What are the Latest Income Tax Slab Rates FY 2019-20 (AY 2020-21) after the Budget 2019?

I already covered the Budget 2019 related posts and you may refer them for your better understanding.

In this post, my concentration is to share you about the Latest Income Tax Slab Rates FY 2019-20 (AY 2020-21) and applicable Security Transaction Tax (STT).

The difference between Gross Income and Total Income or Taxable Income?

Before jumping into Latest Income Tax Slab Rates FY 2019-20 (AY 2020-21), first understand the difference between Gross Income and Total Income.

Many of us have the confusion of understanding what is Gross Income and what is Total Income or Taxable Income. Also, we calculate the income tax on Gross Income. This is completely wrong. The income tax will be chargeable on Total Income. Hence, it is very much important to understand the difference.

Gross Total Income means total income under the heads of Salaries, Income from house property, Profits and gains of business or profession, Capital Gains or income from other sources before making any deductions under Sections.80C to 80U.

Total Income or Taxable Income means Gross Total Income reduced by the amount of permissible as deductions under Sec.80C to 80U.

Therefore your Total Income or Taxable Income will always be less than the Gross Total Income.

Latest Income Tax Slab Rates FY 2019-20 (AY 2020-21)

There are three categories of individuals based on the age of taxpayer.

- Individuals whose age below 60 years.

- Senior Citizens whose age is 60 years and above but less than 80 years.

- Super Senior Citizens whose age is 80 years and above.

Hence, based on these three categories of individuals I have separated them and Latest Income Tax Slab Rates for FY 2019-20 (AY 2020-21) are as below.

Note: – Along with the applicable taxes, you have to additional surcharges at below rates.

- Surcharge:

- 10% surcharge on income tax if the total income exceeds Rs.50 Lakhs but below Rs.1 Cr.

- 15% surcharge on income tax if the total income exceeds Rs.1 Cr.

- Health and Education

cess : 4%cess on income tax including surcharge. This Health and Education Cess replaced the earlier 2% Education Cess and 1% Secondary and Higher Education Cess from Budget 2018.

You notice that there is no change in Income Tax Slab Rates for FY 2019-20. Then how can be it is judged that there is no tax on an individual whose income is up to Rs.5,00,00?

The reason is the change in Sec.87A in

How to calculate Income Tax on your net or total income?

Now we understood the Latest Income Tax Slab Rates FY 2019-20 (AY 2020-21

Let us not take few examples and calculate the income tax amount.

# If you are under 30% Tax Slab and below 60 years of age

Let us say your next taxable income (after all deductions like Sec.80C and all) Rs.15,00,000.

Up to Rs.2,50,000-NIL

Rs.2,50,001 to Rs.5,00,000-Rs.12,500 @5%.

Rs.5,00,001 to Rs.10,00,000-Rs.1,00,000 @20%

Rs.10,00,001 and above (in this case Rs.15,00,000)=Rs.1,50,000 @30%.

So total tax will be Rs.12,500+Rs.1,00,000+Rs.1,50,000=Rs.2,62,500.

# If you are under 20% Tax Slab and below 60 years of age

Let us say your next taxable income (after all deductions like Sec.80C and all) Rs.7,00,000.

Up to Rs.2,50,000-NIL

Rs.2,50,001 to Rs.5,00,000-Rs.12,500 @5%.

Rs.5,00,001 to Rs.7,00,000=Rs.40,000 @20%

Therefore, the total tax will be Rs.12,500+Rs.40,000=Rs.52,500.

# If you are under 10% Tax Slab and below 60 years of age

Let us say your income is Rs.4,00,000

Up to Rs.2,50,000-NIL

Rs.2,50,001 to Rs.4,00,000-Rs.7,500 @5%.

However, using Sec.87A of IT Act, your tax liability will be ZERO.

An individual who is

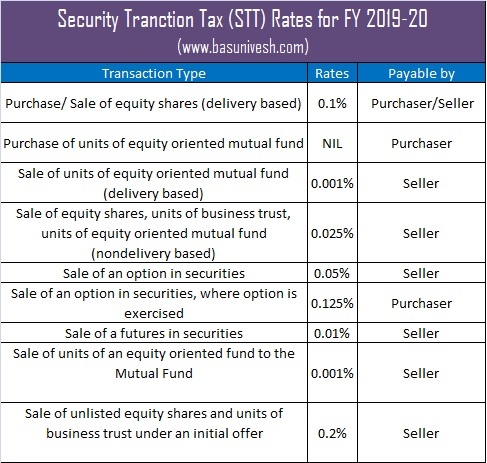

Security Transaction Tax (STT) for FY 2019-20 (AY 2020-21)

Security Transaction Charges or STT is the charges or tax when you buy or sell securities (excluding commodities and currency) through a recognized stock exchange.

