What are the Budget 2023 – 12 Key highlights which are going to impact our personal financial life? Let me list them and try to understand them in detail.

Budget 2023 – 12 Key highlights impacting personal finance

# Mahila Samman Savings Certificate

To empower women, a one-time new small savings scheme called as “Mahila Samman Savings Certificate” is launched. It will be made available for a two-year period up to 31st March 2025. Women or girl child can invest up to Rs.2,00,000 in this scheme. The tenure of the deposit will be 2 years and will have a fixed interest rate of 7.55. A partial withdrawal facility is also available.

# Senior Citizen Savings Scheme (SCSS) limit enhanced

Currently, the maximum limit for Senior Citizen Savings Scheme or SCSS limit is Rs.15 lakh. This is now enhanced to Rs.30 lakh. This I think is a big booster for senior citizens.

Read a full article about the SCSS scheme at “Post Office Senior Citizen Scheme (SCSS)-Benefits and Interest Rate“.

# Post Office Monthly Income Scheme (MIS) limit enhanced

The current limit for the Post Office MIS scheme is Rs.4.5 lakh for individuals and Rs.9 lakh for joint accounts. This limit is now increased to Rs.9 lakh and Rs.15 lakh respectively.

By this, you may assume that with the rate of individual accounts increased, the joint accounts should be around Rs.18 lakh (double of the earlier limit). However, the government restricted it to Rs.15 lakh.

But still, I feel this is a fantastic move as it is a huge relief for many investors who rely on such government, safe, and fixed-income products.

Read more about Post Office MIS at “Post Office Monthly Income Scheme or MIS – A complete guide“.

# Sec.54 and Sec.54F exemption limit is capped

Earlier under Sec.54, and Sec.54F, there was no such amount-based cap. However, now it is Rs.10 Cr.

# TDS on EPF withdrawal is reduced

Earlier during the withdrawal of EPF (within 5 years), if you do not provide a PAN number, then the TDS was at 30%. Now it is reduced to 20%.

Refer to our earlier post on this aspect at “EPF Withdrawal Taxation-New TDS (Tax Deducted at Source) Rules“.

# No Tax on up to an income of Rs.7 Lakh of income under the new tax regime

Earlier, the rebate under Sec.87A was up to Rs.5 lakh. This is now enhanced to Rs.7 Lakh. Hence, if your income is below Rs.7 lakh and opting for new tax regime, then you no need to pay the tax.

Refer the detailed post on this “Section 87A – How is income up to seven lakhs tax-free?“.

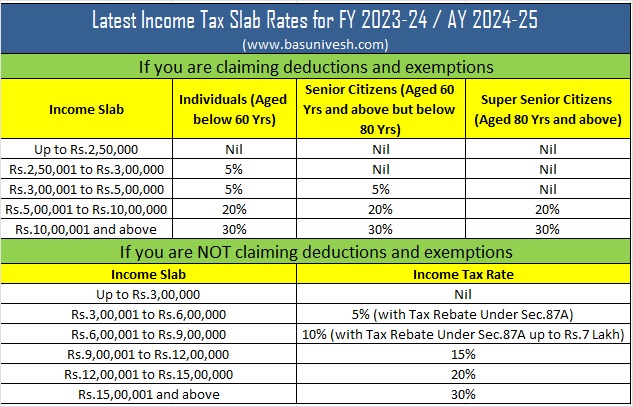

# Tax rates changed under the new tax regime (no change in the old tax regime)

Earlier, under the new tax regime, there were 6 tax slabs starting from Rs.2.5 lakh. Now the number of tax slabs under the new tax regime is reduced to 5. They are as below. Do remember that there is no change in the old tax regime.

The latest Income Tax Slab Rates for FY 2023-24 / AY 2024-25 are as below.

Refer a detailed post on this aspect at “Revised Latest Income Tax Slab Rates FY 2023-24“.

