Based on the Budget 2016 proposal, PFRDA came out with the procedure of how to move or transfer from EPF to NPS. It is a one-time process and now you can get rid of EPF and move to NPS easily.

If you are the EPF or Superannuation contributor, then you can now move to NPS (ONE TIME) without any hurdle. Let us see the procedure of this process.

How to move or transfer from EPF to NPS?

As I pointed above, on 6th March 2017, PFRDA announced the guidelines for the move or transfer from EPF and Superannuation Funds to NPS. Remember that this facility is available only ONE TIME to an individual.

5 Steps to move or transfer from EPF to NPS

I try to explain the process easily using below image.

Step 1-You must open NPS Tier 1 Account

Before jumping into move or transfer from EPF to NPS, you must open NPS Tier 1 Account through his/her employer, by visiting POPs (NPS Point of Presence) or through eNPS portal. Understand the basics of NPS and the accounts and difference of Tier 1 and Tier 2 accounts at first (Difference between Tier 1 and Tier 2 Account in NPS).

Step 2-Submit Request to your employer

The member of Recognized EPF or Superannuation Fund trust has to submit the request through his employer. As of now no special format of request form was suggested. Hence, a handwritten request letter is enough (with all details of your existing EPF and NPS account details).

Step 3- EPFO or Trust will initiate the Fund Transfer

Based on your request for transfer of EPF or Superannuation, EPFO or Trust will initiate the fund transfer process. They usually issue the cheque or DD for this transfer.

Step-4 Request the EPF/Superannuation Fund to issue letter to Employer

The employee should request to Recognized Provident Fund/Superannuation Fund to issue the letter to his present employer/POP by mentioning the amount is being transferred from the Recognized Provident Fund/Superannuation Fund to be credited in the NPS account of the employer’s Tier 1 Account.

Step 5-NPS POPs (Point of Presence) will receive the Cheque or DD

NPS POPs will collect the amount and uploaded the same for the respective NPS account holder’s account.

Taxation while you move or transfer from EPF to NPS

When you move or transfer from EPF to NPS, then such move or transfer from Recognised EPF or Superannuation fund to NPS will not be treated as Income of the current financial year and is hence not taxable.

Also, an employee can’t claim income tax benefit under Sec.80CCD for the move or transfer from EPF to NPS.

Whether you should move or transfer from EPF to NPS?

There are many pros and cons if you decided to move or transfer from EPF to NPS. However, I am pointing it strongly that slowly NPS is the future. Therefore, if you still hesitant to move to NPS, one day you are forced to move.

What lagging in the case of NPS over EPF are tax benefits, liquidity, guaranteed returns (declared yearly by EPFO). Whereas, in the case of NPS, returns are based on fund performance. The only positive part I may see is that even your EPS part will also earn something, which is not with EPF.

# Are you comfortable with Equity?

If you uncomfortable with equity exposure of NPS or your retirement goal is more than 5 years, then you can assume bit equity exposure in case of NPS will be a good option. Otherwise, you consider EPF as pure debt product and do the equity through equity mutual funds also. In this case the control will be in your hand.

Therefore, check for your comfort.

# Liquidity

In case of EPF, if you are unemployed for more than 2 months, then you are eligible for full withdrawal of EPF and EPS (in case you completed more than 10 years). However, in case of NPS, you have to wait till 60 years of age.

# NPS will not provide you pension!

In case of EPF, you are free to utilize the money at retirement and which is also tax-free. Only pension part is from EPS. However, in case of NPS, you have to mandatorily buy an annuity product from insurance providers. You are allowed to withdraw only 60% of the corpus. Rest of the 40% you have to buy an annuity. Hence, no freedom to manage your own money. Also, as per current tax rules, this annuity is taxable income for you.

# Taxation

Taxation of NPS is horrible which makes you to stay away from such product. However, there is a hope and pressure from many quarters that let NPS corpus be given some tax incentives. As of now, the taxation is as below.

NPS Taxation on retirement

Let us say you accumulated Rs.100 at retirement. In that, you are eligible to withdraw Rs.60 or 60% of such accumulated corpus. Remaining Rs.40 or 40% need to be purchased an annuity product.

In the lump sum withdrawal of Rs.60 or 60%, Rs.40 or 40% is tax-free. Remaining Rs.20 or 20% is taxable income in the year of withdrawal.

The income from an annuity will be taxed year on year as per your tax slab. So you are deferring the tax treatment for future years from the 40% annuity you will buy.

NPS Taxation on Pre-mature withdrawal

In this case, you are allowed to buy an annuity product from the 80% of accumulated corpus. So there is no confusion here as the annuity will be taxable income for you year on year.

