Today LIC launched new plan called “Jeevan Sugam”. It is a non-linked single premium limited period plan. This plan will be available for 45 days from now. Let us look at features and who can invest in this plan.

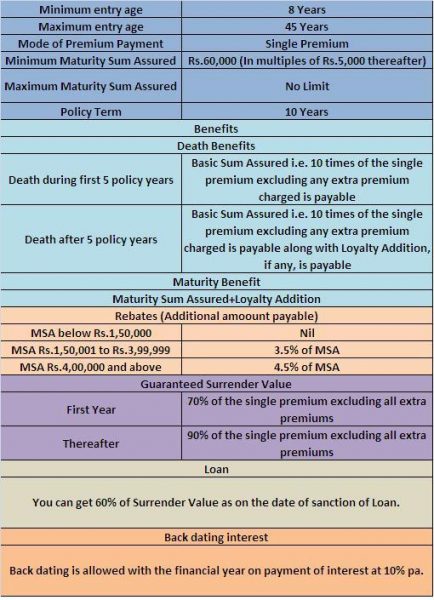

Features:-

Let us take one example. Mr.X who is 25 yrs old want to invest in this policy. He want to opt for Rs.5,00,000 MSA (Maturity Sum Assured-which is guaranteed amount you receive from this policy). So the amount he need to invest is Rs. 2,86,539 (including service tax). Sum Assured available throughout the period is Rs.27,79,500 (10 times of single premium). Now during the first 5 years of policy if his death occurs then his nominee will receive Rs.27,79.500. But if his death occurs after 5th yr and within 10th year then his nominee will receive this Rs.27,79,500+LA (which is unknown as of now and will be provided as per the rates available at that time). If Mr.X survives till maturity then he will receive the MSA which is Rs.5,00,000+Rs.22,500 (Additional MSA at 4.5% of MSA)+LA.

Is it worth to invest?

Even though premiums may looks as if same but difference of premium for the minimum age (8 Yrs) to maximum age (45 Yrs) for above calculation is Rs. 1,02,884. So if you want to invest in this plan then better to invest in your spouse or kid name to benefit the age factor. Considering the other options available like bank FDs, this plan looks attractive in terms of tax angle too. You can avail the tax benefit under Sec 80C during the period of investment (For insurance policies issued on or after April 01 2012, deduction is allowed for only so much of the premium payable as does not exceed 10% of the actual capital sum assured). Also you can avail the tax benefit under Sec 10(10D) post maturity also under current income tax laws (For insurance policies issued on or after April 01 2012, exemption would be available for policies where the premium payable for any of the years during the term of the policy does not exceed 10% of the actual capital sum assured).

Liquidity is the major drawback of this plan compare to Bank FDs. Because in Bank FDs if you want early withdrawal you will get your invested amount full+interest till that period (which is lesser than the normal rate). But in this plan straightaway you will receive less than what you invested. Hence if you are sure about your waiting period of 10 years then best option.

Let us consider same case to compare the returns. I am considering LA as 10% of MSA which is fair in my view.

Point to be noted:-

1) If in above calculation of this plan we considered Rs.1,00,000 one time investment and person investing is under 10%, 20% or 30% tax bracket then the yield may be higher. Because in above example investable amount is Rs.2,86,539, but we can avail tax exemption upto Rs.1,00,000 under Sec 80C.

2) I have not included cess (which is 3% on tax amount) for calculation purpose as it may not make that much difference while calculating yield.

3) For calculation purpose under Term Insurance+Bank FDs, I considered LIC’s term plan which is high priced than the private insurers. So if you take term insurance from other insurers which is cheaper, then your overall yield will be higher than what I calculated.

4) For calculating FD rate, I considered current SBI’s Term Deposit rate.

From above calculation it clearly shows that competition is neck to neck. So if you chose this plan for your investment then their will not be any harm.

Hence this plan is good for investors who are risk averse and looking for some kind of life risk too. But parking all your portfolio in such low yielding product may not be worth for your long term financial goals.

