After the Budget 2019, what is the Mutual Fund Taxation FY 2019-20? What is the Mutual Funds tax rate for FY 2019-20?

3 Factors that determine the Mutual Fund Taxation

First, let us understand what are the factors that determine the Mutual Fund Taxation. The three major part of these are below.

# Your Residential Status-Resident or Non-Resident (NRI)

Your tax will be based on your residential status. If you are resident then the taxation rules will be different and if NRI then it differs. Hence, first, you have to make sure of what is your residential status.

# Types of Funds-Equity Funds or Non-Equity Funds-

Any fund which invests 65% or more in equity is called as Equity Fund. For example, large-cap funds, multi-cap funds, small and mid-cap funds or equity-oriented balanced funds (where the equity exposure is 65% or more) are all called equity-oriented funds.

If the equity portion is less than that, then they are all treated as debt funds or non-equity funds. For example liquid funds, ultra-short term funds, short-term funds, income funds, gilt funds, debt-oriented balanced funds, gold funds, fund of funds or money market funds.

# Holding periods of Investment–

The holding period for Equity and Debt Funds will be different for taxation purpose. For equity funds, if the holding period more than a year, then it is called long term. If the holding period is less than a year, then such equity mutual funds holding period is considered as short term. Whereas in

Whereas in the case of debt funds, holding period more than 3 years is considered as long-term. If holding period of debt funds is less than 3 years, then it is considered as short-term and taxed accordingly.

I will try to explain the same from below chart.

Now you got the clarity on what will be STCG and LTCG. Let us move further and understand the Capital Gain Taxation for mutual fund investors.

Mutual Fund Taxation FY 2019-20 -Capital Gain Tax Rates

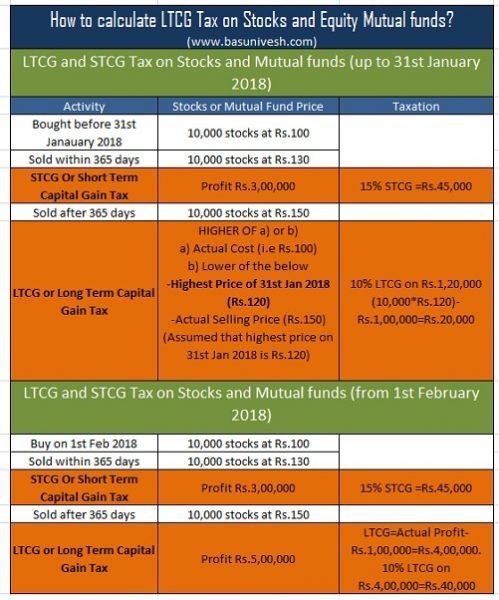

The biggest change from FY 2018-19 is the introduction of LTCG in Budget 2018. There is no change in Mutual Fund Taxation FY 2019-20. Hence, let me explain the same from below image.

Note-Surcharge @ 15%, is applicable where the income of Individual/HUF unit holders exceeds Rs. 1 crore. Also, surcharge @10% to be levied in case of individual/ HUF unitholders where the income of such unitholders exceeds Rs.50 lakhs but does not exceed Rs.1 Cr. Further, Health and Education Cess @ 4% will continue to apply on the aggregate of tax and surcharge.

As you may be aware that during Budget 2018, LTCG was introduced again to Equity Funds. Hence, let me explain the same on how to calcualte the LTCG on Equity Funds as below.

Mutual Fund Taxation FY 2019-20 – Dividend Distribution Tax (DDT)

There are few investors who opt for dividend option in mutual funds. Hence, let us see the taxation on the dividend of such funds. Earlier there was no DDT for equity investors. However, from the Budget 2018, DDT @10% will be applicable to equity investors also.

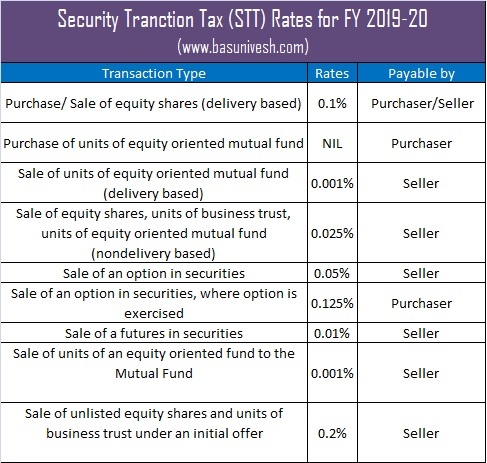

Security Transaction Tax (STT) for FY 2019-20

Security Transaction Charges or STT is the charges or tax when you buy or sell securities (excluding commodities and currency) through a recognized stock exchange. Therefore,

The definition of securities involves the below products.

- Shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate;

- Derivatives;

- units or any other instrument issued by any collective investment scheme to the investors in such schemes;

- Security receipt as defined in section 2(zg) of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002;

- Government securities of equity nature;

- Rights or interest in securities;

- Equity-oriented mutual funds

Therefore, whenever you buy and sell these securities through a recognized stock exchange, then you have to pay this STT.

Now let us understand the latest Security Transaction Tax (STT) applicable for FY 2019-20.

TDS (Tax Deducted at Source) Rates for NRI Mutual Fund Investors 2019-20

Below are the applicable TDS rates for NRI Mutual Fund investors for FY 2019-20.

Hope now you got the clarity related to Mutual Fund Taxation FY 2019-20.

Refer my latest posts related to mutual funds-

- Top 10 Best SIP Mutual Funds to invest in India in 2019

- Latest Income Tax Slab Rates FY 2019-20 (AY 2020-21)

- Best Debt Mutual Funds to invest in 2019 India

Hi Basu,

I had invested in Aditya Birla Sun Life Focused Equity Fund – Growth-Regular Plan (formerly known as Aditya Birla Sun Life Top 100 Fund) as SIP from Feb 2014 to June 2015. I have redeemed all units in March 2019 and got profits of Rs 30,000/-. As per my understanding, income tax not applicable on this profit but needs to mention in ITR. Could you please let me know my understanding is correct ? In which ITR form and section, this needs to be mention ?

Dear Kumar,

Do remember that the gain which is up to Feb, 2018 is tax free. Regarding mentioning in ITR, you can mention it in exempted income.

I have debt STCG of less than Rs. 500/-. Do I need to file ITR2 or can continue with ITR1 like previous years since gain is very small?

Also in ITR2 we fill only gains or we need to show cost of acquisition and sale separately and then balance (gains) will be calculated?

If possible, please share some article or link about how to fill STCG/LTCG for MFs in ITR form.

Dear Rahul,

Whatever the amount, it is better to show it. You have to show as the format is prescribed in ITR2.

Thanks!!!

In view of grandfathering introduced in budget 2018-19, can you please explain calculation of short term capital gain, if units of equity oriented funds are purchased before 31st jan 18 and sold before completion of 365 days.

In this case is cost of acquisition to be taken as original purchase cost or fmv as on 31.01.18. CAMs and some other mutual fund houses seem to be taking fmv as acquisition cost, while some fund houses take original purchase cost as acquisition cost. Hence the question to understand correct procedure under tax laws.

Dear Satish,

It should be fair market value.

Thank you for this post. Given these tax rates, can you please explain us as to whether debt instruments or mutual funds give a better return with an example ?

Dear Meena,

It again depends on your NEED and the holding period. Can you elaborate more about your actual requirement?

Thank you for the post. What are the provisions in case there is a long term capital loss in Equity or MFs. Can it be set off against LTCG or STCG? Also the loss will be reference to the cost of acquisition only and not with the highest price as on 31st Jan 2018. Thanks again.