Recently LIC launched one more pension plan called Jeevan Shanti. However, what is the difference between LIC’s Jeevan Shanti Vs Jeevan Akshay VI? Because both are LIC’s pension plans. But meant for the different purpose. Hence, let us understand the differences.

Before jumping into understanding these two plans, first understand the basics of pension or retirement plans.

What is the meaning of annuity?

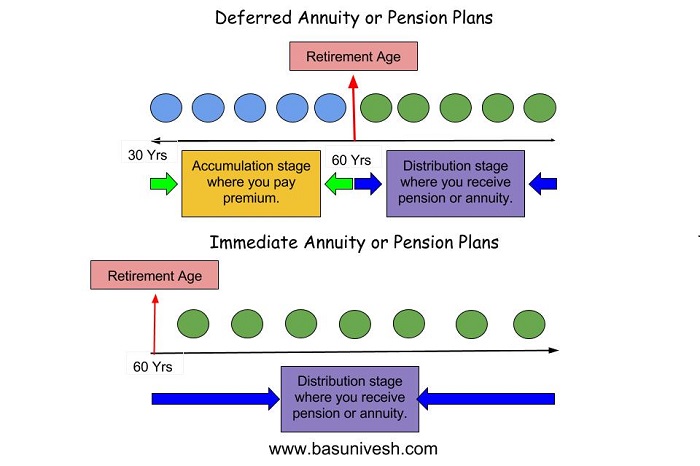

In simple term, you can say it as a Pension, where you will get regular income up to the specified period or conditions. There are two types of annuity.

1) Immediate Annuity-In this case, you invest a lump sum in a product and your pension or annuity starts immediately. Let us say you have around Rs.1 Cr and if you buy immediate annuity plans, then the pension will start immediately from next month.

2) Deferred Annuity-In this case your annuity starts after a certain period. Let us say your current age is 30 years and you are planning to retire at the age of 60 years. If you buy a deferred annuity plan, then you will invest up to your retirement age i.e. up to 60 years of age. After 60 years of retirement, your pension will start.

I tried to explain the same with below illustration as below.

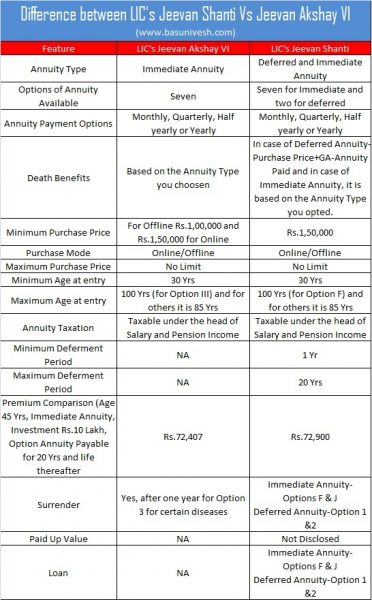

The difference between LIC’s Jeevan Shanti Vs Jeevan Akshay VI

Now let us come to the main topic of this blog to understand the difference between LIC’s Jeevan Shanti Vs Jeevan Akshay VI.

When you look at above comparison, you noticed that there are no such differences when it comes to features. LIC was in need of deferred single premium annuity plan. Hence, they launched it.

However, if you look at annuity rates, I felt Jeevan Shanti offers you better returns than Jeevan Akshay VI. One more big difference is the surrender option. You notice that in case of Jeevan Akshay VI, you can surrender it only if you opted the Option 3 and also suffering from certain diseases. However, no such health restrictions are not mentioned in case of Jeevan Shanti.

Also, under Jeevan Shanti, one can surrender it (If you opted for Options F and J) after the three months of the policy period. However, in the case of Jeevan Akshay VI, it is after one year.

Hence, considering more options, high annuity rate than Jeevan Akshay VI (I cross-checked only with one option) and easy liquidity option in terms of surrender, I feel Jeevan Shanti a better choice than Jeevan Akshay VI.