I am 22 years and already have 4LIC Policies and I want to invest 10K more anualy so please suggest me where should I invest in LIC/FD/MUTUAL FUND/ULIP also specify particular which corp. will be best for that type of iinvestment. Thank u Sir, your review s are very uaeful.

Rahul-First cover your life risk by term plans. Then based on your financial goals start investing.

Sir

I posted a comment as a reply to your another response.

So, posting the comment below again for clarity sake. Also rewording my question slightly differently.

I am 41 years old. Looking for an insurer who can give a life cover by a term. Which insurer is most trustable one?

I tried with LIC. They asked me to go on tests again and again and I finally gave up. the same is the case with my friends too…. So, can you suggest the right Insurer who would give me a term policy?

And another question on Jeevan Sugam.

Can I look at this policy as a means to get a higher life cover even though my returns are too low (considering the age factor i.e. 41 years)? Say, if I invest 100000 now as a premium, how much I would get as Life Coverage?

Regards, Velmurugan

Velmurgan-I am happy with your decision that you opted for term insurance. To be frank, LIC’s term insurance is costliest in the market. Instead better you choose online term plans available with private insurers. In my view better either go with ICICI or HDFC but you may choose with your comfort too. Also better to take online with disclosing all materiel facts and sharing about this cover with your family members. Because usually in online term plans their will not be middlemen, so your dependents may feel heat if they don’t know exactly to whom and how to approach.

Don’t go for any policy other than term plans.

Dear Sir,

Thank you for your response.

One question on the role of private players in the field of insurance…

How safe it is to insure our life with private players? they are not like LIC that has the backing of Government. I know IRDA is there but how strong it is when it comes to private players?

Can we really trust them for a long term association with them? Would they not close their Insurance division once they find that they are running in lose or too many claims happening? Or would they increase the premium over the time period?

I heard from one LIC agent that these players increase the premium from time to time. I don’t know if that is true or not. but he mentioned.

Could you please guide me? Is there any law that allows them to do so?

Regards,

Velmurugan.

Velmurugan-You can trust equally LIC. Reason is, as you told IRDA will always monitor and all insurers need to maintain solvency ratio as a safer way of claim in case of closure of company. Their may be service related issues which may differ from insurer to insurer including LIC too. So based on your comfort you can choose the company. But never forget that hiding materiel fact may lead to reject the claim. Regarding the increase in premium from private insurer, I too hearing it first time. Ask your agent to provide the proof of that. Because usually in life insurance premium will be constant throughout the period.

Now it is left with you to decide which insurer is safer. For your information, expecting a good service from LIC too is risky. I am saying this line being an agent of LIC and monitoring how they do service. Think and decide 🙂

Thank You so much Sir.

Your guidance is very valuable.

Regards, Velmurugan

Velmurugan-Pleasure 🙂

ok sir

my dear BasuNivesh sir

thanks for your comments my brother age is 22 & 28 any medical certificate/examination required for buying 5 lac policy jeevan sugam pl advise tks bi bi

pl send msg as it is tks

Elumalai-Can you let me know what is the exact need of your above line?

Elumalai-In my view not required. But why you are so afraid of medical examination? If their are some health issues then it is better to disclose yourself to avoid future trouble in claim settlement. If no such health issue then let them do what test they need 🙂

i am 30 years old i want to get a premium of 20k .Let me know how much i should pay and plan details

Anitha-For your age you are saying able to pay 20k, which is not possible in this plan.

Hi,

What is the difference between this plan and Bima Bachat or other Single premium Policy’s from LIC

Rajib-Lot of difference, like Bima Bachat is like money back plan. But in this plan returns are after maturity only. Sum Assured is good option than Bima Bachat. So you may consider this as improved version of Bima Bachat.

BasuNivas : Thanks a lot.

Actually,i am looking for plan that will give me equal or better benefit over FD as i think in FD Matured amount is Taxable that i want to save.

Can you please suggest best available options for the same,so that i can think forward.

Thanks,

Rajib

Rajib-In that case you can try with this plan else currently some tax free bonds are also available, you can do that also.

