We all know that currently, the interest rates on all FDs are falling. In such a situation how to earn around 7% from your savings account safely if you have a home loan? Interesting right? No risk of investing in any product or lock your money. Let us discuss this in today’s post.

Nowadays the major concern for many of us is the falling interest rates of Bank FDs and Savings Account. However, I found one home loan product that may easily make your earning from savings account around 7% or equal to your home loan interest rate.

How to earn around 7% from your savings account?

Whatever I am trying to say is meant for those who have home loans. If you don’t have any home loan, then this post is not for you. Here, I am discussing a Home Loan product of Bank of Baroda. The product name is “Baroda Home Loan Advantage”.

It acts like SBI MaxGain. If you don’t know what is SBI MaxGain, then refer to my earlier posts “All about SBI MaxGain Home Loan Scheme features and benefits” and “Difference between SBI MaxGain and Regular Home Loans“. Baroda Home Loan also acts in a similar fashion but with more add-on features which makes this product a unique one in the home loan market.

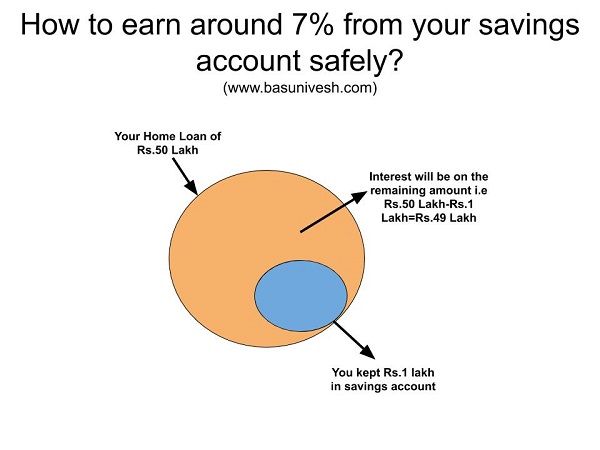

Let me give you an example. Assume that you have Rs.50 lakh home loan outstanding and EMI is around Rs.45,000. The interest for that particular month on this outstanding home loan will be calculated as below.

If the balance in your savings account at the end of 1st of October 2020 is Rs.1,00,000, then the interest on your outstanding home loan of is not on Rs.50 lakh. But the bank will consider the money you parked in your savings account as if the principal payment towards the home loan (even though the money is in the savings account) and interest will be calculated only on Rs.49 lakh (Rs.50 lakh home loan outstanding-Rs.1 lakh your balance at the end of the 1st October 2020). This way, you have reduced interest on your home loan by just parking the money in a savings account.

Let me show you the same through the below image.

I am not going into the product feature of this Barod Home Loan Advantage. However, few points I wish to share with you all before you wish to move to this unique loan.

# It acts exactly like how SBI MaxGain Home Loan. However, in the case of SBI MaxGain, you have to transfer your surplus to OD account. Here, you no need to do anything. Just keeping money in a savings account is enough.

# The savings account which is linked to this home loan account will not fetch any interest. I mean Bank Of Baroda will not give you the applicable savings account interest rate to this particular savings account.

# The interest will be on daily reducing balance at monthly rests.

# Whatever you earn by parking your surplus in this savings account will not be considered as income. Because you just saving your spending (interest payment). Hence, even though you are earning from such parking, it will not be considered as your income for taxation purposes.

# As your interest outgo to the bank will get reduced, your tax deduction under Sec.24 will also be reduced. However, think logically that by paying interest to banks do you really saving tax??? As per me, it is a foolish act to retain home loans for the sake of tax saving.

For a detailed procedure and applicable interest rate, you be in touch with the bank.

Conclusion:-By adopting the daily balance method on home loan and linking your savings bank account balance to your home loan, I think Bank Of Baroda offering you the unique home loan. Usually, nowadays many of us have a surplus of around Rs.50,000 to Rs.1,00,000 in a savings account. In such a scenario, such home loans are handy in reducing the interest outgo on our loan.

Refer our latest posts:-

- The Dark Side of Compounding: How 2% Kills Rs.30 Lakh

- Flexi Cap Funds: Why Your 10-Year Return Chart Is Lying

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

Hi,

Thanks for the informative post.

Could you please let me know if Axis super saver home loan offers the same benefits as Bank of Baroda Home Loan Advantage and SBI MaxGain?

Thanks in advance,

Kunal

Dear Kunal,

Axis super saver home loan works like SBI MaxGain. However, in the case of the above-shared product, even if you park the money in a savings account is considered as prepayment.

Thank you for the quick response, Mr. Basu. Really appreciated.

I think similar to Bank of Baroda, Axis super saver home loan also provides a separate account and issues a separate cheque book and ATM card (as per the website).

As Bank of Baroda is not financing the project in which I have invested in, I am planning to go ahead with Axis Super Saver Home Loan. It would be great if you can let me know the things to look at for this product (apart from listed above).

Again thanks for your response.

Regards,

Kunal

Dear Kunal,

If Axis offers the savings account, then no issues. If you are interested to go for Axis, then better to check their EBLR Vs Bank of Baroda EBLR.

Sure. Will check.

Thank you again.

Kunal

If we already have a homeloan running (with HDFC), how can one move to this Baroda plan?

Dear Kiran,

You can shift the home loan. Be in touch with Bank Of Baroda.

Every bank home loan should have this option in my opinion as we have in overseas, Its called offset account.

Its sad to see banks over complicating these simple things for customers.

Dear Hemanth,

Sadly in India, only a few banks offer such facilities. It is not complicating here too.

How it is foolish to retain home loans for sake of Tax savings. Can you elaborate it. I also have home loan I have sufficient money only for the purpose of Tax savings iam continuing the loan without prepayment.

Dear Sai,

Think wisely 🙂 Assume that Mr.X and Mr.Y fall under 30% tax bracket. Mr.X does not have home loan and Mr.Y opted a home loan for tax saving purpose under Sec.24 (maximum is Rs.2 lakh). Now, in the case of Mr.X, he will pay the tax of Rs.60,0000, this may seems to Mr.Y the foolish thing to pay such hefty tax. However, in case of Mr.Y, to save the tax at any cost (Rs.60,000), he is donating Rs.1,40,000 (Rs.2,00,000 interest-Rs.60,000 tax saved) to the bank. It is like as below.

Dear Bank,

I have to save the tax by hook or crook. Hence, legally I opted your home loan, where, I am ready to pay you Rs.1,40,0000 for the sake of saving tax.

Now, Mr.X, after paying Rs.60,000 tax, will keep Rs.1,40,000 in his pocket safely. But Mr.Y, who is happy that he saved Rs.60,000 tax will have to pay the interest to the bank in the form of Rs.1,40,000.

Now who is wise and who is fool? Paying Rs.60,000 tax and having Rs.1,40,000 in your pocket or saving Rs.60,000 tax and donating Rs.1,40,000 to bank???