After the Budget 2022, what is the Mutual Fund Taxation FY 2022-23 / AY 2023-24? What is the new Dividend Distribution Tax on Mutual Funds and whether there is a TDS if we invest in Mutual Funds?

Refer to the Budget 2022 related post at “Latest Income Tax Slab Rates for FY 2022-23 / AY 2023-24 | Budget 2022 Key Highlights“.

Factors that determine the Mutual Fund Tax

First, let us understand what are the factors that determine Mutual Fund Taxation. The three major parts of these are below.

# Your Residential Status-Resident or Non-Resident (NRI)

Your tax will be based on your residential status. If you are a resident then the taxation rules will be different and if NRI then it differs. Hence, first, you have to make sure of what is your residential status.

# Types of Funds-Equity Funds or Non-Equity Funds-

Any fund which invests 65% or more in equity is called an Equity Fund. For example, large-cap funds, multi-cap funds, small and mid-cap funds, or equity-oriented balanced funds (where the equity exposure is 65% or more) are all called equity-oriented funds.

If the equity portion is less than that, then they are all treated as debt funds or non-equity funds. For example liquid funds, ultra-short-term funds, short-term funds, income funds, gilt funds, debt-oriented balanced funds, gold funds, funds of funds, or money market funds.

# Holding periods of Investment–

The holding period for Equity and Debt Funds will be different for taxation purposes. For equity funds, if the holding period is more than a year, then it is called the long term. If the holding period is less than a year, then such an equity mutual funds holding period is considered a short term. Whereas in

Whereas in the case of debt funds, a holding period of more than 3 years is considered as long-term. If the holding period of debt funds is less than 3 years, then it is considered short-term and taxed accordingly.

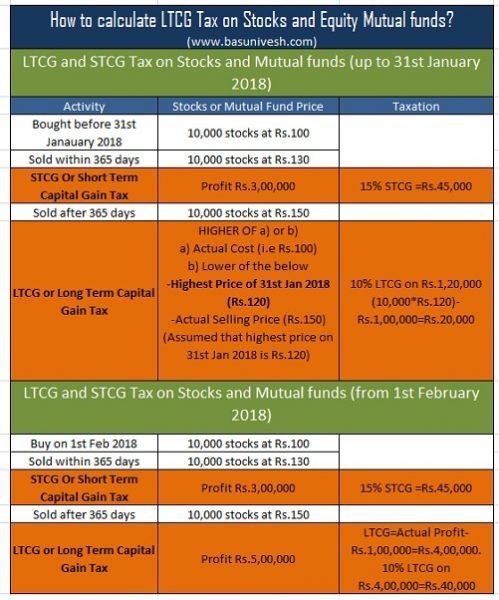

I will try to explain the same from the below chart.

Now you got the clarity on what will be STCG and LTCG. Let us move further and understand the Capital Gain Taxation for mutual fund investors.

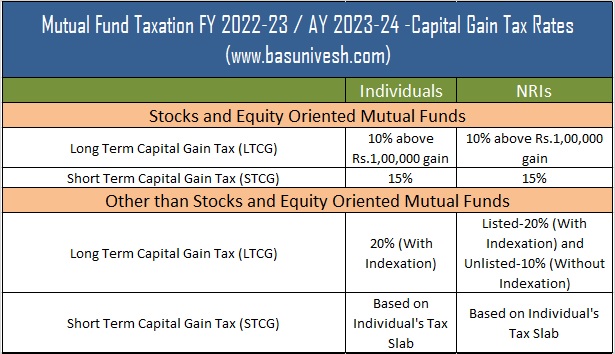

Mutual Fund Taxation FY 2022-23 / AY 2023-24 | Capital Gain Tax Rates

The biggest change in FY 2018-19 was the introduction of LTCG in Budget 2018 and later on during Budget 2020, two more major changes happened and they are as below.

# Abolition of Dividend Distribution Tax (DDT) in the hands of the companies.

Earlier the DDT Tax which used to pay was 10% (Actual DDT was 10% DDT+12% Surcharge+4% Cess=11.648%) for Equity Funds and 25% for Debt Funds (Actual DDT was 25% DDT+12% Surcharge+4% Cess=29.12%). This is the tax Mutual Fund companies used to pay and hence, it used to be Tax-Free in the hands of the investors.

However, due to the abolition of DDT from Budget 2020, now investors have to pay the tax on the dividend they receive. Such a tax is as per their tax slab.

# Introduction of Sec.194K and TDS on Dividend Income in Mutual Fund

With the introduction of new Sec.194K, Mutual Fund Companies will deduct the TDS on your Dividend Income if your such Dividend Income is more than Rs.5,000 in a Financial Year.

There was a huge cry and confusion with respect to this section. However, later on, CBDT came with clarification and mentioned that such TDS will be applicable for Dividend Options only.

Hence, any capital gain in mutual funds with respect to the sale or transfer of mutual funds will not attract any TDS.

Note:-Avoiding TDS does not mean avoiding TAX. As DDT was abolished in the hands of the Mutual Fund Companies, the Dividend income will be taxable as per your tax slab. If your tax slab is 30% and TDS was done at 10%, then your tax liability will not end there. You have to pay the remaining 20% Tax.

However, if your tax slab is 10% and TDS was deducted on such dividend income, then you no need to pay any further tax.

