Confession time: The first time I learned about the markets was when I was 16. My father came home and said he had made 3000 from an ICICI script that shot up within a month and he wanted to celebrate. We went for a dinner and had some of my favorites – Biryani and Kadai.

The next day, looking like the very eager beaver, I jumped on the internet and googled about the stock market. What I saw next befuddled me. There were 256 websites doling out stock tips for the day and this was just until my patience had run out. I told my father that stocks confuse me but he didn’t teach me much because he didn’t know much. And so I googled, on and off for a further 4 years.

When I was trying to learn about money, the topics often delved deep into the concepts of IT returns, cashback and EPF calculators. Throw in some befuddling mutual funds, companies that propagate confusing info to reap better profits, you get Google searches that brain-drain even the best among us. But then,

- What if there was a way to stay away from all that information consumption and still be the star you always dreamed you could be?

- What if there was one direct answer as to how you should handle your money?

- What if in this post, I showed you what the simplification is and how to simplify your money life?

Would you take action upon reading or simply roll over to another tab? Decide the person you’d like to be and from this moment, you’ll be the cynosure of envy because, you actually have time to spend on things you love (aka kids, sports, travel etc.)

If you’ve nodded in the affirmative, this simplification process isn’t going to ask you to save more nor count your pennies. In fact, you are encouraged to spend on everything you like (just one at a time though).

Upon reading, you will have a new lease of life because this question no longer hangs above your head: “Am I spending too much? Should I save more?” You’ll know exactly what you are doing and be confident with every money decision you take.

Let’s dive in.

I’ve believed in two things when it comes to personal finance:

- Never go into debt for something that will depreciate (vacations, electronics, car etc.)

- Pre-plan and allocate cash-flow to run on automatic.

When it comes to thumb rules, many authors write down several must-follow rules. Beyond the above two, there’s just one more after which I promise I’ll tap out. You will roll your eyes when reading this because you might have heard it a million times but pay-yourself-first is a great concept. To the uninitiated, ‘pay-yourself-first’ means you identify which big goals (retirement, child’s college, a home etc.) you’d like to achieve in the future and invest toward them. The difference is: you invest towards it immediately after the salary hits your bank account.

The way to do this is inculcated a ‘Conscious Spending Plan’. CSP is about having a mental map of your money allocation like Sherlock Holmes. This way, you know you’re not forfeiting the future by overspending now or you’re frugal’ing too much and giving the future overdue importance. Dear astonishingly attractive reader, welcome to the world of ‘Conscious Spending’.

The Conscious Spending Plan

Conscious spending doesn’t mean looking up card statements at the end of the month. Insofar, as the things related to finance were concerned, they were in the past tense:

- How much did I spend last week?

- How am I going to stop spending so much?

- Is it movies or jeans? Where does all my money go?

From here on, we look forward. We take a glance at the past, slide the sunk costs and charter plans for our future. People become rich in the future because they made plans for it today – exactly what we’re going to do from now. Based on the interests, CSP is going to assign a number to those desires from your salary account. This, in turn, is going to help us live our version of the Rich-Life.

A few of my friends actively live the rich life: they were brave in choosing the things they loved and mercilessly gave up the things they didn’t care about. Their modus operandi to a rich life goes like this: “I have automated my savings/ investments. What remains, I spend carelessly and I live without any guilt of not being good with my money”. Once they had attained a control over the things they valued most and invested toward their big expenditures, Living the Rich Life seemed easy.

Here are a couple of examples of my friends who massively conscious-spend but have no regrets over the way money is spent.

How Gopal can afford 3 bikes on a 30,000 salary

When he first told me that he was going to buy a Yamaha Yezdi as his 3rd bike, I choked and blurted, “ARE YOU INSANE?” (exactly what you’d have said too). He already had a vintage and also a Duke that consumed petrol like a thirsty cricketer on a dry summer day. When a group of friends and I questioned the logic behind the purchase he had nothing to say. In fact, he had pre-planned investments toward retirement with his company’s provident funds and some more with index funds. To top it all, he had saved for buying the Yezdi by giving up on eating out for four months. On the surface, buying the Yezdi looked like a stupid decision, but was a result of pre-planned conscious spending.

