What are the new EPF Taxation and TDS Rules if your contribution per year is more than Rs.2.5 lakh? How do calculate it and what are the rules? Let us try to understand these new rules with some examples.

In terms of TDS on EPF, there are two situations where TDS will be applicable.

# EPF Withdrawal Taxation and TDS Rules

I have explained the same in the below image. Earlier the limit of such TDS was for more than Rs.30,000 and above withdrawal amount. In Budget 2016, the limit was raised to Rs.50,000.

You may refer to the detailed post on this “EPF Withdrawal Taxation-New TDS (Tax Deducted at Source) Rules“.

New EPF Taxation and TDS Rules – Contributions above Rs. 2.5 lac

As per the circular, the effective date for TDS in case of final claim settlement shall be:

i) 01.04.2022 or final settlement/ transfer – whichever is later, and

ii) in all other cases, TDS shall be on the date of credit of interest.

Applicability of TDS –

TDS is applicable in case of

a) PF final settlement,

b) transfer claims,

c) on transfer from Exempted establishments to EPFO and vice versa,

d) on transfer from one Trust on another,

e) past accumulations transfer, at the time of annual accounts processing, on back period accounting after accounts for year 2021-22 are processed.

The TDS will also be applicable in death cases as in the case of a live member. It will be applicable to all EPF members including members of Exempted Establishments/Exempted Trusts. It will also be applicable in case of International Workers.

This is the new EPF Taxation and TDS Rules rules that came into effect on 1st April 2022 if your contributions to EPF are more than Rs.2.5 lakh a year. Hence, any contribution you done from FY 2021-22 will be taxable and tax is deducted as per this new rule.

The Government has changed the rules for the calculation of interest on EPF accounts. It has set a threshold limit for contribution in EPF Rs. 2.50 Lakhs and GPF Rs. 5.00 Lakhs (as there is no contribution from the employer) on which interest received will not be taxable. Any interest on the contribution made during the FY 2021-22 in excess of the amount of Rs. 2.50 Lakhs (EPF) and Rs. 5.00 Lakhs (GPF) will be taxable as “Income from Other Sources “in the hand of the employee or person contributing to those funds.

The CBDT has notified Rule 9D to calculate the taxable portion of interest pertaining to the contribution made to a statutory or a recognized provident fund in excess of the threshold limit of Rs. 2.5 lakh or 5.0 lakhs as the case may be. It provides that separate accounts within the provident fund account shall be maintained during the previous year 2021-22 and onwards for the taxable and non-taxable contribution made by the person.

Only the interest accrued in the Taxable contribution account would be taxable in the hands of the employee under the income head ‘Income from Other Sources”. The interest accrued in the Non-taxable contribution account shall continue to be tax exempt.

As per the accounting system of EPFO,

Interest is credited on annual basis. However, Member accounts are maintained monthly as per Para 60(2) (a) of EPF Scheme, 1952. I have written a detailed post on this at “How EPF (Employees’ Provident Fund) interest is calculated?“.

To manage this new rule’s applicability, the same method is further divided into two components.

# Taxable

# Non-Taxable

The applicable TDS rates for this new rule are as below –

i) 10% if PF account is linked with valid PAN,

ii) 20% if PF account is not linked with valid PAN (i.e., TDS rate would be double)

iii) 30% under Section 195 subject to provisions of DTAA; in case of non-resident.

The threshold limit in the case of GPF is Rs.5 lakh and for EPF it is Rs.2.5 lakh.

Let us take few examples here.

Scenario 1 – Taxation for FY 2021-22 contributions

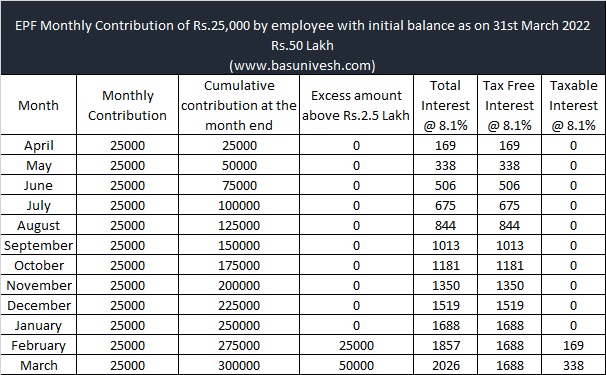

Mr. X’s monthly contribution towards EPF from 1st April 2021 is Rs.25,000. He has an earlier balance of Rs.50,00,000. EPF interest rate considered is at 8.1%. Then the monthly contribution, taxable, and tax-free interest table look like below for FY 2021-22.

