There are 24 Life Insurance companies in India. Among those 24 companies, which one we can choose to buy the term life insurance? Let me share with you my Top 5 Best Term Insurance Plans in India 2021.

Majority of us who are looking for term life insurance always try to concentrate on the claim settlement ratio as a first indicator. However, what are the other things we have to consider while buying term life insurance?

What is Term Life Insurance?

Term Insurance is the type of Life Insurance. If death occurs of the policyholder during the policy period, then his/her nominee will receive the Sum Assured selected. If the policyholder survives till the end of the policy period, then he/she will not receive any maturity amount.

This is the reason, these policies cost you very less and cover a large amount of life risk. This is the PURE LIFE INSURANCE. Hence, anyone who has financial dependents must buy this product immediately.

However, nowadays there are so many variants in Term Life Insurance. For example, the return of premium, Term Life Insurance up to 100 years of age, a variety of riders, and a variety of claim payable options.

But instead of complicating your dependents, buy simple plain term life insurance. Why you complicate your dependents when you are buying this is that this product’s benefit will come into the picture when you are not here.

What are the advantages of online Term Insurance Plans?

Nowadays all Life Insurance companies offer you online term insurance plans. The advantages of online term plans are as below.

# It is convenient to buy as with the click of a button you can buy it.

# As there will not be any middlemen involved, the price is cheap than offline term insurance plans.

# You fill the proposal form on your own. Hence, an error of margin is LESS.

# Undue influence by agents is not there.

# Those who claim that online buying is RISKY as there are no middlemen involved are those who are representative of some companies and they may get a commission if you buy through them. Hence, they crease such stories.

Top 5 Best Term Insurance Plans in India 2021

Now let us discuss on what basis we can choose our Top 5 Best Term Insurance Plans in India 2021. Few pointers I will suggest which may help you in selecting your term life insurance.

# Claim Settlement Ratio

DON”T RELY ON THIS DATA. The reason is that it is raw data of all life insurance products a company is selling. It will not classify the death claim settlement ratio of term life insurance. This is the biggest reason why you must stay away from concentrating too much on this data.

However, if you are willing to know the current data, then you can refer to my latest post “IRDA Life Insurance Claim Settlement Ratio 2021“. Below are few latest reports from IRDA Annual Report.

As I pointed, few Life Insurance companies claim settlement ratio may be attractive. However, it is not an indication that they are settling your claims. Hence, don’t be get fooled by the claim settlement ratio. As a pointer to validate my saying, refer to the below image.

Notice the average claim settlement of LIC. It is the least compared to all others. This data itself shows that their claim settlement is mainly traditional plans.

However, if you are a fan of the claim settlement ratio, then it is left with you to decide which one to consider.

# Premium cost of Term Life Insurance plans

Even though whatever the features we look for, the premium is what we have to take into consideration while buying our term life insurance. I am not saying that the one which is offering at cheap is the best and at the same time the one which is offering at costly is worst. I mean to say that you have to balance between feature and price.

Hence, consider this point while buying your term life insurance. However, never choose the option like RETURN of PREMIUM. It is a waste feature that these insurers added you to lure while buying. Stay away from this return of premium.

# Features of Term Life Insurance

Term Life Insurance is the simplest product a life insurance company can offer you. However, if you look at the current products, I am sure that you will run away or get confused about which one to buy. Hence, rather than complicating your life, follow the below steps.

The ideal coverage should be around 15-20 times of your yearly income. Hence, buy accordingly. Term of the life insurance should be up to your working age. During your retirement age, Life Insurance is a WASTE product. Hence, don’t go for a term of up to 80 years or 100 years.

Never go for riders like accidental or critical illness. The main reason is that life insurance is required only for a limited period. However, accidental or critical illness insurance is required for you throughout your life. Also, if you buy these riders as a standalone product, then they may offer better features than these riders.

