Budget 2017 is finally out and now let us discuss the Mutual Fund Taxation FY 2017-18 and Capital Gain Tax Rates. There are no major changes. However, let us refresh it.

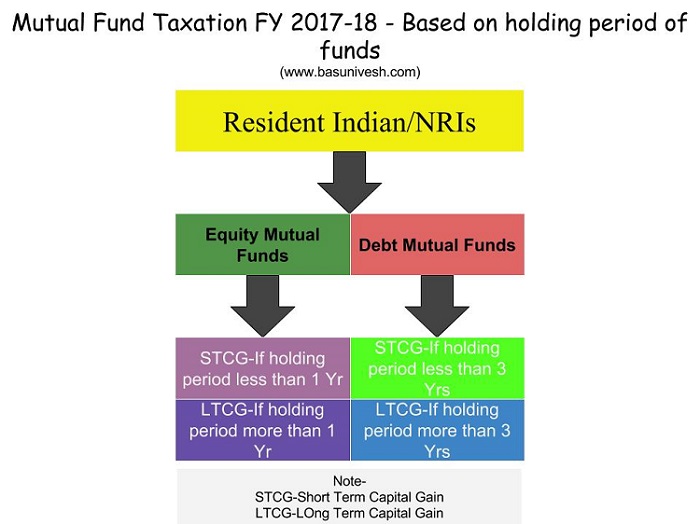

3 Factors that determine the Mutual Fund Taxation

First, let us understand what are the factors that determine the Mutual Fund Taxation. The three major part of these are below.

# Your Residential Status-Resident or Non-Resident (NRI)

Your tax will be based on your residential status. If you are resident then the taxation rules will be different and if NRI then it differs. Hence, first, you have to make sure of what is your residential status.

# Types of Funds-Equity Funds or Non-Equity Funds-

Any fund which invests 65% or more in equity is called as Equity Fund. For example, large-cap funds, multi-cap funds, small and mid-cap funds or equity-oriented balanced funds (where the equity exposure is 65% or more) are all called equity oriented funds.

If the equity portion is less than that, then they are all treated as debt funds or non-equity funds. For example liquid funds, ultra-short term funds, short-term funds, income funds, gilt funds, debt-oriented balanced funds, gold funds, fund of funds or money market funds.

# Holding periods of Investment–

The holding period for Equity and Debt Funds will be different for taxation purpose. For equity funds, if the holding period more than a year, then it is called long term. If the holding period is less than a year, then such equity mutual funds holding period is considered as short term. Whereas in

Whereas in the case of debt funds, holding period more than 3 years is considered as long term. If holding period of debt funds is less than 3 years, then it is considered as short-term and taxed accordingly.

I will try to explain the same from below chart.

Now you got the clarity on what will be STCG and LTCG. Let us move further and understand the Capital Gain Taxation for mutual fund investors.

Mutual Fund Taxation FY 2017-18 -Capital Gain Tax Rates

In below chart, I will show you the applicable Capital Gain Tax Rates of Mutual Fund Taxation FY 2017-18.

Note-Surcharge @ 15%, is applicable where the income of Individual/HUF unit holders exceeds Rs. 1 crore. As per Finance Bill, 2017, surcharge @10% to be levied in case of individual/ HUF unit holders where the income of such unitholders exceeds Rs.50 lakhs but does not exceed Rs.1 Cr. Further, Education Cess @ 3% will continue to apply on the aggregate of tax and surcharge.

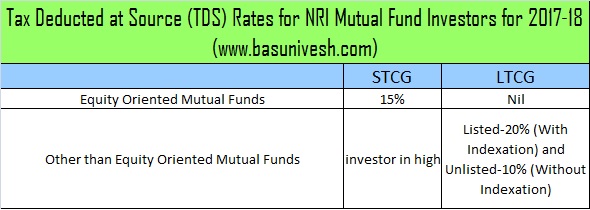

Tax Deducted at Source (TDS) Rates for NRIs

Now let us understand the TDS rates applicable to NRIs. Remember that for resident individuals, there is no TDS if you invest in Mutual funds. The rates of TDS for NRIs are as below.

