Recently LIC declared the bonus rates for the year 2020 – 2021 (As per March 2020 valuation). Let us see the complete details about LIC Bonus Rates for 2020 – 2021 and how they affect your life insurance returns.

LIC of India has declared the latest bonus rates for the valuation period 1 st April 2019 to 31st March 2020.

Meaning of bonus for LIC policies

When you buy a traditional with profit product from LIC, then your returns from such policy mainly depends on what will be the rate of bonus. LIC declares bonus on the yearly basis. Usually, you will not find any such drastic change. But it is always better to track the bonus rates.

Let us say you bought LIC’s Jeevan Anand for the term of 20 years and the sum assured as Rs.5,00,000. If LIC declared a bonus as Rs.45 for this product, then the calculation will be as below.

The bonus rates will be based on three criteria.

# Term of policy-Higher the tenure means higher the rate.

# Sum Assured-LIC bonus depends on per Rs.1,000 of Sum Assured. Hence, if you bought higher sum assured policy, then your bonus accumulation will be at the higher end.

So from above example, if LIC declared you Rs.45 as bonus per Rs.1,000 sum assured for 20 years policy, then the bonus accumulation for that year will be as below.

Rs.22,500=(Rs.45 x Rs.5,00,000)/Rs.1,000.

Remember this Rs.22,500 will not be payable to you. But it will be with LIC and you receive this amount during the time of death claim or maturity. The most important point to note that they will not add any amount on this Rs.22,500. It will remain same till the period of death claim or maturity date.

There are various types of benefits LIC policies offer you like Bonus, Loyalty Addition or Final Additional Bonus.

Types of LIC benefits

# Simple Reversionary Bonus

LIC will declare this on yearly basis and added to your policy account. You will get it either at maturity or if there is a death claim. If you decide to exit from the policy during the policy period by surrendering it, then a certain portion of such accrued bonus will be payable to you. Do remember that this type of bonus does not compound every year and hence it is called a simple reversionary bonus.

# Final Additional Bonus (FAB)

Final Additional Bonus (FAB) is a one-time additional bonus, which is paid along with the maturity amount. It is an additional one time bonus along with the simple reversionary bonus and added to the policy account. As I told, it is a one-time payment you will receive at maturity, death claim if you surrender it (one year preceding the date of maturity).

# Loyalty Bonus (LA)

Based on the policy features, certain LIC policies are eligible to avail this LA. LA is also a one time payment kind of benefit. Unlike the simple reversionary bonus, which becomes a part of the policy benefits as and when it is declared, loyalty additions shall be available to the policyholder only at the time of exit from the policy. Hence, they became the part of policy benefit at once during the policy exit (due to maturity, death or surrender)

How to calculate returns for your LIC policy?

In simple, I explained how to calculate bonus for a year. But LIC offers different products like the endowment, limited endowment or money back plans. In such a situation, you may find it difficult to calculate returns on your LIC plan. Hence, I created a video about this.

This below video will explain you about how to calculate returns on your LIC plans using excel sheet. It is too simple and convenient for you to calculate.

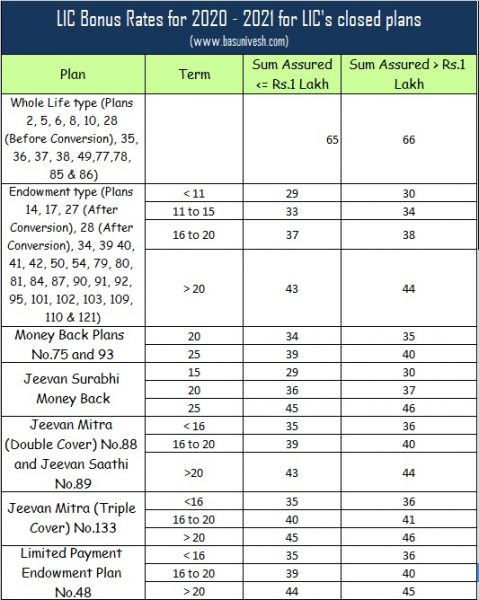

LIC Bonus Rates for 2020 – 2021 for closed plans

Hope you got clarity about the importance of bonus rates for your traditional plans. Now let us concentrate on recently declared LIC Bonus Rates for 2020 – 2021

The below reversionary bonus rates are applicable for policy year entered upon during the inter valuation period i.e. 01/04/2019 to 31/03/2020 and in force for full sum assured as on 31/03/2020. It would apply to policies resulting into claims by death or maturity (including those discounted within one year of maturity) or surrendered on or after 01/01/2020.