The definition of securities involves the below products.

- Shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate;

- Derivatives;

- units or any other instrument issued by any collective investment scheme to the investors in such schemes;

- Security receipt as defined in section 2(zg) of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002;

- Government securities of equity nature;

- Rights or interest in securities;

- Equity-oriented mutual funds

Therefore, whenever you buy and sell these securities through a recognized stock exchange, then you have to pay this STT.

Now let us understand the latest Security Transaction Tax (STT) applicable for FY 2019-20 (AY 2020-21).

Hope now you became familiar with Latest Income Tax Slab Rates for FY 2019-20 (AY 2020-21) and also the way we can calculate our income tax liability (in simple terms). Any doubts??

Very informative article with tons of knowledge. Thanks for sharing!

Hi

My name is Ravi and I quit my job on November month and I am jobless for three months now. I need few clarification on withdrawing PF amount and added below . Please check and update me to proceed further.

1. Do I need to fill in the hard copy of form 15 or is there any other options available to fill in online and sumit the same form…?

2. Can I withdraw my full amount of PF?

3. I have worked only for eight months in that company and I am jobless for 3 months now.

Dear Ravi,

1) You can submit it online using your UAN login details.

2) Yes

How to pay STT?

Dear Prasad,

It is not you who has to pay the this. Mutual Fund companies will pay it and mention the same in your statement.

What will be the income tax if my income is above 10 lakhs per annum, let’s say 1050000 PA? I didn’t find the income slabs ranging from 1000001 – 9999999 in this post!

Dear Vanga,

There are only three tax slabs. Hence, the said individual falls under 30% tax slab.

Sir all the things you explained are good.

but u didn’t mentioned about the standard deduction to the Government Salaried employees…Is it Rs. 50,000 or not, please explain this point.

Dear Amandeep,

Please refer above post and also the relevant posts related to Budget 2019.

Dear Sir,

I am an individual below 60 years. Please find below my tax calculation and confirm if it is right?

Total Income: 938000

PT(Deduction under Sec 16) 2500

Annual PF (Employee Contribution)( 80c) 21600

Mediclaim Premium(80D) 2539

LIC(80c) 2904

Taxable Income 908857

Non taxable Income Basic Limit 250000

Taxable Income 658857(908857-250000)

250001 to 500000 =5%(5% on 250000(500000-250000) 12500

50000 to 100000 =20% +12500; 20% on 158857(658857-500000) 44271

56771

4% Cess on total tax 2271

Total taxable amount for the year 59042

Tax per month 4920

Is my calculation right?

Dear Vijaya,

It is hard for me to calculate for each and every one. I can help you only if you have certain doubts.

st deduction 50k…we need to deduct man from total

Dear Sir,,

Say for eg, if total taxable income after deductions is 900000 and upto 250000 Tax amount is Nil , then net taxable income is 650000 INR (900000-250000) on which slab rate at 250001 till 500000 and 500001 to 1000000 has to be applied. Is this right?

Dear Vijaya,

Yes, you are right.

Thank You Sir!

Dear Sir, My Taxable Income after deductions is 9088557. What will be my TDS

Dear Vijaya,

Does avoiding TDS means avoiding TAX?

Sir,

you have described the new rates of income tax slab for the assessment year 2020-21 alongwith all the changes i.e. U/s87A. But unfortunately you did not mention about the change in Stranded Deduction.

reagrds

Dear Rajinder,

This post is related to income tax slabs only.

For current DAY 2019-20 the maximum limit of ?1.5 lakhs in PPF is same or increased

Dear KP,

PPF limit is not increased and it is the same.

Hi,

Can you please explain how this 12,500+Rs.1,00,000+Rs.1,50,000 is calculated. I am not able understand

Dear Basava,

The first one is at 5%, second one at 20% and third one at 30% as per the slabs. Let me know if you still have confusion.

ignore the above comment.

Yes, for 5% and 20% calculation I got it, you are calculating from the lowest amount, but for 30% slab mentioned amount is not coming …can you please tell me how it is done. thank you.

Dear Basava,

Above Rs.10 lakh it is at 30%. In the above example, the taxable income of an individual is Rs.5,00,000 (which is above Rs.10 lakh) for 30% tax bracket. Hence, 30% of Rs.5,00,000 is Rs.1,50,000.

Let us say your next taxable income (after all deductions like Sec. 80C and all) Rs.15,00,000.

