For the FY 2012-13 you may expect series of tax free bonds from authorized 10 issuers. Period is already started with issues from REC and PFC earlier this month and now from today onward IIFCL. This will continue till this financial year. So let us looks at features of these bonds and who can invest?

Below is the list of issuer who can offer you these tax free bonds for FY 2012-13.

- Indian Railway Finance Corporation (IRFC)

- India Infrastructure Finance Company Limited (IIFCL)

- Housing and Urban Development Corporation HUDCO)

- National Housing Bank (NHB)

- Power Finance Corporation (PFC)

- Rural Electrification Corporation (REC)

- Jawaharlal Nehru Port Trust

- Dredging Corporation of India

- Ennore Port Limited

- National Highway Authority of India (NHAI)

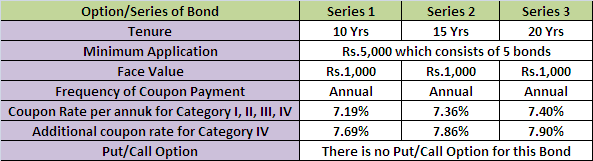

We will take the example of IIFCL which is currently open.

Note:-Category I-Qualified Institutional Buyers (QIB’s), Category II-Domestic Corporates, Category III-High Networth Individuals (HNI’s) and Category IV-Retail Individual Investors.

Issuance will be both in physical and demat mode. Also it is proposed to be listed on BSE. Credit Ratings: AAA by CARE, AAA (Stable) by ICRA and BRICKWORK.

First let us look at the taxation of these tax free bonds.

1) Interest is tax free. Which is not the case with your Bank FDs. Hence no TDS.

2) No Wealth Tax.

3) This being listed on BSE and treated equally with any other financial instruments. If you sell these bonds by holding more than 12 months and the profit over and above the face value will be considered as Long Term Capital Gain and taxed at the rate of 10% (No Indexation on Bonds). But no STT (Security Transaction Charges).

4) Holding these bonds less than 12 months will be treated as Short Term Capital Gain and will be taxed according to normal rates.

Who can Invest?

Highest rating by rating agencies means investors who are risk averse can definitely go for such products. Eventhough tenure looks longer but the same post tax returns not possible from any other fixed instruments. Remember that only interest is tax free, it does not mean that this investment will come under any section (like Sec 80c) which will benefit you in your taxation. Hence before going for this investment first consider your tax liability for this year. Liquidity will not be the issue as bonds will usually list on any of stock exchanges (for IIFCL it is BSE). As everybody predicting the lowering of interest rate by RBI in near future, so you may get best pricing in future if you want to sell in secondary market too. If you are in 30% tax bracket and if we consider the IIFCL issue’s interest rate to pre tax returns then they work out to be 10.98%, 11.22% and 11.28% respective for 10, 15 and 20 years bonds. This return for such a long term investment will not be possible with your Bank FD’s.

Disadvantages-

1) Tenure bond is 10,15 and 20 years their is interest rate risk attached with it.

2) Eventhough post tax interest rates looks attractive but the payout of interest will be annul. Hence you may end up not re-investing it in a proper way and finally after the end of period you only get Face Value. So if you re-invest the received interest then you may get higher returns than other products. In FDs you receive interest at the end of tenure which is not the case of these bonds.

3) As usual, request you not to park all your fund in such products, instead park some percentage of your portfolio.

I tried many a time.( nly. 10 yrs for 15 yrs time ) But not able to get allotted the same.

All such announced bonds are over subscribed on the same day of announcement.

The max amount should be increased to 20/25 lackhs & or the allotment should be on ratio equally to all applicant.

Dear Mukundan,

You can try your luck from secondary market.

Hello Sir,

I would like to know whether this infrastructure bonds will come under which tax section.

Can we show this investment for tax on top of 1.5 Lac of 80C?

Thank You!

Jay-No, such bonds are not part of Sec.80C limit. Only the interest you earn is tax-free.

Hello Basu sir,

I’m interested in these Tax free bonds. Could you please tell me from where I can purchase these bonds for eg. recently lanuched NHAI bonds.

thanks

Vimi-There are many brokers (like stock brokers) or agents who offer such service. Contact the nearest one to you.

Hi

Where can we buy tax-free Bonds and presently which are the best bonds to buy and is it safe buy from secondary market

Looking for the guidance

Thank you

Maneesh

Maneesh-At present no such offerings.

if i will invest in this IIFCL 20 year bond so what is actual rate of return ?

if i will come in 10% tax bracket than (7.9/0.9) = 8.78%

if i will come in 20% tax bracket than (7.9/0.8) = 9.875%

if i will come in 30% tax bracket than (7.9/0.7) = 11.285%

my calculation is right or wrong ? and how ?

Rushabh-You did pre tax return calculation. This you can use to compare with other products where returns are taxable. I did the same above. Please check it.

ok

thank u

Are NRIs allowed to invest in these bonds? If yes, repatriable or non repatriable basis?

Shirish-I dont think NRIs allowed to invest in these bonds. Because as per current available IIFCL Tax Free Bonds product detail, NRIs not allowed.

Whether if the interest is tax free for the nominee after the death of the bond holder. or after the tax period of 30% is over to the present bond holder and the bond holder becomes a no tax and transferred to the nominee who @ that time is in the highest tax bracket Thanks

Bala-In all case it is tax free. Either main investor survives or not or whatever may his and his dependents tax slab.

Finally a blogger talks about the disadvantages of these bonds! It is extremely disappointing that many financial bloggers have contributed to mis-buying of these bonds by claiming to write reviews of the bonds and all they would do is to list all details available from the company floating the bonds.Unfortunately many buy these only because of tax free interest without see if it is suitable for their financial goals

Pattu-Thanks for your appreciation 🙂