The confusion is about 20% lump sum withdrawal. IT Department need to come out with clarity. The rules just say 40% of lump sum withdrawal from NPS is tax-free. However, in this particular case the lump sum investment is 20%.

Hence, whether the whole 20% is tax-free (as it is less than 40% tax-free limit) or 40% of 20% is only tax-free (i.e. 8% from 20%). As of now, there is no clarity on this aspect.

NPS Taxation on Partial withdrawal

Partial withdrawal from NPS is allowed on certain conditions. I explained the same in my post “National Pension System (NPS)-New Partial Withdrawal and Exit Rules“.

There is no clarity about the tax treatment relating to this partial withdrawal. However, I feel such partial withdrawal will be taxed in the year of withdrawal as per subscriber’s income tax slab.

NPS Taxation in the event of death of subscriber

For Government Employees-Nominee will be allowed to withdraw only 20% lump sum. The nominee must purchase the annuity from remaining 80%. However, in case the accumulated corpus is less than or equal to Rs.2,00,000 then his spouse (or nominee) can withdraw all the amount at once without any mandatory.

For others-Nominee will be allowed to withdraw 100% accumulated corpus. However, the nominee has a choice to buy an annuity too.

The lump sum withdrawal by the nominee will be exempt from Income Tax. If the nominee opted for buying an annuity, then annuity income will be taxed as per nominee’s income tax slab in the year of receipt.

# Additional Tax Benefit in NPS

Many of us invest in NPS to get additional tax benefit under Sec.80CCD (2). However, no one think about liquidity and also the taxation part once you retire. I explained the the tax benefits of NPS as below.

NPS Tax Benefits under Sec.80CCD (1)

- The maximum benefit available is Rs.1.5 lakh (including Sec.80C limit).

- An individual’s maximum 10% of annual income or an employee’s (10% of Basic+DA) contribution will be eligible for deduction.

- As I said above, this section will form the part of Sec.80C limit.

NPS Tax Benefits under Sec.80CCD (2)

- There is a misconception among many that there is no upper limit for this section. However, the limit is least of 3 conditions. 1) Amount contributed by an employer, 2) 10% of Basic+DA and 3) Gross Total Income.

- This is additional deduction which will not form the part of Sec.80C limit.

- The deduction under this section will not be eligible for self-employed.

NPS Tax Benefits under Sec.80CCD (1B)

- This is the additional tax benefit of up to Rs.50,000 eligible for income tax deduction and was introduced in the Budger 2015

- Introduced in Budget 2015. One can avail the benefit of this Sect.80CCD (1B) from FY 2015-16.

- Both self-employed and employees are eligible for availing this deduction.

- This is over and above Sec.80CCD (1).

Maximum tax benefit under NPS is discussed as below.

For Self-Employed

The maximum benefit you can avail under Sec.80CCD (1) is Rs.1,50,000 (including Sec.80C limit). Along with this Rs.50,000 under Sec.80CCD (1B). So total maximum benefit an individual can avail is Rs.2 lakh (where Rs.1.5 lakh will be part of Sec.80C limit).

Even though on paper it looks like maximum benefit available will be Rs.2 lakh. But under Sec.80C, you will have lot of choices and few default options to save (like life insurance premium or PPF). Hence, never be in wrong belief that NPS will ALONE gives you Rs.2 lakh tax benefit.

For salaried

You can avail the tax benefit under Sec.80CCD (1)+Sec.80CCD (1B) up to Rs.2 lakh. Along with that you have another additional option to claim deduction under Sec.80CCD (2), which is unlimited and based on certain conditions. I explained the same in my above post.

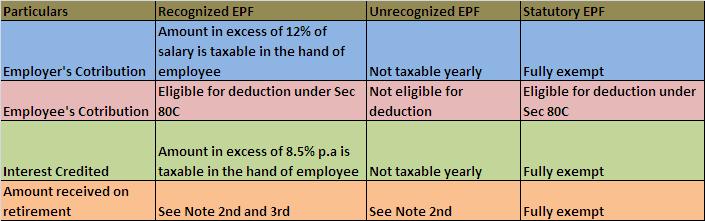

Tax benefits of EPF is explained as below.

Notes:–

1) Salary for this purpose means basic salary and dearness allowance and commission as a percentage of turnover.

2) Amount received is fully exempt in case of an employee who is in continues service for a period of 5 years or more. Full exemption is also available for employees who not completed 5 years because of his ill health, discontinuance of employer’s business or any other reason which is not in control of an employee. If the account is transferred to the new employer then the previous service from whom the account is transferred is also considered as a service period. If none of the above conditions satisfy then the amount will be taxed as unrecognized EPF. Also, concessions availed under Sec 80C will be withdrawn.