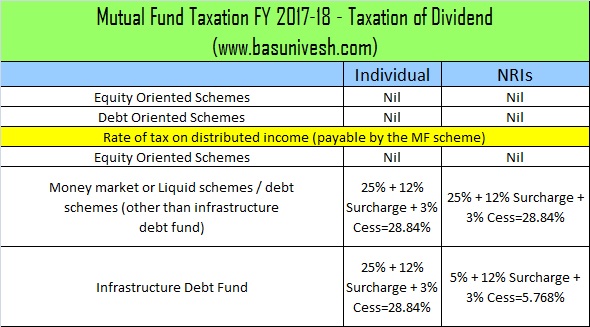

Mutual Fund Taxation FY 2017-18 – Taxation on Dividend

There are few investors who opt for dividend option in mutual funds. Hence, let us see the taxation on the dividend of such funds.

Security Transaction Tax (STT) for FY 2017-18 or AY 2018-19

Security Transaction Charges or STT is the charges or tax when you buy or sell securities (excluding commodities and currency) through a recognized stock exchange. Therefore,

The definition of securities involves the below products.

- Shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate;

- Derivatives;

- units or any other instrument issued by any collective investment scheme to the investors in such schemes;

- Security receipt as defined in section 2(zg) of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002;

- Government securities of equity nature;

- Rights or interest in securities;

- Equity-oriented mutual funds

Therefore, whenever you buy and sell these securities through a recognized stock exchange, then you have to pay this STT.

Now let us understand the latest Security Transaction Tax (STT) applicable for FY 2017-2018 (AY 2018-19).

Hope now you got the clarity related to Mutual Fund Taxation FY 2017-18.

Refer my latest posts related to mutual funds-

- Top 10 Best SIP Mutual Funds to invest in India in 2018

- Top 5 Best ELSS Tax Saving Mutual Funds to invest in 2017

- Top 5 Best Liquid Mutual Funds in India in 2017

- Top and Best Debt Mutual Funds in India for 2017

Hi Basavaraj,

I need to report LTCG on equity mutual fund (ard 2.3 Lakh), which ITR form I have to fill – ITR1 (as it asks for details of sec 10(38) ) or I have to fill ITR2.

Please advise.

Thanks

Dear Nitin,

Any other income sources for you other than this LTCG?

Can NRIs claim indexation benefit for LTCG (tax @ 20%) for debt mutual fund (e.g. SBI Debt Fund Series A-19, or ICICI Pru FMP Series 74 369 Plan I-G) ? Or, they have to pay tax @ 10% for LTCG. These funds were kept for more than 3 years. At redemption, as per account statement, no STT were deducted.

Debt mutual funds and FMPs from AMC’s (like SBI, ICICI) are considered listed securities or unlisted securities for purpose of computation of LTCG ?

Dear Manish,

Refer my latest blog post “Budget 2018 – Mutual Fund Taxation FY 2018-19“.

At Part ‘B2’ and ‘B3’ of the Schedule with ITR-2 Form, why there is no provision for indexation of Debt Mutual Funds held for 3 years and more? Also, what could be ‘cost of improvement’ of financial instruments like Debentures, Bonds, etc. in the hands of the holder?

Dear Chaudhuri,

Please recheck once again for provisions. Regarding cost of the improvement, this applies to physical assets but not for financial assets.

Sir,

I have purchased SBI Magnum Balanced Funds for Rs.5,50,000/- on 20/2/2017 and for Rs.4,00,000/- on 22/3/17 and as per Mycams, the period being shown as 330 days by today. In order to meet certain domestic urgency, I propose to sell some units valuing Rs.7,00,000/- on completion of 365 days (by end March, 2018). Kindly advice whether the said sale proceeds effects Exist Load of 1% and Post Budget 2018 Taxation Rules on Taxation / TDS. Kindly suggest. snmurthyk

Snmurthy-There is no exit load if you withdraw after 365 days completion. LTCG will be applicable if you withdraw the money on or after 1st April, 2018. There is no concept of TDS in mutual funds for resident Indians.

