Those who already invested in Franklin India’s six closed Funds, the biggest question for them is when they will get back the money?

As you may be aware, due to the suspension of Franklin Templeton India’s 6 Funds, investors have no choice but to wait for the money to get back. I have written a post on this issue already (You can refer the same at “Franklin Templeton India Closed 6 Debt Funds – Is it right?“.

However, yesterday Franklin Templeton India shared the timeline of approximately when you can expect the money from each of their six funds. Let me share the same.

Franklin India’s six closed Funds – When you will get back the money?

Let me first share the codes and fund names of those six schemes and they are as below.

Scheme Codes and Scheme Names

FIUBF Franklin India Ultra Short Bond Fund (No. of Segregated Portfolios – 1) – (under winding up)

FILDF Franklin India Low Duration Fund (No. of Segregated Portfolios – 2)- (under winding up)

FISTIP Franklin India Short Term Income Plan (No. of Segregated Portfolios – 3)- (under winding up)

FIIOF Franklin India Income Opportunities Fund (No. of Segregated Portfolios – 2) – (under winding up)

FICRF Franklin India Credit Risk Fund (No. of Segregated Portfolios – 3) – (under winding up)

FIDA Franklin India Dynamic Accrual Fund (No. of Segregated Portfolios – 3) – (under winding up)

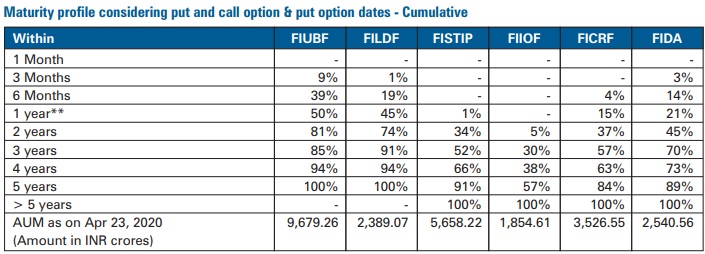

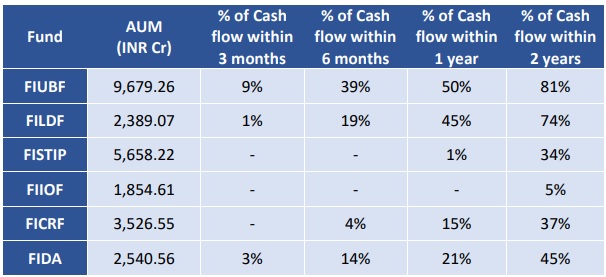

Maturity profile of all these six funds are as below.

You noticed that Franklin India Low Duration and Franklin India Ultra Short Term Debt Funds maturity period is less than 5 years. However, for others, it is beyond five years.

Each fund has its own cash flows and borrowings and therefore will be able to return monies at different points of time. Based on AMC’s best estimate of cash flows at this time, the schemes are expected to return monies as follows:

Franklin India’s six closed Funds – Why such a long wait?

Reason quoted by Franklin India is as below:-

“Before any monies can be returned to unitholders, the borrowing in the fund that was taken in order to fund the heightened levels of redemptions will need to be repaid. Further, due to sustained redemptions, many of the funds were forced to liquidate some of the shorter maturity or more liquid holdings in the portfolio. Both these factors are causing a further delay in how soon we estimate the schemes can return monies to unitholders. As can be seen from the data above, continuing to permit redemptions with high levels of borrowing or selling the shorter maturity or more liquid papers would not have been in the interest of our unitholders. These were also some of the important considerations in making the extremely difficult decision to wind up these funds in order to preserve value for

existing unitholders. While repaying the borrowing does not impact the value of money returned to unitholders, it does delay when we can start to pay out to unitholders.”

Macaulay Duration and it’s real impact on you

Many investors failed to understand the definition of Macaulay Duration in Debt Funds. They have nicely given the explanation.

“The Macaulay Duration reflects the average duration of the bonds held in the portfolio basis the expected cash flows of the bond. A portfolio will typically have an average maturity that is slightly longer than the Macaulay Duration. Hence, for example, in Ultra Short Bond Fund, a Macaulay Duration of 4.53 months means the portfolio has an average maturity of 5.27 months. This indicates, in very broad terms, that this is the mid-point of the maturity dates for the bonds held in the portfolio, not the date for the last maturity in the portfolio. Accordingly, you will see that with a Macaulay duration of 4.53 months, the fund should be able to return around 50% in year 1 and substantial money in 2 years.

Also, for securities with an interest rate reset at periodical intervals which have a floor and cap rate as per the terms of the issuance, the maturity date has been considered for the cash flow projections vis-à-vis the interest reset date which is normally considered in Macaulay duration and valuation by the valuation agencies. Further, this cash flow is after taking into account the fact that initial cash flows received will go towards paying the borrowing in the fund, which delays how soon the schemes can start to return monies to unitholders. It may also be noted that these calculations are on a conservative basis and do not consider any sale or prepayments or coupon payment. It will be the endeavor of the schemes to accelerate these payments through actively seeking pre-payments and opportunities to sell in the market while preserving value for unitholders.”

Franklin India’s six closed schemes – What investors do now?

Unitholders will receive a request to vote electronically on the process of winding up the funds under regulation 41 of SEBI (Mutual Fund) Regulation 1996 to authorize the Trustees, to take steps for winding up of the schemes. Once this

the vote is complete and results notified, the schemes will be able to start monetizing its assets and distributing the investment proceeds in compliance with SEBI regulations.

Conclusion:- Now you got the clarity that when you can expect the money from these 6 closed schemes. Let us wait for the action.

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

Hi Basu sir,

I saw in NSE website SBIN-N5 series has a coupon rate of 9.95% maturing in March 2026. I believe the current yield would be around 8.9%. Will it be a good investment if i can hold it till maturity? Can you throw us some light on buying bank bonds? If you can write an article on how to buy bank bonds, what are the types of bank bonds, advantages and risks?

Dear Vignesh,

Wait for my next post.

Thank you very much sir!!

Dear Vignesh,

Refer my latest post. I just wrote it.

Dear Basavaraj,

Now that Ultra short fund is blocked for uncertain time and also my other fund like HDFC balanced/hybrid is also taking a huge beating and dwindling of accumulated corpus from last 9 years, kindly advise should I go for redemption option for considerable amount but with still continuing SIP or take a pause and stop even SIP for some time to come?

Dear Saleem,

Debt Fund issue is different than the equity market fall. Hence, don’t compare both.

Sir,

We have assured our investor, its a debt fund nothing will happen, there is more transparency, Fund Manager is well experienced and we informed our clients you can redeem with in 1 to 3 Years.

now what should we tell to our investors? Also what will be the Future of other Debt Funds of other AMCs, should we keep or move to equity.

It is difficult to digest such a Old AMC is short of liquid money, we loose hope in other AMCs also.

Dear Naresh,

From your comment, I can sense that you are an adviser. You have to understand why it happened with Franklin or it may happen with other funds. Hence, understanding the risk is very much important.