@BasuNivash : With respect to interest rate, which option is better ?

Rajib-If you look for interest then all are almost equal when tax comes into picture. So choice is your’s.

Hi Basu,

Thanks a lot.

One more thing i am having a LIC ULIP policy where i invested Rs 90K for 3 years ,But now its value id Rs 86400k.

As per plan,if this amount will be matured after 8 years.

What do you suggest, should i wait for more 5 years or i should invest that money with other plan or so.

Awaiting for your reply.

Thanks,

Rajib

Rajib-That’s the cost you are paying now for your agents bad advice. Anyhow better to come out and invest according your financial goal but not according to your agent’s financial goal 🙂

@Basu : Correct !!!!

Thanks a lot

Rajib-Pleasure 🙂

Hi Basu

i have few queries,iam having son aged 4 yrs,i want to invest for his further studies can you suggest which is the better plan for investment.

Ekta-Your plan is long term. Hence better to go for equity exposure with mutual fund route of SIP. Also not forget to cover your life risk by taking term insurance.

My children are 19 and 13. Can you please suggest the minimum amount to invest in this plan?

Sudharsana-For 13 yrs kid minimum amount to invest is Rs.33,661(life risk will be Rs.3,26,520) and for 19 yrs kid minimum amount to invest is Rs.34,147 (life risk will be Rs.3,31,230). For both cases MSA will be Rs.60,000.

dear basu,

i hav few queries related to this paln.My age is 25 n i am lokking forward to invest in this plan.I will be investing 30k, pls guide me for minimum locking period, charges on premature withdrawal, sum assured amount, tax benefit on premium paid n sum assured received, limitaion(amount to be invested) n lastly is it a one time investment plan or can be invested periodically.

Pls help me all the details…dont forget to mentioned ur calculation.

Waiting for ur reply….

Hitesh-For your age minimum amount of investment is Rs.34,385. Rest of your doubts will be get cleared once you go through the above full article.

I cant u/stand d plan nicely.1st ly is it granteented plan? how much will I get after 10 years at maturity not my nominee after death. I am 36 years old. Plz rep soon.

Anulekha-In this plan only MSA is guaranteed. Apart from MSA (maturity Sum Assured), you also receive Loyalty Addition which is the only part that is not guaranteed. Suppose you opt for Rs.10,00,000 MSA, based on your age they fixed the premium which is Rs.6.08,592. So MSA of Rs.10,00,000+Rs.Rs.1,95,000 (4.5% of additional MSA for opting higher MSA)=Rs.11,95,000 is guaranteed. But LA on this is not guaranteed. Hope I cleared your doubt.

Hi Basu,

I am 36 years old, I have 1.5Lakh in hand, want to deposit for child future plan, is jeevan sugam is ok to invest or can I try others

Please advice

Thanks n Regards

Sudhakar

Sudhakar-Can you tell me your kid’s age and your current insurance coverage?

Hi Basu,

Nice to see your reply,

Presently with jeevan saral for 20 years 5 laks Sum Assured for this I am paying 28K yearly

kids(baby boy) age is 7 months, he got few money from grandparents so i want to safe that money for his future

Thanks and Regard

Sudhakar

Sudhakar-Why can’t first you fulfill your insurance need by purchasing term insurance plans? Do this on high priority. About your kid’s planning, which I think 18 years long from now, is better to opt for a better option than any LIC policy. Park around 70% in 3-4 well diversified mutual fund, 30% in PPF. This will actually balance your portfolio. I am suggesting equity mutual fund, reason is over the years of 18 years, you will definitely get a handsome return which actually beat inflation. If you choose any LIC plans then returns will be around 8% and the inflation is 7%. So actual return on investment is just 1% not 8%. So think and decide wisely considering the inflation too.

Hi Basu,

can you guide little deeper, I have no idea about mutual fund,PPF, please guide me in correct path

Thanks and Regard

Sudhakar

Sudhakar-You google it about PPF, you will get the all information about that. About mutual fund, do mail me your financial goals to my official mail id. I will definitely guide you.