How Monisha can afford 15,000 on make-up on a 45,000 salary

Monisha comes from a long family line of ‘men go to work, women take care of the household’. This meant, her father never expected her to work or provide anything for the family. And that left her to expend every inch of the salary she was earning. Upon graduating, she got into marketing at a top tier firm and that resulted in hanging out at Starbucks more often than she’d have liked.

Being presentable was seen in her industry as a great way to position yourself and she started getting a taste for 2,000? lip garnishments. A couple of years later, her father asked Monisha to save toward her wedding. She agreed instantly, as up until then she wasn’t saving anything and it seemed like a good idea.

Then over time, slowly, the saving request progressed to buying a flat in the city for her to live-in after marriage. She kept her head down and plodded along. Right now, 3 years later, she keeps up her expensive lifestyle with aplomb while simultaneously funding her father’s demands in equal measure. Like many daddy’s daughters, the moment her salary gets credited, she transfers 20,000 to her father who takes care of the saving/ investment part. Whatever remains, she spends as erratic as rainfall during a non-Monsoon month.

My friends are an exception few that have sorted out their heads around the financial mess young people get entangled in. What they did well, is they paid-themselves-first or their futures first and then moved over to spending. Maybe they differed in amounts and instruments they used for investments, but they did have a head-start. While that may not be much, it still is a desirable position for many of us.

Here’s what they’re doing good:

- They’re clear on the things they like.

- They know what their big goals (money-wise) in life are and fund them.

- Spending comes only after investments and savings.

A simplified equation to replicate their rich life is

Salary = Investments-Savings-Expenditure

The explanation: When the salary hits your account, fund the future investments first. Then, take care of saving for short-term expenses such as vacations and down-payment for a home. Finally, only after you’ve taken care of the future, expend whatever you have, irrationally.

The reason that I write ‘irrational spend’ is because it can be as varied as possible. January might be f

for paying gym subscriptions after New Year resolutions, while February might be for canceling gym accounts and buying a new cycle. Each month is different to another and that’s why we allocate resources for irrational spending.

While looking up on info for ‘how to make the most of debt funds’ or ‘CAGR to expect for various instruments’, they’re more of theoretical learnings. They are easier compared to what we’re looking to do right now, as this involves human psychology with money. If you’ve mastered this simple aspect, you’re on the path to money stardom.

# Initial 20% of effort and time taken

- Fund your retirement and big expenses in future.

- Save toward short-term goals (down payment) and repetitive expenses (Diwali and other festivals).

# Remaining 80% of time and effort

- Spend it irrationally. Just make sure to last through the month.

This approach gives us a great head-start but we’re not there yet. To get there (pro level), we must take it a step further and divide the Cashflow into a few divisions.

Establishing the cash flow

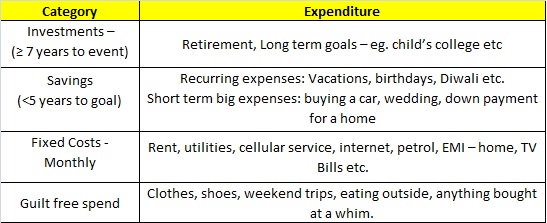

The cash flow will majorly involve four partitions:

- Inescapable fixed costs

- Investments

- Savings

- Guilt free spending

1) Inescapable fixed costs

Fixed costs are the damage triangle: rent, transport, nd food.

- The rent on a PG or the EMI of the home that you inhabit is an inescapable cost.

- At the same time, the transportation costs depend on how you commute to the office.

- While eating outcomes under guilt free spend, having three meals a day is a pretty default. A basic percentage of your salary must go toward consuming food and that is the fixed cost we’re talking about.

- Other fixed costs are monthly bills such as mobile phone, credit card balance, the internet, utilities etc.

