Sounds interesting right? How to create Rs.100 Cr for your child? Well, it is actually simple, realistic and possible also. Let us see how we can achieve Rs.100 Cr for your child.

By writing this post, I want to actually share a certain concept of investment. Here, my idea is not to give a magic stick of creating Rs.100 Cr for your kid. But certainly a practical approach of creating wealth.

How to create Rs.100 Cr for your child?

For this, I considered below assumptions. You must be clear with what I have assumed at first.

I assumed that the kid born today. Immediately after the birth, the father starts monthly investment of Rs.25,000. This he will increase every year at a rate of 10%. I mean his monthly investment in the first year will be Rs.25,000 and the second year it will be Rs.25,000+10% and so on. Therefore, his first-year investment will be around Rs.3 lakh and next year it will increase to Rs.3,30,000.

The asset allocation between debt to equity is 40:60. The returns from equity I assumed is 10% and from debt it is 6%. Hence, the combined debt and equity portfolio will be 8.4%.

This investment he will continue up to the kid’s age of 20 years. So totally he will invest around Rs.1,72,29,244. Then how can this Rs.1.7 Cr will turn to be Rs.100 Crore?

Well, once the kid turns around 20 years of age, the father stops the fresh investment. He handover this whatever the accumulated corpus (which is approximately around Rs.3.48 Cr) to his kid and suggest him to manage the same asset allocation and not touch the same for the next 40 years. That is up to the kid’s age of 60 years.

So at 60 years of kid’s age this Rs.1.7 Cr will be worth of around Rs.100 Crore!! Yes, you are hearing it right. It is all because of using the compounding formula for your side.

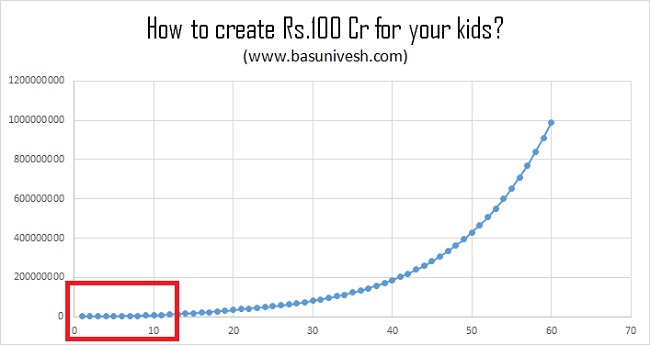

It looks fantastic to see handover Rs.100 Cr to your kid when he or she turned 60 years of age. The growth looks like below.

Notice the growth for the first 10-15 years, it is not at all noticeable. However, as the investment period passes, see how it takes a big leap.

So by doing this unimaginable numbers into imaginable, what I am trying to say? Well trying to say few important aspects of investment.

# Compounding works only for LONG TERM

Yes, you noticed above image that, you not feel the compounding effect if your investment horizon is around less than 10 years. However, if it is beyond 10 years or so, it starts to provide us the real effect of compounding.

Hence, never expect that wondering numbers if you are short term investors. Also, do remember one thing that only two things are under your control when you invest. First one is how much you invest and the second one is how long you wait.

But sadly we concentrate on KITANA MILEGA.

# Actual returns are not like LINEAR

You noticed in the above image that the return on investments are shown in a linear way as if we get around 8.4% year on year returns. However, in reality, it is not so easy. There may be certain periods like 4-5 years flat return, 4-5 years negative returns and another 4-5 years of positive returns.

Hence, never expect especially from the assets like equity that the returns will be linear like Bank FDs or it is shown in the above graph.

Hence, being calm, investing continuously, doing proper asset allocation and holding your behavior is a must for long term investing.

# Return on investment

For calculation purpose of the above example, I have considered the equity investments as 10% and debt returns as 6%. Hence, with an asset allocation of 60:40 between equity and debt, I am assuming 8.4% returns from the portfolio.

These numbers I think are fair numbers to consider the return expectation for long term investment from equity and debt portfolio.

# Asset allocation is a must

Yes, even though the investment period is long term, asset allocation between debt to equity is a must to protect money. Risk management should be your first priority.

