Recently LIC launched it’s first online policy with launching new version of pension plan “Jeevan Akshay VI”. Let us look at it’s features and how it is beneficial.

Note-LIC reintroduced the plan with few changes and reduced annuity rates. Refer my latest post on the same at “Jeevan Akshay VI – LIC’s Single Premium Pension Plan Reintroduced“.

Before that I want to give you small glimpse on few terminologies used in pension plans.

Annuity-In simple term you can say it as a Pension, where you will get regular income till the specified period or conditions. Two types of annuity are their 1) Immediate Annuity-In this case your pension starts immediately. 2) Deferred Annuity-In this case your annuity starts after certain period. (Suppose your current age 40 yrs and if your annuity will start from the age of 60 years).

Jeevan Akshay VI is the immediate annuity plan where you pay lump sum one time to purchase this plan and your annuity starts from next month.

Basic Features–

1) Minimum age is 30 years and maximum is 85 years of age.

2) Minimum purchase price is Rs.1,00,000 for off line and Rs.1,50,000 for online purchase. But no maximum limit.

3) This policy does not acquire paid up value.

4) No Surrender Value under this policy.

5) No loan available under this policy.

6) If your purchase price is Rs. 2.50 lakh or more, you will receive higher amount of annuity due to available incentives. In addition of this, for policies sold online, a rebate of 1% by way of increase in the annuity rate shall also be available.

7) Annuity will be payable on monthly, quarterly, half yearly or yearly base according to your choice.

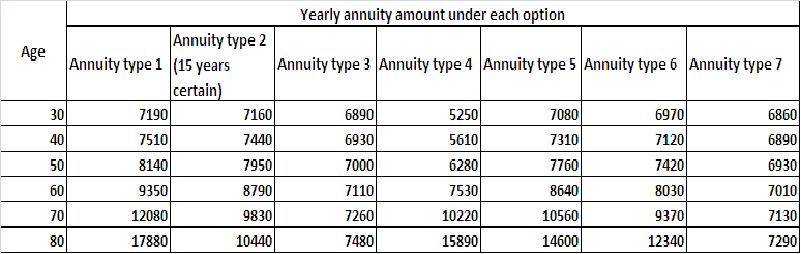

Types of Annuity available–

How much you get by one time investment of Rs.1,00,000?

From the above table you notice that persons who are at their younger will receive less annuity than the older. Eventhough this plan provides facility to enter at the age of 30 yrs but when you calculate for purchaser of this annuity as 60 years then it looks bit attractive. For example if you opt the annuity type 1, age 60 years and investable amount is Rs.25,00,000 then you will receive monthly pension as Rs.19,479 throughout your remaining life span.

Now if we calculate the returns for the annuity type 1st and considers post retirement life as 20 years (means purchaser who is currently at 60 years of age and his life expectancy 20 years from current age means till the age of 80 years) then return on his investment will be around 6.90%. Now let us see the annuity type 4th by using the same annuity purchaser data, where every year your annuity will increase by 3%, then return on your investment will be 7.03%

But remember two things in mind, whatever the annuity you will receive in this plan is taxable as per current tax slabs for individual and it will not support the inflation adjusted returns. Hence if we consider the both factors then it is a big no no…plan. Eventhough from the annuity type 4 we can assume that inflation will be dealt to the some extent, but still if you consider post tax returns then it will definitely eat your annuity returns drastically.

It is really a good plan for investors who want some steady income throughout their remaining life span without bothering about taxation and inflation. Also one more positive point is, if you invest in this plan then you will diminish the interest rate risk. Because instead of investing in this plan, if you invest in monthly income plans, then you are not sure the same interest you will receive after maturity too. But in this plan you no need to bother, because whatever market interest rate, you receive stable income.

Remember too that, always invest your retirement accumulated corpus into secured products rather than risky products. Because if your age is 60 years then you are not in a position to take the same risk what 30 years of age investor can take by investing in equity oriented schemes. So think twice and decide to proceed further based on your requirement.

EPF Scheme 2026 explained fully: EPF withdrawal, EPS pension, and EDLI insurance changes with examples,…

Chasing financial freedom? Do health, time, relationships and contentment matter just as much? Sadly, we…

Your "safe" SIPs, SGBs, PPF, or Index Funds are secretly sabotaging your wealth. Peltzman Effect…

Thinking your retirement plan is foolproof? Why LUCK - not asset or fund selection or…

Nifty 50 Index Funds Vs Active Large Cap Funds — Can we really compare them…

Should you pick Nifty 500 Multicap 50:25:25, Nifty 500, or Nifty LargeMidcap 250 Index Fund?…

{kind=link}

View Comments

Sir,

Found your article very useful. Has Jeevan Akshay plan been withdrawn? LIC's main portal lists it under withdrawn plans, whereas LIC Direct, https://eterm.licindia.in/onlinePlansIndex/login.do, still has link to purchase that plan. Besides, the annuity rates listed in LIC direct portal are higher than what you have mentioned in the article. Which portal is to be trusted?