Hi Basu,

Today i took jeevan sugam for Rs.50180 it showing sum assured as Rs 5,01,797, what exactly the sum assured means in this policy

Please reply

Thanks

Sudhakar

Sudhakar-Sum Assured is the risk of your life what LIC will cover during these 10 yrs. Suppose policy holder dies during this 10 yrs period then his/her nominee will receive this amount (Please see death benefits I shown in above table). Remember that if policy holder survives then he will not receive sum assured instead he receives maturity sum assured.

im 43 years old, i want to buy this plan .will u plz tell me minimum premium for me?

Zakir-Minimum amount you can invest is Rs.42,067.

I am novice in this field, let me know age wise minimum investment amount and tax rate(total taxin detail) on that amount . if there is any formula related to this i will be very thankful to you

Jay Shanker-I am unable to share the premium for all age group. Instead if you share me your age then I may tell the specific premium. For whole data of age group wise premium, you may visit LIC website. Formula for premium calculation? It is usually a confidential data which insurers maintain. It depends on lot of factors. For layman like me and you it is difficult to understand also. Please let me know what are your actual need.

Dear Basu,

Thank you very much for your detailed explanation.I have another question w.r.to SBI Smart ULIP. I took this policy in 2010 and paid all the premiums (total 1.5 lakhs). Now in the fund value its just showing 1.4 lakhs. In this situation shall i continue this policy or surrender the same. Please advise.

Thanks

Rama-These are the long term product but agent sold it as short term. Expenses are high. Better to come out after minimum lock in period. Immediately take term insurance and rest of amount invest in other asset classes bases on your financial goals.

Hi Basu,

As per your advise i am planning to take Bajaj Allianz I secure term plan which will cover for both wife and husband. The premium for 75 lack is around 10500.

Is it a good plan to take.. Please advise…Also advise me on the claim settlement ratio of bajaj..

Thanks

Rama-Go ahead if your are comfortable with company and premium. Claim settlement ratio is one tool to judge the performance of insurance company but it does not mean that higher claim settlement company will always be customer friendly. Hence declare whatever they ask for openly without hiding any facts. Then even god too can’t stop in getting claim. I didn’t get why you want to purchase term plan for your wife? Is she earning? Are you or anybody of your family members depend on her income? If so then go ahead else it is not necessary.

Hi,

Thanks for the details of the policy . My age is 29 years and can you please let me know the minimum amount that needs to be invested in this plan .

Khushbu-For your age minimum amount you can invest is Rs.34,567.

Thank you detailed explanantion and understandable in terms for financial “illiterate” ppl like me. 🙂

Kumaran-Pleasure and hope you pass this info to your near and dear.

I want to take term plan for me and my wife, currently i am working in other country. I have the below queries:

a. Can i take online term plan to my wife (aged 26) who is a house wife and is it required medical tests, if yes what is the process

b. Can i take online term plan to me (aged 35) as i am working abroad

c. Please suggest us the best term plan with less premium

thanks

rama

Rama-

A) As you mentioned that your wife is housewife then it is difficult to get term plan for her. Reason is, insurance is need when proposer have some “Human Life Value”. So in case of your wife’s death their will not be any financial loss to near and dear as she is not earning anything.

B) You can take online term plan online. Even few plans are available for NRIs too.

C) Plenty of term plans are available online. Few of them are from ICICI and HDFC, Aviva, Kotak. But choose according to the feasibility of premium and the maximum age they offering.

under section 10(D), for the maturity amount, if I get 60000 as my Maturity, then 10% of 60000 is 6000 and my premium is 32000, which is more than 10%, then this means I have to pay tax on the maturity, is it? Please explain in detail how much tax will I have to pay on maturity ?

SDas-This policy meet the requirement of premium to sum assured ratio (1:10), hence whole maturity or death claim will be tax exempt.

My age is 35 year What is the minimum investment if I invest Rs.60000/- what is the maturity value.

