Which are the LIC Term Insurance plans available for us to buy in 2020? What are the features and benefits of the same?

We are fond of LIC and its product as it is a Government company. Hence, obivously we look for its products before we look for other insurers. Even though, I have written post separately with respect to LIC Term Insurance plans, I thought to sum it up and share it in a single post.

LIC Term Insurance plans 2020 – Features and Benefits

Currently LIC is offerning on OFFLINE Term Insurance and one ONLINE Term Insurance. Let us go one by one.

LIC’s Tech-Term (No.854) – Online Term Life Insurance

LIC’s Tech-Term (No.854) is a Non-Linked, Non-Participating Term Life Insurance Plan. After a long gap, LIC launching a term life insurance. It is mainly because of the competition in this field of product.

It’s features are as below:-

# It is a pure ONLINE Term Life Insurance from LIC.

# Minimum Sum Assured is Rs.50 lakh and there is no limit for maximum sum assured.

# You can pay the premium as regular, single or limited.

# You can opt for a level sum assured, where the sum assured you opted will remain the same throughout the policy period.

# You can opt for an increasing sum assured also, where the death benefit will remain the same up to 5 years of the first policy period. After that, it will increases at a rate of 10% for the next 10 years. From the 16th year, it will remain the same.

# Death Benefits can be taken in installments also of 5 years, 10 years or 15 years.

# Coverage up to 80 years of age.

# You can opt for Accidental Rider also.

# Lower rates for Non-Smokers and special rates for women.

Below is the eligibility conditions for LIC’s Tech Term Policy.

LIC’s Tech-Term (No.854) – Death Benefit Options

Death Benefit Sum Assured

As I have mentioned in the above post, there are two death options under LIC’s Tech-Term (No.854). They are as below.

# Level Sum Assured

Your nominee will receive the Sum Assured you opted while buying the policy. It will remain the same throughout the policy period.

# Increasing Sum Assured

Under this feature, the death benefit will be the same as that of the initial sum assured you have chosen for the first five years.

From 6th policy year to 10th year, it will increase at the rate of 10% per year.

From the 16th year of the policy period, it will remain the same throughout the remaining policy period.

Accordingly, your nominee will receive the death benefit during which period of the policy your death occurs.

Death benefit payment option to the nominee

Your nominee can receive the death benefit as a lump sum or in installments. If you opted for installments, then LIC will pay the death benefit installments in 5 years, 10 years or 15 years.

You can choose the full death claim amount be payable in installments or a certain portion of death claim in installments.

You can choose this installment option either at the time of buying or during the policy period.

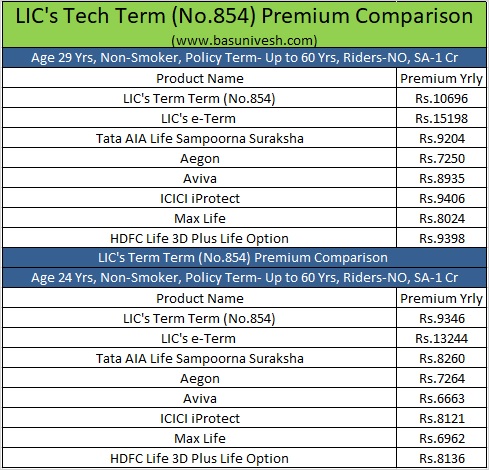

Let us now compare the premium of LIC’s Term Term (No.854) with other private players.

You notice that the premium of LIC’s Term Term (No.854) is cheap compared to the existing LIC’s online term plan (LICs’ e-Term). However, if you check the premium with private players, it is still costlier.

My view on this plan:-

Considering the market competition in online term life insurance plans, LIC launched this plan with the utmost care and including the many features which are already available in the market.

# It is an online term life insurance. Hence, the premium will be cheap. Also, it looks upfront that LIC’s Term-Term (No.854) premium is much cheaper than it’s earlier online term life insurance (e-Term). Hence, it is a big benefit for those who are desperate to buy the term life insurance from trusted LIC.

# Coverage of the policy is up to 80 years of age. Even though Life Insurance is not required up to 80 years of your age, but LIC added this feature to compete with private players. Hence, this is an attractive move.

# This plan comes with an accidental rider. It’s an earlier version of term life insurance was without any rider. Hence, this time LIC added accidental rider benefit. This is one more positive.

# Special discounts for a female is unique and attractive to all-female who are looking for online term life insurance from LIC.

# Premium paying option is too flexible with options like Single, Limited Period and Regular Period. This gives us flexibility.

# Increasing Sum Assured option is first time added by LIC. Where for the first 5 years it will not increase. However, after 5th year to 15th year it will increase at the rate of 10%. From 16th years onward, it will remain the same throughout the policy period. This is the big relief for those who have to review their life insurance coverage and avoid having multiple life insurance products.