Is the annuity paid under this plan subject to TDS? The comment by Sidharth posted in June 2018 suggests TDS is applicable, but the plan details document does not mention TDS. Can you please clarify? Thank you.

Dear Guest,

The earlier version of Jeevan Akshay was withdrawn. But the new version is available now also. Regarding the change in annuity rates, they revised recently. You may go with LIC portal. Do you feel avoiding TDS means avoiding tax?

Sir,

Thanks for your quick reply. The LIC Direct and normal LIC portals show different details causing confusion. I will contact their customer service or an agent to get correct details.

I realize no TDS does not mean no tax. But in the absence of clear information on TDS for this policy, there is the concern that LIC may apply 30% TDS rate even if the customer comes under a lower tax rate slab and customer will be forced to claim tax refund

Dear Guest,

Whether they deduct 30% or 10%, you have always a window to file IT return and claim (if they deducted more TDS) right?

Is this policy can be revoked once the bond is issued. As other policies can be revoked within 15 days from the date of the bond issued. As my brother in law who is a NRI invested in it having a misconception of the policy is Tax free told by agent. Can we still revoke it he purchased it around month ago policy is not received yet.

Dear Anshu,

Yes, you can do so during free-look-in period.

Thanks Basu for your reply.

my annuity money credited to my NRE account. LIC started deducting the tax @ 31%, Annuity(monthly) amount is 20621 deduction is 6372 I have made a complained, they are asking to produce Tax residence certificate from the country. I just forwarded my residency permit. I am currently working in Qatar.

Dear Sidharth,

If your maturity is exempt under Sec.10(10)D, then there is no TDs for NRIs also. I am not sure on what basis they deducted the TDS. Please check with them.

Basav and Basu

I also experienced same issue. I had an annuity of 1,04,000. They paid me only 71000/-. Do you have any resolution for this ??

Dear Shaji,

I don't have such resolution. However, you have every right to ask them.

ok thanks

Dear Sir

1. If I purchase JA VI through online, where should I submit the existence certificate and other documents?

2. Is it possible to submit Existence certificate online on required frequency?

3. Which branch will service my request or if any queries, which branch will I have to contact?

4. I will be going for option 7, and in this case, which branch my wife will have to contact in case I am deceased and she has to get the annuity. Also the same for nominee?

Mohan-1) They will inform you about this.

3) They assign the branch for the same.

Thanks for the quick response

Hello Basu,

Appreciate you for this Great write up, the provided information is very much helpful for me.

on the interest rate aspect, i have following few queries, it would be great if you could clarify those.

1. Would like to know the current interest rate.

2. Does the interest rate revision happen during the Policy terms? if yes, then how often.

3. comparing FD vs Jeevan Akshay VI what is your recommendation.

Thanks

Prakasam

Prakasam-1) Refer the LINK.

2) During policy period, even if it happens also, it will not affect YOU. It is for those who want fresh investment. The rate which is there during the policy period will be applicable for you till the end.

3) Hard to generalize.

Thanks Basunievsh, Appreciate your prompt response.

I am 44-year old and would like to know about Option-7 for an amount of INR 30,50,000. The above calculator shows a monthly payout of 16,982. I would like to know what would be the TDS amount on the monthly payout. I would like my wife to receive the same pension amount after my death and my son to receive the purchase price. Kindly clarify.

Vittal-There is no TDS, but it is taxable income for you. Hence, you have to pay the tax on such income.

Jeevan Akshay VI probably be Closing from today 30 Nov, 2017. From 1st, Dec, 2017 New Return rates will be applicable, maybe less then current rates

mail4om-YES.

Sir i want to know that can we get our purchase price back when we needed?...... Or it is only available at death of the annuitant.

Karanpreet-You can get the purchase price if you have opted that option available in above options.

Sir can i get my purchase price easily after 1 year of purchase?

Is that option available?

Karanpreet-NO.

Tnk u sir

If I take Jeevan akshay6 under option 7 for 4 lacs. What do I get if the policy is taken/purchased offline vs online. I want specific amount to be mentioned. Not %. That's already mentioned 1%extra.

Satvinderpal-It is 1% of your total investable amount you get as discount.

Will it be wise to dump around 20-30 lac in this policy? Thanks.