Deepak-If you invest Rs.60,184 then MSA will be Rs.1,00,000 and life risk throughout the period is Rs.5,83,800. Your returns will be Rs.1,00,000 (MSA)+Rs.10,000 (Assumed LA at 10% of MSA)=Rs.1,10,000.

Hi,

All the comments were about investment. My concern is about Insurance cover. For 30L SA, whats the Medical Test criteria ? Is it same as Term Plan ? How about claim ? Lots of formalities or simple and documents free claim ?

Take care

C. Saravanan

Saravanan-You are askingb procedural requirements, which your agent or insurer will explain you in a better way than me. Regarding claim, it if is within 3 years then insurers do in depth research, if it is more than 3 years then the normal procedure.

A.Rafique:Thanks for Your extraordinary presentation.Sir You have considered 80C but you have not calculated sec 10/10d for LIC MATURITY & taxable return for BANK FD.Pls may consider this…Thanks

Abdur-Thanks. I considered Sec 80C during the time of investment too (Only Rs.1,00,000) and anyhow maturity proceeds are tax free for this plan. For FDs I considered and calculated directly instead of mentioning it. Please do calculation your end and let me know if I did anything wrong.

Hi Basu,

I am a 32 year old person and my wife’s age is 26 .I have recently invested 50,000 in HDFC crest and interested to take a LIC plan side by side and mainly interested in single premium plans my goals are to purchase a house in 3-4 years and to plan my retirement ,so should I go with this plan.

Please suggest

Vinit

Vinit-Your waiting period is 3-4 years away from today, so this plan is not meant for you. This is 10 year plan and if you want to liquidate in middle then you will receive the less than what you invested. Hence better to opt some other options like Bank FDs or Debt Funds. Hope your retirement will be around the age of 55-60 yrs. This is the long term goal. You can take the calculated risk by investing in a well diversified equity oriented mutual funds, balanced funds, PPF and some percentage into Gold (not physical gold). Hence for both of your goals this plan is not suitable.

Hi Basu,

First of all thanks for the reply and valuable suggestion.Since long I was looking for a source which can solve my finance related queries and specialy in a unbiased way such as yours and my search ended up here ..As I have just started to take my finances seriously if you could please suggest me some good debt funds,diversified equity oriented mutual funds, balanced funds and a retirement plan as I have already invested in Bank FD’s and NSEL ETF.

Vinit-Please send me the mail to my official mail id. Will share you the funds you need to invest.

Hi Basuvinesh,

Can you please clarify if a NRI eligible to opt for this.

Thanks…

Naga-In my view no.

HI,

Thank you for your reply. can i have your cell number and suitable time when i can call you and discuss further? Please email me your contact details. I need more details on investnet.

thank you.

Dnyanesh-My contact details are available on the page “Contact Us” (tab on top right side of blog). Before calling just message me whether I am free or not. We can definitely discuss.

Sir, My friend want to invest 1,00,000/- in this policy for the sake of both Insurance and maturity value. Are you recommending this policy or any other LIC policy which will be more suitable to him. His age is 40 years.

Arabinda-Please let me know his financial goal for this Rs.1,00,000 investment.

My wife is 42 years and currently has no insurance cover.

Which term insurance plan of LIC would you suggest for my wife? She would like to go for full life cover (not 10 years like this plan).

Would prefer a single premium policy as we have the capacity to pay a higher amount now. Could pay up to Rs.1 lakh this financial year.

Thanks in advance.

Karan-First of all please let me know whether your wife is earning or not, someone depend financially on her or not? If your answer is yes then she definitely need insurance. In LIC their are only two Term Plans 1) Anmol jeevan (Max Sum Assured is Rs.24 lakhs) and 2) Amulya Jeevan (Min Sum Assured is Rs.24 lakhs). But compare to online term plans these plans are costlier. Hence if you are comfortable with private insurers then you can go ahead with online term plans. In my view it will not cost you more than Rs.20,000 yearly which I hope affordable for you. So better to opt for yearly premium instead of one time payment. Let me know your views too.

