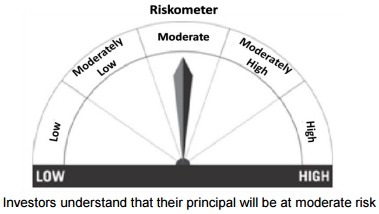

If you are already an investor of the mutual fund, then you may be familiar with the color coding of mutual fund schemes based on the risk involved. Such color-coding based on risk is called Product Label. However, effective from July 01, 2015, SEBI implementing a new Product labeling called Riskometer. Let us look into it.

First look at the earlier color coding or product labeling procedure.

You notice that all mutual fund categories are divided among three categories. Blue with low risk, yellow will be at medium risk and brown at high risk. You may notice this color coding when you go through the Mutual Fund Scheme Information Document (SID).

In my earlier post, I pointed that classifying funds only within 3 categories is not good. Because, Debt funds with longer maturity holdings are equally volatile like equity funds. To provide more clarity of risk, SEBI now come up with product labeling in 5 types than earlier 3 categories. Earlier color coding is now replaced with a new pictorial meter called “Riskometer”. These below categories are as below.

- Low-Principal at low risk.

- Moderately Low-Principal at moderately low risk.

- Moderate-Principal at moderate risk.

- Moderately High-Principal at moderately high risk.

- High-Principal at high risk.

For example, a scheme of moderate risk looks like below in newly implemented riskometer.

Implementation of this new riskometer will be applicable from July 01. 2015.

Will it really give you any indication while selecting funds?

To the certain extent, yes, you can judge the risk involved. However, while investing in mutual funds, how many of us go through the Mutual Fund SID (Scheme Information Document)? Because it consists of many pages and confuse the new investors? Hence, chances are high that you may miss this Riskometer.

I feel it is a good move that now the classification is moved from 3 to 5. However, investing blindly by following this riskometer is not at all right strategy. You have to analyze the risk and return for whatever category of funds you are investing.

Hence, I suggest you not to depend on this Riskometer only and select the fund. It just gives you a simple glimpse of risk, but not an in-depth.

Hi Basu,

I started mutual fund (direct) investing for attaining two goals detailed below.

Kids Education

25L in 8 Years with SIP Totalling 18000 in below funds

Canara Robeco BlueChip

Parag Parikh Flexicap

MO S&P 500

ICICI UST Debt Fund

Retirement

1.5 Crore in 20 Years with SIP Totalling 15000 in below funds

Axis BlueChip

IIFL Focussed Flexicap

Kotak Nasdaq 100

I already feel like this is too many funds. Is it possible to maintain single set of funds for two different goals ? How can i achieve that equilibrium of allocation without knowing if i would be dipping into the corpus of my retirement when doing a profit booking ?

Dear Jaimie,

Yes, you can have same funds for both goals by creating two folios under each fund.

Does the below MF SIP Portfolio look good for annualized 25% return in 8-10 years time?

Goal: 20+ Lacs

Total Investment: Rs 10K / month.

Equity+Debt:

SBI Bluechip fund: 3000 | HDFC Mid Cap Opp Fund: 1000 | DSP Micro-cap fund: 2000 | HDFC Balanced Fund: 1000

Debt:

Birla Sun life Floating rate long-term plan: 1000 | Birla Sun life Short Term: 1000 | SBI Magnum gilt fund: 1000

Risk appetite: Average

Somenath-25% return expectation? How you selected this number?

Dear baswaraj,

I am non resident Indian and have read through most of your articles, thanks for your help for suggesting good ideas on investments & financial awareness.

I have following Mutual funds with investment percentage , some of them started last year, I have horizon of 10-15 years.

Could you please suggest your views whether I should continue investing in same funds. All funds are under direct plan growth option.

