What if your loan interest rate is less and FD rate high? Is it happening like this? I don’t think so. But I recently came to know about this, where your loan interest is less than your bank FD rate. Therefore an opportunity to earn RISK-FREE return from your LOAN!

Recently I went to my native and found that loan is available at 4%. So many are using this opportunity to earn the risk-free return from such loan. Let me share what is this 4% loan. Below are some features of this loan. I tried to explain the same in a graphical way.

- Loan disbursement again will depend on the value of your agricultural land and the value of gold you pledge to the bank.

- But the bank will not pledge your land as a collateral against this loan.

- You have to provide land records to show that you own an agricultural land.

- You have to pledge gold against this loan.

- All rural public sector banks offer this scheme.

- Every year, the Government declares the discount it give under this scheme like in 2009-10- 1%, 2010-11 -2%, 2011-12 -3%, 2012-13 -3%, 2013-14-3% and for 2014-15-3%.

- You have to repay the loan within a year. Otherwise, you will not be eligible for a 3 % discount on your loan.

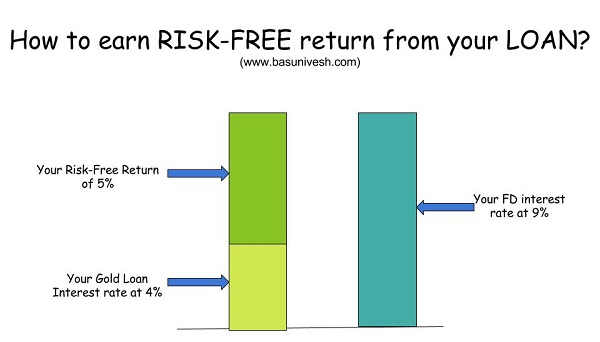

- So the actual interest rate on your Rs.3, 00,000 will be JUST 4%!

- If you repay the loan within a year, then they give you the discount of 3%.

- In this scheme, banks lend you up to Rs.3, 00,000 at a marginal interest rate of 7%.

- This scheme was launched in 2006-07.

- Farmers are eligible to take this loan.

- This is nothing but “Interest Subvention Scheme”.

How many utilizing this scheme and earning a RISK-FREE return?

I searched more about the features of “Interest Subvention Scheme,” and found that there is no such guideline mentioned about for what purpose the issued loan amount MUST be used. In addition, there is a huge pressure from Govt to spread awareness and disburse this loan.

So whenever someone approaches banks for a gold loan, banks use to push this product. The borrower has to just submit agriculture land ownership. Banks will not pledge the land. However, they issue loan against the gold, which you pledge with the bank.

Using this eagerness of banks to issue such low-cost loan and sensing the risk-free return of around 4% to 5% over their loan, many obviously opt for such loans.

They get the loan amount of Rs.3, 00,000 at 4% and deposit the same either in the same bank or with some other bank at the rate of 7% to 8%. So the risk-free return of 3% to 5%. If you take a bit risk, then deposit the same in co-operative banks. Usually, co-operative banks offer higher interest rate than nationalized bank. So few opt to deposit their money in such co-operative banks.

The lending bank never asks whether the disbursed loan is utilized for agriculture purpose or not. So a great opportunity for the one who own agriculture land.

Whether the banks and borrower stick to one-year loan agreements? That also just in papers. They renew the loan once in a year before the completion of a year of an old loan. For this, the borrower has to submit the recent dated land ownership proof. That’s it…The loan will continue as usual for next one year. The borrower continues to enjoy the risk-free return.

By sharing this loophole in the system, I am not pointing to follow this method to earn. However, I am pointing on how our Government schemes work and where our hard-earned taxpayer’s money wasted. In addition, 4% to 5% on Rs.3, 00,000 is not a big amount (may be Rs.10, 000 to Rs.15, 000). However, this may be useful for your payment of term insurance of health insurance premium 🙂

Hi

Please note that FDs attract tax deducted on the interest. This should also be taken into account. This is a big

Prasanth-Yes, thanks for pointing. But it differs from an individual to individual due to change in tax slabs.

hi Basavaraj, I have couple of queries regards to how to minimize the TDS by do investment as per current financial rules.

Could you share your email id so I can share necessary details with you and seek your advise.

Thanks

Mohan

Mohan-You can raise the doubt at Blog Forum. But do you feel avoiding TDS means avoiding income tax?

Interesting piece, not only the subject matter, but your Point of View as well! Sad thing is, it is intended for farmers, and they may not be reading this.

Animal part of my brain is thinking how to own agricultural land to take advantage of this 🙂

Bharani-You must already be owning an agricultural land to buy further. So first check your assets NOW 🙂

Can I apply this loan in Delhi? If yes, please let me know the names of the banks.

Ravinder-Yes, many nationalized banks offer this loan.

Thanks for your valuable advice. You are doing a fabulous job. Keep it up the good work.

here in saudi they are giving 4% loan.for 69,635 loan amount monthly installment is 2166 for 3 years on 4% rate.if I go with agent additional .10 to .20 reduced.do you think it is wise decision to take loan at 4% and invest in debt product or buy a house.

Mohmedaakib-It is purely your call.

I came acoss same type loan scheme fron HDB.they asked me to buy a HDFC Uday Policy for Rs 50000/- paid yearly for 10years via then through telephonically and they were assisting me getting a Loan Amount of Rs 700000/- @ intersest rate of 4.99% flat. And attractive thing was i was not required to pay montly EMI on it. They will deduct all the principal and Interest amount from the return amount after 15 years that comes around 1050000 to 1100000 approx and also they told me that i will be having a look in period of 30 days and if i did’t get loan amount by 25th day i can cancel my policy and get my premium back. But Iam thinking following points provided by them via illustration provided to me by hdfc standard life.

1.After paying Rs 50000/- yearly for 10 years sum assured provided is Rs 3,85,961/- after 15 years, rest 5 years after 10th year i will not have to pay.

2.Gurenteed benifit uday is Rs 443855/-

Iam in question if you can put some light on this HDFC uday Policy, that are they providing me a good offer or i will have to suffer after 15 years

Thanks

Puneet-It is typical traditional insurance plan where you may expect a return of around 5% to 6%. Stay away from such dangerous products.

Thanks Dear for your views.

Hi Basu,

Very good article for farmer & they can take advantage of it .I request others people to spread this article on social media so it could be reached to farmer as they really need it & agriculture sector is lagging in many areas.

Thanks,

Shalabh

Shalabh-Pleasure 🙂