LIC is launching its new pension plan Jeevan Dhara 2 (No.872) on 22nd January 2024. Should you invest in this GUARANTEED new pension plan of LIC?

LIC Jeevan Dhara 2 is a pension plan that GUARANTEES a fixed income for your retirement. It provides life cover only during the deferment period and offers both single and regular premium options. Additionally, existing LIC policyholders, nominees, or beneficiaries can enjoy enhanced benefits of this plan.

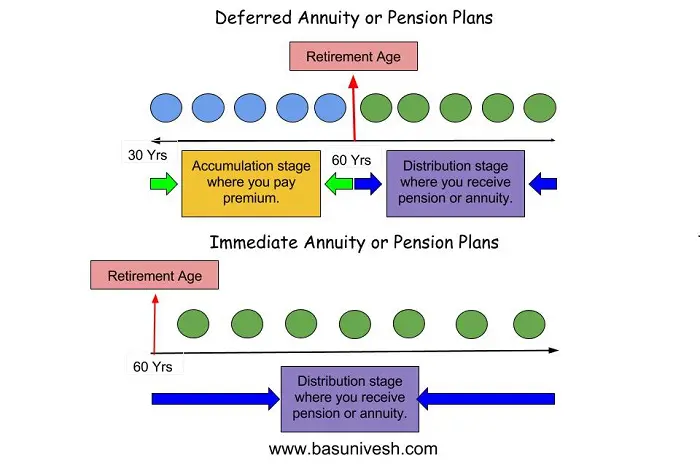

Do remember that this is a deferred annuity plan but not an immediate annuity plan. Before proceeding further, first, let us understand few terminologies used in retirement plans.

In simple terms, you can say it is a Pension, where you will get regular income up to the specified period or conditions. There are two types of annuity.

1) Immediate Annuity-In this case, you invest a lump sum in a product and your pension or annuity starts immediately. Let us say you have around Rs.1 Cr and if you buy immediate annuity plans, then the pension will start immediately from next month.

2) Deferred Annuity-In this case your annuity starts after a certain period. Let us say your current age is 30 years and you are planning to retire at the age of 60 years. If you buy a deferred annuity plan, then you will invest up to your retirement age i.e. up to 60 years of age. After 60 years of retirement, your pension will start.

I tried to explain the same with below illustration below.

As I mentioned above, LIC New Pension Plan Jeevan Dhara 2 is a deferred annuity plan but not an immediate annuity plan.

LIC New Pension Plan Jeevan Dhara 2 – Features and Eligibility

Let us see the features of LIC New Pension Plan Jeevan Dhara 2 features and eligibility.

| LIC New Pension Plan Jeevan Dhara 2 Features (www.basunivesh.com) | |

| Minimum Age At Entry | 20 Yrs |

| Maximum Age At Entry | Option – 1,2,8,9 (10 & 11- Single Premium) – 80 Yrs minus Deferrment Period. Option – 5,6 & 7 – 70 Yrs minus Defferment Period Option – 3 & 4 – 65 Yrs minus Defferment Period Option – 8 & 9 (Secondary Annuitant) – 75 Yrs Option – 11 (Single Premium Secondary Annuitant) – 79 Yrs |

| Minimum Vesting Age | Option – 1 to 9 – 35 Yrs Option – 10 and 11 – 31 Yrs |

| Maximum Vesting Age | Option – 1,2,8,9 (10 & 11- Single Premium) – 80 Yrs Option – 5,6 & 7 – 70 Yrs Option – 3 & 4 – 65 Yrs |

| Defferment Period | Option – 1 to 9 – 5 to 15 Yrs Option – 10 and 11 – 1 to 15 Yrs |

| Premium Payment Term and Mode | Regular (Yrly, Hly, Qtly and Mnthly (Equal to defferment Period) and Single |

| Pension Payment Mode | You can pay an additional premium to top up your benefits. The rates will be based on the prevailing annuity rates. Each such top-up is treated as a single policy for benefits. |

| Minimum Pension | Yrly – Rs.12,000, Hly – Rs.6,000, Qtly – Rs.3,000 and Monthly – Rs.1,000 |

| Top Up Facility | Available only for RETURN OF PREMIUM options (Options 2,9,10 and 11) You can avail of it after the 5 years of commencement of pension. Max 3 times you can withdraw. Withdrawal must not exceed 60% of the total premiums paid. |

| Liquidity | Available only for Return of Premium Option or Purchase Price. |

| Incentive for Policyholders/Nominees/Beneficiary | Available only for OFFLINE purchase policy. 0.5% increase in pension – For regular premium 0.25% increase in pension – For single premium |

| Loan | Available only for Return of Premium Option or Purchase Price. Loan can be availed during or after the deferment period. |

Note – You can surrender at any point in time for the policies of a single premium. However, for regular premiums, surrender is available during or after the deferment period if you paid at least 2 years of premium.