Thanks for your response.

She is working and earns Rs.4 lakhs a year but her is not a steady job. Yes, Rs.20000 premium in a year is affordable. So will go for yearly premium. Thanks to your blog, I have learnt that if we put a good amount in FD, then its interest could take care of annual premium of Rs20000, right?

Karan-If she is earning and you are depending financially on her then Term Insurance is a must for her too. Good to hear that you are going for yearly premium. But in my view putting Rs.2,00,000 for paying insurance premium is not a wise way. Because term insurance are not costlier and anyhow insurance companies will issue insurance cover to the tune of maximum 15 times of her annul income (but differ from insurer to insurer). So it will not cost you more and you can easily utilize that money for other financial goals.

@BasuNIvesh : My wife is 26 years old and I am already claiming 90000 under Sec 80C and if I take up this policy for Rs. 60000 (fro my wife) , then can I claim for whole 60000 amount or I can claim only for 10000 under sec 80 C.

One more thing I wanted to know the minimum amount to be invested in this policy for my wife whose age details has been shown above.Even I want to know the assured returns for the same….

One silly question …Which is good ??? This policy or New Bima Gold(3 Lacs) or any other for my wife….

Please suggest…..

Sunny-You can claim only Rs.10,000. Minimum amount she can invest is Rs.34,431. Return will be Rs.60,000 (MSA)+Rs.6,000 (LA assumed at 10% of MSA)=Rs.66,000. In my view neither this plan nor New Bima Gold. Best is to separate your investment with insurance. Take term insurance online to the tune of 10-12 times of your yearly income. Rest amount invest on goal based.

HI,

I am expecting maturity benifit from this plan around l0kh that means my one time premium would be some where 5 lakh plus. is it worthful to invest so much in single premium?

I am looking for good risk cover and at the end maturity returns too.

I am planning to buy the same for my wife too.

please suggest whether this is right decision or wrong?

Dnyanesh-In my view this is not the worth plan as returns are around 8% and life risk is 10 times of your premium. Instead it is best option to take term insurance to cover your life risk. Rest in other asset classes. It is plan who are totally risk averse and too much faith in LIC 🙂 But you can generate the more returns by investing in PPF (which is 15 yrs). Else you can easily create a good corpus by investing in equity mutual funds, debt funds and some percentage in gold. Which makes your investment a well diversified. Let me know your views.

BasuNivesh sir,

I have an amount of Rs. 1 Lac in hand and I want to invest this amount for a long period. But, I want to have gurranted returen and investment must be made in a well recognised or govt. entity. Mobile No. 9654508919

Thanks sir in anticipation for having a nice investment plan.

Pankaj-If your waiting period is more than 10 yrs instead of this plan better to chose PPF which gives you more return than this. Keep some amount for term insurance too, which covers your life risk.

Thanks for such a detailed information. Please let me know whether this plan is feasible for the age of 36 and 31 by investing Rs. one lac each and what would be the sum assured in each case together with the maturity value at the end of the policy term

Brijendra-Feasibility depends on your financial goal. If you are ready for return of around 8% and little bit of risk (ideal life risk should be 10-12 times of your yearly income), then go ahead. Still you are ready to invest then let me know how much you afford to invest.

My wife is of 32 years. She wants to invest 50,000 in this plan. Can you guide me how much returns she will be getting after 10 years ?

Vishal-She can invest Rs.58,663. MSA will be Rs.1,00,000 and life risk will be Rs.5,69,050. You return on investment will be Rs.1,00,000 (MSA)+Rs.10,000 (LA assumed at 10% of MSA)=Rs.1,10,000.

Sir can you explain -Even though premiums may looks as if same but difference of premium for the minimum age (8 Yrs) to maximum age (45 Yrs) for above calculation is Rs.11,134. So if you want to invest in this plan then better to invest in your spouse or kid name to benefit the age factor.??

how age factor will benefit?