1. DSP blackrock microcap MF – Lump sump investment 28.5%

2. Axis long term equity fund – Lump sump investment 4.4%

3. ICICI prudential focused bluechip MF – SIP 1000 per month 8.6%

4. Canara Robeco emerging equities fund – Lump sump investment 4.3%

5. Reliance gold savings fund – Lump sump investment 19.9%

6. Reliance small cap fund – Lump sump investment 21.2%

7. SBI bluechip fund – Lump sump investment 4.6%

8. SBI magnum global fund – SIP 3000 per month 13.5%

Could you please check and suggest if you have any best fund for investment required to be added in my portfolio.

Thank you in advance,

Chetan

Chetan-Three small cap funds(DSPBR Microcap, Canara Robeco Emerging equities, Reliance Small Cap), two large caps (ICICI and SBI Bluechip) and Reliance Gold Savings Scheme actually required? Think and decide. Maximum you can have around 3-4 funds. Also, where is your debt portfolio?

Dear Baswaraj,

Thanks for your reply,

I do not have debt portfolio, could you please recommend.

Thanks,

Chetan

Chetan-Use short term debt funds and PPF (if you have goals more than 3 years). For short term like less than 3 years, use Bank FDs or RDs.

Hi Vasu,

I am now in dilemma, I have below SIP funds running for last 4 years, please suggest me if and I should change it now.

1. HDFC TOP 200 – 2K

2. HDFC Prudence – 3K

3. IDFC Premier Equity Fund – 2K

4. ICICI Prudential Value Discovery Fund – 2K

5. ICICI Prudential Focused Bluechip Equity Fund -2K

I would like to continue my SIP for another 10 years with same above amount or may be i can another 5K per month to above amount.

Could you please help me to re-arrange my portfolio in order to make it balance?

Note – i am thinking of changing all my regular SIP to Direct SIP in January. So keeping in mind for going for Direct investment instead through demant account, i want to re-balance my portfolio.

Please help in above and adjust it?

Also, i can notify HDFC Top 200 is not doing well, is it wort to continue there? if i need to discontinue or switch fund then which fund I should move my HDFC Top 200 invested money?

Appreciated your help as always.

Thanks

Raj

Raj-Retain either HDFC Top 200 or ICICI Bluechip. In my view I still stick to HDFC rather than ICICI. Rest of the funds are fine.

Hi Basavaraj,

Thanks I will keep HDFC.

How about other MF?, Shall i switch HDFC Prudence to HDFC Balanced fund?

Again, one more info i missed to shared with you. My Age is 38, and plan to continue above SIP for another 10years minimum. Could you please let me know what should be my % of distribution of above 11K among Large Cap, Balanced Fund and Mid/Small cap funds?

Note: I have plan to add another 5K from next january in Mutual Funds i.e. monthly I will invest 16K in Mutual funds.

Again JFYI, i will keep continue invest 1.5L in PPF also my company add 48K(both mine and company contribution) PA into my PF account.

thanks

Raj

Raj-Continue with HDFC Prudence. If your timeframe is 10 years, then try to incline more towards large cap and balanced fund rather than small and mid cap.

Thanks Basavaraj for the tips,.

Hi

one of my dad advisor has made me to make investments in below funds .

Birla sunlife MNC Fund – 4k

Axis mid cap opportunities – 8k

Would you recommend this funds, should I continue?? how are they performing?

Please help me with your inputs

Thanks

Satish

Satish-How long you want to stay and on what base he selected these funds?

Hello Sir,

I am looking for a investment horizon of 20 t0 25 years from now, I want to build a corpus for my retiremnt. I have made following sip investments

ICICI Pru Tax Plan – Regulr plan growth 3000

reliance liquidity fund growth plan growth option 4100

icici pru balanced advantage fund regular plan growth 3000

I would like to know given my investment horizon is my portfolio ok or should i invest in some more mf’s, pls request your suggestions and advice …

Neil-How you chosen these funds? ICICI funds for tax planning as well as investment? If so then continue. Reliance fund meant for keeping aside your short term money or emergency money as it is liquid fund. Hence, stay away. ICICI Balanced fund is good but I suggest HDFC Balanced Fund. Select one large cap and one small and mid-cap fund from above list. Invest more towards HDFC to match your overall portfolio exposure of debt at around 30%.