# If you already holding LIC’s e-Term, then don’t discontinue just because of this plan offers you a lesser premium. Instead, while enhancing, you can buy this product.

# For those who trust LIC and looking for a term plan newly, they can opt for this policy. But do remember that buying term life insurance not completely depends on PREMIUM. Hence, take your conscious decision.

Overall, this product seems to the BEST product I may have reviewed with no such big negatives in this product to look for. Go ahead and buy it!!

LIC’s Jeevan Amar (No.855) – Offline Term Life Insurance

LIC’s Jeevan Amar (No.855) is a Non-Linked, Non-Participating Term Life Insurance Plan. After a long gap, LIC launching a term life insurance. It is mainly because of the competition in this field of product.

Under this plan, there two categories of premium 1) Non-Smoker and 2) Smoker Rates. You can choose any one option. However, if you have chosen the Non-Smoker category, then you have to undergo the additional medical examination like Urinary Cotinine Test. Based on the findings of the Cotinine Test, the premium will be applicable for the Non-Smoker proposer.

It’s feature are as below:-

# It is an OFFLINE Term Life Insurance from LIC.

# Minimum Sum Assured is Rs.25 lakh and there is no limit for maximum sum assured.

# You can pay the premium as regular, single or limited.

# You can opt for a level sum assured, where the sum assured you opted will remain the same throughout the policy period.

# You can opt for an increasing sum assured also, where the death benefit will remain the same up to 5 years of the first policy period. After that, it will increases at a rate of 10% for the next 10 years (up to it will turn double of the basic sum assured). From the 16th year, it will remain the same i.e double of the basic sum assured.

# Death Benefits can be taken in installments also of 5 years, 10 years or 15 years.

# Coverage up to 80 years of age.

# You can opt for Accidental Rider also.

# Lower rates for Non-Smokers and special rates for women.

# For regular premium policies, there is no surrender value as it is a term life insurance. However, for a single premium policy and limited premium policy, the surrender value is calculated based on the formula set by LIC.

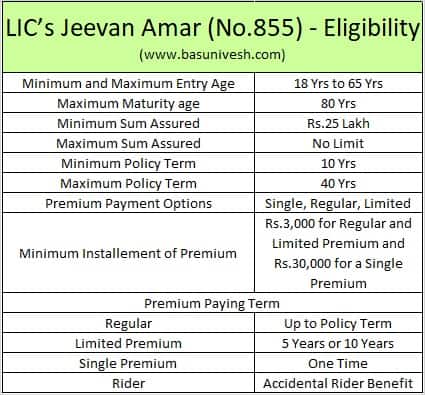

Below is the eligibility details of the Jeevan Amar (No.855).

LIC’s Jeevan Amar (No.855) – Death Benefit Options

Death Benefit Sum Assured

As I have mentioned in the above post, there are two death options under LIC’s Jeevan Amar (No.855). You have to choose the type of death benefit sum assured option at the time of buying only. You can’t change the option in the middle of the policy period. They are as below.

# Level Sum Assured

Your nominee will receive the Sum Assured you opted while buying the policy. It will remain the same throughout the policy period.

# Increasing Sum Assured

Under this feature, your sum assured increase as below.

- Under this feature, the death benefit will be the same as that of the initial sum assured you have chosen for the first five years.

- From 6th policy year to 15th year, it will increase at the rate of 10% per year till it becomes the double of the basic sum assured. The increase in the sum assured will continue under an inforce policy till the end of the policy term, till the date of the death of the policyholder or till the 15th year, whichever is earlier.

- From 16th policy year, the sum assured payable at death will be constant and i.e double of the sum assured you opted initially.

As per the chosen option, your nominee will receive the death benefit during which period of the policy your death occurs.

Death benefit payment option to the nominee

Your nominee can receive the death benefit as a lump sum or in installments. If you opted for installments, then LIC will pay the death benefit installments in 5 years, 10 years or 15 years.

You can choose the full death claim amount be payable in installments or a certain portion of death claim in installments.

You can choose this installment option either at the time of buying or during the policy period.

The installments will be payable to nominee in advance at yearly or half-yearly or quarterly or monthly as one has opted for. But make sure that these minimum installment payment rules.

- For monthly payment, the minimum installment amount is Rs.5,000.

- For quarterly payment, the minimum installment amount is Rs.15,000.

- For half-yearly payment, the minimum installment amount is Rs.25,000.

- For yearly payment, the minimum installment amount is Rs.50,000.

If the net claim amount is less than the required amount payable in installment, then LIC will pay as a lump sum one-time payment to your nominee.

