 8.00% |

| 30-07-2008 | 9.00% |

| 25-06-2008 | 8.50% |

| 12-06-2008 | 8.00% |

| 30-03-2007 | 7.80% |

| 31-01-2007 | 7.50% |

| 30-10-2006 | 7.30% |

| 25-07-2006 | 7.00% |

| 24-01-2006 | 6.50% |

| 24-01-2006 | 6.50% |

| 26-10-2005 | 6.30% |

| 26-10-2005 | 6.30% |

| 31-03-2004 | 6.00% |

| 19-03-2003 | 7.00% |

| 07-03-2003 | 7.10% |

| 12-11-2002 | 7.50% |

| 28-03-2002 | 8.00% |

| 07-06-2001 | 8.50% |

| 30-04-2001 | 8.80% |

| 09-03-2001 | 9.00% |

| 06-11-2000 | 10.00% |

| 13-10-2000 | 10.30% |

| 06-09-2000 | 13.50% |

| 30-08-2000 | 15.00% |

| 09-08-2000 | 16.00% |

| 21-07-2000 | 10.00% |

| 13-07-2000 | 9.00% |

| 28-06-2000 | 12.30% |

| 27-06-2000 | 12.60% |

| 23-06-2000 | 13.10% |

| 22-06-2000 | 13.00% |

| 21-06-2000 | 13.50% |

| 20-06-2000 | 14.00% |

| 19-06-2000 | 13.50% |

| 14-06-2000 | 10.90% |

| 13-06-2000 | 9.60% |

| 12-06-2000 | 9.30% |

| 09-06-2000 | 9.10% |

| 07-06-2000 | 9.00% |

| 05-06-2000 | 9.10% |

Dear Niveshji

Very nice data collection and good explanation

Currently Iam doing research in which I need the data of Repo, Reverse Repo, Cash Reserve Ratio, Statutory Liquidity ratio from 2014 to 2024

Can you please provide the data or source of data for the required data so that I can complete my research work

Dear Naresh,

Thanks for your kind words. You will get it from RBI itself.

Which website you used to get this data?

Dear Anand,

It is available freely online.

Dear Sir,

We have taken a Loan from LICHFL in December-2022 and the ROI is Charged for us is 8.7%pa, from May 2023 onwards they are changed the ROI and charging 9.3% pa…as the RBI changed the Repo rate.25% but the LICHFL increased the ROI up to .60%..Generally up to what % that the Banks / Financial Institution may increase the ROI. Regarding this we are not received any communication from LIC HFL and we noticed the same in DEC-2023.

If the Banks / Financial Institutions increased the ROI is it not the responsible to intimate the same to their customers regarding the change of ROI.

In this concretion can we give any complaint / escalate the same to RBI.

Dear Ramesh,

Sadly banks have no such mandatory disclosure each time they increase the interest rate.

Ramesh, First of all check if LICHFL has given you a loan on repo rate linked rate. As far as I know NBFCs mostly follow their own rates or link to MCLR. In case of banks, the rate given to customer is repo rate + spread (bank margin) where the bank margin usually remains constant. You can negotiate with LICHFL for reducing the rate as well. In my case, the loan was sanctioned in 2021 at repo+2.9%. When the repo increased the ROI increased with no change in spread. i negotiated with the bank and they readily reduced it by 0.7% (though there was a minor charge around 2000 for this).

Sir my loan sention in december 2022 Amout os Rs. 2442094 from indiabulls finance company. My EMI was 22668 For tenure month 240. But RBI chage ROI 25 basis and 35 basis. He increased my month 36.

I don’t understand what should I do.

Dear Arun,

It is an effect of interest rate hike and we can’t do much here.

Arun, You should pay a higher EMI and get the loan cleared fast otherwise you are paying a lot of interest. Ask your bank to restructure the EMI as per original date of loan closing and increase your EMI.

hy sir i have a project for repo rate change that time what is effect on bank intrest sir can you any tip/help me ? analysis 2019 to 2022 year data

Dear Naresh,

Can you elaborate more?

Thanks for the informative article!

Quick question – If the lending and deposits by RBI is for one day only, how does it affect the long term borrowing and deposits by bank customer. E.g. if X bank borrowed at higher rate from RBI for 1 day, how will it impact anyone doing a FD or taking a loan. Isn’t it immaterial?

Dear Abhishek,

Good question 🙂 It is the cost of borrowing and the profit margin that acts as an impact for long term lending and depositing for banks too.

Sir… I need a historical bank rate data of RBI, I mean from 2000 to 2023

Dear Sharanappa,

It is hard for me to fetch for each bank and share it here. You can visit the respective bank websites and search for the same.

Hi Sir,

Very informative article and you made it so easy to understand basic concepts. Can you please show banks interest rate hikes in relation to RBI rate hikes?

Dear Insiya,

Sure.

Very informative and interesting article, can you share the 10 year gsec interest rates for the same period?

Dear Milind,

Sure.

Thank you so much for sharing the information. It is very clear and easy to understand.

Dear Ramesh,

My pleasure 🙂

Thankyou very much for your detailed informative artical, it is easy to understand.

Dear Govardhanam,

My pleasure 🙂