LIC Jeevan Azad (868) was launched on 19th January 2023. However, considering the features, eligibility and return expectations, should you invest?

LIC’s Jeevan Azad is a Non-Linked, Non-Participating, Individual, and Savings plan which offers a combination of savings and protection plan.

This plan is available only through OFFLINE mode.

Eligibility of LIC Jeevan Azad (868)

The eligibility conditions are as below.

- Minimum age at entry – 90 days

- Minimum age at maturity – 18 years

- Maximum age at entry – 50 years

- Maximum age at maturity – 70 years

- Policy Term – 15 years to 20 years

- Premium paying term – Policy Term minus 8 years. Hence, if you choose 15 years policy, then the policy payment term will be 7 years and for 20 years policy, it will be 12 years.

- Minimum Sum Assured – Rs.2 lakh

- Maximum Sum Assured – Rs.5 lakh

- The total Basic Sum Assured under all policies issued to an individual under this plan shall not exceed Rs 5 lakh.

- This plan offers a settlement option (to get the maturity benefits in installments).

- This plan offers the death benefit also in installments.

- Premiums can be paid regularly at yearly, half-yearly, quarterly or monthly intervals (monthly premiums through NACH only) or through salary deductions.

Benefits of LIC Jeevan Azad (868)

# Maturity Benefit

On Life Assured surviving the stipulated Date of Maturity, ’Sum Assured on Maturity’ which is equal to ‘Basic Sum Assured’ shall be payable.

# Death Benefit

The death benefit payable on the death of the life assured during the policy term after the date of commencement of risk but before the date of maturity shall be “Sum Assured on Death” where “Sum Assured on Death” is defined as higher of ‘Basic Sum Assured’ or ‘7 times of Annualized Premium’.

This Death Benefit shall not be less than 105% of “Total Premiums Paid” up to the date of death.

However, in the case of minor Life Assured, whose age at entry is below 8 years, on death before the commencement of Risk (as specified in Para 2 below), the Death Benefit payable shall be a refund of premium(s) paid (excluding taxes, extra premium and rider premium(s), if any), without interest.

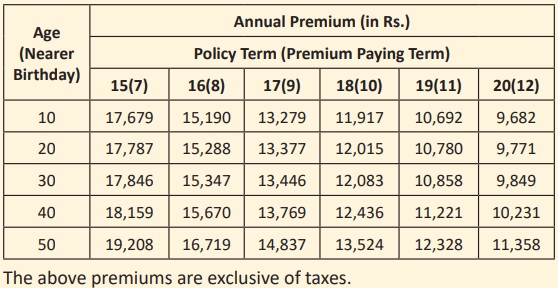

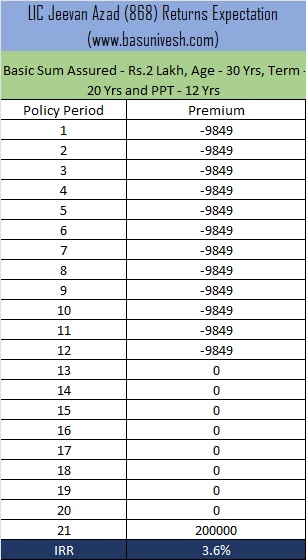

How much returns you can expect from LIC Jeevan Azad (868)?

Let us take an example from the LIC brochure itself.

Now let us take an example of a 30-year-old guy opting for 20 years policy. Hence, his premium paying term is 12 years. Based on that if we calculate the returns on investment, it is equal like your savings account interest rate!!

If we add the tax, then returns will again reduce. I am not sure why LIC launched this plan where nothing is new and in the current higher interest regime, who can opt for such policies?

LIC Jeevan Azad (868) – Why you must NOT invest?

Let us consider this as pure insurance products (for time being ignore the returns part), then you noticed that the maximum sum assured is just Rs.5 lakh. Think for how many years your family can survive in your absence with this death benefit. A year or to the maximum two years. Then how this plan is going to be considered a protection plan??

If we concentrate on the returns part, then you noticed from the above calculation that it is less than 4%. No matter whatever way you calculate, the returns will not cross beyond 5%. When in the current scenario of high-interest rates attractive products are available means why one will invest for 15 to 20 years and satisfy with a meager savings account rate.

LIC has a history of launching a new product during the month of December or January. Mainly to concentrate on tax-saving individuals. This plan I think a hurriedly launched product targetting such individuals.

Considering all these pointers, I strongly suggest you stay away from this product. Investing in products like PPF gives you a superior return than this product.

HOWEVER, IF YOU ARE HAPPY WITH 4% TO 5% RETURNS FOR YOUR LONG-TERM INVESTMENT OF 15-20 YEARS, THEN PLEASE GO AHEAD AND INVEST!!

LIC thinks that based upon it’s dominant position, the image of the corporation and the field force that it has builtup to market such products, it can sell any product through them. The policyholders always see that it will be in their benefit to purchase LIC policies due to their blind faith in the organization and it’s sales force. Only 2% of them can make such calculation. Misselling is at it’s best. So don’t worry, it will be a success story. Money will creep in.

Dear Mohinder,

Thanks for sharing your views.