LIC is launching a new plan Bima Jyoti Plan (Plan No.860) with effect from 22nd February 2021. It is usually a tax-saving season for many salaried. Considering this in mind, every year LIC launch such new plans. Let us see the features, benefits, and eligibility of this plan.

LIC Bima Jyoti (Plan No.860) is a Non-linked, Non-participating, Individual, Limited Premium Payment, Life

Insurance Savings Plan. Under this plan, Guaranteed Additions shall accrue at the rate of Rs.50 per thousand Basic Sum Assured at the end of each policy year throughout the policy term.

This plan is available in both ONLINE and OFFLINE mode.

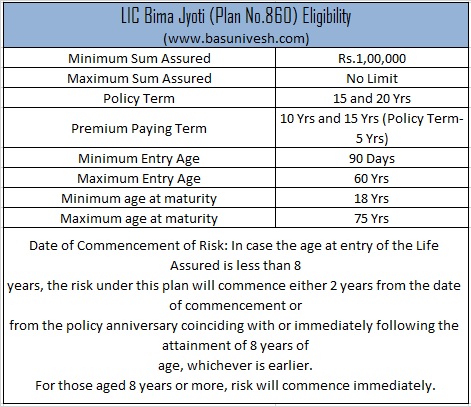

LIC Bima Jyoti (Plan No.860) Eligibility

Let us now look into the eligibility of LIC Bima Jyoti (Plan No.860).

Available riders in this plan are – Accidental Death and Disability Rider Benefit, Accident Benefit Rider, Term Assurance Rider, New Critical Illness Benefit Rider and Premium Waiver Benefit Rider.

Premium Payment Option – Yearly, Half Yearly, Quarterly and Monthly.

Loan is also available under this plan. After payment of premiums for at least two full year’s subject to the following conditions:

a) The maximum loan that can be granted as a percentage of surrender value are as under:

• For inforce policies – upto 90%

• For paid-up policies – upto 80%

b) The rate of interest to be charged for the loan amount would be determined by the Corporation from time to time.

c) The loan during the minority of Life Assured can be availed by the proposer provided the loan is raised for the benefit of the minor Life Assured.

d) In the event of default in payment of loan interest on the due dates and when the outstanding loan amount along with interest is to exceed the surrender value, the Corporation would be entitled to foreclose such policies. Such policies when being foreclosed shall be entitled to payment of the difference of surrender value and the outstanding loan amount along with interest if any.

e) In case the policy shall mature or surrendered or becomes a claim by death, the amount of

outstanding Loan together with all interest shall be recovered from the claim benefit

payment.

LIC Bima Jyoti (Plan No.860) Benefits

The benefits payable under this policy are as below.

Death Benefit

a) Before the commencement of Life Risk- On death during the policy term before the date of commencement of risk: Return of premiums paid excluding taxes, any. extra amount chargeable under the policy due to underwriting decision and rider premium(s), if any.

b) Death during the commencement of Life Risk – On death during the policy term after the date of commencement of risk: “Sum Assured on Death” along with accrued Guaranteed Additions Where “Sum Assured on Death” is defined as the higher of

• 125 % of Basic Sum Assured or

• 7 times of annualized premium

This death benefit shall not be less than 105% of all the premiums paid upto the date of death. Premiums referred above shall not include taxes, any extra amount chargeable under the policy due to underwriting decision and rider premium(s), if any.

Maturity Benefit

On the life assured surviving to the end of the policy term, “Sum Assured on Maturity” along with accrued Guaranteed Additions, shall be payable. Where “Sum Assured on Maturity” is equal to the Basic Sum Assured

Guaranteed Addition (GA) in LIC Bima Jyoti (Plan No.860)

This policy not offers any bonus. Instead a fixed GUARANTEED ADDITION at the rate of Rs.50 per thousand Basic Sum Assured shall accrue at the end of each policy year. In case of death under inforce policy, the Guaranteed Addition in the year of death shall be for full policy year. In case the premiums are not duly paid, the Guaranteed Additions shall cease to accrue under a policy.

In case of a paid-up policy or on surrender of a policy, the Guaranteed Addition for the policy

year in which the last premium is received (i.e. wherein full year’s premiums have not been

received) will be added on proportionate basis in proportion to the premium received for that

year.

LIC Bima Jyoti (Plan No.860) – Should you invest?

In India, to sell any products easily three things are important. They are SAFETY, TAX BENEFIT and GUARANTEED. This plan offers all these three features. However, at what cost? Let us see.