The above chart is only with respect to the monthly contribution done during a year. However, as I mentioned above, he has an earlier balance of Rs.50 lakh also. Hence, the taxable and non-taxable list looks like the below.

a) Tax-Free account

Opening balance – Rs.50,00,000

Interest on opening balance – Rs.4,05,000

The contribution made up to the threshold limit for FY 2022-23 – Rs.2,50,000.

Interest earned on the threshold limit – 12,659

TDS @10% in case PAN is available and linked with Aadhaar – NIL

TDS @20% in case PAN is not available and not linked with Aadhaar – NIL

TDS @ 30% for NRIs – NIL

Year-end balance (as on 31st March 2022) of tax-free account is Rs.50,00,000 (initial balance) + Rs.4,05,000 (interest on Rs.50,00,000 balance) + Rs.2,50,000 (contribution of last year below the threshold limit) + Rs.12,659 (interest on such contribution of below Rs.2,50,000) = Rs.56,67,659

b) Taxable account

Opening balance as on 1st April 2021 – NIL

Interest accrued on opening balance – NIL

Cumulative excess amount above Rs.2.50,000 – Rs.50,000

Interest earned on such excess amount during FY 2021-22 – Rs.507.

TDS @10% in case PAN is available and linked with Aadhaar – Rs.50.07

TDS @20% in case PAN is not available and not linked with Aadhaar – Rs.101.4

TDS @ 30% for NRIs – Rs.152.1

Total year end balance (as on 31st March 2022) in such taxable account is Rs.50,000 (contribution above Rs.2,50,000) + Rs.507 (interest on such contribution above Rs.2,50,000) = Rs.50,507.

Scenario 2 – Taxation for FY 2022-23 contributions

From here onwards there are two accounts to be managed. One is a taxable account and another is a tax-free account. Let us first discuss tax-free account details.

The monthly contribution table and interest earned on such monthly contribution will remain the same as the above table of scenario 1 for FY 2022-23. Because our contribution is same and interest rate is also same. However, the tax-free account and taxable account details will vary. Hence, I am not again sharing the above table. Rather, I will explain the taxation from FY 2022-23.

a) Tax-Free account

Opening balance as on 1st April 2022- Rs.56,67,659

Interest on opening balance – Rs.4,59,080

The contribution made up to the threshold limit for FY 2022-23 – Rs.2,50,000.

Interest earned on the threshold limit – 12,659

TDS @10% in case PAN is available and linked with Aadhaar – NIL

TDS @20% in case PAN is not available and not linked with Aadhaar – NIL

TDS @ 30% for NRIs – NIL

Year end balance (as on 31st March 2023) – Rs.56,67,659 (Initial balance) + Rs.4,59,080 (interest on such initial balance) + Yearly contribution below the threshold limit Rs.2,50,000 + Interest on such contribution of below threshold limit Rs. 12,659 = Rs.63,89,398.

b) Taxable account

Opening balance as on 1st April 2022 – Rs.50,507

Interest accrued on opening balance – Rs.4,091

Cumulative excess amount above Rs.2.50,000 – Rs.50,000

Interest earned on such excess amount during FY 2022-23 – Rs.507.

Total taxable interest earned during FY 2022-23 – Rs.4,091 (from the initial balance) + Rs.507 (on the monthly contribution in excess of Rs.2,50,000) = Rs.4,598.

TDS @10% in case PAN is available and linked with Aadhaar – Rs.459.8

TDS @20% in case PAN is not available and not linked with Aadhaar – Rs.919

TDS @ 30% for NRIs – Rs.1,379.

Year end balance (as on 31st March 2023) -Rs.50,507 (Initial balance) + Rs.4091 (Interest on year end balance) + Rs.50,000 (Contribution above Rs.2,50,000 in a year) + Rs.507 (Interest earned on contribution beyond threshold limit) = Rs.1,05,105.

Conclusion – I hope that the above examples will give you clarity. However, I have one doubt which I am unable to find from the notification of EPFO regarding Rule 9D (Dated 31st August 2021) is whether the future partial withdrawals are considered as part of the taxable EPF amount or from tax-free EPF amount. If anyone of you found the clarity on this aspect either from EPFO or from CBDT, then please do share the same by commenting to this post.

Hello Sir,

I had short tenure (less than 5 yrs) in my job, which incidentally started on 1st April 2021 (quit in Jun 2024). I have withdrawn the EPF from the trust, which the private company was maintaining. For two years I have crossed the 2.5 Lakh contribution limit. I am confused about the income tax calculation – for filing of the return for FY 24-25. Could I send more details and would you help me out. Kindly respond.

Thanks

Atul

Dear Atul,

Both are taxable and you have to show it in your ITR as income from other source. Regarding helping, I strongly suggest you to take the help of local CA.

