How to create ONE CRORE Rupees from EPF? Sounds interesting right? Let us see whether it is possible or not as EPF Is the most ignored investment for many salaried.

Many of us know the power of compounding and also the majority of the salaried are EPF members. Unknowingly they are contributing to EPF as it is deducted from your salary before you get in hand.

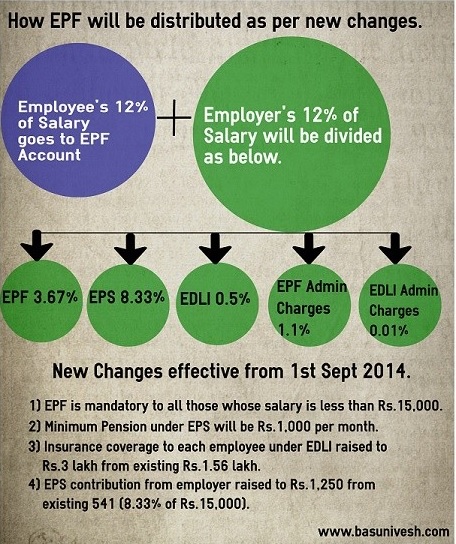

What is EPF or Employee Provident Fund Scheme?

I have written a lot of posts on EPF. However, to simplify how you and your employer contribution will work in this EPF structure, let me share the below image for your reference.

I hope you got a clear idea of how the EPF deduction from your salary and employer contribution is deducted on a monthly basis and get invested.

If you wish to look at the current interest rate or historical interest rates, then refer to my latest post “EPF Interest Rate 2019 – 2020 – Historical interest rates from 1952 to 2019“.

How to create ONE CRORE Rupees from EPF?

Let us move on and understand to create one crore rupees from EPF when you retire. For the accumulation of Rs.1 Crore calculation, I have assumed as below.

Your Salary (Basic+DA)-Rs.20,000 per month, Rate of Interest on EPF-8.5%, your age-25 years (assuming you retire at 55 years of age) and hence you are contributing around 30 years towards EPF, assuming your salary (Basic+DA) increment at 5% yearly. Also, I have assumed that you and your employer are contributing 12% of your salary (Basic+DA) and assumed that you have no prior EPF account (Balance).

If we do this, then we may tabulate the same as below.

If we draw the graph of this EPF accumulation, then it looks like below.

You noticed that for the first 5 years period, you never experience the compounding effect. From 6th to 10 years onwards a slight visibility. However, post 10 years, it is zooming and touching the Rs.1 Cr mark after 30 years.

Conclusion:- You noticed the power of compounding here. It creates the wonder to your wealth creation IF you hold your investments for the long term. Investing for a few years and expecting a compounding effect is MYTH.

Never touch your EPF accumulated corpus unnecessarily like withdrawing when you change the job or withdrawing for house contruction or any other purposes. Let it slowly build your solid retirement corpus. More than that, this retirement corpus is TAX-FREE as of now. Hence, consider EPF as your BEST debt component of retirement funding.

I know that EPF interest rate changes on yearly basis and also, the time horizon to retirement differs from person to person. However, you can still easily accumulate Rs.1 Crore from EPF by increasing your contribution to EPF through VPF. But do remember that EPF is illiquid investment where the liquidity is possible with certain restriction. Hence, use the EPF as certain portion of your debt portfolio of retirement funding.

Refer our latest posts:-

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

Rs 2400 is clear for the first year salary of 20000. But how did you get 1151 (5.7%)? And sharing is still not enables in Quora.

Dear Tej,

May I know which Rs.1,151 you are talking about? You mean to say that you wish to share this post in Quora?

Dear Sir,

My job transferred to abroad and no more working in India and contribution to EPF and VPF has been stopped for last 2 months.

Q1. Am I eligible to withdraw funds completely tax-free ? Note that I worked in India and with this company for only 3 years and reason for withdraw is moving abroad.

Q2. If I wish to continue, can I keep my EPF and VPF account running, without any contribution? If so for how long?

Q3. For how long I will continue to earn interest on my EPF and VPF account?

Q4. Is there a time limit until when I can withdraw my EPF and VPF funds tax-free?

Thanks,

Deep

i started at the age of 33 in paper industry over all 3000/- salary (in 1997) now at present iam drawing 26000/- what may be my result in epf.

Dear Suresh,

Sadly you are looking for readymade answers based on your OWN case. It is hard for me to calculate each individual 🙂

Dear Basu,

I was underestimating my EPF contribution and overestimating power of mutual funds. This article is an eye opener. A question: Can i use VPF as debt component for Children education and children marriage? Is it better than PPF? Howmuch can i invest in EPF per year? May be a detailed post on VPF would be helpful.

Dear Rajnesh,

“A question: Can i use VPF as debt component for Children education and children marriage?”-NO. Keep EPF and VPF as debt part of your retirement goal. For kids debt part, use PPF, SSY (for girl child) or Liquid Fund. “How much can i invest in EPF per year?”-Hard to say as I don’t know the debt part of your retirement goal. Surely, I will try to write a detailed post on VPF.

Thanks for making me to understand the power of compounding in tabular form. Graph which is part of the blog explains everything. Longer you stick to it, compounding benefits results in Wealth Creation & also understood its limitations of Liquidity.

Can you please post a blog on VPF in-detail to have wider view.

Dear Anil,

My pleasure. Sure, I will write on VPF in detail.

hi

My age completed 50 years with 13 years experience and I have no employment since 17th July this year. My understanding is Form 31 and Form 19 both are required for submission .

My question is what about Form 10C and Form 10D ? Should I submit only 10C form or 10D form or both these forms ?

Dear Rajeev,

Use composite claim form.

Thanks for this sir

One question – EPS for Year 1 should be 8.33% of 20,000*12 which is 19,992. Whereas in your calculation you are showing it as 14994. Am I missing something in my calculation ?

Dear Rohith,

The EPS contribution is always either 8.33% of Basic+DA or 8.33% of Rs.15,000 (whichever is lower). Hence, in this case it is Rs.14,994 but 8.33% of Rs.20,000 (Basic+DA).

Sir, how about the EPS be claimed after retirement.

I closed my initial PF account after 7 yrs. But current PF account is active and now I understand the compounding effect.

But how EPS will be calculated? For my previous years of exp when I contributed to Eps and closed it.

Please clarify.

Thanks

Senthil

Dear Senthil,

EPS will not earn any interest.

Hi Sir, ok, but will the EPS calculation will also include the earlier years of experience when I closed the first EPF account?

Dear Senthil,

If you not transferred the EPF but withdrew already, then how can that be counted?

Basavaraj, you should enable sharing your blog posts to Quora also.

Dear Tej,

Sure will do that.

Could you please explain how did you get the number 3551 for Year 1.

Dear Lawish,

12% of Rs.20,000 is Rs.2,400 (employee side) and Rs.1,151 (from employer side) together per month Rs.3,551.

Dear Sir, Thank you very much for the article. It helps to understand the importance of staying invested over the long term.

I have a question. Say I worked for a company (Exempted establishment) for 5 years and my PF balance is X. When I move to another company and I transfer the PF balance from the previous company and the PF contribution in the new company is Y. At the year end, how will the interest be calculated in the new company? Will it be calculated based on (X+Y) or will it be based on Y? Please confirm. Thanks.

Dear Balaji,

It is calculated based on X+Y.