We know that budgeting sucks and maintaining a scorecard is like acid rain on your brain. But combing through the finances once in 3 months shows that you’re serious about living the rich life. The simplest way to do this is to open the bank statements and record what you see into a back of napkin calculation. It provides a decent amount of accuracy of your expenses and that’s 85% of the job done (remember, 85% done is very well done).

Once you finish, add a couple of thousands (or 10% of your salary) to that amount for expenses such as bike repair, new mobile etc. These expenses come with a longer timescale regularity but do not come in monthly repetition. When you divide these expenses into a monthly timeframe we usually get 2000 as its monthly equivalent.

In personal finance, there are no hard and fast rules and personalizing it to each individual is the fascinating part. But maintaining these costs within the confines of 40-65% of your total salary is an indicator of healthy management. As you finish adding a couple of thousands, minus this total amount from your take home pay. The amount that remains is for investing, saving and spending.

2) Investments

Basu’s blog dives into depth about the instruments to use for investing. Right now, though, we’ll identify which goals demand more importance and the cash flow percentage you’d like to allocate toward that.

Why is retirement a big deal?

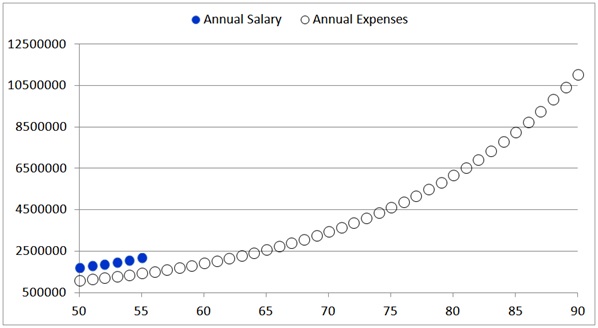

Let’s say you are a 25-year-old earning 5 Lakhs a year and spending half of that toward essential needs. If we assume your salary will increase at a conservative rate of 5% a year and your expenses at 6% (possibly an underestimate), this is how they will pan out in future.

If we assume you no longer wish to work after age 55, then your ledger will look like this.

Notice that your expenses will not stop when your income stops. They are going to continue till the day you die (we have only considered your present essential expenses, new such expenses will come – car, EMI, a school for the child as you age).

Retirement is a big deal because your income drops to zero while inflation keeps rising every year. Unless you have assured means to generate income that keeps up for essential expenses and medical emergencies, you will have to continue working or depend on your relatives/friends. Now, nobody wants that! With the previous generation, post-retirement income typically meant a pension. And pensions were a flat income – the equivalent of about 50-60% from the last drawn salary. If you pan it across the same chart, pensions will not be enough to cover the expenses the very next year.

As you can see above, pensions are clearly insufficient. While the minimum post-retirement income should match your expenses, we must be prudent to cover for unexpected medical emergencies as well. This means that the income post-retirement must increase at the rate at which your expenses do. In other words: an inflation-protected income.

Since no ‘pension plans’ will provide you with inflation matching income, we have to invest toward it. We must invest right, invest early and create a finite corpus from which we can draw inflation-adjusted income in perpetuity.

Similarly, by investing early, we can fund any future big expenses. For example, you could have children and their school expenses, college expenses can be invested toward by utilizing time factor of compound interest. Maybe you wish to get an expensive car, or take a long international holiday – any financial goal can be invested toward if we plan and make contributions early.

Juggling all these priorities from the onset is not possible. Moreover, this kind of complexity often leads to inaction. In investing jargon, ‘time wasted due to inaction is like sitting on a gold-mine but waiting for a shovel’. You can start dirty by digging with your hands and focus on just one goal: retirement. As you plod through, you can acquire the tools and balance various priorities.

Personal finance writers believe 10% of your income is a good amount for investments. Again, if you figure you’d give more importance to future goals over current expenses, you can buck the trend. In fact, you can make investing as much as 30% of your monthly paycheck, as I’ve often done in conducive times.