Dear Sir

How to report EPF interest on amount above 2.5 lakhs for the current year and interest from accumulated balance greater than 2.5 lakh that was the opening balance for this year in ITR-2 form. Need help. As I understand, it should come in income from other sources, but that section itself has many sub-sections. I presumed this is under section 10(11) first provision. As soon as a value is entered in 10(11) first provision the other 3 fields -10(12) first provision, 10(12) first & second provision gets grayed out. Kindly advise if the entry has to go under 10(11) first provision (mine is pvt sector with threshold limit 2.5 lakhs)

Dear Kumar,

It is sadly still a grey area which many are facing.

Hello Sir,

Please confirm if the following is a valid EPF withdrawal scenario.

– Employee quits job/service at the age of 47.

– He does not close the EPF account.

– Every year he withdraws the EPF interest till the age of 58. He pays the income tax according to the tax slab considering this interest as income.

– The EPF account gets closed at the age of 58 and the entire corpus is returned to the employee.

– Pension starts at the age of 58.

Thank you,

E.S.S.Kiran.

Dear Kiran,

Correct.

Dear Sir, I’ve got the employee contribution to EPF, including VPF greater than 2.5 lacs for FY 2021-22. Hence, I need to pay tax on the interest earned on the contribution greater than 2.5 lacs. While submitting the ITR before 31st July 2022, I did some rough calculations and submitted ITR. Now, I see that some TDS is deducted on the interest earned for FY 2021-22 in EPF passbook. Few queries: 1. How can I find the EPF interest income for which this TDS is deducted ? I do not see it in the EPF passbook nor in any form 16, 26AS. 2. How do we fill the ITR-2 form for this EPF interest income ? Need help. As I understand, it should come in income from other sources, but that section itself has many sub-sections. Please elaborate.

Dear Alok,

I have replied to your email.

Sir do EPF and vpf both earn same interest? Any limits or restrictions? Please advise. Thanks.

Dear Tej,

Yes. The maximum allowed is EPF + VPF = Basic Salary.

Thank you.

I could not find on TDS for accounts where there is no PF contribution for 6-7 months in a year in the article. Can you please clarify if there will be TDS for such accounts or not?

Thank you

Dear Viswanath,

TDS is applicable when you withdraw EPF.

Dear Sir,

Please let me know if there will be a tax deduction on interest for a PF account in which there are no transactions for the past 7 months? The PF account having a continuity for more than 10 years.

Also, are there any complications from transferring to a private trust PF account from EPFO PF account and Vice versa?

Thanks

Dear Vishwanath,

Please refer the above post. Your doubt is already answered there.

Dear Basu,

As per my salary slip, my basic pay is 95,375INR. PF contribution by my employer is 1,800INR and my VPF contribution is 10,000INR. When i requested to increase my VPF by additional 10,000INR , i have been informed that i cannot increase my VPF not more than 15,000INR per month which includes my employer contribution also. I want to understand is there any such limit exist or i can increase my VPF based on my basic pay to further more. Please clarify.

Dear Aravindan,

Your employer is misguiding you. You are allowed to contribute 100% of your basic towards EPF (EPF+VPF).

EPFO has neither credited the interest nor deducted TDS for the year FY2021-22 yet. How should we then show EPF interest in Schedule OS of ITR filing which is due in 2 days? (Assuming employee contribution is more than INR 2.5 lakh)

Or is it better to show it next year’s ITR when the TDS is actually deducted by EPFO? Though I am not sure if EPFO will deposit as TDS corresponding to FY2021-22 or FY2022-23.

Dear Krishna,

Let them first show the credit of interest and TDS to reflect in your AIS, then you can. This is what I pointed out from day one of these new regulations. EPFO is a mess when it comes to service. Floating rules are easy for the Govt but there should be coordination between EPFO and IT Dept. Otherwise, this new rule is turning out to be a huge issue for many salaried.

with introduction of taxation on EPF interest on contribution of more than 2.5 lakhs, would you suggest investing more than 2.5 lakhs via EPF+VPF for people whose income fall in 30% tax bracket?if the EPF interest rate is 8.1%, after 30% tax, it becomes approximately 5.6% only.

Dear Sandipan,

I still feel it the best option (even if you are falling under 30% tax bracket). However, the biggest issue is managing this tax process on yearly basis 🙂

Sir

In the chart shown above, the interest, credited for April would be for 12 months, while for May, it would be for 12 months or 11 months (it is for 12 months in your sample computation)

pl clarify

Dear Mallikarjuna,

It is for 11 months but not for 12 months. I have shown cumulative interest in the first month’s contribution and the second month contribution together. Hence, I think you got it confused.

If my PF account is having No Employer contribution from Jul 2020 ( due to loss of job ), and if i continue to Hold my PF account ( No withdrawal, planning to keep it till Mar 2032 age of 58 ), do i end up any Taxation or TDS?

Dear Sunil,

For any such non-contributory accounts, the interest earned is taxable (NO TDS).