# Introduction of standard deduction under the new tax regime

Currently, the standard deduction offered under Section 16 of the Income Tax Act is a flat deduction of Rs. 50,000 on the taxable income of salaried employees and pensioners irrespective of their earnings..

However, from 1st April 2023, the benefit of the standard deduction of Rs.50,000 is applicable to the new tax regime too.

# Surcharge for those whose income is above Rs.5 Cr is reduced

Earlier the surcharge on those individuals whose income is more than Rs.5 Cr was 37%. This is now reduced to 25%. Based on this the effective tax rate was reduced from earlier 42.74% to 39%.

# Leave Encashment limit is increased to 25 Lakh

Earlier encashment of earned leave up to 10 months of average salary, at the time of retirement in case of an employee (other than an employee of the Central Government or State Government) was exempt under Sec.10(10AA) as below (lowest).

- Rs. 3 lakh

- Actual leave encashment amount

- Average salary (basic salary + dearness allowance) of the last 10 months before the employee’s retirement or resignation

- Cash equivalent of pending leave days. The leave basis is a maximum of 30 days leave for every year of service.

Now, this limit of Rs.3 lakh is increased to Rs.25 lakh.

# TDS on interest income of NCDs

“It is proposed to withdraw the exemption from TDS currently available on interest payment on listed debentures.”.

Earlier the interest you receive from the listed NCDs is exempt from TDS. However, you have to pay the tax as per your income tax slab. This exemption is now removed. Hence, you will receive the interest post-TDS.

# Traditional Life Insurance policies where the premium is more than 5 lahks are not tax-free

“It is proposed to provide that where the aggregate of premium for life insurance policies (other than ULIP) issued on or after 1st April 2023 is above Rs.5 lakh, income from only those policies with aggregate premium up to Rs.5 lakh shall be exempt. This will not affect the tax exemption provided to the amount received on the death of the person insured. It will also not affect insurance policies issued till 31st March, 2023.

This I think a big jolt to insurance companies.

Conclusion – Considering all these, we can assume that the government in one way aggressively pushing for adopting the new tax regime. I hope the message is clear to all of us. This post is updated with the limited information available as of now. However, as and when I get the clarity, I will update this post.

Hi Sir,

The tax rules still allows deduction on interest paid towards loan on a rented property under section 24(b) max 2 Lakhs.

Is this still applicable in new Tax regime? What are the deductions allowed other than Standard deduction in general?

https://www.livemint.com/money/personal-finance/switching-to-new-tax-regime-you-can-still-claim-deduction-on-home-loan-interest-11635249674520.html

Dear Mani,

Refer my earlier post “List of Income Tax Deductions FY 2020-21 – Under New / Old Tax Regime“.

Thank you, Sir.

In the above post, section 24 (b) for the let-out property has been mentioned under Deductions under Old regime. But in the livemint article I have shared says that Under New regime too, we are allowed to claim max 2 Lakhs deduction on interest paid towards loan on a rented property under section 24(b).

Is it correct one?

Dear Manimekalai,

I don’t think so. Or I am missing something? I have to check the ITR website rather than relying on media.

Standard Deduction of 52500 is only on Salary Income above 15.5 Lakh, according to this article.

What if a person’s Salary is 5 lakh but Gross Income from all sources is above 15.5 lakh? Does he get the Standard Deduction of 52500?

Dear Sir,

There is no mention of Rs.15.5 lakh in Budget speech or Finance Bill. I am not sure from where this Rs.15.5 lakh is popping up.

Personally with my limited financial knowledge and being already in New Tax Regime, I feel i will save roughly 50k from Tax. Those who are already under new tax regime stands to benefit.

Dear Narayanan,

New tax regime is future 🙂

People living in metro cities earning more than 15 lakhs (though as per the standard of living it is not high income) still required to pay more tax in new tax regime compare to old tax regime. And no benefit to Old tax regime tax payers.

Though I’m big fan of Modi Ji, but feeling like cheated in every finance budget, now I’ll caste my vote to Congress.

Dear Nitesh,

The idea is to force you towards new tax regime.