Many of us investing in NPS (National Pension Scheme). But have you ever checked NPS Returns for 2021? Whether you analyzed who is the best NPS Fund Manager for 2021 or which is the best NPS Scheme for 2021?

NPS now slowly turning to be one of the major investment choices for many of us. It may be due to the default option provided to Government employees, tax benefits at the time of investment or to create of a retirement corpus.

What is Scheme Preference in NPS Account

In NPS, there are two types of options available to create your portfolio. They are as below. Remember this scheme preference is not available for Government Employees Tier 1 Account Type. However, they have the freedom to choose scheme preference in their Tier 2 account. For the rest of the investors, you have an option to choose scheme preference.

# Active choice – You will decide on the asset classes in which the contributed funds are to be invested and their percentages. There are four asset classes available.

- Equity or E

- Corporate Debt or C

- Government Securities or G

- Alternative Investment Funds or AIF

Up to 50 years of age, the maximum permitted Equity Investment is 75% of the total asset allocation. After 60 years of age, the maximum permitted equity investment is 50%. Percentage contribution value cannot exceed 5% for Alternative Investment Funds.

# Auto choice – Lifecycle Fund– This is the default option under NPS and wherein the management of investment of funds is done automatically based on the age profile of the subscriber.

- Aggressive (LC-75) – Maximum Equity exposure is 75%, Corporate Debt 10% and Government Securities 15% up to the age of 35. It reduces to the maximum of 15% in equity 55 years and above. But retained same in Corporate Debt 10% and increases in Government Securities 75%.

- Moderate (LC-50) – Maximum Equity exposure is 50%, Corporate Debt 30% and Government Securities 20% up to the age of 35. It reduces to the maximum of 10% in equity and Corporate Debt 10% 55 years and above. But increases in Government Securities 80%.

- Conservative (LC – 25) – Maximum Equity exposure is 25%, Corporate Debt 45% and Government Securities 30% up to the age of 35. It reduces to the maximum of 5% in equity and Corporate Debt 5% 55 years and above. But increases in Government Securities 90%.

Such changes will be done on the birth date of the subscriber. Such changes can be done once in a financial year.

What are the types of funds available in NPS?

There are foud types of NPS funds available. They are as below.

- Asset Class E : Invest in equity market instruments. This is the riskier asset class among all three.

- Asset Class G : Invest in fixed income instruments. The best example of this is the central government bond. This is secured among all three.

- Asset Class C : Invest in fixed income instruments. Examples of these are bonds issued by firms or companies. this neither risky like Asset Class E nor safe like Asset Class G.

- Asset Class A – Alternative Investment Funds including instruments like CMBS, MBS, REITS, AIFs, Invlts etc.

Do remember that Alternative investment Fund is not available for “Auto Choice” and Tier 2 Accounts.

List of NPS Fund Managers

Currently, there are 7 Fund Managers who are managing our NPS corpus and they are as below.

# Pension Funds for Government Sector-

- LIC Pension Fund Ltd.

- SBI Pension Funds Pvt. Ltd.

- UTI Retirement Solutions Ltd.

# Pension Funds for Private Sector-

- HDFC Pension Management Co. Ltd.

- ICICI Prudential Pension Fund Management Co. Ltd.

- Kotak Mahindra Pension Fund Ltd.

- LIC Pension Fund Ltd.

- SBI Pension Funds Pvt. Ltd.

- UTI Retirement Solutions Ltd.

- Aditya Birla Sunlife Pension Management Ltd

Few important points to note:-

Different fund managers can be selected for Tier 1 and Tier 2.

2. But only one fund manager can be chosen to manage assets within a particular tier e.g. If HDFC pension fund is chosen then all Equity, Corporate, Govt securities in Tier 1 will be managed by HDFC only. It is not possible to choose HDFC for Equity, UTI for Corporate, ICICI for Government.

3. Considering the above, it is prudent to select a fund manager based on overall performance in Equity, Corporate, and Government securities instead of a single category. Further, the asset allocation percentage chosen by subscribers should be considered too.