Arsh-Suppose Mr.X whose age is 8 yrs, opted for MSA of Rs.5,00,000 then he need to pay premium as Rs.2,75,405. Mr.Y whose age is 45 yrs opted for same MSA i.e. Rs.5,00,000 then he need to pay premium of Rs.3,78,289. Maturity amount will be same. But due to age factor Mr.Y need to pay Rs. 1,02,884 more than Mr.X. That is what I pointed. (But I made error while calculating which I corrected now-I did difference between 25 yrs with 8 yrs proposer). Hope you understood what I pointed.

Very nice comparison sir, But there are some other nationalized Banks with interest rate 9.25% for their FD, like SBH, SBM etc. Then there will be huge difference. My age is 43 years. it may not be much suitable for me. isn’t it? Also, I already have some other policies. Already Rs 50,000/- covered by LIC & PLI policies. Remaining Rs 50,000/- I use to invest in PPF every year and my tax is in 10% slab only.

Gajanan-Their may be some higher FD rates available. But for comparison I took SBI’s 10 years term deposit rates. Yes it is not suitable for you. But investing all surplus in secured products may harm your financial goals. Keep that too in mind.

Dear BauNivesh,

For Age: 40 Yrs.

Even if we open a FD @8.5% worth Rs.60000 and pay rest of Rs.4880 for term plan, we get insurance worth Rs. 10,00,000 and FD return of approx. Rs.1,11,000.

So why one should opt for this plan?

Gireesh-That’s what I told, it is best to younger investors. But worst to older investors like 35+. Even for younger too returns are neck to neck. But for your information, returns on FD is taxable. I sum up all those points what you said above in few lines of “Points to remember”.

my age is 40 yrs if i pay 60k as premium how much i will get after 10 years (approx).

Kumari-You need to pay Rs.64,880, life risk will be Rs.6,29,350. MSA will be Rs.1,00,000+Rs.10,000 (LA assumed at 10% of MSA). So total you will receive Rs.1,10,000.

This is awsome Sir ! ! we can give various options to our esteemed customers aligned to this product.

Santosh-Check the above comment which I mentioned to Sachin K

This is such a nice plan.

Sachin-Is it? I dont think so….10 years and return just around 8% and inflation 7%…..so real return 1%. Can anybody sustain?

I am sorry, but I do not buy this theory.One should not mix Insurance with Investement.Buy A term plan and put remaining amount in PPF(upto Rs 100000/-), if your investment horizon is around 15 years.Maturity amount and Interest in PPF is Tax Free.And for 5/10 years period invest in some good balanced fund, even here returns will be tax free.

Manish-Wonderful…hope others also follow the same.

My age is 42 years (DOB 10th April 1970). I wish to have sum insured of Rs 50 Lac under this policy. This will give me a adequate cover for life risk together with some assured return. Kindly confirm the one time premium amount.and the maturity value which I will get at the time of maturity from LIC.

Vivek-As per current available readymade charts, you can avail Sum Assured of Rs.66,01,000, MSA will be Rs.10,45,000 and premium you need to pay is Rs.6,80,497. So you will get Rs.10,45,000+Rs.1,04,500 (LA which I considered as 10% of MSA for calculation purpose, but remember this LA is not predictable as of now)=Rs.11,49,500. But think twice whether this insurance coverage you are taking is enough? Whether this investment will fulfill any of your financial goals?

You have to pay 523983 which covers insurance for 5082770

I wish to invest Rs.200,000 in name of my daughter who is 14 years old how good would this policy be.. also note that as far as Tax benefits are concern hv other policies so would not able to avail any benefits.

Gyanesh-Suitable of this plan depends on your financial goals not about this product. Hence from this product you can expect around 7-8% return and this return really fulfills your financial goal then go ahead. Taxation is part of investment but dont invest amount think only taxation.

please sent me ful detail of this polcy as what is the monthly primium

Rakesh-For your information this is one time investment and all details about this plan is shown above.

Sir,

My son is an NRI and 30 years old. is this policy advisable and taxation of proceeds on maturity?

If not what are the alternate plans.