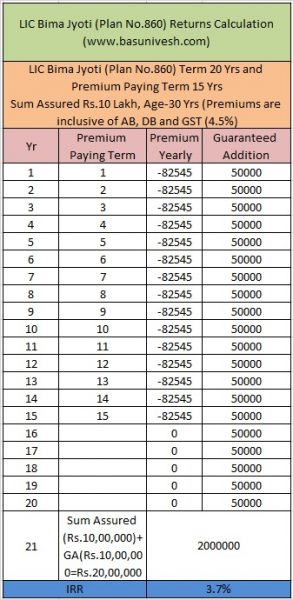

# In this plan the main highlight is GUARANTEED ADDITION of Rs.50 per Rs.1,000 SA. We feel great that in such a low-yielding Bank FD rates, LIC is offering us the GUARANTEED Rs.50 per Rs.1,000 Sum Assured. It is nothing but 5%. Also, such GUARANTEED ADDITION added each year to your policy will not earn additional interest. LIC will show it as yearly accumulated guaranteed addition. But as it is idle for the next 15 years or 20 years, its value will diminish drastically. Hence, never assume that your returns on investment is 5%. Instead, it may be around 4%. Let us take an example of Term 20 Yrs and Premium Paying Term 15 Yrs

Sum Assured Rs.10 Lakh, Age-30 Yrs (Premiums are inclusive of AB, DB and GST (4.5%). The yearly premium will be Rs.82,545 . The returns are less than 4%. Look at the below table.

As I told above, even though you may feel LIC is giving us the GUARANTEED ADDITION of Rs.50 per Rs.1,000 Sum Assured, due to no additional returns to this GA, the end results will be less than 4%.

# But few may argue that it is tax-free. Hence, why not explore? I feel if you really looking for safety, tax benefit, and decent returns, then products like PPF or SSY (if you are thinking of this policy for your daughter’s educational or marriage goals) are far far better. Even though interest varies in these two products. However, if we compare the current rates, these two are far better than this product.

# If you are looking at this product as insurance, obviously it will not cover your life risk with a hefty premium. If you try to buy the Life Insurance coverage of around 15-20 times of your yearly income (The ideal life insurance one must have to protect his or her life risk), then you have to cough huge premium.

Conclusion:-Considering all these aspects, I repeat again which I am repeating since 10 years of my blogging journey – NEVER COMBINE INSURANCE WITH INVESTMENT. WHEN THE AVERAGE COST OF AGENT COMMISSION IS AROUND 6%, HOW CAN YOU EXPECT RETURNS BEYOND 5%? BUY A PURE TERM LIFE INSURANCE (Even LIC offers it online “LIC’s Tech-Term (No.854) – Online Term Life Insurance Review“) AND STAY AWAY FROM SUCH DUMMY PRODUCTS. If you still feel less than 4% returns for 20 years of your investment is the BEST, then don’t wait…Go ahead and buy it. Your agent will also be richer than you as without investment he will earn a decent around 6% returns for the next 10 or 15 years (as per your premium paying term). The best product for agents but not for investors 🙂

Read our latest posts:-

- EPF Scheme 2026: EPF, EPS and EDLI Rules Explained Fully

- Financial Freedom Without Health? You’ll Regret It Later

- The Peltzman Effect: Why Playing It Safe Can Make You Poor

- Your Retirement Success Depends on Luck, Not Skill

- Never Compare Nifty 50 Index Funds Vs Active Large Cap Funds!

- Nifty 500 Multicap 50:25:25 vs Nifty 500: Which Is Best?

Dear Basu Sir . I am reading your blogs since 2014 ( i guess). Blogs are very interesting,knowledge based,thoughtful and debating . As there is a fair competetion in insurance market and its still a mystry about many things like commission,bonus,death claim ,irr etc.Most among us are not much literate financially. Comments where readers have alleged you for being biased or anti lic is also there. For this i think you should come up with comparision of all companies plans categorywise. That will enrich our knowledge. Actually what i Fssl personally is still pvt cos.are not very much transparent.I have seen many brouchers where they written Guaranteed pension/annuity but the policy is Market linked.Is it possible? One thing people feel more connected with lic the blog goes debatefull when you post something like that.That can even be seen in business tv channels too.

Even I faced some suited booted bank managers who has sold me and my friends some abc policy in names of loan,investment,mortgage and what not.No body is taking care of insurability,human life value etc…

Sorry,if my reply is somewhat lenghty but i request you to have a though on this .I am a great fan of your blog and wishing you very best for getting bigger and better.

Thank you

Dear Deep,

Thanks for your unbiased views. Yes, I know that it is more rampant in private companies. But comparing all the expenses of all private players is impossible for me. At the same time, one thing I want to question that just follows this simple advice of “NEVER COMBINE YOUR INSURANCE WITH INVESTMENT NEED”.