My views on this plan:-

Considering the market competition in online term life insurance plans, LIC launched this plan with the utmost care and including the many features which are already available in the market.

# It is an OFFLINE term life insurance. Hence, the premium will be higher than their newly going to be launched plan LIC’s Tech-Term (No.854). Also, it looks upfront that LIC’s Jeevan Amar (No.855) premium is much cheaper than it’s earlier offline term life insurance. Hence, it is a big benefit for those who are desperate to buy the term life insurance from trusted LIC. However, I strongly suggest you to buy it online. Because agents commission under this plan is 25% for 1st year, 7.5% in 2nd and 3rd year, 5% in subsequent years (for the policy period of 15 years or more). Hence, why not pay more than opting the same from the online?

# Coverage of the policy is up to 80 years of age. Even though Life Insurance is not required up to 80 years of your age, but LIC added this feature to compete with private players. Hence, this is an attractive move.

# This plan comes with an accidental rider. It’s an earlier version of term life insurance was without any rider. Hence, this time LIC added accidental rider benefit. This is one more positive.

# Special discounts for a female is unique and attractive to all-female who are looking for online term life insurance from LIC.

# Premium paying option is too flexible with options like Single, Limited Period and Regular Period. This gives us flexibility.

# Increasing Sum Assured option is first time added by LIC. Where for the first 5 years it will not increase. However, after 5th year to 15th year it will increase at the rate of 10% (up to this increasing sum assured double the basic sum assured). From 16th years onward, it will remain the same throughout the policy period. This is the big relief for those who have to review their life insurance coverage and avoid having multiple life insurance products. However, keep one thing in mind that the maximum benefit one avail under this plan is DOUBLE of basic sum assured you availed at the start of the policy period. Hence, consider the actual need and take a call.

BUT WHY IS LIC LAUNCHING AN OFFLINE PRODUCT WITH the SAME FEATURE, WHEN IT JUST LAUNCHING ONLINE TERM LIFE INSURANCE WITH THE SAME FEATURE?

IS IT JUST TO CATER TO THEIR AGENTS FORCE? OR THOUGHT OF TO CATER TO THOSE WHO ARE NOT WELL VERSED WITH ONLINE BUYING? I DON’T THINK SO. BECAUSE WITH THE KIND OF SMARTPHONES, ONLINE BUYING AND ONLINE PAYMENT THE PEOPLE ARE ACCUSTOMED, IT IS USELESS TO BUY COSTLY OFFLINE PLAN WITH THE SAME FEATURE OF ONLINE (except lower minimum sum assured).

I strongly suggest you go for online term life insurance LIC’s Tech-Term (No.854) rather than this offline product.

Refer my latest post on “Top 5 Best Health Insurance Plans in India 2020” for the better comparison and choosing the products.

Conclusion:-You noticed that feature-wise LIC’s both term life insurance are best. However, if you compare the premium with private insurers, obviously LIC’s term life insurance are still costlier. If you are really looking for safety and trust, then you can choose LIC’s term life insurance plans.

Refer our latest posts:-

- The Dark Side of Compounding: How 2% Kills Rs.30 Lakh

- Flexi Cap Funds: Why Your 10-Year Return Chart Is Lying

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

Hello Sir,

I have gone through the policy document of online lic e-term insurance, there is on clause which stated that

Death benefit payable in case of admissible death claim

during the policy term, provided the policy is inforce shall

be “Sum Assured on Death”.

For Regular premium and Limited premium payment policy,

“Sum Assured on Death” is defined as the highest of:

• 7 times of annualised premium; or

• 105% of all the premiums paid as on the date of death;

or

• Absolute amount assured to be paid on death.

For Single premium policy, “Sum Assured on Death” is

defined as the higher of:

• 125% of Single Premium.

• Absolute amount assured to be paid on death.

Premiums referred above shall not include any extra amount

chargeable under the policy due to underwriting decision

and rider premium(s), if any.

I didnt understood this wordings , can you please explain me.

Dear Rahul,

What is your doubt? Try yourself with an example, then you will realize. They are clearly mentioning the death benefits properly. I am not sure what is your doubts.

I Didnt understood this

For Regular premium and Limited premium payment policy,

“Sum Assured on Death” is defined as the highest of:

• 7 times of annualised premium; or

• 105% of all the premiums paid as on the date of death;

or

• Absolute amount assured to be paid on death.

because, in any case highest will be our Sum Assured only. then why they have mentioned (7 times & 105%) points in clause.

It will be better understood if you explain with an example.

Thanks in anticipation.

Dear Rahul,

In certain limited premium payment options, few try to misuse and hence the regulator forced such clauses. If you are paying a regular premiums, then the highest will be the sum assured. Hence, why to worry for you?