Please note that the above comparison is based on basic and main features of both the plans. However, for a better understanding of the products, refer below posts and then take your own decision.

- Jeevan Akshay VI – LIC’s Single Premium Pension Plan Reintroduced

- LIC Jeevan Shanti – Single Premium Guaranteed Pension Plan Features, Benefits and Review

Hello Basavraj

The comparison you have given above is quite useful. I tried to simulate given scenario with LIC https://ebiz.licindia.in/D2CPM website and observed that the annuity for jeevan shanti 72900 is correct as you mentioned in your above table but for same scenario annuity for Jeevan akshay is coming 74444 which is not matching with your value. And this seems higher than Jeevan shanti.

Am I missing something?

Also Jeevan akshay is still seen available to buy on LIC online website . But LIC agent was telling that its withdrawn ..Any idea?

Thanks

-Janu

Dear Janu,

I am not sure about the difference. Because I have written this post based on what I got as a premium from their website.

Thanks lot Basavaraj Sir .

Very informative blog .

VAKHARIA M J

Dear Vakharia,

Pleasure 🙂

Very informative blog indeed . Just one query Are the returns tax free for jeevan shanti?

Dear Rekha,

NO. Because currently the pension is considered as taxable income like Salary.

Under Jeevan Shanthi LIC policy is the single premium amount is returnable after the expiry of the term?

Dear Banu,

YES.

Can Jeevan Akshay VI policy be surrendered under Option F? If so, after how long? What will be the Surrender Value? 100%?

Dear Mahesh,

Refer my post on this “Jeevan Akshay VI – LIC’s Single Premium Pension Plan Reintroduced“.

Sir, i want to start Jeevan Tarun policy for my daughter and her age is 3 yrs at present and for Sum Assured which cost around 27000 /- premium per year. Should i go with it or no. Sir if any other better option you have than plz suggest me.plz sir

Dear Rajesh,

Life Insurance is not required for HER. It is required for her (I mean PURE TERM LIFE INSURANCE but not such bundled savings and investment products).

is putting money in jeevan shanti better than keeping it as fd?

Dear Chatterjee,

Both are different products for different need. Don’t compare both.

hello Basu,

I have invested as follow in LIC and want to get rid of all those plan. what is the procedure and how much will i get approx. if surrender those plan?

1. Jeevan mitra triple cover

Premium Paying Term : 30 Yrs

Installment Premium : ? 1,12,967.00

Commencement Date : 28/04/2013

accrued bonus so far : 5,25000

2. Jeevan Saral

Premium Paying Term : 30 Yrs

Installment Premium : ? 60,050.00

Commencement Date : 28/04/2013

thank you,

Dnyanesh

Dear Dnyanesh,

Please contact the nearest branch for the values.

Sir my papa had made lic Investment JEEVAN SURKSHA in 2001 and on 1-jan-19 it will mature. Plz guide me whether my papa will get pension according to his policy doc s. Or his plan will be converted in jiwan dhara/jiwan akshay. If possible put all details of jeewan surksha and current rules applied… Thx

Dear Nirav,

He will get the benefits as it is mentioned in Jeevan Suraksha Plan.

Thanks for good information as always. There is another Good article to understand jeevan shanti. May be helpful to people who wants to take decision on buying it: https://www.moneylife.in/article/lic-jeevan-shanti-another-case-of-mis-selling/55730.html

what is the expect rate of return if I invest 5 lakhs in jeevan shanti?

Dear SB,

It depends on the age and the option of annuity you choose.

Jeevan Akshay VI has higher annuity rate. Please check and confirm. Premium for Jeevan Shanti is higher for the same amount.

Dear Mohit,

I checked on LIC portal for same data of a person and based on that I wrote this.

Doesnt matter we need to understand logic with an example as provided you…then take one’s one case calculate for his age, years, conditions etc and then decide. Thanks for writing such articles. High appreciated