The interim bonus rates are applicable to policies in respect of each policy year entered upon after 31/03/2020 and result into claims by death or maturity (including those discounted within one year of maturity) or are surrendered during the period commencing from 01/01/2020 and ending 9 months from the date of next valuation.

This time, I separated the plans in two ways. One for the old policies which are closed and another list for the new policies which are currently available for purchase.

The above list is for the basic policies. In the below list, I am sharing with you the remaining special products which are closed.

LIC Bonus Rates for 2020 – 2021 for new plans

Let us now look into the bonus rates of new plans.

Final Additional Bonus for 2020 – 2021

As I mentioned above, FAB is a one-time additional bonus payable to policyholders. The minimum term of the policy to be eligible for FAB is 15 years and above. LIC maintained the same FAB rates which are available for the last year. You can refer the last year’s FAB rates at the LIC website.

his Final (Additional) Bonuses are applicable In the case of Plans of Groups 1, 2, 8, 9 and 10 mentioned below.

- (Group 1) Whole Life type (Plans 2, 5, 6, 8, 10, 28 (Before Conversion), 35, 36, 37, 38, 49,77,78, 85 & 86)

- (Group 2) Endowment type (Plans 14, 17, 27 (After Conversion), 28 (After Conversion), 34, 39 40, 41, 42, 50, 54, 79, 80, 81, 84, 87, 90, 91, 92, 95, 101, 102, 103, 109, 110 & 121)

- (Group 8) Jeevan Mitra (Double Cover plan), Jeevan Saathi (Plans 88 & 89)

- (Group 9) Jeevan Mitra (Triple Cover Plan: Plan 133 )

- (Group 10) Limited Payment Endowment (Plan 48)

LIC Loyalty Addition Rates 2020 – 2021

Few plans like Jeevan Saral or Jeevan Shree have additional beneficial features like offering you the LA. I will try to share the LA rates for Jeevan Saral, Jeevan Shree and for few popular plans. .

LIC Jeevan Saral Loyalty Addition Rates for 2020 – 2021

Let us now look at the LA rates for most popular product of LIC Jeevan Saral.

Conclusion:- It is evident that LIC policies even though invested heavily by Indian investors, are low in returns and the returns may vary anywhere around 5% to 6%. For long term goals, relying on such debt products and also illiquid products may not be a prudent idea of wealth creation. It is up to you to judge whether you want to go ahead and buy such low yielding products are not. At the same time, those who already invested may continue if you feel 5% to 6% tax-free returns are best for your long term goals.

- The Dark Side of Compounding: How 2% Kills Rs.30 Lakh

- Flexi Cap Funds: Why Your 10-Year Return Chart Is Lying

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

What is the loyalty Addition for New Jeevan Shree Table 151 for 16 year term plan. It is very difficult to get this exact info for Table 151

Also how does one get this info as even the branch is not very helpful

Dear JK,

It ranges from Rs.35 to Rs.60 per Rs.1,000 Sum Assured. You can easily get this information from the nearest branch.

Thank you for your prompt response sir! Would we be eligible for Loyalty addition for 2021, if we surrender now or should we wait till Jan 2022? I read somewhere that Loyalty additional declared as of March 2021 will apply to policies maturing after Dec 31, 2021. Not sure how that works and if there is a different process for surrender vs Maturity?

Dear Ajay,

How much additional amount do you get by waiting for another 6 months? It is peanut. Better to close now.

Apologies for the typo sir, I meant to say we started our jeevan saral policies in March 2010, so have completed 11 + years. Would it make sense to surrender them now and would we be eligible for the Loyalty addition declared in Sep 2021 or do we have to wait till Jan 2022, to get the latest Loyalty addition benefit?

Dear Ajay,

As it completed 10+ years, better to surrender.