Thanx for ur reply sir.

If investment in FD is giving 6.25% guaranteed return…then why to liquid funds??

And about 20% tax for long term for liquid funds

Raj-Good question. If your holding period is more than 3 years, then Liquid Funds will have an edge over FDs in terms of taxation. Also, there will not be yearly TDS in case of Liquid Funds, which makes you more fund available each year for compounding. This is not the case. However, if you are uncomfortable with Liquid Funds, then stick to FD. There is no harm in sticking to FD for such short tenure.

Thanx sir.

And special thanx to make aware regarding hidden pinpoints while investing.

Misguiding at this stage may harm someone’s lyf.

Lots of appreciation for ur efforts.kp it up?

Dear sir thanks for info…

I’m having 5 lakhs…if I hv to go for debt fund rather than FD which is giving 6.25% interest….what will be your suggestion….

And what will be tax I have to pay after 3 yrs(liquid fund) considering avg.8-9 % returns per year?

Plz guide..

Raj-Debt Funds (Liquid Funds also) taxation is already explained in above post. I do not understand your doubt. Can you elaborate more?

I have invested Rs.20,000/- in SBI Magnum Balance fund (General) in January 2017. Now its worth in January 2018 is Rs.25,000/-.

Whether I have to pay Tax on Rs.5000/- profit, in this financial year ending on 31 March 2018?.

I am planning to close that after three years of deposit i.e. February 2020.

Mohammad-Taxation in Mutual Funds (Debt or Equity), will come into picture when you sell the units. Hence, you no need to worry on such appreciation in your investment.

Suppose tax is there for long term capital gains. If taxation is more,I think mutual funds will generate returns, similar to that of FDs, right. Is I am correct? In that case we will not be able to achieve our long term goals. Is am correct. Kindly advise.

Alfin-To arrive at your assumption, what return you expect from equity and also what tax % you considered?

Equity =12%.

Tax slab = 30%

Alfin-So as per your the LTCG applicable will be 30% if Govt started to tax?

LTCG = 15% on redemption(no tax according to year).

Ignore tax slab value(my mistake )

Alfin-Let us assume 15% LTCG tax, then post tax return of 12% MF return will be still at higher side than Bank FDs or PPF or any other debt funds right?

True. Let’s hope government will not do that.

Alfin-We can only HOPE that also a reality 🙂

Hi ! , Thanks for sharing valuable information . Just would like to know are liquid funds tax free if held for a year or less and if not, then how are they better than saving account as now few banks are already giving 6 to 7 % interest on amount over 1 lakh,

Thanks

Deepa-Liquid funds are taxed as debt funds. You have to use such funds to park your emergency fund or immediate cash requirement BUT not to earn more.

Hi,

If I am investing in liquid mutual fund with divident reinvestment option on daily basis. Do I need to pay tax at current income tax slab if I hold them less than 3 years or Mutual fund paying dividend distribution tax at 25% is enough?

please explain

Nilesh-You no need to pay the tax on the dividend paid out to you as it is tax-free in the hands of investors. But may I know the logic behind choosing this circus?

I need to park my part of my emergency fund in liquid MF which allows greater return than saving account and liquidity to get money next day. I may not hold them for 3 years, so will end up paying tax. Was checking if dividend options saves tax ?

Nilesh-I agree with your investment choice but not agree with the circus of DIVIDEND. Simply choose growth rather than the current option. Because in long run, each dividend re-investment will be considered as a fresh investment and taxed accordingly which confuse yourself.

Thanks for prompt reply.

In case of growth option it will taxed at my current tax slab then if hold for less than 3 year.

was not aware reinvestment is considered as fresh investment.

Do you have any other option to park emergency fund without tax implications?

Nilesh-When your priority is LIQUIDITY and SAFETY, then why bother about returns and taxation?

Dear sir,

If I change my individual account to NRO account what will happen to my existing Sips.

Gagan-You have to stop and re-start from your NRO account along with updating your KYC details.

