LIC Jeevan Akshay VII Pension Plan (857) introducing it from 25th August 2020. It is the immediate pension plan. At the same time, LIC is withdrawing the immediate pension option from Jeevan Shanti (850).

Considering the decreasing interest rate, it was expected from LIC that it may revise the pension rates of Jeevan Shanti. Instead, it removed the immediate pension option of Jeevan Shanti and introduced the LIC Jeevan Akshay VII Pension Plan (857).

Before proceeding further, let us understand few new words related to pension or annuity plans.

What is the meaning of annuity?

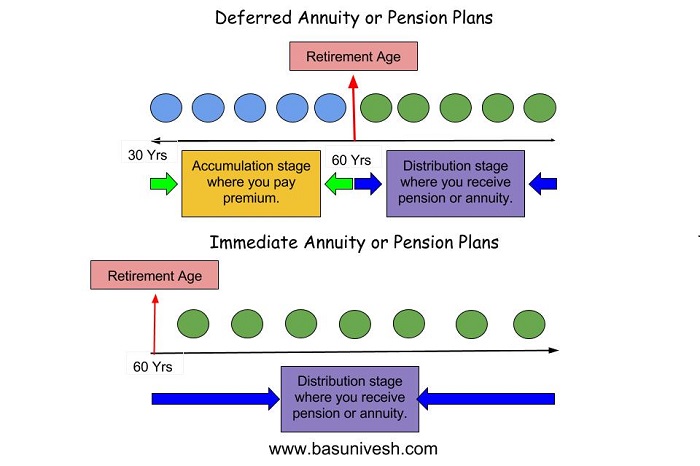

In simple term, you can say it as a Pension, where you will get regular income up to the specified period or conditions. There are two types of annuity.

1) Immediate Annuity-In this case, you invest a lump sum in a product and your pension or annuity starts immediately. Let us say you have around Rs.1 Cr and if you buy immediate annuity plans, then the pension will start immediately from next month.

2) Deferred Annuity-In this case your annuity starts after a certain period. Let us say your current age is 30 years and you are planning to retire at the age of 60 years. If you buy a deferred annuity plan, then you will invest up to your retirement age i.e. up to 60 years of age. After 60 years of retirement, your pension will start.

I tried to explain the same with below illustration as below.

LIC Jeevan Akshay VII Pension Plan (857) – Features, Benefits, and Eligibility

Below are the silent features of this plan.

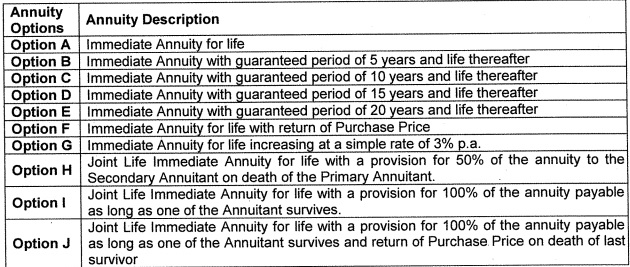

Below are the pension options available under LIC Jeevan Akshay VII Pension Plan (857).

The additional feature of what this plan offers is that the death benefit payable to the nominee can be opted in installments ranging period from 5 years, 10 years or 15 years.

NPS subscribers may opt for this immediate plan. However, for Government employees, the default options are Option J and Option F.

The policy is eligible for surrender after 3 months (only for Options F and J).

You can avail the loan also under this plan.

Taxation of annuity products:-

As it is a pension plan, the pension you receive is taxable income as per your income tax slab.

LIC Jeevan Akshay VII Pension Plan (857) – Should you buy?

Let us take an example of a 50 years old guy and opting for this product. the annuity rates (for offline) looks like below.

You noticed that the annuity rates hover around 5% to 6% based on the option and the age group. If we consider the taxation, then obiviously the returns are much lower. However, such plans are suitable for those who are under lower tax bracket and looking for constant stream of income.

Do remember that inflation is one more enemy (along with taxation) which you have to consider before opting for such products.

Conclusion:- LIC Jeevan Akshay VII Pension Plan (857) is obviously offer you lesser pension than the existing Jeevan Shanti Plan. Also, tax and inflation are the biggest enemies for such plans. Do your own research before jumping into such plans. I prefer RBI Floating Rate Bonds, PMVVY or Post Office Senior Citizen Savings Schemes better option. However, it is up to you to take your own call.

Refer our latest posts:-

- Your Retirement Success Depends on Luck, Not Skill

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

- 5 Important Investing Truths Most Investors Ignore

- Retirement Is Personal — Stop Comparing Net Worth and Move On

- EGR: The Gold Investment 99% of Indians Have Never Heard Of

Dear Sir

please provide a illustration of annuity payable monthly for H and I options per lakh investement in Jeevan Akshay VII Pension Plan (857)

I am 59 year old and spouse 53 year.

Dear Jagadish,

Please visit the LIC website and by inputting your details, you can get the results instantly.

Thank you for the wonderful information on this Jeevan Akshay VII plan. I would be obliged if you could clarify one doubt. My cousin brother (68 years) who does not have any legal heirs (he was the last surviving member of his family) invested an amount of ?30 Lakhs in this plan in October 2020 with monthly pension option putting me as nominee. He was a diabetic and heart patient. Soon after that, he died due to heart attack. Now the purchase price is being paid in full to me as nominee. I wish to know whether this is taxable. I am getting a lot of information with ambiguity. Some say that death benefit under all plans paid to nominee is not taxable under Section 10 10 D. Some say that the amount is taxable since I am not a blood relation but a cousin brother.

I would be thankful if you could share factual and correct information on this. This is important as I will be transferring more than ?20 lakhs of this amount to some of my other cousins who are not economically well off and are suffering. Thank you.

Dear Adishankar,

It is tax free.

Is it advisable to purchase Jeevan Akshay VII for my mother aged 68 Years. Can I opt Option F for her while purchasing the annuity. She is within the taxable limit as allowed to Sr. Citizen.

Dear Dev,

I suggest PMVVY or SCSS than this product. If both of those options exhausted, then you can explore this product.

Sir,

Thanks for the blog and helps people to get investment ideas.. but I always seen you advising not to invest in any plans that includes funds, LIC plans, gold bonds etc..

if I look back your post on LIC pension plans, 3 years back interest rate was 8/9 and now it’s 5/6.. imagine someone who read your post that time missed a great opportunity to invest.. similarly when gold bond was 28k your advise was not to invest and now its doubled in value.. Please publish articles on the current investment needs considering macro and micro economic factors and not to misguide people on best opportunities that are presented to retail whether it’s goi 7.75 bond , Gold bonds, LIC, banking and psu, Gilt funds etc.. all these plans invested at right time yielded excellent returns…

Dear Santosh,

Regarding my earlier post on LIC Pension Plans, whether the last and the current product address my concern of INFLATION or TAX BENEFITS? Issues remain the same as they were earlier. At the same time, regarding the gold, few years of uptrend means everything changed for the Gold 🙂 Gold is still highly volatile asset like equity. Few basics of what I shared remain same irrespective of the change in rate for few years.

If you are ready to have EXCELLENT RETURNS at BLIND RISK, then you are very much free to go ahead 🙂

Sir, beg ur hlp plzz..

How mny times I cn deposits into SSY of my daughter?? Someone scared me saying I can deposit only 10-times in one financial year??

Unlike what I had read recently that as per latest rules I can make multiple deposits into same SSY(one) account..

I’m very confused, plzz hlp/clarify sir.

Thankfully, rjn&fly.

Dear Rjn,

Whatever you read is correct.