Dear Sir – This is very useful. We have a couple of Jeevan Saral policies that we started in March 2020. We would like to surrender these policies but got understand that LIC has declared the Bonus/Loyalty addition for 2021 in Sep this year. Should we wait till Jan 2022 to be eligible for the Loyalty addition or would it be applicable even if we surrender now i..e oct 2021

Dear Ajay,

In this plan, you will get LA only if you surrender after 10 years but not before that. Hence, you have no option but to close after 10 years.

I have started a Bima diamond policy of sum assured 100000 in Feb 2017. Paid premium of Rs. 6235 yearly for 2017, 2018 and 2019. I did not paid premium for 2020 and 2021.

Kindly suggest me approximately how much amount I will get if I surrender my policy now

Hello,

My Policy for plan T-112 matures in Aug.21

Loyality bonus rates for 2021-22 will be declared in the month of Sep-21

What Loyality bonus rates will be applicable for my policy as maturity will be prior to declaration of rates ?

Thanks

Dear Anil,

It is the previous year LA.

Dear Mr. Basavaraj,

Thank you for sharing this.

However, your conclusion is incomplete.

In your conclusion, where you mentioned LIC’s return 5% to 6%, you seem to have forgotten to 2 VERY Important words: “Guaranteed” & “Safe”.

An article’s conclusion must always give complete & impartial information.

Dear Naresh,

GUARANTEED and SAFE at what cost????

I hope the day will come soon when the poor indian common man will stop considering LIC as an investment avenue. Not to mention the fact that the government is seriously considering divestment of it’s holding in LIC.

I am also sharing a moneylife link, to an article on how Jeevan Saral has the potential of being a Jeevan Terdha ..

https://www.moneylife.in/article/jeevan-saral-lic-pays-up-rs2667-lakh-after-chairman-is-summoned-by-consumer-commission/59165.html

Dear SRR,

God BLESS YOU and if you are confident, then let LIC relaunch one more new version of this product 🙂

Hi

I have a clarification on the Jeevan Shree loyalty bonus rate. My 5lakh policy of 20year (with 12 premiums paid) is maturing in July ’21. Loyalty bonus of 2.75L @ 550/1000 rate is indicated in the maturity claim statement from LIC

I remember checking the loyalty bonus last year and the table indicated 810/1000. I know that rate applied for policies maturing last year and LIC issues rates for every year separately but what explains a drop of 260/1000?

Can you throw some light on the basis of loyalty bonus rate calculations of LIC, apart from the usual ‘it is based on the gains from investment that LIC wants to say’!

Thanks in advance & regards, Sreedhar

Dear Sreedhar,

Sadly neither LIC discloses why the fall nor we can question it.

Hello Sreedhar,

My Jeevan Shree policy with exact details as your Policy (i.e 5lakh policy of 20year & 12 paid premium) is maturing next month (Aug-21).

Can you share the breakup of amount and what rates were given to you by LIC and did they deducted any tax ?

Thanks

Anil

Dear basu ji ,

Plan no 152 of lic jeevan rekha

Please give a complete chart of final addtional bonous (f.a.b)chart of this plan

Policy is fully paid up at the year 2009

Thanks

Regards

Nikhil dwivedi

Dear Nikhil,

With whatever limited information I have, I shared it. However, you can get the same on LIC website or with the branch.

Why Jeevan Saral premium band ( for LA calculations) has been changed from annually to monthly? Any idea

This will make investors loose few lakhs per policy

Dear Nikhil,

Hard to say.

Hi,

I have Jeevan Saral policy which is ending this Oct 2021. 20000 premium with double accident/death benefit. How much money I will get when I exit after 10 yr

thanks, a lot

Dear Mouli,

Approach the branch in this regard.

Hello Sir,

First of all, thank you so much for this forum as I suppose it definitely helps people like me who are confused and need clarity but are unable to get it from the LIC office or the agent themselves.

I took the Jeevan Saral policy in April 2010 for a yearly premium of 24,020.

1. I want to surrender this policy and want to know how much to expect if I close it?

2. Can I expect any bonus? Loyalty benefit or so?

3. Procedure/Documents to surrender?

4. How long does it take to get the money credited to my account post surrendering?

5. Do you suggest I wait for another month before surrendering as then it will be 11 years completed.

6. I hope it’s fine if I do not pay this year’s Premium as I anyway plan to surrender. Suggest pls!

7. Is it a must to go to the branch to surrender? I am residing in Delhi currently but the actual branch is in Hyderabad. Any workaround I have to surrender policy without having to travel which will cost me money and time in these covid times.