# Clarification regarding the taxation on Side-Pocketed or Segregated Mutual Funds

There was a concern on what should be the cost of acquisition and the date of acquisition with respect to the segregated or side-pocketed portfolio. This is cleared in the budget. I have written a detailed post on this aspect. Refer to the same:-

# Taxation on Side Pocketed or Segregated Mutual Funds

The Mutual Fund Taxation FY 2022-23 / AY 2023-24 and applicable Capital Gain Tax Rates are as below.

There is no change in Capital Gain Tax Rates from the last year. Hence, the old rates will be applicable for FY 2022-23 also.

Note-Surcharge @ 15%, is applicable where the income of Individual/HUF unit holders exceeds Rs. 1 crore. Also, a surcharge @10% is to be levied in case of individual/ HUF unitholders where the income of such unitholders exceeds Rs.50 lakhs but does not exceed Rs.1 Cr. Further, Health and Education Cess @ 4% will continue to apply on the aggregate of tax and surcharge.

As you may be aware that during Budget 2018, LTCG was introduced again to Equity Funds. Hence, let me explain the same on how to calculate the LTCG on Equity Funds as below.

Mutual Fund Dividend Distribution Tax (DDT)

As I pointed above, effective from FY 2020-21, DDT was abolished in the hands of Mutual Fund Companies. Hence, any dividend you receive will be taxable for you as per your tax slab.

At the same time, if your such dividend income is more than Rs.5,000 in a Financial year, then there will be a TDS @ 10%.

Security Transaction Tax (STT) for FY 2022-23

Security Transaction Charges or STT is the charges or tax when you buy or sell securities (excluding commodities and currency) through a recognized stock exchange. Therefore,

The definition of securities involves the below products.

- Shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate;

- Derivatives;

- units or any other instrument issued by any collective investment scheme to the investors in such schemes;

- Security receipt as defined in section 2(zg) of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002;

- Government securities of equity nature;

- Rights or interest in securities;

- Equity-oriented mutual funds

Therefore, whenever you buy and sell these securities through a recognized stock exchange, then you have to pay this STT.

Now let us understand the latest Security Transaction Tax (STT) applicable for FY 2022-23.

TDS (Tax Deducted at Source) Rates for NRI Mutual Fund Investors 2022-23

Below are the applicable TDS rates for NRI Mutual Fund investors for FY 2022-23.

STCG Equity-15%

STCG Other than Equity-30%

LTCG Equity-10%

LTCG Other than Equity-10% for unlisted and 20% for listed.

Conclusion:-

# As per me, the Growth Option is the default and best option from now onwards for mutual fund investors.

# Suppose you are investing in Debt Mutual Funds and for short term capital gains, there is no change at all in tax structure between dividend and Growth Option as both are taxed as per your tax slab. In fact if you opted for the Dividend Reinvestment option, such dividend paid by Mutual Fund companies will be the first taxable as per your tax slab. Hence, there is no logic in opting for the dividend reinvestment option.

# Regarding Debt Mutual Funds with long term capital gain tax, it is not wise to compare as the tax in case of growth option is 20% with indexation whereas dividend option is taxable as per your tax slab. The reason is hard to predict the indexation benefit and differs from case to case. However, to a certain extent, 0% or 5% tax bracket investors may opt for dividend option and benefit it from this as in case of growth it is 20% with indexation. But for higher tax bracket individuals, it is better to opt for growth options.

# If you are an investor of equity mutual funds and the holding period is less than a year, then the dividend option is better for those who are under a lower tax bracket (less than 15%. If your tax bracket is more than 15%, then it is better to choose the growth option.

# If you are an investor of equity mutual funds and the holding period is more than a year, then obviously growth option is the best one. Because up to Rs.1 lakh, there is no tax. However, in case of dividends, it is taxed as per your tax slab.

Hence, the clear winner is a Growth option, and better to stick to it rather than opting for the dividend option and running behind saving a penny and entertaining TDS and tax filing issues.

so sir the taxation will apply in MF A and not B where the difference is less than 1 lacs.. If one were to plan redemption in a manner where the redemption value for each mf and cost value is less than Rs 100000then LTCG can be avoided.

Dear Andy,

Sadly NO. The limit is not per mutual fund withdrawal but the total equity asset withdrawal in a financial year per individual.

One has multiple mutual funds in case if i were to redeem following equity mutual funds the 10% long-term tax will be on capital again will be levied on the difference on each individual fund it will be applicable to mutual fund A and not B is my understanding correct. Tax on mutual funds cannot be avoided right by investing right or redeeming from one mf and transferring to another scheme in the same mf or an other mf company.

Mutual fund A Cost 50000 Today’s market value 200000 Difference in redemption without indexation rs 150000

Mutual fund B Cost 50000 Today’s market value 80000 Difference in redemption without indexation rs 30000

Dear Andy,

Yes.

Dear sir, I invested Rs1,00,000 in canara robeco mutual fund 3 years log in period

After 3 years I got 1, 20,000. Whether Rs.20,000 is taxable income

Dear Kumaresh,

Yes.

Sir, interest from NCD of 3years or more obtained yearly,can it be treated as long term capital gain?Any tax benefit from such income? Please let me know.

Dear Oommen,

It is not treated as capital gain but as income from other sources (like interest income) and taxed as per your tax slab.

Sir, please let us know when will the Blog for Best MF SIPs for 2022 would be available?

Dear Suchit,

I know it was delayed. But will publish soon.

Dear Sir, I have CPSEETF more than 3 years. When I sell, do i need to pay tax if less than 1L rupees

Dear Girija,

I think it will be treated like equity fund and taxed accordingly.