Let us say you took home loan 2 years back and suddenly you received some unexpected cash which may be around 10% to 20% of your home loan principal. You paid this amount towards your outstanding home loan to ease your EMI burden. But after few months once again you need the cash of what you paid to your home loan, then how to get and where to find such huge cash needs urgently? Either you need to take home equity loan or search for any other source to fulfill your needs.

To avoid such compulsions and use your idle amount to reduce your loan too, few banks in India offering the type of home loans called “Home Saver Loans”. In such type of loans usually your bank account (Usually non saving accounts like current account or Overdraft accounts-means no interest on idle amount) is connected to the loan account. Whenever you park more than your EMI amount for that particular month then that amount will be treated as payment towards Principal for that particular month. Your EMI will be same as usual but as principal will be less than the usual principal balance, interest part too will be less. So the remaining EMI part will be get adjusted to principal which get reduced and considered as next month’s principal. Confusing??

Suppose you have loan of Rs.50,00,000 tenure 20 years and rate of interest 9%. Now the EMI for the first month will be Rs. 44,986. In this interest part will be Rs.37,500 and principal will be Rs.7,486 and outstanding loan will be Rs. 49,92,514. Now next month beginning you parked around Rs.10,00,000 into the connected account to reduce your loan burden then next month EMI too will be Rs.44,986. But your outstanding principal for the next month interest calculation will be Rs. 39,84,971 instead of usual Rs.49,84,971. So saving will be one months interest on Rs.10,00,000 loan. Below I showed you different scenarios to make you familiar with this concept.

Let us take example where if Mr.X took home loan of Rs.50,00,000 for the tenure of 15 years and interest for normal loans we consider as 8.5% but for home saver loan we consider as 9% (usually home saver loans have higher interest of around 0.5% to 1% than normal home loans). Let us see the difference between two if in home saver loan option Mr.X start to park in the beginning of the month Rs.10,000 till the loan get fully paid off.

From the above table you noticed that Rs.19,82,914 saved by opting the Home Saver Loan with the option of parking monthly Rs.10,000 into savings account.

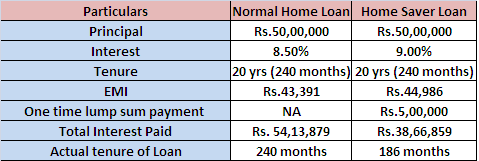

Let us take another case where Mr.X parked around Rs.5,00,000 lump sum after into his savings account till the loan amount totally get paid off.

Total saving of interest will be Rs.15,47,020.

Total saving of interest will be Rs.15,47,020.

I showed above examples where Mr.X paid either monthly payment or lump sum at the beginning of the loan disbursement to make it simpler for you. But in practical this may not the case. In such situations monthly average balance on your savings account will be calculated and adjusted towards the principal for that month.

Let us see few of the advantages of Home Saver Loans.

1) This facility makes you to earn more than your savings account interest rate as indirectly it will be taken as principal towards your home loan which have higher interest rate than normal savings account.

2) If you have surplus cash then it really helps you to reduce your EMI burden in advance.

3) It makes sense to deposit your surplus in this account and take the benefit of lower EMI and withdraw it back when you actually need without any hurdle.

4) This type loan is usually suited to business class or self employed who expects large cash and same can be parked in this account and withdraw it immediately when they need.

5) For salaried people to pay monthly EMI and above that to park cash in this account may not possible. Hence depending on your requirement it is better to go for this type of loans.

Now few advantages of this type of loan schemes.

1) Eventhough in plain it looks simple calculation, but for layman it is bit difficult to understand how their banker calculates and get benefit him or her.

2) Interest rates will usually be higher than normal home loans.

3) Only few banks offer such type of loans.

4) Usually such type loans available on floating rate base instead fixed rate.

Products available as of now for customers are SBI MaxGain, IDBI Home Saver Home Loan, Citibank Home Credit, HSBC Smart Loan and Standard Chartered Home Saver.

Hi Bhavesh,

I have a question. In such a loan, if I have a loan of 50L and park 50L in there, will they deduct the same amount and put more towards the principal or will the monthly payment come down (and keep the tenure the same).

Dear Tarun,

EMI will continue as usual.

Dear Basu

I have taken 1.6 Cr from IDBI interest saver home loan product , but I am thinking of SBI maxigain , what is your suggestion, when you compare which product is more beneficial. please advise

Thank Q

SivaSankar-Both are interest saver home loan products. You can chose anyone as per your convenient. Compare interest rate and comfort with bank. Based on that you can decide.

Dear Basu ,

I have home loan (48,30,000= 41 lakh + 7,30,000 top up loan) from IDBI. Could you please suggest whether I should go for IDBI home loan Interest saver to park surplus in current account and get benefited.

Also is there any condition/criteria of having minimum balance or number of amount tobe parked limit. I had word with bank and they are saying they would charge 0.50% processing charges for this scheme.

Could you please put more light on this case.

Rasik-It is best if you are expecting any surplus during loan tenure. But regarding conditions and interest rate facilities, contact the bank ONLY.

Hi Basu,

I am planning to transfer my existing loan with LIC having fixed interest rate for 3years(now getting into into Floating mode) to Interest Saver Scheme.I can contribute 10K to the Current account of the Interest Saver Scheme.

Please suggest me which one to choose other than SBI Max gain.

Also would like to know

1. Is all banks facilitates TOP up loan

2. Is there any hidden charegs, annual charges & preclosure charges

3. Is there any other different clause/ terms & conditions when compared to standard Home Loan?

Thanks

Aravind

Aravind-1) Yes, usually all lenders offer top-up loans.

2) For which loan? There will be processing charges and no preclosure charges.

3) Nothing special, but you can look at the documents before signing.

Dear Basu ,

I have been reading your blogs from a month now ,almost , trust me , it was so useful and i am making sure if i can read all your archives on a daily basis or on weekends to learn more on finance and investent – thanks for assistance and great work going ,please continue this…

was trying to browse and search for a specific content on the below home loan products, could not find .

I am trying for a home loan currently and had chosen some products across the banks.

Need Your Advise on choosing the best and Safe Home loan Product at present.

1)Axis Bank – 20 Year tenure -Fixed interest Home Loan -10.40%

2)SBI- Max Gain- floating 10.15% , 20 year tenure .

I am personally fond of the AXIS bank product – fixed for 20 years with 10.40 % ,so that i can plan my monthly budget with no surprises on raising interest rates ,although i have to forget the loss if the interest rate goes further down . but I am little suspicious on this product especially 20year fixed , no bank had dared or taken such a risky step

below queries .

1. is this a guaranteed product(axis bank fixed interest for 20 yrs) which actually does what it says , or is there any hidden agenda or hidden clause which i may over look in this product and suffer in future. ? -any suggestion on this product , can i go for this ?.

2. are there any forums or customer feedbacks/firsthand users experience on this specific product of Axis bank (axis bank fixed interest for 20 yrs). i did search for reviews on this specific product ( bankbazaar) and even in your blogs , no luck! – any links you could suggest to chck this product real performance.

3. if the above product is not guaranteed on what is told as , then i am planning for SBI Max Gain product .

4. please suggest , your advise is most help at this point . you can also other good home loan products as per your experience .

Deepak-Fond of Axis Bank is another thing and feaure of loan to your finance is different. You have gone through SBI Max Gain? To me this is attractive than fixed interest Axis Bank Home Loan. The problem with fixed interest loan is, you are on sword edge. Don’t know whether it benefits or loss you because it all depends on future interest rate cycle. In my view consider SBI.

Nice Post

Parie-Pleasure 🙂