Stick to the yearly payment option rather than choosing monthly or limited payment. Few choose premium payment as monthly. However, these term life insurance products are high sum assured, a single default of premium may be converted to a lapsed of policy. To reinstate the same, life insurance companies may ask you to undergo a medical examination. Hence, to avoid such hassle, better to opt for a yearly premium. To accumulate the same, RD of a year is enough.

These are the main pointers when you look for plan features. Few more are listed at the end of this post which may help you in shortlisting a product.

# Age of the company

As Life Insurance is a long-term contract between you and the company, look for stable companies than the one where the management or takeover happening frequently or the newly entrant.

Go for stable and old companies. However, even if a new company shut its doors, it can’t run away from the responsibility. For a better understanding of this concept, read my post “What if your Insurance Company goes bankrupt?“.

List of Term Life Insruance products available in India

Now, let me share with you Term Life Insurance products available among all 24 companies.

- LIC Jeevan Amar (Offline Plan)

- LIC Tech Term (Online Plan)

- HDFC Click2Protect Life

- ICICI Pru iProtect Smart

- Max Life Smart Term Plan

- Max Life Term Plan with return of premium

- Max Life Online Term Plan Plus

- Kotak e-Term Plan

- ABSLI Life Shield Plan

- ABSLI Digishield Plan

- Tata AIA Maha Raksha Supreme

- Tata AIA Sampporna Raksha

- Tata AIA Sampporna Raksha+

- SBI Life eShield

- SBI Life Poorna Suraksha

- SBI Life Smart Shield

- Exide Life Elite Term Life Insurance

- Exide Life Smart Term Pro

- Exide Life Smart Term Edge

- Exide Life Term with Return of Premium Plan

- Bajaj Allianz Life Smart Protect Goal

- Bajaj Allianz Life eTouch Online Term

- Bajaj Allianz iSecure

- PNB Metlife Mera Term Plan Plus

- PNB Metlife Mera Term Plan

- PNB Metlife Aajeevan Suraksha Plan

- Reliance Nippon Life Protection Plus

- Reliance Nippon Life Digi-Term Insurance Plan

- Aviva Lifeshield Advantage

- Aviva Jana Suraksha

- Shriram Life Smart Protection Plan

- Shriram Life Smart Protection Plan SP

- Shriram Life My Spouse Term Plan

- Shriram Life Cash Back Term

- Shriram Life Family Protection

- Bharti Axa Flexi Term Plan

- Bharti Axa Premium Protect Plan

- Bharti Axa Smart Jeevan

- Bharti Axa Income Protection Plan

- Future Generali Flexi Online Term Plan

- Future Generali Express Term Life Plan

- Ageas Federal Life Insurance MyLife Protection Plan

- Ageas Federal Life Insurance Income Protection Plan

- Ageas Federal Life Insurance Termsurance Life Protection Insurance Plan

- Canara HSBC Oriental Bank of Commerce Life Insurance iSelect Star Term Plan

- Aegon Life iTerm

- Aegon Life iTerm Plus

- Pramerica Life Trushield

- Pramerica Life U-Protect

- Star Union Dai-Ichi Life Insurance Life Abhay

- IndiaFirst Life Insurance Guaranteed Protection Plan

- IndiaFirst Life Insurance Life Plan

- IndiaFirst Life Insurance Online Term Plan

- Edelweiss Tokio Life Insurance Zindagi Plus

You get confused right?? Yes, me too 🙂 This is a classic example know how the financial industry complicates your life. Term Life Insurance is a simple product. But in the mad rush to show that they are the BEST in the market, these life insurance companies are adding one by one feature to the product and made our LIFE COMPLICATED.