Hi Sir,

Thank you for your prompt reply, further could you advise fund names for large cap & small & mid cap funds pls and also what should be sip amount as i am long term player in these…

Thanks

Sir,

I want to invent in Mutual Funds for 10+ Years,I have identified 2 funds from each sector, need your suggestion and comments to choose one from each or Best funds.

Large Cap:SBI blue Chip

Birla SL Frontline Equity

Mid/Small Cap:Franklin India High Growth Companies

ICICI Pru Value discovery Fund

Small Cap:DSP BR Micro Cap

Frankline India Small companies

Please suggest ..

Pranjali-But few funds like Franklin are now under small/midcap category. Also, why you opted two funds within a category?

Sir ,

Best on last 5 yrs performances i have selected these.

Large Cap: SBI blue Chip

Mid/Small Cap:Franklin India High Growth Companies

Small Cap: DSP BR Micro Cap

Pranjali-Minimum should be 5 years. Look back for long tenure like 10, 15 or for 20 years period. This gives a good indication of how the fund is performing.

HI

Iam new to mutual funds and planning to invest in the following funds

Franklin india high growth companies fund (multi cap)

Franklin india smaller companies fund (mid & small cap)

Mirae asset emerging blue chip fund (mid & small cap)

Axis long term equity fund(ELSS tax saving)

iam looking to invest in SIP 6000 rupees each in above mentioned funds . iam planning for long term(15 years) .

Since iam planning for long term let me know should i go for Axis ELSS fund or not ?

Also please let me know if above mentioned funds have proper diversification?(Equity and debt)

Siva-How you selected these funds as you yourself claiming that new to MF?

Hi Basu

I selected the funds after going through Value research online website and CRISIL

P/B P/E SD Sharpe ratio Beta Alpha

Franklin india high growth companies fund (multi cap) 3.2 23.7 15.34 1.62 0.99 15.36

Franklin india smaller companies fund (mid & small cap) 3.4 22.3 16.2 1.82 0.97 20.13

Mirae asset emerging blue chip fund (mid & small cap) 3.42 23.43 15.34 1.88 0.91 19.24

Axis long term equity fund(ELSS tax saving) 8.55 35.3 13.43 1.76 0.88 15.1

Checked portfolio overlap for above mentioned funds and its below 20 % for all the funds

After verifying the analysis total average mid &small cap investment % is 57 and Gaint &Large cap investment % 43 for the funds selected

i selected Small&midcap because iam ready to take risk and since iam looking for long term investment i think i will get better returns (as per the previous 10/5 year returns)compared to Large cap funds

In case of Axis long term equity fund for the following synopsis i got about this fund in Value research

“The outstanding performance is mainly due to the steady increase

in small- and mid-cap stocks in its portfolio, which was initially tilted

towards large-cap stocks. Currently, the fund holds around 43 per cent

mid- and small-cap stocks in its portfolio. The large presence of small and

mid-cap stocks and such aggressive positioning make it a risky bet

and suitable only for investors with a higher risk-taking ability”

Hope i made my point clear to you .

Please give your suggestions and if any mistakes in my invest plan

Regards

Siva

Reddy-But to you feel having two funds in same category really a good sign? What if the same valueresearch suddenly change it’s view on Axis? Will close the investment and come out?

Hi Basu

I selected 2 Mid and Small cap funds for the following reason

The Mid & small cap funds i selected have less than 20% portfolio overlap i.e both the funds are investing in fairly different sectors .

If i opt for only 1 fund and if it doesnt perform as expected then i will loose all the money invested in the fund .

By investing in 2 funds in the same category (investment overlap <20%) in my view iam reducing the risk . if one fund doesnt perform well the other fund might make up for the loss .