E.g. If you have Equity: Corporate in Tier 1 with 75:25 percent allocation. If you like the UTI fund for Equity and the HDFC fund for Corporate, as your Equity allocation is higher, you can select UTI as my fund manager. So, UTI manages both Equity and Corporate assets in Tier 1.

NPS Tax Benefits 2021

Many of us invest in NPS mainly because of tax-saving options. But sadly many fail to understand the different sections one can avail by investing in NPS.

I am explaining the same from the below image.

NPS Returns for 2021 – Who is the best NPS Fund Manager?

Now let us concentrate on NPS Returns for 2021 and try to find who is the best NPS Fund Manager for 2021 or which is the best NPS fund for 2021.

Note:- Refer to our last post on NPS changes in 2021 at “NPS Changes in 2021 – New changes you must know“.

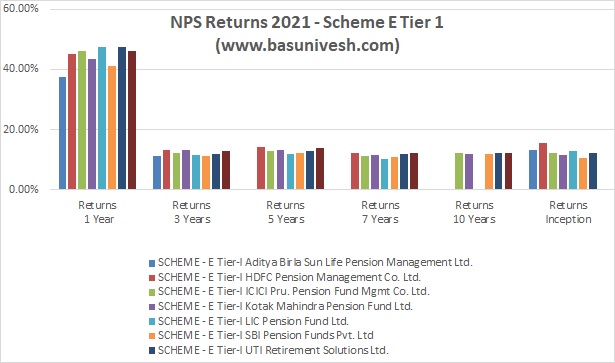

a) NPS Returns 2021 – Scheme E Tier 1

Let us look at the NPS returns from scheme E Tier 1.

You noticed that 1-year returns are the highest. It is all because of the bull run we are witnessing since a year. But the consistent performers are UTI and ICICI since inception.

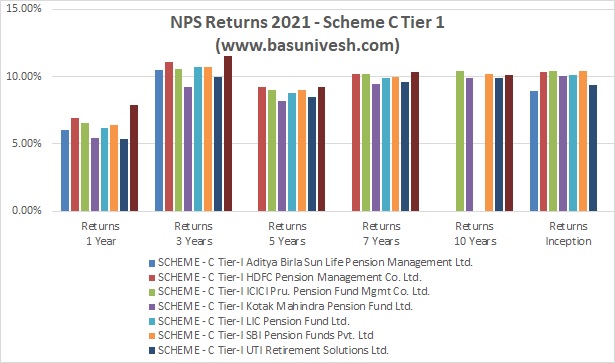

b) NPS Returns 2021 – Scheme C Tier 1

Let us look at the NPS returns from scheme C Tier 1.

Here also, we can notice that UTI and ICICI are the consistent performers for 10+ years.

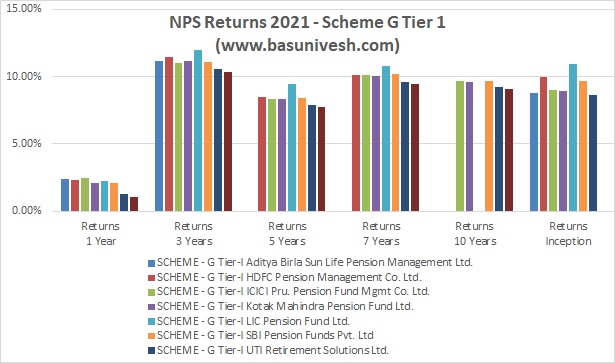

c) NPS Returns 2021 – Scheme G Tier 1

Let us look at the NPS returns from scheme G Tier 1.

Here, SBI and ICICI top the performance if we look into 10+ years of performance.

d) NPS Returns 2021 – Scheme A Tier 1

Let us look at the NPS returns from scheme A Tier 1. As I told you above, this is a newly added category and is available only for Tier 1 active choice.

e) NPS Returns 2021 – Scheme E Tier 2

Now let us move on to Tier 2 fund performance.