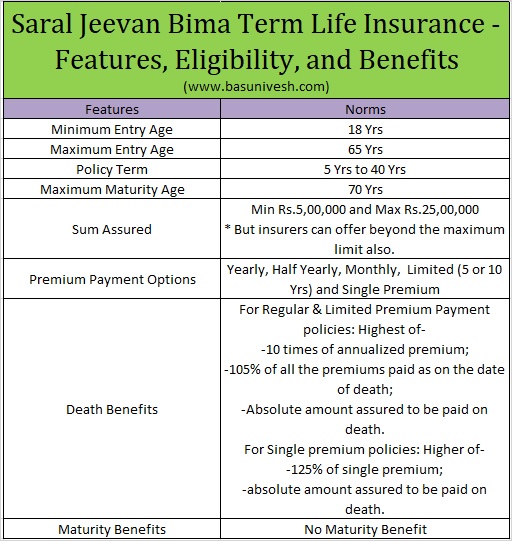

Then which one to buy? The answer is IRDAs recent initiative of standard Term Life Insurance called “SARAL JEEVAN BIMA YOJANA“.

It is a standard life insurance product with a standard feature. You can look into this product. However, the default maximum cover is Rs.25 Lakh (however insurers can offer you higher coverage also). Hence, if your opted life insurance company is offering Saral Jeevan Bima Yojana at higher coverage, then the best option is to choose it. Mainly because it is simple to understand and standard basic features are available with this product. Sharing with you the features of the same.

Let me now share my choice of Top 5 Best Term Insurance Plans in India 2021.

- LICs Tech Term

- HDFC Click2Protect Life

- ICICI Pru iProtect Smart

- Max Life Online Term Plan Plus

- Aegon Life iTerm

Few points to consider while buying term insurance

# Never rely on Claim Settlement Ratio

Claim Settlement Ratio is raw data. This data will not give you enough picture of what type of products the insurance companies settled. Hence, relying too much on this single data and selecting a product is not a good idea.

# Quantum of Life Cover

Ideally one must have at least 15-20 times of your yearly income. This is the basic calculation.

# Fill the data properly

Sharing data especially materialistic information must be accurate. If you are unable to understand anything, then immediately contact Life Insurer for help. Understand the questions and fill them only when you know what you are filling.

# Never allow someone to take over your decision

Never budge on the decision which is against your wish. If you are fully comfortable, then only go ahead and buy.

# Term of the policy

Ideally, it should be up to your retirement age. Because you retire when you are financially free. Hence, Life Insurance is not required during your retirement age.

# Splitting of Term Insurance

There are few who are apprehensive of relying on a single insurer. Hence, they try to split among few. But in reality, there is no logic in splitting. What is the guarantee that all insurers will accept or reject the claim?

# Stay away from riders

Never combine Life Insurance with General Insurance requirements. You will get better-featured covers from general insurers regarding accidental and critical illness covers. Hence, simply avoid riders.

# Never heed the aggregators choice

Nowadays there are so many online aggregators. You may not know that they act exactly like insurance agents. Hence, never rely on their claim. Do your own research. If you are satisfied, then only go ahead and buy. Refer to my post about the same “Beware of Insurance Comparison portals in India“.

# Know about Sec.45 of Insurance Act

After the recent clarification about Sec.45 of the Insurance Act, the customer became king. It states “No policy of life insurance shall be called in question on any ground whatsoever after the expiry of three years from the date of the policy, i.e. from the date of issuance of the policy or the date of commencement of risk or the date of revival of the policy or the date of the rider to the policy, whichever is later.”

Refer the complete post at “Term Insurance-Claim Settlement Ratio no more a big criteria“.

# Review your life insurance cover

Buying Life Insurance of Rs.1 Cr or Rs.3 Cr is not a one-time affair. You must review your life insurance requirement at least once in 5 years. If required, then you must increase the sum assured.

# Be cautious with premium payment

In case of term insurance, you have to be very cautious when it comes to the premium payment. It is always better to opt for yearly premium payment and also if possible make it automated by the way of ECS. If policy lapses due to your negligence, then you have to undergo medical tests and all kinds of stuff once again. If there are any health issues, then the insurer may reject to renew the policy.

# Never go for Telemedical Examination

Recently one of my blog readers pointed that few Life Insurance companies insisting just Telemedical Examination by questioning about your health details on the phone (Refer-Can I buy Term Life Insurance with Telemedical Verification?).

