Recently Government announced some changes to Post Office Savings Schemes interest rate calculation method and these changes will be effective from 1st April, 2016. Let us understand what are these changes.

1) Post Office Savings Schemes rates change on quarterly base–

The biggest change I can say is that the interest rates will change on a quarterly basis instead of yearly. Earlier interest rates on all Post Office Savings Schemes used to be changed every year and used to be applicable from next financial year.

However, from now onward the interest rate will be fixed on a quarterly base. So you may feel the fluctuation in your return in each quarter. Notification and effects of such change in interest on a quarterly base will be as below.

Therefore, the feel of security or constant interest income may vary from 1st April. But what is this FIMMDA month end G-Sec. rate?

FIMMDA (Fixed Income Money Market and Derivatives Association of India) is a voluntary market body for the bond, money and derivatives markets. They publish the Government Security rate. Based on these rates, the next quarter’s interest rate on various Post Office Savings Schemes be considered.

However, I am not sure of whether the average of last three months FIMMDA month end G-Sec. rate be applicable for next quarter or the only last month of a previous quarter only. Let us see how they calculate and arrive at the interest rate.

What is this G-Sec. rate?

It is nothing but a yield on Government security of the same maturity. The yield on bonds is inversely proportional to its price. Raise in interest rate will result in a fall in bond price. This will raise the yield. The reverse will happen when the interest rate starts to fall.

Let us say you have a bond with a face value of Rs.1, 000 and the interest (coupon) on this bond will be 10%. Therefore, if you bought it at face value and returns from this bond is 10%, then yield on such bond will be 10% (100/1000).

Now let us say RBI increased the rate of interest to 11%, then whether anyone try to buy such bonds, which offer less than the current market interest rate? Obviously, no, in that case price of such bond, which bears a face value of Rs.1,000 and coupon or yearly interest 10% will have to fall. Let us say it fell to Rs.900. Then yield will be 11.1% (100/900).

Why yield raised? Because the person who buy the bond which bears the face value of Rs.1,000, but currently priced at Rs.900 and the interest rate (coupon) on such bond is fixed i.e. 10%. Therefore, by investing Rs.900 one can get 10% return. Earlier you have to buy this bond at Rs.1,000 (face value) and return is 10%. Now, due to increase in interest rate and fall in bond price, the yield on such investment will increase. Hence, the fall in price resulted in higher yield.

2) Sukanya Samriddhi Yojana, Senior Citizen Savings Scheme (SCSS) and the Monthly Income Scheme (MIS) enjoys a higher interest rate than other Post Office Savings Schemes.

These three schemes are considered as savings schemes based on laudable social development or social security goals. Hence, the interest rates for these three schemes are over the G-Sec rate of comparable maturity viz., of 75 bps, 100 bps and 25 bps respectively. (100 basis point means 1%). This is also called as SPREAD.

So let us say FIMMDA month end G-Sec. rate for last quarter is 9%, then Sukanya Samriddhi Yojana will offer you 9.75% (9%+0.75%), SCSS will offer you 10% (9%+1%) and MIS will offer you 9.25% (9%+0.25%).

Remember that this will be only for a quarter. We don’t know the interest rate of these schemes for next quarter. So now onward the fluctuation in Post Office Savings Schemes rates will be on a quarterly basis.

There is no change in the spread for above three schemes. However, the change is in the quarterly interest rate declaration.

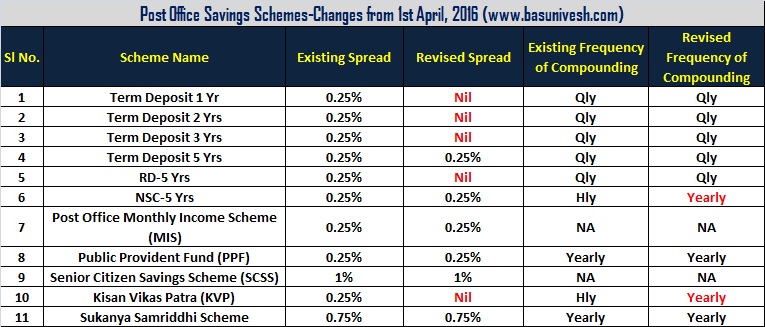

3) 5 yr Term Deposit, 5 years National Saving Certificates (NSC) and Public Provident Fund (PPF)

These schemes interest will also be declared on a quarterly base with a spread of 25 bps over and above G-Sec rate of comparable maturity. Let us say the G-Sec. interest rate for the last quarter was 8%, then these three schemes, offer the interest rate of 8.25% (8%+0.25%) for next quarter ONLY.