For the above mentioned reason i contradict with your ( 1 fund in 1 category theory).

Coming to Axis ELSS fund iam not God and i cant predict future . iam trying to analyse based on the previous performance and invest in the fund .

To be frank iam not happy with the reply i got from you for one main reason

I asked you a question (to help me out based on your experience and expertise) ,instead of suggesting better options you are asking me questions

At the end the aim is to have constructive discussions and sharing of knowledge and as a forum manager you are the one who should give clear cut solutions to the problems we( new investors )come up with

regards

Siva

Siva-By investing in 2 funds in the same category you are reducing the risk?? But what about the overall portfolio risk? Yes, I ask plenty of questions. Because mere two lines sharing, I can’t judge your requirement or your financial details. If you are expecting some readymade answers then SORRY. Without knowing fully, I can’t guide you. It may be harsh to you, but you will understand my point down the line 🙂 Whether your doctor prescribe medicines without understanding the cause?

Think and decide !!!

Hi Basu

what information should i provide so that you will come to know about my financial status and give me the correct medicine

Iam not asking for readymade answers . Iam reading the mutual fund sites as much as i can and from my understanding i came to above mentioned conclusions . If you see some thing wrong in it why dont you point out and give better solution.

When you think even by considering 2 Mid & small cap funds i cant avoid overall portfolio risk then why dont you suggest in which way i will be able to manage risk

Iam not asking you to tell me in which mutual fund should i invest . iam asking you what kind of funds should i go for ( balanced , diversified equity etc ) and how should be the allocation (equity ,debt etc)

Regards

Siva

Siva-Go through from your first comment to the last one. How I dig into the information about you. Also, go through your first comment, you just mentioned few funds. How can I know that how you selected these funds? Many investors run behind funds based on STAR RATINGS also few select ELSS funds only thinking that ELSS have just 3 years lock in, whereas other tax savings options are LONG TERM. Hence, it is my right to understand you better before giving you suggestion.

Why I suggested less exposure towards small/midcap? I know the majority of MF investors first choice is to look for fancy returns like 30-40% return. Definitely the small/mid-cap funds catch their eyes. But they forget that high return always come with high risk also. That is the reason, I am not a fan of small or mid-cap. However, for better diversification one fund is enough. Investing in two funds may give more exposure towards that sector (when I consider overall portfolio).

Rest is left with you to decide. Because you know best than anyone on this earth about your own RISK taking ability.

Hi Basavaraj,

I have been investing in MF from last 5 years.Here is my summary.All are Dividend Re-investment.

1) Rs 2000 each in HDFC TOP 200 & BSL Frontline Equity (started investing from April 2010 and still continuing).

2) Additional Top up of Rs 3000 each in HDFC TOP 200 & BSL Frontline Equity (started investing from June 2014 and still continuing).

3) Rs 5000 each in HDFC -MID-CAP opportunities & Franklin India Smaller Companies Fund (Started from June 15 and still continuing).

Total investment towards MF is Rs 20,000 per month.My Question is as below

1 ) whether quality of my fund choosed is Good enough for an Investment period of 10 to 12 years minimum ?

2) Is my Portfolio with Proper mix and so I need to add any other funds to it ?

Regards,

Swapnil

Swapnil-I think you have to retain all funds. But if HDFC Top 200 Fund not perform well continuously then switch to some other large cap. Also, there is no such difference between dividend reinvestment and growth, but I prefer growth. You can check portfolio overlap from my earlier post “How to compare Mutual Fund portfolio overlap?“.

Hi Basavaraj,

Thanks I agree with you if HDFC top 200 may not do good i would switch to other large Cap in future.

1 ) In that case should i transfer all the money invested in this fund to new large cap or should I start fresh in new large cap without pulling any fund from earlier invested money in HDFC Top 200.