As I was reading an investment book, I am sharing you the research result of what are the ingredients for one’s success in investment. What makes you successful in investing-Asset Allocation 93%, Fund Selection-2.5%, Other-2.2% and MARKET TIMING-1.7%.

Hence, never ignore the concept of asset allocation.

# Controlling your BEHAVIOR is a MUST

In the above example, the biggest task for both father and son is controlling behavior. Father has to invest continuously for 20 years without deviating from what he believed. At the same time, his biggest task is to teach his kid to manage the same principle and behavior for his kid also.

The same way the biggest task for a kid is to HOLD ON the accumulated corpus which his father handover when he will be 20 years and hold it for the next 40 years (i.e up to his 60 years of age).

It is not easy for both father and kid. However, winning in investment requires such a strong grit to hold on and believe in what they do.

Conclusion:-I am repeating again, here my point is not to create you a plan for achieving Rs.100 Cr when your kid turns 60 years of age. But here my idea is to share the investment principles and how it works. I hope you got my point.

Note:-The inspiration to write this post is from Subramoney.com.

Hello Basu Sir,

Thanks for explaining in simple terms likewise we have so many compounding theories and stories, theoretically yes its possible but if there is any real life example of someone achieved would make more sense, the theories never take into consideration about external factors like taxes, inflation and what not, the equities are always risky always comes with disclaimers one says go with SIP but SIP also requires portfolio balancing with churning else if one does SIP in single MF or multiple MF if the stocks are not rotated in that list will they really make money ? Also its the MF fund managers decisions which will decide how the fund will grow.

Do you think one sticks to only index funds can make money in long term ? What if govt decisions are not bringing results or negatively having effects how will one expect that they will make real money.

Do you think there is difference in theory and practical gains taking into consideration moderate gains while all hear and want to hear success stories but no one wants to see what is % of success v/s failure stories with similar strategy ?

Thanks

Raj

Dear Raj,

I want to reply in one sentence “WEALTH CREATION IS SIMPLE BUT NOT EASY”. Otherwise, all of us may be the wealthiest life Warren Buffet who used this concept of what I explained with around 10% returns and waiting invested for more than 55 YRS. How many of us have that PATIENCE, LEARNING and BEHAVIOR controlled SKILL? Taxes, inflation, government policies and returns always change. But we are not ready to do the things which are under our control-AMOUNT TO BE INVESTED and HOW LONG WE KEEP THAT TO BE INVESTED.

Good article .one can aim 100 cr/50 cr/25 cr/10 cr/5 cr according his/her wish.it is a motivation.thanks!

Dear Varadarajan,

Pleasure 🙂

Dear Basu Sir,

In india inflation is so high, that Inflation compounding is more than investment compounding. so 10 lakh today will be 100 crore after 60 years. Instead we need to teach kids how to be wise and brave to earn their own rather than creating asset for them. I hope you agree.

In the developed counties like UK and US hardly there is an inflation of 0.3%/year.

Thanks

Dear Prashanth,

Here, I am not pointing to create retirement corpus for your kids nor I am saying they depend on you forever. But I am explaining the importance of compounding. How you take is left with you.

Dear Basu Sir,

Thanks for your reply.

Agree with you.

Sir in India inflation and interest even after balancing in Debt and Equity is almost same, in this situation would investment make any sense ? I just want to know your views sir.

Thanks

Dear Prasanth,

In the long run, beating inflation is the main idea. At the same time, it does not mean I take an undue risk by throwing an idea of asset allocation. Preserving capital along with taking calculated risk of generating 1% more than inflation is enough for me.

Well explained the investment principles.

Dear Sarvesh,

Pleasure 🙂

There is no real ‘compounding’ in market products, it’s only related for the sake of representing the asset growth.

Dear Rathesh,

I am not pointing COMPOUNDING only available in MARKET.

Good example of how to create wealth in the long run. However the issue is the human behaviour and circumstances which is not allowing him to hold the investment for so long term. History says that he one generation’s effort will benefit the upcoming generation. So iF you want to pass on a good fortune to your next generation, systematic investment is a key..

Dear Vishal,

Thanks for sharing your views.