4) 1 yr., 2yr., and 3 yr. term deposits, KVPs and 5 yr Recurring Deposits (RD) fetch lesser returns

Earlier the interest rate on the above said Post Office Savings Schemes had spread of 25 bps over the comparable tenure Government securities. Now this is totally removed. So now these schemes, offer the same interest rate of banks for particular tenure.

5) The Effective interest rate on National Savings Certificate (NSC) and Kisan Vikas Patra (KVP) reduced.

Earlier the compounding of NSC and KVP was half yearly. Now the compounding will be YEARLY. What will be the effect?

Let us say the NSC offering you the interest rate of 8.5% and what will happen if we change the half-yearly compounding to yearly compounding? Half-yearly compounding will result in an effective return of 8.68%. If it reduced to annual compounding then the effective return will be same as that of what interest rate i.e. 8.5%.

Therefore, from now onward NSC and KVP will fetch you less than earlier.

I tried to highlight all these changes in below images with red colour.

6) Higher liquidity in Public Provident Fund (PPF)–

From now onward, one can close the PPF before the maturity. But this will be permitted in genuine cases like a serious ailment, higher education of children etc,. In addition, if you try to close the PPF before maturity, then there will be a 1% reduction overall amount as penalty. This closure is allowed only to those accounts, which completed minimum 5 years of a term.

1% reduction of interest from a whole amount as penalty for earlier closure is unwarranted. Because it is already set that such closure will be allowed in genuine cases. Then why such penalty clause?

Let us wait for the next interest rate declaration on 15th March, 2016.

I invested in NPS Tier I after my retirement at the age of 63 and investing some amount every month.I could see average return of 10% from the statement.

Can I continue?

Can I withdraw partial amount from Tier I

NPS after 5 years?

Please clarify

Dear DRD,

It is hard to say whether you should continue or withdraw. Because I am unaware of your financial life and requirements.

I AM SALES MANAGER IN B-B COMPANY .I WILL GETTING INCENTIVES REGULARLY DEPENDING UPON THE SALES .AND ALSO I WILL GET YEARLY INCENTIVES.I WANT INVEST PLEASE SUGGEST IN WHICH I HAVE TO INVEST PPF OR?

Dear Ramesh,

It is hard for me to suggest anything BLINDLY.

I opened SCSS a/c on 290316 & obtained premature payment on 260219. They deducted 1% of principal amount but they had not also paid complete interest wef 010119 to 260219. Are they right, please suggest.

Dear Rajinder,

Refer my earlier post “Post Office Savings Schemes (RD, NSC, MIS, SCSS)-Premature closure rules“.

Can RD account in Post Office be closed after 3 years (prematurely). Local PO is asking to open a SB account in PO for payment. Can amount be not paid by cheque to person concerned ? Is opening a SB account a must for refund of amount in RD account

Dear Prakash,

Yes, you can close it. Yes, Post Officials are correct.

Hi Basavaraj. Loved this post. I want to open SCSS with SBI, really confused if the rate of interest remains fixed or floating for the entire tenure once i open it? SBI says it is floating.

Dear Altamash,

Yes, it is floating.

I have to invest around a lakh for saving tax before March. Pl recommend the best option .

Achuthan-Without knowing much about your financial goals, I can’t suggest you anything. Also, do you feel it is the BEST strategy to invest in a product ONLY FOR THE SAKE OF SAVING TAX?

hi bashu Sir,

I have a completed FD on behalf of my Father Late with out nominee so tell me the procedure of withdrawal and about all supporting Docs.

tks, Sunil

9810282974

Sunil-His death certificate, FD certificate, legal heir certificate and the first legal heir’s KYC details.