I think to buy lic’ s jeevan labh(936)

In this plan we get 4 times return in 25 year.

While paying term is 16 year

It is approx 8% return

Sir should I buy this plan

Dear Aman,

8% returns from this policy or from other LIC policies? Can you elaborate how you arrived at that 8%?

I checked with LIC official website and for 30 yrs individual, premium paid in 15 years will be approx. 76000*14+77500.

This is for 45 years of age. So returns will be around 4% tax free.

Dear Anuj,

What is this 14 in this? As I said, returns are around 4%. If you feel this is the BEST returns for your 15-20 years of investment, then GO AHEAD!!

If you take a 10yr premium payment term and 15yr plan, the return is 7.2% am I missing something?

Dear Ankit,

May I know how? Can you elaborate more? As per me, in this case also, the returns are approximately the same.

Hey Basavaraj,

Thank you for guiding us on the investment part and superb blog on this current LIC Bhima plan. I have been advised from legends to buy LIC term insurance rather than buying a maturity plan.

It would be glad if you will explain me on LIC whole life policy name Jeevan Umang (Plan-945). I only had interest in this however, it would be great if you could give me a breakdown summary of this plan as well. This plan has both Guaranteed and Non-Guaranteed benefits but the agent was not able to give me a valid summary of this at the end of the Premium Paying Term.

Also, are you there on social media platforms/ somewhere I can easily have an interaction with you. Your current website has lot of information of finance and investment planning. This is what amazed me.

Awaiting your revert on this.

Thank you

Prasad

Dear Prasad,

Thanks for your views. Regarding Jeevan Umang, I have already written a post. Please refer the same. Yes, I am on social media. Refer the footer links.

Dear Sir,

My IRR & XIRR are higher that what has been shown in the article.

I would like to know if something is missed in the calculations shown below.

The example that I worked on is similar to what you have shown.

This is a 20y plan with 15y premium paying term with 10L of SA and GA being the same as in the article.

A B C D

Yr Starting Premium Gua.Add Cash Flow XIRR IRR

22-Feb-21 -82,545 – -82,545 6.66% 7%

22-Feb-22 -82,545 50,000 -32,545

22-Feb-23 -82,545 50,000 -32,545

22-Feb-24 -82,545 50,000 -32,545

22-Feb-25 -82,545 50,000 -32,545

22-Feb-26 -82,545 50,000 -32,545

22-Feb-27 -82,545 50,000 -32,545

22-Feb-28 -82,545 50,000 -32,545

22-Feb-29 -82,545 50,000 -32,545

22-Feb-30 -82,545 50,000 -32,545

22-Feb-31 -82,545 50,000 -32,545

22-Feb-32 -82,545 50,000 -32,545

22-Feb-33 -82,545 50,000 -32,545

22-Feb-34 -82,545 50,000 -32,545

22-Feb-35 -82,545 50,000 -32,545

22-Feb-36 – 50,000 50,000

22-Feb-37 – 50,000 50,000

22-Feb-38 – 50,000 50,000

22-Feb-39 – 50,000 50,000

22-Feb-40 – 50,000 50,000

22-Feb-41 – 1, 050,000 1,050,000

Dear Prashant,

For your information, you will not receive the GA on yearly basis. You will get the GA at maturity. Hence, your cash flow during the premium payment term must not be adjusted to declared GA. This is what I told above. LIC will declare the GA. They will not add a single rupee to such accumulated GA up to maturity. Hence, as there are no additional returns on such accumulated GA, even though GA looks 5%, the actual IRR will be less than 4%. Hope you understood what I am trying to say.

Thank you Sir.

Time value of money plays an important part here.

50,000 today is more important than 50,000 after 20 years.

Dear Prashanth,

Yes, and that’s why GA of 5% of this plan does not mean returns of 5%. It is less than that as we are receiving at maturity.

Dear Sir,

The formatting has gone awry after posting my comment..

Am not sure why because I had ensured that the numbers are properly spaced & formatted while typing.

Essentially, there are 4 columns:

A -> Year starting

B -> Premium

C -> Gua. Add

D -> Cash Flow = B+C

From the 16th year onwards (22-Feb-36), there are no premiums and so no negative cash flows unlike how the table shows.

Would be obliged if you can have a look at these numbers.

Dear Prashanth,

In cashflow, you are considering the unrealized GA (which you will get at maturity or death). How can you consider and adjust to premium? If you are receiving that in your pocket, then you can adjust such cash flow towards the premium. I hope you got it.