It may be the easiest process for you and for life insurance companies. However, I feel suspicious of such kind of medical examination. Because in future insurance companies may find 100000 reasons to reject the claim on health ground.

Instead, I suggest you to go for a medical examination. This will really clear the dust or doubt in your mind about future claim settlement.

Final Note:-The list of “Top 5 Best Term Insurance Plans in India 2021” is my personal choice and comfort with insurance companies and by verifying features. However, it does not mean that my selection will be the UNIVERSAL selection.

Hence, if you have a different opinion from my selection, then it does not mean you are buying the wrong product. My only concern here is not to shortlist “Top 5 Best Term Insurance Plans in India 2021”, but to give the gyaan which you must take into consideration before you shortlist your term life insurance.

Note:- From 16th April 2021, LIC is offering a standard term life insurance Saral Jeevan Bima (Plan No.859). Refer the details at “LIC Saral Jeevan Bima (Plan No.859) – Term Life Insurance“.

Recent posts:-

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

Can you please share 2024 updated blog for above list.

Dear Anil,

Sure.

thanks for your kind support to a policy buyer like me.

Dear Alkesh,

My pleasure.

Thanks a lot Basu. Can u Suggest few good Accidental Insurace Policies?

Dear Virendra,

Better you go with the company where you have health insruance.

Hello Sir,

I always read your article in case of any doubt/reference. Presently, I have a Kotak e-Term Plan which is to be renewed by 27th July 2022. While I was going through the Policy Wordings, I came to know that the Policy doesn’t have Payout option in case of Permanent Disability (though it has option of No EMI Payment further in case of that).

I just wanted to know whether Payout option in case of Permanent Disability should be considered seriously, as in case of a Lone Earner family like me, this will be equal to the case of Death. There are few policies of other companies which are providing payout in case of Permanent Disability or Terminal Illness. So, should I go for them or continue with the existing policy? Early response will be highly appreciated and thanked.

Thanks and regards

Virendra

Dear Virendra,

Rather than discontinuing the existing policy, make sure you buy separate accidental insurance. This will serve your purpose.

Dear Basu,

When I compared the quote online between multiple companies, i got around 30% less in Edelweiss Tokio when compared to icici, HDFC , kotak. Can I proceed with Edelweiss Tokio.? Why they are giving much lesser when compared to their peers? Is there a problem will I face in future

Dear Guna,

It depends on what type of mortality table they are using, their profit margin, and some other factors. Sadly we can’t question the premium rate.

Hi Sir,

Great analysis as always 🙂 … Would it be possible to review ‘navi’ health insurance as well?

Dear Sachin,

Sure will do.

Hello Basu Sir,

I took Max life insurance(plain term insurance without riders) 5 years back after seeing you article at that time, over these years my salary increased and I want to increase my sum insured. Could you please suggest whether I should increase my coverage in existing policy or take new policy from other provider.

Dear Abhinay,

Better to go with an existing insurer.

I agreed with most of your points. But I have doubts regarding one of your points – Stay away from riders (Never combine Life Insurance with General Insurance requirements. You will get better-featured covers from general insurers regarding accidental and critical illness covers. Hence, simply avoid riders). I think riders in term insurance are important as they give extra peace of mind and protection cover with some additional premium amount for critical illness, premium waiver in CI/ Accidental disability, terminal illness, etc.

Dear Sandeep,

Life Insurance is required for you for a limited period but the riders which you feel better to combine with Life Insurance are required for you throughout your life. How do you manage this?

Can You share your views on ABSLI digishield plan(Ease of claim, customer service etc), I am planning to take this , where Policy term is upto 75yrs(43yrs) Life Cover of 1Cr, Payment term 28 Yrs upto the age of 60 Yrs, that means I have to pay 45000*28.., From 61 year onwards I would get annual survival benefit of rs 144000/- till 75 or death, incase of death in b/w nominee gets lumpsum of sum assured less the survival benefit already paid..