Sir,

I opened SCSS a/c in Canara bank in DEC 2015.and received qtrly interest in 31 March around Rs.34,000. however in july the interest deposited was less amounting 32,000. Is rate of interst 8.6% declared on 1.4.2016 is applicable to SCSS A/C opened prior to 1.4.2016 also.Please clarify.Thanks

S.K.bhatnagar

Bhatnagar-The rate of interest must be the one which is applicable at the time of depositing. Hence, it must be equal. Check with bank.

Hi Basu,

Am planning to invest 20k per month for 1 year duration.

Could you please suggest me which plan or investment returns more with interest rates?

Firdous-FDs.

hello sir…if I decide to invest in post office rd/FD(5yr) before 31st march,will interest rate for whole tenure be fix or it will be change after April as per new rule???

Rajesh-It is fixed for next 5 yrs as per the rate on 31st March, 2016. You no need to worry.

thanks a lot sir

Dear Sir,

My RD account matures on April 30, 2016. What interest rate will apply!

Thank you for your help…Rajshri

Rajashri-It will be the interest rate offered while opening the account for you 5 years back, but not today’s interest rate So no need to worry.

Hi Basu,

Is there any scheme to satisfy below requirements

1) Target period 5 years

2) Applicable for Tax Exemption Under 80c

3) I can take money whenever i want

4) Good returns

Karthik-When you say tax savings, all product comes with lock-in.

Hi Basu,

Whether it is political related scheme or not for Sukanya samrudhi,,but i am interested for this 🙂

I have been investing 2000/- per month from past 1 year..But now i want to split this money into 2 ways.

1000/- in Sukanya samrudhi and 1000/- in PPF

1) Please suggest me is it good to Split? OR

2) can i continue in Sukanya samrudhi itself to invest 2000/- per month, because rate of interset is more compare to PPF.

Regards,

Karthik.

Karthik-If already decided, then why suggestion? Go ahead.

Hi Basu,

Yes..I wanted to invest money in Sukanya samrudhi,

but now i want to change my current paying amount(2000/- per month)

1) Please suggest me is it good to Split?

1000/- in Sukanya samrudhi and 1000/- in PPF

2) can i continue in Sukanya samrudhi itself to invest 2000/- per month, because rate of interset is more compare to PPF.

Karthik-Everything decided, then what doubt?

Dear Sir, I am 62 year old

plan 1 -I want to invest 2 lak RS in senior citizens saving account & the interest come in a saving account is reinvest in R.D

plan2rdeposit 2 lak in montly income plan & interest come is to reinvest in R.D

Sir, please tell me which plan is better.

Thanks

Want to open an PPF account for family i.e Self Wife and 2 Kids

Which is the best place to open PPF account.

Sachin-It is where you feel comfort (but not with Post Office).

say the best ways of high interest rates in fixed deposit

Sivalingam-Meaning of HIGH INTEREST RATES according to you?

Basu Sir , kindly clear my doubt regarding Post Office Monthly Income Scheme (MIS) which is of 5 years duration . I invested in 2014 and getting 8.4% percent interest monthly. So according to new rule does quaterly rate change will affect me also or whether applicable only to new MIS investment during that quaterly period. Thank you.

Rahul-I think it will not affect to you. But to the new investors from 1st April, 2016.

Thanks sir for replying my query

Hi Basu,

What is the present quarter G-Sec rate and where do i find the latest G-Sec rate.

Vinay-You can find that on FIMMDA portal.

I searched for it in the entire site but could not find the rate.

I feel it is not transparent and hope the govt. reconsiders this change.

Vinay-Let us wait till 15th March.

Hi Basu,

Post office information very useful. If I go with MIS, is it best best return ?. Please advise me

Nagabhushan-It depends on may things. How can I say blindly?

Very important

Hi bashu

I plan to invest 30 lac on nsc for 5 years which returns @10.54 at maturity. Is there any other profitable returns I get if I invest the same amount for 5 years. Ian ready for lock in period of 5 years. Kindly advise.

Regards,

Sudip-You can use short term debt funds which are bit tax efficient than NSC. However, returns are not guaranteed.