Up to Rs.2,50,000 @ 0% = NIL

Rs.2,50,001 to Rs.5,00,000 = Rs. 250000 @5% = Rs.12,500

Rs.5,00,001 to Rs.10,00,000 = Rs. 500000 @20% = Rs.1,00,000

Rs.10,00,001 to Rs.15,00,000 = 500000 @30% = Rs.1,50,000

So total tax will be

Rs.12,500+Rs.1,00,000+Rs.1,50,000=Rs.2,62,500/-

Dear sir,For sr citizens say aged 64 like me if gross total income is Rs.7lacs and under 80c investment made upto 1.50 lacs whether I will have to pay tax?Whether std dedn of 50000/= is eligible for dedn.Ifso any tax to be paid by me for FY 2019-20?

Dear Mohan,

Standard deduction is applicable only for salaried and pensioners. Regarding your tax liability, if your total income is beyond Rs.5,00,000, then yes you have to pay the tax.

Sir,I am a pensioner from bank service.Hence if i have to pay tax as per details given by me

Is investing in muthoot finance NCD(9.75%)Or commercial paper(9.25%)is safe Or not.. Should I go with this Or not..

Dear Vikas,

Wherever there is a HIGHER RETURN, there is always a HIGHER RISK. Analyze the same and invest.

SIR, WHO ARE ELIGIBLE FOR STANDERED DEDUCTION?

Dear Partha,

Salaried and Pensioners.

Sir I am sr citizen 68 years.My total gross income will be say 7.50 lacs for fy 19-20 , AY 20-21, as below:-

1. Pension income. = 4.50 lacs

2. Interest income FD/saving = 2.80 lacs

3. Medical reimbursments. = 0.15 lac

Total gross. = 7.45 lac

Deductions:-

1. U/S 16 , std ded. = 0.50. Lacs

2. 80C. = 1.50

3. 80TTB. =0.50

4 . 80 G. = 0.01

5. 80D. = 0.04

Total ded. = = 2.55 lac

Taxable total income. = 4.90 Lac

Tax, 0-3 lac. ( sr. Citizen ) = nil

Tax 3-4.90 Lac @5%. = 9500

Rebate u/s 87A.( max 12500) =9500

Tax NIL

Pl tell whether I am right in my calculations?

Perfect calculation

Hi Sachin…when the Celing Limit for Sr Citizen is Rs 5.00 L + Deduction US 80C 1,50,000.00 + Standard Deductions….etc. are applicable why a “Slab Rate Like upto Rs.3.00 L No Tax…..” etc. is seen being worked out in your calculations. The Slab Rate for Sr. Citizen should be corrected as “Rs.5.00 L No Tax etc.”, is it ??

Dear Rajinder,

Yes, your calculation is correct. Your tax liability turn to be ZERO.

I think you are wrong.because you did not avail rs 500000 rebate as per union budget 2019-20.

Dear Kuldeep,

After applying the same enhanced limit of Sec.87A, he mentioned that his tax liability is ZERO.

Yey…I have opined above similar. SinghJi is seen in line with my comments…

No tax benefit to senior citizens

Dear Satya,

Sadly no such benefits in this budget.

So sorry

Please clarify whether one individual has to pay tax on the amount excess of Rs5 lac or on the whole amount ie (Rs 5 lac+ Excess amount) as per Union Budget 2019-20 ?

Dear MR,

EXCESS amount means? If your TOTAL income is less than 5 lakh, then you no need to pay the tax.

If its say even 5.01 lac and u r not sr. Citizen, , u have to pay tax on full amount in excess of 2.5 lacs I think.

Am I right Basavraj ji?

Dear Rajinder,

Yes, because you can’t avail the Sec.87A deduction benefit.

Yes, agreed with you, SirJi…5 lakh + Std deduction Rs.0.5 lakh + deductions under section 80C 1.5 L etc. + finally the Rebate of 12,500 deducted…Correct ?

Mr.Basu,

While appreciating your quick reaction on budget for 2019-20 there appears an error in the above chart Latest Incometax Slab rates nullyfying benefit of no tax limit raised from 2,50,000 to 5,00,000, please

clarify.

s.v.sudharsanam

Dear Suvadharsanam,

For your information, tax slabs were not revised. But Sec.87A limit raised. Hence, we all feel that our income tax slabs raised. Please read above post once again for the clarity.

That confusion still exist and awaiting for a suitable revision. Primarily for Senior Citizen, the Slab, while being revised should read as “…Upto Rs.5.00 L = No Tax, From 5.00 L to …etc…..” May be a revision soon is expected. At the outset, upto Rs.5.00 is destined as No Tax for Sr. Citizen, overlooking any Slab Range, correct ??

Dear PVS,

Yes.

Dear sir,Am Ramesh, I applied epf in online and submitted 15 G,and mentioned pan and aadhar details,but reaction reason is

1)15G, 2)Form 15G/H, pan not summited by member,

am paying Tax, please help me to reapply and please let me know the procedure, Thank you

Dear Ramesh,

As per rule, they must not ask Form 15G. But sadly they are asking. Resubmit once again.