In 2017, my investment portion is in high 40 percentiles

When you’ve shortlisted the major goals you’d like to invest in and then proceeded to fund them, what remains from your monthly salary is for short-term savings and finally current expenses.

3) Savings

Often misunderstood and misinterpreted with investing, we save in places where we should have been investing in the first place. To avoid this mistake, the savings bucket can be categorized into two: Short Term Goals and Recurring Expenses.

Expenses that are recurring every year (Diwali, NY bash, vacation) come under the recurring expenses umbrella. We will save toward these expenses by opening separate RD’s in their name drawing from your salary account.

Short-term goals such as a car, downpayment for a home, your wedding come under this umbrella. While these are not repetitive, they are forecast to happen a few years down the line. The reason we don’t invest in the equity market for these goals is because they’re too near. Returns over the short term in equity is not guaranteed and that’s why we save under the safer neighborhood of a Bank’s RD. The returns are definite, risk is negligible and we can save with precision.

To differentiate short-term goals from long-term, take the golden number as 5 years. If your goal is only 5 years away, save using a bank’s RD. If longer, always invest some portion in the equity market. (reasons have been explained in-depth before – here and here)

Now, as you’ve detailed into the saving bucket, you can allocate the percentage to each goal. Depending on the importance you have for each expense, you can divvy the amount accordingly.

From the monthly salary, as you take out fixed costs, investments and small-term savings, the balance remains for irrational expenditure – FINALLY!

4) Guilt free spending

Imagine the feeling you’d have when someone gives you money with no chip on your shoulder: No worries over the future nor any pre-determined commitments to fulfill (ex: parents’ home loan). This is guilt free spending.

You could take the money, buy shoes, or you could do an impromptu bike trip. You could do peanut butter fingers all night, every night or slam-chow cheese pizzas at will. Whatever you do, this question no longer hangs over your head: ‘Am I spending too much?’ The feeling of having money that I can spend irrationally sometimes makes me the happiest person on earth. You could feel the same if you’ve followed the money allocation process:

Salary = Fixed costs – Investments – savings – expenditure

Being brought up in a middle-class environment made me acutely aware that there is some responsibility perennially hanging over one’s head. As I grew up, my mom had to keep working to keep me educated. As time progressed she wanted something for herself but it wasn’t possible always.

An impulsive purchase or miscalculated expenditure stung for days. Seeing what my parents had been through made me realize that having some amount for irrational expenditure is a saner version of living life. Funding my future needs first, I could rely on this feeling of being assured for the remainder of the month. This sort of represented, that I have done my homework before I spent the evening at the park.

Most of the friends I know have kept 15 percent to guilt-free spending. But you can accord this portion depending on your conscious spending plan.

To sum up, your monthly money table will look like this.

As we’ve looked at the theory of simplifying finances, let’s dive into a real life example

Recent Example: Ashwath was a classmate of mine with whom I walked through the 4-bucket system. I told him about the next-100 idea. He asked me what it meant and I replied: “It means you know where the next 100 is going to go.” He decided to allocate his salary in terms of % as below.

Per his next-100 breakdown, 15 would be toward fixed costs like car EMI and petrol. He doesn’t have more fixed costs because he stays at home with his parents and has no student debt. With his investments, 5 goes toward the employer match EPF and another 5 toward a Nifty 50 Index fund for retirement. 30 of savings splits between 25 for a house downpayment and 5 for Himalayan trekking expeditions that he does every year. The remaining portion of 40-50 from guilt free spend gets spent irrationally. When he finished working this out he exclaimed, “Unbelievable!!!” and stopped speaking for a few minutes.

Since he works in technical sales at Saint-Gobain, he gets to travel a lot and eating out is his second giving of life. To impress clients, he spends quite a lot on clothes too. When he automated this allocation, it seemed unreal. Previously, he used to do things with money haphazardly. Now, he knows how much he can save, how many designer ties he can buy and how many times he could eat out. Automation made sure the money from the salary account was disbursed into each bucket appropriately without him thinking about it.