Dear Venela,

As it completed 10 years, you can surrender now and eligible for LA. Regarding the other process-related queries, be in touch with the concerned LIC branch.

Could you please explain how the one-time FAB is calculated? The link in the article points to the Bonus Information which is the rate for reversionary bonus ( which I believe is yearly bonus accrual). How will the FAB be added? I am assuming for New Jeevan Anand(815) – In case of death during the policy term (Before 35 years ), 125% of Sum Assured + Bonus ( as mentioned in Bonus link) + Final Addition Bonus (???) will be paid. Thanks.

Dear Saurabh,

FAB is a one time payment either at death or maturity based on sum assured.

Hello sir

I bought Jeevan Anand last year in October 2020 .but today I feel I should have invested in PPF and terms insurance.

I am paying 6000 per month .for sum assured of 20 lacs

Sir should I leave LIC now.?

Please guide

Dear Navneet,

If you are ready to forgo the payment that you already made, then you can close it.

When does the bonus start to get accrued. I mean if I bought a policy in the month of January 2017, will I start getting bonus accrued from year ending March 2017 or March 2018?,

Dear Arvind,

From March 2017.

Dear Sir,

Your articles are quite helpful for a layman to understand the complexity. I still have a question regarding my own policy. I have a Jeevan Surbhi Plan 106 for 15 Years, Premium was 5253 paid in 12 installments. Sum Assured was 50000. 30% of Sum Assured have been paid twice by LIC to me as I remember. I submitted the Bond Paper to LIC a month ago and Final Sum paid was just 26150. I don’t understand the calculations here as you can see that my total payment was 63000 approx and I am getting just 56150. LIC people just say that it is all done by computer.

Dear Prakash,

You are not receiving all Rs.56,150 now. Instead as per your claim, you received two survival benefits earlier. Hence, you forgot the time value of money. What they paid is correct.

Hi, I’m in a fix whether to discontinue my LIC Policy. I had taken Jeevan Lakshya (833) plan in Feb 2019 for 20years. I’m paying a monthly premium of rs.6019. Basic sum assured is 15lakhs. Now I feel I could have invested in something better like PPF with a term insurance cover. Kindly advise whether I should discontinue or not considering the returns from LIC is just about 4-5%? If I discontinue when should I do it, because I will not get any money back if I do so now.

Dear Sharon,

You have currently no option but to complete at least 3 years to get part of what you paid or you have to forget of whatever you paid now.

Dear Sir, I have invested in Jeevanshree 112 policy (25 year term) in 2002, sum assured 8 lakhs, premium paying 16 years. How much will i get on maturity in 2027? Can i surrender earlier?

Dear Ashok,

As the premium payment period is over, better to continue till maturity.

Hi Sir,

I have invested Rs18375 in Jeevan Saral on quarter basis from last 9 years. So i just want to know shall i need to continue with this policy or quit ? Someone says to me quit from this policy and invest in PPF .

Please suggest

Dear Rahul,

Quit after the completion of 10th year.

Basu,

Do you think LIC paying 21,000 crores to buy IDBI Bank last year and getting nothing as profit out of it has cost the LIC customers so bad?

Dear Pradeep,

Every move to save a failing institute and acting BLINDLY on Government instruction is obviously at the cost of customers of LIC, which many unable to understand.

Cheaters have reduced bonus rates further this year (which was already very poor) to pay more to the govt as dividends.

Dear Pradeep,

It is we the buyers must beware always than pointing at LIC.

Thanks for posting on LIC bonus rates. This is very useful to individuals like us who are fooled by advisors who are against LIC and tell to invest in SIP/Mutual fund. My jeevan Shree policy has matured this year and given me a decent tax-free return of 18 Lakhs on savins of Rs.4.5 lakhs and IRR works out to be above 9%.

Dear Naresh,

Great 🙂 But can you check the XIRR of 9%? If it is really 9% from LIC’s New Jeevan Shree, then it is obviously the greatest product.