2) Also should I start any of Balance fund of approx 3000 per month as long term investment ? Should Balance fund be in my above portfolio to complete the portfolio since i have Large Cap and Mid & small cap .

Sapnil-Switch all invested to new fund. Balanced fund is required because that fund will provide you the cushion of 35% debt. This will give debt diversification and provide a tax-free return (which is not possible with investing in separate debt funds).

Hi Basavaraj,

Thanks for wonderful advice.

1 ) I Would definitely start Balanced fund SIP very shortly.Could you recommend couple of Balance fund which I should look for.

2 ) If I want to maintain the portfolio and need to invest Rs 100 as total in Mutual Fund via SIP What should be my % allocation in Large Cap,Mid & Small Cap & Balanced Fund as Thumb rule ? The purpose of asking this question is to understand % diversification across the Portfolio for long term investment of 10 to 13 yrs.

Regards,

Swapnil Jadhav

Sapnil-1) HDFC Balanced Fund. 2) If your time horizon is around 10-13 years then invest more towards large cap and balanced funds and part into small and mid cap fund. For example, 40% in large cap, 40% in balanced (this creates a cushion of around 14% of your overall portfolio into debt. But I feel ideal should be around 30%. Hence you can increase more towards balanced)and 20% in small/mid cap.

Hi Basavaraj,

I would be starting a SIP of HDFC Balanced Fund from next month of Rs 15000.

1 ) Need your advice whether investing all the Rs 15000 via monthly SIP in HDFC Balanced Fund would not be risk or should i split it into 7500 each with balanced fund only but 2 different house (E.g HDFC & Franklin).

2)As you mentioned in general you prefer Growth over Dividend reinvestment , Could you elaborate what the difference between Growth Vs Dividend re-investment in long term span of 12 to 15 yrs.

Since all my earlier/Current investment are Dividend reinvestment only.

Regards,

Swapnil

Swapnil- 1) One Balanced fund is enough. If you still feel scary then opt two but check portfolio overlap.

2) There is no such difference. You can opt either one (This considering as an equity investment and holding period is more than a year).

Hi Basavaraj

I wanted to split my investment for balanced fund between HDFC and Tata Balanced fund,But i have a query here,

HDFC mutual fund has Dubai office here and I can go and get directly get the SIP done without any charges but for Tata balanced fund i need to go via Barjeel Geojit Securities LLC ( joint venture between Sheikh Sultan Bin Saud Al Qassemi and India based Geojit BNP Paribas Financial Services Limited).

Now Geojit is saying they would be charging around 0.5% to .75% commission on my monthly SIP.

1) Are they like Karvy ?

2) Don’t you think above commission too high and also would be there any additional charges which might be hidden if I go via Geojit ? Do i need to ask any specific Question to them ?

3) Now few of earlier investments are direct and few of them through one of my friends CFP bank in india and now this new Geojit.So even though I will get consolidated statement what would potential loss/problem I might face if my investment happens via different mode.

Swapnil-Stick to HDFC.

Thanks I invested in HDFC Balanced as per your advice.

Hello Basavaraj ,

I needed your advise on the MF I am planning to invest into , I am a moderate/conservative investor and planning to invest 20 lacs over a period of 15 years into following fund each with 2k per month.

Equity

HDFC Top 200 ( Large Cap )

Franklin India Prima Plus Fund ( Large & Midcap )

ICICI Prudential Value Discovery Fund – Growth Plan ( Small & Midcap )

Debt Conservative

ICICI Prudential Balanced Advantage Fund – Regular Plan

ICICI Child Care Study Plan

Birla Sunlife Dynamic Bond Fund

Considering I am a conservative investor would you suggest the above fund is the right choice , If not can you suggest any alternative ?

Joseph-How you opted these funds?

Basavaraj , I did my own analysis based on open source information when option for these funds , Not sure if these are the right ones to go for.

Joseph-Go for large cap like Franklin or ICICI Bluechip, retain ICICI pru discovery. In debt category try to invest in short term debt funds rather than long term or income funds.