After automation, this is how his cash flow works:

- Right when the salary is to be deposited, 5% goes toward the employer EPF match.

- A day later, an additional 5% gets pulled out for investing in a Nifty 50 fund – towards retirement in addition to EPF.

- 3 days later, the fixed costs are paid from the salary account – car EMI (he has a lot of travel).

- 1 day later, he pays the credit card balance for the irrational spend and fuel costs of the previous month.

- The same day, 30% of savings are siphoned – which automatically spread into 25% for home down payment and 5% for vacation treks into 2 separate RD’s.

- Whatever remains, he gets to spend it irrationally. Nominally, he uses a credit card/ Paytm wallet to pay so that he can keep tabs of his financial situation.

When the 20th of the month rolls around, he looks at his bank balance and makes a frugal living for the remainder of the month (if he’s over-spent before).

After he’s automated everything, I’ve seldom heard him say, “It’s the month end and my finances are tight, bro.” In fact, he never cancels on an eating-out plan due to finances and he’s spent a grand total of 1-hour managing money. This is automation at its finest exploitation!

As you’ve automated, the tangible result is: you need less than 5 minutes of work per month and you’ll know how every gear of the bigger machine is working. Now, you could actually dream about spending more time with kids or having bigger vacations – your money life is sorted.

To help you further, we’ve documented the entire journey from being lackluster with money to becoming smart in our book ‘Gamechanger’

The Gamechanger

If you’d like even better tips for how you can leverage cheap travel – flights that just cost 200 from Mumbai to Entebbe, automate your finances and be something of a Jedi-master of money, we’ve compiled everything into 166 pages. Right now, I’ve co-authored a lifestyle book with Pattu of Freefincal that delves into personal finance, cheap travel, credit cards, automation and many more.

Get your copy on Amazon right here. It hit the shelves on June 2nd and is already on it’s way to becoming a best-seller.

If you are ready for some advanced material on travel, make sure to grab a copy of the Ultimate Travel E-Book. It has earned generous praise and people have emailed in saying they’ve secured flights for half the price than they normally find after reading the E-Book.

Don’t wait too long though. Your purchase decision is mightily appreciated!

Note-This is the guest post by Mr.Pranav, the co-author of the book “GameChanger”. Pranav Surya with an MBA in Hospitality & Tourism at Glion & Bachelors in Mechanical Engg. He did a project at Bosch Bangalore which was when he realized engineering wasn’t for him. Upon asking multiple people from different industries, moved into hospitality and tourism and right now have traveled to 9 countries across 3 continents for work and some leisure. He can be found half of the time at Anna Centenary Library in Chennai and the other half traversing across the globe for work.

Disclosure-I am in no way associated with both the authors of this book nor I am benefitted in any way by publishing this guest post. This is purely on knowledge sharing basis. There are no monetary benefits involved in publishing or promoting this book.

Thanks for sharing a nice article. It is very knowledge information to share.

infy is offering share buy back at 1150 on nov1. If i buy infy shares through a broker like fundsindia, how do i offer them to back to infy on nov1? how do i take part in this buyback? is there a any risk for that?

Jerry-I am not direct stock expert.

Hello sir, Thanks for nice article. Recently i was watching a video related to agriculture. The lady who was practicing the agriculture saying that she has splitted the income into daily, weekly, monthly, yearly and future generation income.

Daily income – Selling Hen eggs (100 rs), Milk

Weekly – Greens, Vegetables

Monthly – Paddy, Banana, Fish, Papaya, lemon

Yearly – Lemon, Puppy selling, Hen selling, Goat, Cow and Calf

Future Generation – Teak wood tree

As a salaried person her talk was influenced me lot. Could you please suggest something like this kind of splitted income throughout the year for a salaried person like me. Thanks in advance.

Marimuthu-There are many business which can be run in this way. However, it is hard to say or name one or two. Because even though agriculture seems fancy when we sit in AC Rooms or discuss the things in media, the reality is something different.