3) Employee’s own contribution is not taxable but the interest thereon is taxable under “Income from Other Sources”. Both employer’s contribution and interest thereon are taxed as “Income from Salary”.

Few doubts still exist-

# In it’s recent guidelines of move or transfer from EPF to NPS, there are still confusions on which PFRDA must come out with clarity like what about the % of the breakup of employer and employee and also the future of EDLI.

# Whether the employee can move only his EPS part of whole EPF+EPS can be moved?

I will update this post whenever I get any news related to this. As of now, if you wish to move or transfer from EPF to NPS then you can go ahead by following the above procedure.

If you still need clarity on this, then you can be in touch with Mr.Akhilesh by sending the email to [email protected] or call 011-26543158.

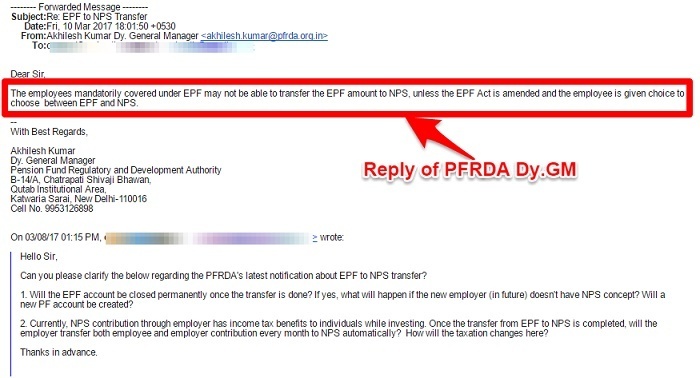

Latest update-One of our blog reader contacted PFRDA Dy.Gm and he got the reply that as of now moving from EPF to NPS is not possible as long as EPF Act amended and employee has given an option to choose between EPF and NPS. Refer below image for the same.

Refer our blog posts related to NPS-

- Difference between Tier 1 and Tier 2 Account in NPS

- NPS Tax Benefits – Sec. 80CCD(1), 80CCD(2) and 80CCD(1B)

- NPS Returns for 2016 – Who is best NPS Fund Manager?

- NPS Tier 2 – Alternative to Savings Account, FDs or Debt Mutual Funds?

- NPS Mobile App – View Statement and Change your Profile details

- eNPS – How open and invest in NPS account online?

- National Pension System (NPS)-New Partial Withdrawal and Exit Rules

Am working in private Sector & Planning to Switch EPF & EPS amount to NPS, but not clarified following points in anywhere, Can You doing for us?

1. Incase fully Transferred, than what will happen my UAN Account as well as Number?

2. Shall I get coverage 6, 00,000 Lacks, which was providing EDLI?

3. Is it Employer will contribute same 12 % to NPS or 10%? Or Is Mandatory to Employer to Contribute Equal to Employee Contribution?

4. Is it Partial Transfer allowable from EPF to NPS?

5. Is it Possible to transfer only EPS amount to NPS account?

Dear Mahendran,

As of now, it is not possible.

Gentleman, Its not Clear. Can You Explain one by one?

Dear Mahendran,

Better you read. Because I am a bit lazy to explain or spoon-feeding.

What is the current status, please? Has anyone transferred from EPF to NPS including FPS corpus successfully?

Dear Mitter,

It is not yet implemented. Please wait.

Sir,

I have an Resign a Company After 19 Years and Then Join a govt Job. Previous time I was a EPS Mebmber during in Company working but Now I am member of NPS in Recently.

My Question is How to link EPS a/c to NPS a/c ?

Mehra-As of now YOU CAN’T.

Can we move PPF to NPS ?

Raghu-NO.

Dear Sir,

I am an NRI now and there is no contribution to EPF. I am not returning to India for now.

In that case what will be a better suggestion to close the EPF account or create a new NPS or leave the EPF account till retirement.

Looking forward for your answer thanks.

Regards,

Manirathnam

Manirathnam-In your case better to withdraw.

Thanks for your reply.

Can you please explain why it will be better to withdraw?

Manirathnam-First thing, hard to rely on EPFO that they keep your money safely especially when they are implementing and experimenting many many things. Second thing, I believe you will not come back to India and work.

Okay. Thanks for your answers

Hi Sir,

I have applied for transfer of PF via online. When i checked for the transfer status it shows my present employer accepted the transfer whereas my previous employer status is still in pending acceptance.