Hi

Needed your suggestion on my current MF portfolio and future plan:

Current- Total Rs 10,000 monthly

1) HDFC Top 200- Rs 2500

2) HDFC Prudence- Rs 2500

3) HDFC Balanced- Rs 2500

4) IDFC Premier Equity A- Rs 2500

Going forward- plan is to invest Rs 25,000 monthly. Investment horizon atleast 20 years- I am 34 now.

a) Are the above MFs ok? HDFC Top 200 has been a laggard- should I continue or stay invested?

b) I understand I am invested in two balanced funds- hdfc prudence and hdfc balanced- should I exit one or continue investing in both? Should I increase my contri?

c) If I look at HDFC Top 200, balanced and prudence- am I right to say that I am overinvested in large caps ( ignoring the debt allocations of large caps) and trying to overheadge myself? I am 34 years now

d) I like HDFC stable- moreover I am an NRI and already created HDFC Direct account- so easier to open a new SIP through HDFC- am I being foolish by investing only in HDFC AMC?

e) I am planning to invest additional Rs 15,000 per month in SIPs and I am building a retirement corpus. Would adding more large cap and mid cap fund be good? my plans are as follows:

– HDFC Midcap- Rs 2500

– Sundaram Select Midecap- Rs 5000

– Franklin bluechip- Rs 2500

– Any others (including increasing SIPs in exisiting MFs….would like to add varied and MFs which divrsify my porotfolio and gives aggressive returns….)- Rs 5000

– For debt- I am looking at PPF + NRE fixed deposits 1-2 years (both tax free)- should I consider liquid/ short term debt mfs?

Regards

Rohit

Hi

Needed your suggestion on my current MF portfolio and future plan:

Current- Total Rs 10,000 monthly

1) HDFC Top 200- Rs 2500

2) HDFC Prudence- Rs 2500

3) HDFC Balanced- Rs 2500

4) IDFC Premier Equity A- Rs 2500

Going forward- plan is to invest Rs 25,000 monthly. Investment horizon atleast 20 years- I am 34 now.

a) Are the above MFs ok? HDFC Top 200 has been a laggard- should I continue or stay invested?

b) I understand I am invested in two balanced funds- hdfc prudence and hdfc balanced- should I exit one or continue investing in both? Should I increase my contri?

c) If I look at HDFC Top 200, balanced and prudence- am I right to say that I am overinvested in large caps ( ignoring the debt allocations of large caps) and trying to overheadge myself? I am 34 years now

d) I like HDFC stable- moreover I am an NRI and already created HDFC Direct account- so easier to open a new SIP through HDFC- am I being foolish by investing only in HDFC AMC?

e) I am planning to invest additional Rs 15,000 per month in SIPs and I am building a retirement corpus. Would adding more large cap and mid cap fund be good? my plans are as follows:

Additional Rs 15,000 SIP monthly

1) HDFC Midcap- Rs 2500

2) Sundaram Select Midecap- Rs 5000

3) Franklin bluechip- Rs 2500

4) Any others (including increasing SIPs in exisiting MFs….would like to add varied and

MFs which divrsify my porotfolio and gives aggressive returns….)- Rs 5000

5) For debt- I am looking at PPF + NRE fixed deposits 1-2 years (both tax free)- should I consider liquid/ short term debt mfs?

Looking for your kind reply

regards

rohit

Rohit-Continue HDFC Top 200. Restrict your investment to one balanced fund. For your fresh investment, you can use the same funds. Adding more funds may not be wise. How can you open PPF (being an NRI)? You can include short-term debt funds in case you want to manage portfolio perfectly like equity:debt.