Below are the pension or annuity options one can choose from LIC New Pension Plan Jeevan Dhara 2.

| LIC New Pension Plan Jeevan Dhara 2 Annuity Options (www.basunivesh.com) | |

| Regular Premium Single Life | Option 1 – Life annuity for single Option 2 – Life annuity with return of premium Option 3 – Life annuity with 50% of the return of premium after 75 Yrs Option 4 – Life annuity with 100% return of premium after 75 Yrs Option 5 – Life annuity with 50% of the return of premium after 80 Yrs Option 6 – Life annuity with 100% return of premium after 80 Yrs Option 7 – Life annuity with 5% return of premium after 76 Yrs to 95 Yrs |

| Regular Premium Joint Life | Option 8 – Life annuity for joint life Option 9 – Life annuity with return of premium for joint life |

| Single Premium Single Life | Option 10 – Life annuity with return of ourchase price |

| Single Premium Joint Life | Option 11 – Life annuity with return of purchase price |

LIC New Pension Plan Jeevan Dhara 2 Death Benefits

# Single Life (Options 1 to 7 and 10)

Death during the deferment period -105% of the total premiums paid up to the date of the death will be payable to the nominee.

Death during pension payment period – Pension will stop immediately. No death benefits if you opted for the option of an annuity without the return of a premium. If you opt for the return of purchase price, 100% of the total premium paid will be payable to the nominee. However, if you opted for the return of premium under options 3 and 7 and death happens at 75,80, or between 76 to 95 years of age, then the nominee will receive 100% of the total premium paid minus the sum of early return of premium already paid till the date of death.

# Single Life (Options 8,9 and 11)

Death during the deferment period – On the first death of either of the policyholders, there will not be any death benefit and the policy will continue as usual. However, on the death of the last survivor, death benefits equal to 105% of the total premiums paid up to the date will be payable to the nominee.

Death during pension payment period – On the first death of either of the policyholders, there will not be any death benefit and policy benefit will be payable to the survivor. However, on the death of the last survivor, under option 8, no death benefit will be payable. But under the 9 and 11 annuity options, 100% of the total premium paid is payable to the nominee.

LIC New Pension Plan Jeevan Dhara 2 – Should You Invest?

- As it is a deferred non-linked annuity plan, you can call it a typical TRADITIONAL PLAN of LIC.

- Then what is GUARANTEED here? The pension you will get a post-deferment period is guaranteed. It means you are sure of how much pension you will get.

- Examine the available pension options more closely and you will notice that they all offer a fixed pension amount, although with slight variations. However, this approach fails to consider the potential effects of inflation on your retirement funds. To address this, you have no option but to invest more to sustain your retirement with increasing inflation.

- The second biggest disadvantage is as this is an annuity plan, the pension you receive during your retirement is taxable income and taxed as per your tax slab.

- LIC has introduced additional pension options that were not available in its previous plans, such as the return of premium during the pension period at a specific age. This provides some relief for pensioners in terms of expenses like healthcare. However, as mentioned earlier, it does not address the issue of inflation. Even though Option 7 allows for a 5% premium payout from 76 to 95 years (in addition to regular premiums), the annuity rate is likely lower than the simple annuity for life option.

- In an attempt to attract current policyholders and their beneficiaries, LIC has introduced another tactic by providing incentives in the form of pension benefits. However, these benefits appear to be insignificant. Furthermore, these benefits are exclusively available for offline purchases, indicating a strategy to boost sales through agents.

- If you are willing to overlook the impact of inflation on your retirement funds, have a strong faith in LIC, anticipate lower inflation during your retirement, and depend partially on this product for your retirement, then this policy is an option for you.

- Do remember that the above post is written based on the features but does not consider the annuity rate. However, even if the annuity rates are good (compared to other insurers), I strongly suggest you to stay away from such GUARANTEED products.

Hello Sir kindly post an article on tata aia fortune guarantee supreme plan

Dear Pawan,

Sure. But the result is known as they are low yielding products and hence better to stay away.