Request you to clarify whether the dividend income from Mutual Fund ( equity/ Arbitrage/ Balanced etc) taxable. Is it to be clubbed with Dividend income from direct equity investments and does it attract tax of 10% if the total ( direct equity & MFs ) is over Rs 10 lakhs ?

Does dividend from Equity Mutual Fund attract different tax rate as vs dividend from Arbitrage, Balanced or Debt MFs ? Thank you

Lila-Dividend income from equity products is tax-free. However, if your such income crosses Rs.10 lakh in a year, then there will be a 10% TDS. However, incase of debt funds, it is tax-free in the hands of investors. But the Mutual Fund Companies pay the tax 28.33% from the distributable dividend surplus and then pay it to investors.

Could you please clarify how UTI Gilt and SBI Gilt (long term) have been giving a return of 12 to 17% when coupon/YTM on the government securities seldom exceed 7 to 8%?

Arvind-Refer my post “Top and Best Debt Mutual Funds in India for 2017“. In debt funds, higher the average maturity of the fund, higher the volatile. Hence, as now the trend (since 1-2 yrs) is downfall in interest rate, such funds who hold long duration bonds, will defenitely benefit and generate you higher return. Reverse is also true when interest rate cycle start to move up.

Hello – Do you have this explained for FY 2015-16 by any chance?

Manu-NO.

Hi,

I am currently invested into SBI Magnum Balanced fund. The SID says it would have an equity allocation of “Not less than 50%”. HDFC Balanced fund’s SID says its Equity allocation is “Not less than 60%”. HDFC Prudence says “Not less than 50%”. All these under normal circumstances.

The funds are said to be either hybrid – equity oriented or equity funds (in the case of HDFC). My question is, on selling them, will one be taxed as they do not clearly fall in the 65%+ Equity allocation catagory? Have I missed something in the finer print? Pls advise…

Gaurish-The fund is considered equity fund when they hold minimum 65% into equity and rest in debt. But do remember this definition “the percentage of equity shareholding of the Scheme shall be computed with reference to the annual average of the monthly averages of the opening

and closing figures”. Hence, the monthly average holding matters. Even if the equity allocation is less than 65% for one month, it is the average of the average monthly allocation that matters. They just claim that they have the mandate to move that much into equity and debt. But at the end to claim and consider the fund as equity, they do the average allocation to 65%.

Thanks for the clarification!

Dear Sir

If my mother wants to transfer her FD worth Rs. 20 Lac to me, will there be any tax implication for me?

Thanks

BRR-No. Because it is within the relation of the definition of FAMILY. Refer my earlier post for the same “Income Tax on Gift in India – Rules and tips to save tax“.

Hi, what would be the most tax efficient strategy for investing thru STP? As a retiree , if I invest a lump sum in say SBI Magnum Gilt Fund – Long Term Plan Divdend, and say transfer the funds to a Balanced Fund in next 12 months, would that me tax efficient?

Thanks,

Shailesh

Shailesh-What is your actual logic of investing? Why this circus of STP? May I know for what logic you thought of STP?

Hello Basu Ji,

Request you to review my portfolio: All investments are made using SIP for >15+ years.

Axis LTE – Direct(G) – 4000/month

ICICI Pru val Dicovery – Direct(G) – 2500/month

UTI mid cap – Direct(G) – 25000/month

Lump investment of 9000 Rs in DSPBR microcap. I was planning to start SIP in this but further investment in this fund has been temporarily suspended.

Debt investment in PPF.

Now, I am planning to add two more funds using SIP. Request you to suggest:

1. Franklin India Smaller Co – Start sip of 2500/month

2. Want to add one balanced fund. Can you suggest me from these 3: ICICI balanced/sbi magnum balanced/Tata balanced.

3. I am investing in Axis LTE from sept-15. I have read that performance of this fund has been deteriorated in last 12 months. But I think i do not need to worry if investment is for > 15 years. Please advise on this.

Mukul-One large cap, one mid cap and small portion of small cap fund are enough.

Dear Sir,

I am an existing active Mutual fund investor and my registered bank for all folios is NRE account as I am an NRI for the past 15 years.