Regards

Sreekanth

Dear Sreekanth,

May I know why you have selected this product?

thanks a lot Sir! I have Maxlife online term plan for 3 years now… I have a very impt question – I may be relocating to the US in the next few months so wanted to know what happens to my term insurance, medical insurance (individual) in that case? Will I be able to continue my policies in India? I’m in a dilemma…

Regards

isha

Dear Isha,

Yes, you can continue both policies.

thank you as always! if I have 3 individual medical policies (for me, dad and mom) apart from my employer cover – can I take one super Top up policy for 20-30 lakhs for all 3 of us? or should i take 1 for dad and mom and separate for me?

Dear Isha,

If you feel the current coverage is not sufficient, then you can take one super top up for you and another for your parents (combined together).

okay Sir, let me do some reading and decide. As both my parents have different health insurance policies… Religare (care) and another is a public sector company

Dear sir, How to issue the lic tech Term policy under married woman’s property act? I have tried to search for this since some time but no success. Even LIC customer care is clueless about this

Dear Ravi,

That option is not available online. You have to send an email before they issue the policy.

Sir I have taken eterm lic (825) plan and now lic introduced a new plan tech term(854) . The premium of tech term is less than eterm in terms of policy terms(yrs). Should I switch to new policy or run the old policy (eterm since 4 yes)?

Dear Abhinav,

If the premium for your current age is lesser than eTerm, then you can. But don’t cancel the existing one until the new policy is issued.

I liked the survival benefit option, but after doing some research, I decided to go for a simple term plan( half the premium) and invest elsewhere in mutual funds or shares..

Thank you

Dear Sreekanth,

Far better option.

Dear Basavraj ji,

Very informative article.

Dear Raghuram,

Thanks 🙂

Hello Sir,

Need your advice. I want to take another 1 crore insurance. Am the only earning member in my family as my wife is a home maker. I want to take your advice on the following:

1. Which company I should choose as the price very widely. Am considering LIC, ICICI and HDFC.

2. Should I buy accidental disability and terminal illness, critical illness add-ons

3. Should I take limited partner of premium to 60 years of age or full term?

4. Should I go for 70 years or 80 years?

LIC doesnt have disability and terminal illness benefit with their Tech Term.

Thank you so much for your help

Regards

Prasanna

Adding to the first point above, I have an existing Aegon Term Policy, Should I consider that as well?

Dear Prasanna,

Yes.

Dear Prasanna,

Go with the one where you already have a policy. The more you diversify the companies, the more work for your nominee in your absence. Don’t go for any riders. Go for a term of up to your working age.

Hello Sir,

Very Informative post. Thank You.

My question is – Is ‘Death due to Accident’ not covered in Basic Term Insurance Plan. What is the point in adding a Accidental Death Rider with a Term Insurance Plan? If a person dies due to Accident, his dependents will not get any settlement if he has not taken a Accidental Death Cover? Please guide.

Dear Hemant,

Yes, death due to an accident is covered under the basic plan. However, if you add an accidental rider, then along with the basic sum assured, your nominee will get an additional amount that is equal to an accidental rider.

Hello Basu,

Its been mentioned one should revisit the “Term Insurance” requirement every 3-5 years based on family requirements, if that so, will the existing insurer will allow to increase the coverage with additional premium or will it be new policy?

Thanks,

Ramesh

Dear Ramesh,

Sadly you can’t enhance the cover within the same policy. You have to buy a new one.

Hello Sir,

I have 2 questions/ doubts, please help me in resolving the same

1) What category should a person select if he is a smoker and has quit for few years now and If a non smoker starts smoking down the lane will his claim be disqualified

2) The settlement numbers shared above includes the settlements that has happened after court cases and out of case settlements? Cos I heard a lot of them dont pay and come up with some reason and drag the issue to the court and later settle for a very minimal amount

Dear Ganesh,

1) If you are sure that you will not smoke again, then mention non-smoker else smoker.

2) How come you assume that these settlements were only through a tough patches?