My previous organisation is closed and i wont get any sort of help from them. In this case what should i do ?

Is it enough if my present employer accepts my pf transfer ? will i be able to withdraw both the company PF if i quit from my current organisation ?

Please clarify me. Thanks

Divya-If the status continue the same way, then contact EPFO.

Hi Basavaraj,

I have a query regarding the pension part EPS, when the epf(employee & employer contribution) from previous accounts is is transferred to new account.

While the PF account number of the new employer shows the transferred EPF balance(employee & employer share), what about the EPS money from the previous employers? This is my 4th company and in the passbook the EPS has been updated as 0 when I did the transfer.

I have 10 yrs of service, how can I keep track of the EPS amount that was accumulated ?Can I get in touch with the EPFO and claim that amount or buy certificates ?

Please help !

Shreya-When you change the company or transfer EPF, then EPS will never get transferred. The service records just get updated. Hence, the data you are pointing is correct.

Hello sir

My self Arvind Kumar. I want to move my EPF account to NPS. At present my age is 56 years. Can it possible. And my EPF balance is 1600000.

Arvind-Stick to EPF than to NPS.

I don’t understand

Let’s say you are driving your car to your home town which is 300 km. away. You reached 280 km already safe. For the rest of the 20 km, would you like to drive faster and increase the probability of an accident or drive slower and reach home safer? May be the author meant the same when he suggested to continue EPF than switching to NPS. If you are not sure of your decision, may be it is worth listening to the author who has formal knowledge in finance (besides, he answered straight forward without charging you).

If you have already decided to switch to NPS then you may need to wait until EPFO clarifies rules in detail.

In epf After retirement I got only 60% amount and approx 2500 per month pension and after my death my 40% amount laps.

But in NPS my 40% amount shall be given to my nominee.

Is that true or not ?

Arvind-What is the problem in giving remaining 40% either to you or to your nominee?

Arvind-What is your confusion?

I want to call u .

Pls share ur mobile number

Arvind-For what?

A lot of confusion hare

Arvind-Wait for clarity.

I want to know about EPs transfer to NPS.

Is it possible ?

Arvind-The procedure is already explained.

EPS not EPF

Arvind-Transfer also includes EPS.

I read the 2 page notification but I felt it doesn’t answer few critical questions.

1. Will the EPF/UAN account be closed permanently once the transfer is done? If yes, what will happen if the new employer (in future) doesn’t have NPS concept? Will a new PF account be created then?

2. Currently, NPS contribution through employer has income tax benefits to individuals while investing. Once the transfer from EPF to NPS is completed, will the employer transfer both employee and employer contribution every month to NPS automatically? How will the taxation changes here?

I raised an RTI with the above questions to EPF organisation today morning.

Sreekanth-This is what I pointed. May questions no ANSWERS as of now!

1) Future is NPS. Slowly and surely EPF will vanish. So no question of what if employer not providing NPS.

2) It has to be automatic like EPF. Let us wait for clarity. We have to see how they handle the NPS taxation post this activity.

Hi basu,

What you mentioned is true……NPS is the future. Though at present EPF members& corpus far outnumber the NPS, each passing months, the number of EPF is gradually dwindling &NPS rising. Each budget, govt gives some or the other incentive to promote NPS. In my opinion,its only a matter of time,before govt gives tax parity between NPS&EPF.

Suppose a subscriber shifts from EPF to NPS,under which category will he?she come under? private/corporate category?

Sreekumar-There is no clarity about which category the EPF member be counted. However, category I don’t think matters much than returns to investors right?

I’m guessing this one time switch from EPF to NPS is only applicable to those whose employer’s have NPS in their salary structure else I can’t think of a way how the employer can contribute the EPF amount as NPS every month.

Sreekanth-There is no clarity and also no official intimation from EPFO. So we have to wait.

As per the reply I got, “The employees mandatorily covered under EPF may not be able to transfer the EPF amount to NPS, unless the EPF Act is amended and the employee is given choice to choose between EPF and NPS.”

Sreekanth-May I know who replied to you? I know it is one way decision which PFRDA took without considering the same action by EPFO.

Akhilesh Kumar Dy. General Manager, PFRDA . I emailed to the contact that is listed on notification requesting for information. He was kind enough to respond promptly. I also raised RTI to the EPF (not PFRDA) on the same day to know what their view also but no response till this time.

Sreekanth-Share the same to my email [email protected]. I will update the reply image in this post.

Meanwhile… My RTI raised to EPFO was redirected to Director General of Income Tax (Systems),New Delhi; I’ll forward the reply as and when I get it.

Sreekanth-Sure 🙂