Though I am an NRI, I have some investments (resident deposit) in Primary cooperative banks and its earnings are bit higher than the tax limit of 2.5 Lack per year. I do not pay any tax to income tax for these .After demonetizations, it is not safe to maintain and continue investment in such society as all cooperative societies and its investments are under the radar of income tax department. So, it is advisable to redeem/cancel investments one by one because I am not supposed to maintain such resident investment as per income tax law.

As I cannot deposit/convert these amount into existing NRE account ,I would like to deposit such amount in NRO and start investment in mutual fund through SIP. By doing this, I can gradually reduce the local resident amount and avoid queries from income tax if occur in later.

1. As all my Mutual funds folios are registered with NRE account, I would like to know whether I can Invest in the same folio from my NRO account too.

2. By doing this , Does it create any complication in my investment ? if yes, what are they ?

3. As I mentioned above, what is your opinion if I start investment from my NRO account instead of NRE ?

4. I hope I can deposit less than 2.5 lack per year in my NRO account and start SIP in mutual fund that will reduce my resident deposit amount that much. What do you think about this ?

I kindly request you to give me your opinion above my queires.

Thanks in advance.

Shankar V

Hi

Any comments on or can you please explain on the commission on MF

https://coin.zerodha.com/ IS claiming it will not take any commission how true it is

Thanks

Ankur-They launched the DIRECT platform. But there will be some flat fee. NONE on this earth is for SOCIAL WORK. They have to run their show.

Hi Basavaraj Tonagatti,

It is indeed a great post, specially Mutual Fund taxation for Individuals and NRI. Its so simple to understand. One quest. In MF if one acquires LTCG, does he still need to declare those gains in his IT-FR.

SRT-You can show such income in exempt income.

Can you post something similar for OCI card holders? Example: US citizen living/earning in India. Thanks

Unimax-Taxation for mutual funds for OCI Card Holders is not different. It is same for NRIs. Only the limitation OCI Card holders have is barring the purchase of agricultural or plantation properties.

Hi,

i have questions regarding NSE NMF II. It is a platform provided by NSE for all distributor for Mutual fund Investment purpose. Also, Investor (client) can use the same platform and invest in Mutual fund through distributor.

1. Are there any charges applicable to investor (client) to pay to NSE NMF or Distributor?

2. What if client chooses to break relationship with distributor and still want to access NSE NMF account? is it possible to access account? or that account will be deactivated?

3. if the online account is deactivated how can investor have access to mutual fund transaction and all?

sorry, but i am very to new to this platform and one of the distributor approached me and requesting me to join NSE NMF platform, so thought to check with you first 🙂

really appreciate your efforts to make awareness regarding financial sector within investor.

thanks,

Rajendra.

Rajendra-1) For investors no charges. You are indirectly paying for it through the commission your distributor earn from your investment.

2) I don’t think it is possible.

3) Through respective AMCs portal.

Instead of NSE NMF platform, I suggest you to use the MF Utility (for both direct and regular funds and which is free for both investors and distributors) or portals like FundsIndia (for regular).

I have one more question on point 3, is it possible to have MF utility account while having NSE NMF account via distributor? Can i have both at the same time?

So in future if i break relationship with distributors i can still access nd continues my MF.

Thanks,

Rajendra

Rajendra-Yes, you can have both the accounts.

What about arbitrage funds? any change in tax treatment in this budget?

Sures-Arbitrage funds still treated as equity funds and they enjoy same status like equity funds for taxation purpose for FY 2017-18. There is no changes in this.

Hi Mr Basu

First of all let me appreciate ur invaluable knowledge to all free of charge.

My Query is this that in last Financial year 2015-16 I paid taxes on Interim Relief (2000/- per month) given by my govt to itz employees till 7th CPC. Now 7th CPC implemented w.e.f. 1.1.16 n govt is recovering that Interim Relief amount now from my pay arrear. So how I get refund that tax amunt on that Jan-Feb 2016 Interim Relief amount?

Is there any rule to adjust that taxes in current financial year?

Thnx

Chaudhary-I think you have to revise.