Hi, any reason for leaving out bajaj allianz ? They are one of the oldest insurance house, with decent track record. What are your thoughts on bajaj allianz smart protect plan ?

Dear Santosh,

No specific reason. If you have a belief in that company, then please go ahead.

Hi,

Is it best to pay for 10/15 yrs & get coverage till 60/70/75 years as we would be earning in this period ?

Plus these premiums offer discounted prices for 10/15yrs payment terms.

Do let me know.

Thanks,

Kunal

Dear Kunal,

Why a HURRY to finish it off your premium?

Sir why have you not taken Bajaj Allianz as one in top 5 it has good solvency ratio when compared to others just want to know whether it is a good company or not

Dear Rahul,

If you are comfortable with the Bajaj, then why not go ahead? I can’t list all as my choices.

This was very useful. Thank you

Hi Sir,

In one of the comments from last years post, you have mentioned that a claim can be rejected if some one hides any information for telemedical examination even after paying 3 yrs of premiums. In this years post you’ve said the contrary. Can you clarify, if someone go for telemedical or video medical and pay 3 yrs of premiums, can the claim be rejected on any grounds?

Dear Teja,

Whether it is TELEMEDICAL or PHYSICAL, if you hide the information deliberately then obviously your claim will be rejected. When I said that the contrary to this?

Apologies Sir, I might have read it wrong. So if one has provided wrong information by mistake at time of policy taking , can we update at later point or it is better to cancel the plan and take a new one.

Also I have a term insurance plan with Max, and i plan to take another plan, is it okay to go with Max or to go with another insurer.

Thanks for all your information over the years.

Dear Teja,

“can we update at later point or it is better to cancel the plan and take a new one.”-Better to update. If the insurance company not accepting it, then cancel it.

It is better to go with Max.

Thank you Sir,should we always go with same insurer for all our future plans?

Dear Teja,

Mostly.

Hi basu,

As you mentioned above that term plan should not exceed your retirement age i e 60. What if somebody(salaried person) is interested to do self employed business or the post retirement interests (which he could not complete due to service or lack of time), such interests may or may not be in favour of family members or dependents. At this time, if sudden death occurs, dependents (family members) or any single dependent (spouse) may suffer or face financial crisis.

Do you still suggest that life insurance is upto 60 age only. Or as a whole, the name ‘ life insurance’ itself covers a life….

Dear Rahul,

In many cases, you take up such hobbies or freelancing only when your basics are set (retirement fund is ready or no one is financially dependent on you). If this is the case, then life insurance is not required. If you find that because of your absence, there is a financial loss, then one can opt as per their suitability. However, once you are financially free (no one financially dependent), then life insurance is WASTE.

Some companies are insisting for telemedicals and some companies are not operating at all places.is it safe to go with telemedicals as per their requirement if they don’t allow for physical examination.

Dear Rahul,

It is all may be due to Covid. You can go ahead but declare the facts properly.

Hello, do you recommend policies which come with an increasing term cover and if so, which do you suggest?

Dear Korem,

Many of these increasing cover does not match with the real inflation. Hence, I would not suggest.

Mr. Basavaraj,

Thank you so much for timely updates on the list of Insurance. They have been most useful.

Request you to please write an updated article on Independent Critical Insurance and Accident Disability Insurance.

Dear Nilay,

Thanks for your kind words. Sure, I will write the updated posts on those two subjects.

If I choose Tele medical for my term plan, it can be under scanner after 3 years if any thing happens??

Dear Debasish,

NO.

Hello Sir,

This is very nice and useful Article as usual.

I have one question.

I have ICICI Pru iProtect term insurance. Currently I am living in UK so this is NRI policy, purchased in Feb-2020.

I have come to know that if NRI pays premium through SWIFT transfer (paying premium directly from foreign bank account) then GST on premium is exempted as GST is only applicable for sales in India, not out of India.

Is this true ?

Can you please provide some more details if you are aware of anything ?

Thanks.

Dear Jalpesh,

I don’t think so. GST is still applicable as sales happened within the INDIA.