If you look for 10+ years of consistency, then I think UTI and Kotak did fantastically. However, my preference is UTI or ICICI.

f) NPS Returns 2021 – Scheme C Tier 2

Here, UTI, SBI, and ICICI did well if we look for 10+ years of performance.

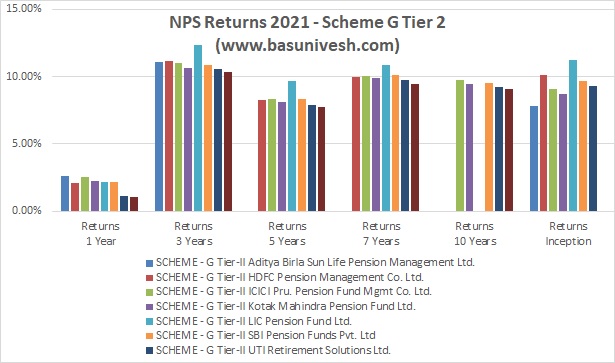

g) NPS Returns 2021 – Scheme G Tier 2

Here too, ICICI and UTI are toppers.

h) NPS Returns 2021 – Central Government Scheme

As I mentioned above, in the case of the Central and State Government Scheme of NPS, only three fund managers are there. Hence, let us look into their performance.

Here, there is no such a great difference if you look into 10+ years of performance.

i) NPS Returns 2021 – State Government Scheme

Here also all the three fund managers did well.

Who is the best NPS Fund Manager for 2021?

Based on the above returns, we may assume that UTI and ICICI are the best performers. However, even LIC, Kotak and HDFC are also doing well.

Hence, as I pointed out above, choose the fund manager based on which asset class has a heavy weightage in your portfolio. However, personally, to speak, I am not a big fan of NPS. Read my views here “National Pension Scheme (NPS) – 5 Biggest Disadvantages“. Those who are employed in State and Central Government may have no choice and at the same time, those who enrolled through corporate. However, for others investing more than Rs.50,000 (Additional Tax Advantage under Sec.80CCD(1)) is useless. Stay away from this product.

Dear Basu Sir,

Could you please provide NPS best performers with latest data? Now, we can select different fund manager for different assets. It would be very helful for NPS investors.

Dear Rajan,

Thanks. Will do Rajan.

What happens to NPS if investor becomes NRI.

Dear Aakanksha,

As NRIs are also allowed to invest in NPS, you can continue the same.

Your analysis of best performing is biased towards certain fund houses. Look at HDFC . It has been the most consistent and given best overall Returns.

Dear Piyush,

For your information, I do not get anything with my bias towards a particular Fund Manager. I have looked for 10+ years of time horizon. In that case, HDFC has not yet completed 10 years in many categories. Hence, said so. Above that, if you feel HDFC is the best, then you are free to choose.

Hi Bashu, just wondering, according to you what is the best long term investment plan! I have gone through your outdated article in the link in the summary (National Pension Scheme (NPS) – 5 Biggest Disadvantages). Lot of recent changes have done in NPS including exemption of tax on returns. Why don’t you update your first article before posting another one!

Dear John,

There are many ways to create your retirement corpus. Better to stay away from products that will lock your money. Regarding my OUTDATED post, may I know which part of the post is outdated? What have the changes happened with respect to returns on NPS? Look beyond taxation and see how horrific the product is.

In first 3 graphs, there are 8 bars and only 7 names in legend. Please fix.

Dear Amol,

Thanks for pointing. Actually, the 8th one is a benchmark which I forgot to mention in legend.

@Subakumaran

Sir, the legacy funds i.e accumulated NAVs are also invested from forthcoming FY.

Hi sir, even CG employees can change the scheme preference in Tier 1 ( except LC 75).

However, this scheme preference is applicable only for subsequent contribution and not for already existing corpus.

Hope it helps ?

Dear Subakumaran,

Thanks for your updates.