Hi Basu,

Thanks for your response, then why the brochure of policy has mentioned above 2 clause with or statement.

Please make me more clear.

Dear Ganesh,

It is the mandatory disclosure for all Life Insurance products (like an endowment, ULIP, Money-Back or Term Life Insurance). Hence, they are disclosing so.

Hi Basu,

I have gone through the policy document of online lic e-term insurance, there is on clause which stated that

Death benefit payable in case of admissible death claim

during the policy term, provided the policy is inforce shall

be “Sum Assured on Death”.

For Regular premium and Limited premium payment policy,

“Sum Assured on Death” is defined as the highest of:

• 7 times of annualised premium; or

• 105% of all the premiums paid as on the date of death;

or

• Absolute amount assured to be paid on death.

For Single premium policy, “Sum Assured on Death” is

defined as the higher of:

• 125% of Single Premium.

• Absolute amount assured to be paid on death.

Premiums referred above shall not include any extra amount

chargeable under the policy due to underwriting decision

and rider premium(s), if any.

My question is that if i buy policy for 50 lac the above clause makes confuse that how much SA, we will receive in case of death of person.

Dear Ganesh,

If you fill your own example, you noticed that the minimum benefit you receive is the sum assured you opted. Hence, no need to confuse yourself.

Very well written article Basavaraj! I have a question; If I choose the increasing sum assured option, will the premium remain fixed or it’ll increase over time ?

Dear Deb,

It is also fixed. However, the increasing sum assured option premium is costly than the level sum assured premium from day one.

Thanks for the article, Basu. Very crafted.

I am an Indian Citizen and a Permanent Resident (PR) of Australia and I would like to know whether I can purchase the Tech-Term online policy.

(I was going through the information in LIC website under NRI center and its mentioned that Green Card Holders are not treated as NRI. Considering Green Card is Permanent Residency in US, is this applicable to PRs in other countries?)

Dear Arun,

I think you are not eligible for this plan. However, I suggest you to contact the LIC for better clarity on this aspect.

Sir, Can I take this Term insurance policy for my wife who is a house wife who does not have any income. However I am an earning member.

Dear Vasavan,

First think yourself, whether she actually needs a term life insurance? They will not give to your wife as she has no earnings.

All other insurarer are not accepting proposal due to income proof and education but you are not required any income proof and education so I am asking this,

My father is riksow driver earning 15 k monthly his education is 5th class. Is he eligible for this product.

And why other insurarer asks for income proof and education but lic not .

Dear Minaj,

Does he need such huge insurance? Usually, the Life Insurance companies arrive at your life insurance requirement based on your earnings. This is called the Human Life Value. Hence, even your father applies also, they issue the policy based on this but not based on what you proposed.

What is minimum income required for this policy and what is the education qualification required to buy this policy.

Dear Gopal,

There is no such income and educational qualification requirements. However, your proposal will be verified by the underwriter and accordingly, they will take the decision to issue the policy to you or not.

You have mentioned that a non-smoker has to under cotine test,please check your writeup

Dear Peter,

I wrote based on what it is mentioned in their product feature submitted with IRDA.

If taking an online term plan from LIC, what will be the procedure for claiming the assured sum if in case something happens to the insurer. Will it be difficult for the family? Also, which branch needs to be contacted? That also could be a reason people opt for offline plans. Could you please provide your suggestions on this?

Dear Abhinav,

With the kind of network offices LIC is holding, I don’t think the claim will be difficult. They will assign a branch for you. However, you have an option to approach the nearest branch also. Advisers usually create such fear among buyers. But advisers themselves don’t know for how long they run their advisory business. Hence, don’t heed to all these gimmicks.

Is it possible to buy this policy for student completed the age 20 ?

Dear Saurabh,

Whether he is a student or someone, if they have no income, then there is no financial loss. Hence, no company will provide you the insurance on someone whose income is NIL.

Nice information.

Permanent and partial disability benifit is included in jeevan amar plan?

Dear Abhijit,

It is a rider you are looking for by default its not part fo any term life insurance.

Thank you Basavaraj for your detailed explanation. I have been subscribed to LIC eTerm policy from past 5yrs. But even though it says online, I had to submit all documentation hard copy to LIC branch office (online). Atleast in the latest Tech Term policy, is there an option to upload soft copies of the documents and finish the process completely online itself? Without the need to courier or submit hard copies.

Pls let me know. I want to enhance the coverage with buying Tech Term policy.

Regards,

Sanjay

Dear Sanjay,

I think the process of submitting the hard copies to the concerned LIC branch is still there. But I don’t think this a hindrance.