Hi Basavraj

Thanks. I had opened the PPF account while I was working in India. Hope I can still invest in the same account even being an NRI.

regards

rohit

Hello Basu

i am invsesting in SBI FMCG fund from last 29 months 2-3 days ago it fall about 10 rs

i actually already decided go out from it but on 29th may it fall about 10 rs and my profit / loss is 0 rs

now i am confused that should i continue in it or i stop investing in it and wait for its NAV increase or should i accept that in this fund i gain nothing and come out of it totally .

please guide me ASAP its very urgent for me because personally i feel a mutual fund never down like this except they give dividend.

please reply ASAP.

thank you

NIitish kumar

Nitish-You are acting like trader than a investor. For investor day to day fall not matters. Hence, without knowing your requirement of holding this fund, I can’t guide you.

Hi ,

I have been following this blog from past 3 Months thoroughly and have helped to increase my financial knowledge.

I have planned to Invest in ICICI Prudential Wealth Builder 2(ULIP Plan)? Any Comments on It?They Claiming their Maximizer Fund V is yielding great returns Ur Help will be greatly appreciated.. I am 23 Years of Age and have planned for a Tenure of 10Years. What premium payment option you would prefer?

Thank You.

Prithivi-I am against a product which combines INSURANCE+INVESTMENT. ULIPs are hard to track and you can’t come out easily (without any penalty) to switch funds. You have to satisfy with their choice of few funds. Whereas, in case of mutual fund you can switch either the fund or company itself.

hello,

I invested in Bajaj Alliance Insurance(Bajaj Alliance Unitgain) for tax saving way back in 2006-09.

After a long gap now i want to invest in MF’s thru SIP. Should i hold on to it and reinvest in other Mutual funds.

I have enough life insurance coverage. I am looking at atleast 5 year investment period.

Rajasekar-What you invested is not a mutual fund but a ULIP plan. Check the performance and decide. If your time horizon is just 5 years then I suggest you not to enter equity.

Hi,

I am following your posts and they are very helpful.

My age is 24 and my salary is Rs. 50,000/- per month.

I have term insurance. I don’t have any other investments. Currently I am investing only in chits and RD.

I need help to invest Rs. 5000/- PM in mutual funds with tax savings.

And I need help to find good retirement plan.

Kindly advise. Thanks in advance

Regards

Avinash

Avinash-Whether you have enough Life, Health and Accidental Insurance coverages? If not then first fill that gap. Create an emergency fund of 6-12 months of household expenses. Then start investing in mutual funds or any other products.

Hi,

I have taken HDFC Income plus term insurance. For health insurance my company and my wife’s company provides insurance.

Kindly suggest on accidental insurance. For house hold expenses I don’t have liquid cash but do have some gold which will be enough for 12 months household expenses in case of emergency. Please advise if it is not a good idea to depend on gold savings.

Regards

Avinash

Avinash-What about health insurance once you retire from your work? It is tough to have insurance at that time. Because your health risk will be at higher and companies may decline to issue health insurance. Hence, it is better to have separate insurance. All general insurance companies offer accidental insurance. Buy the product based on your budget and comfort with the company.

Gold for the emergency? Is it possible to liquidate your gold in midnight and provide it to your immediate emergency.

Hi,

Thanks a lot for your valuable suggestions.

Kindly advise on best health insurance for family and accidental insurance. I can pay max Rs. 1000/- per month for both of them.

Regards

Avinash

Avinash-Please read my earlier post “IRDA Incurred Claim Ratio-How to choose the best health Insurance?“.

Thanks alot

Hi ,

Im closely following your group i had a query in NPS can you check and revert back

Not an objective of launching NPS-LitePFRDA

a.to make small investments viable to low administration charges

b.To Harness theout reach& Capacity of govt operated schemes

c.to include majority of unorganized workers in this scheme& effectively harness govt swallabh scheme

d.To popularize the already launched nps by making some of its provision

Thanks in Advance Please revert me back @[email protected]

Mohan- a.Whether you invest only because it offers low charges? b. Why to be our investment scapegoat for Govt harness? c. But what about taxation, lock in issues and the fund manager activeness? d. Unable to understanding your exact requirement.