Regds

Sethupathy

Sethupathy-I dont think this plan is available to NRI. It is only for individual and HUF. But still it is better to contact your nearest LIC branch for this clarification.

dear if you detuct the premium of 10 time insurance cover for 10 years ( term plan Premium) the returen will be more. for examble I calculate myself age 35 for 2 lakh maturity sum assured the premium Rs.120368 and i detuct the term plan of 10 lakh for year 3277X10=32777 the premium will be 87591 and i will receive the guaranteed maturity Rs. 200000 with LA. I thing is it really good one

Vijay-When you are investing in this plan, insurance is the feature you will get. Hence calculating insurance separately and returns will not be suitable. But when you are investing in any other instrument then we need to consider the cost of insurance too for comparison which I did above.

What is the premium amount for this jeevan sugam plan?

Deva-Please look at above comment. Premium depends on your age.

What is the premium for ages 22,27 and 48?

Deva-You are asking about minimum premium?

Sir, thanks for educating people on this plan in much simpler way than others.

My wife (42 years) wants to buy this policy. She can invest up to Rs.100000 in order to take tax benefits. Her annual income is Rs.5 lakhs. Will she gets full tax benefit as under 80C with this amount of investment? And what will be her total risk cover and maturity amount?

thanks in advance

Karan-Thanks for your kind words. Yes she can invest and avail tax benefit. As I told above, this works out best for younger than older. So in my view at your wife’s current age, investing in this plan is not a good option. Is she have term insurance? If not then my first advice to her is to cover her life risk. Then don’t restrict your investment based on plans, instead choose the products based on your financial goals. Hence think twice wheather this plan suites your financial plan or not. Let me know your views too.

Sir

I am 41 male. I have tried the term insurance in LIC and they prolonged the medical tests again and again and I finally gave it up. I want to increase my life cover. What do you suggest for me?

is there any other reliable insurance companies where I can purchase a term insurance?

or can I invest say 100000 to get life cover of approx 25Lakhs?

I am looking for life cover also than just returns only.

This was very informative Thanks a lot Vasu

Uddalak-Pleasure 🙂

Just want to check whether the maturity proceeds are taxable or tax free. Not very clear on this issue.

Raghuveer-They are tax free under Sec 10(10D) of the current rules.

I’m 29 and wanted to invest 10k in this policy.. what will be the maturity amount and risk cover…Is it one time investing primium?

Akshita-Under this plan for your age minimum amount you can invest is Rs.34,669, this gives you Rs.60,000 MSA (minimum MSA) and Life Risk will be Rs.3,36,300. So you can’t invest Rs.10,000 in this plan.

I am 29+ now. From ur blog I think last year Jeevan vriddhi was better than this. Please let me know how much would be Life risk cover for 50k. Thank you.

Santu-For your age for Rs.1,00,000 MSA premium will be Rs.57,782 (nearer to your mark) and the life risk throughout the period will be Rs.5,60,500.

I have seen 80C is applicable there but is 10 10(D) also applicable ??? WIth most of the LIC plans 80c and 10 10(D) comes. What would be the maturity sum assured for single premium of 50K?

Santu-Yes it applies for both. If you share your age then I can tell you the MSA.

what is th minimum amount of investment in this plan

Nishtha-Premium is depends on age too. So if you share your age then I can share the info.

Nice Article in detail. Thanks BasuNivesh.

Senthil-You are welcome.

Just see the brand name of LIC and invest money according to your comfort and leave everything else to LIC. It will take care of you forever 🙂

Shailendra Prasad-Wow what a wonderful comment. Giving such a wonderful free advice is a great. But we need to take care that either it is LIC or any other organisation, product analysis and suitability is the must. Blindly investing in any product is such a dangerous act that LIC may give you the committed amount from it’s end. But what will be your financial life if it not fulfill your need?

realy it is a beautiful plan for investers

Debabrata-It looks good but it does not mean that we can park all our investable amount in such products.

Thanks for the details

it is useful to all

Regards

G.S.Hegde

G.S.Hegde-Pleasure 🙂 Hope you spread this to your friends too.