This comment can be ignored.

Dear Prashanth,

No worries. It is learning for both of us and for the visitors to this post 🙂

What ever Basu sir writes it is in the interest of investors and fundamental rule never combine insurance with investment and they never balance each other.have a pure term plan and invest in market if you want to take risk or invest in ppf or ssy if you do not want to take risk.lessons learnt from basu

Dear Rahul,

Thanks for endorsing my views 🙂

The blogger has tried to mislead with flawed information.He has shown the premium as consistently 83545 throught out incl GST, he is either naive or wicked not to mention that the premium is 78990 and the rest is GST which goes to GOVT. With diff rates for 1st and subsequent years.Which analogous product does not incurr GST.He has also not mentioned the cut available on IT rebates under sec80c and 10(10D) on Maturity.People should save themselves from such self proclaim advisers.

Dear Partha,

Oh sorry!! Now if we consider Rs.78,990 as a premium from the second year onwards (2.25% GST than the flat 4.5% of what I considered wrongly for the whole tenure), then is it create more than 4.5% returns?? I can understand your anguish 🙂 Come out with valid points to show me more than 4.5% returns from this plan, then I surrender to your knowledge than my ILLITERACY. Second thing, I have not tagged myself as ADVISER 🙂

Sir,

Though bit aware of not mixing investments and insurance together, my friend in his age 44 bought a Jeevan Umang 845 policy for a substantial yearly premium of 4 Lakhs for 15 years. He has got PPF, PF, company provided life insurance and limited MF investments as well. As LIC provides guaranteed returns say around 5% with insurance, he has been convinced of the same. As he has done the premium for the past 2 years now, is it worth to stop the premium after 3 years payment (I believe minimum tenure of 3 years payment is mandatory out of 15 years) and start focusing on high yield investments like NPS/MF. Will the NPF/MF returns outweigh the losses due to the early termination/surrender charges and any other loss of bonus of this LIC policy termination. Please advice. Thanks a lot.

Dear Ramesh,

Except for GA (if declared in plan feature), nothing is guaranteed in LIC also as it depends on the bonus or LA rates (as applicable). If he closes after 3 years, then there may be a huge loss. Is he in a position to bear this?

It’s stupid to post article on LIC if you are not recommending them, do you get paid from any private insurance firm for writing against LIC . I don’t know how you get insider information of LIC when the product is not out in the market?

Dear Naresh,

I can understand your anger 🙂 It is common to me!! Come up with valid reasons to point out my wrong. If you prove that I am getting paid by private insurance companies to write against LIC, then I will be your servant throughout my life. Can you accept the challenge before doing such allegations? If you not able to prove, then let me know what you do? Can I sue you against your baseless allegations? Be matured 🙂

Dear Author,

I agree that you share your independent views but let me point out its not bias free. I agree 100% with your views.

But can you please also reviews all life insurance companies products and compare them with each other also. Compare and show each companies plan current bonus rates. Then you can surely say you are bias free.

You never share private companies plans and review then as freely as you try to bash out avaery single lic plan on the basis of roi.

Be clear. Do you ever show roi of the person who invest in Anand for 3 years and get death claim. You just simply love bashing LIC products for whatever reason is urs that u knw very well. Not every decision is based on roi for an average middle class person.

I am again saying ur views are right but not bias free.

Dear Arpit,

If you land only on the posts where I wrote about LIC, then it is your BIAS 🙂 Check my old posts and you noticed that I wrote about private players products also. Now coming back to Jeevan Anand 3 years payment and death claim part, ROI (I feel pity to use this word for death claims but forced to use this mainly because of you used it) is much much higher if the same person purchased the term life insurance from the same insurance company (LIC). I am repeating again, for me it doesn’t matter whether it is LIC or private players. I hope you understood my point of views 🙂

Dear Naresh ,

Please try to see the world out of LIC’s sunglasses !! Try to educate yourself financially to advise anybody about personal finance and for yourself too . Requesting you to focus on conclusion , where you will find the basic grammar of personal finance and answer of your immature thought.

If anybody really want to give security to his client he should sell only pure protection (that is term ins) with pure investment ( you can find so many things to learn from this blog ).

Dear Saikat,

I agree with your views.

There are good and bad products in the market. The Author intend here to help people pick the right one. In the conclusion he clearly mentions why it is not a good idea to mix insurance and investment. You have no right to allege someone without understanding. In case of doubts you could have simple post a question. I am pretty sure author is competent and matured enough to answer your queries.

Dear Lawish,

Thanks for endorsing my views 🙂

Dear Lawish

I agree with your views. But has author ever reviewed any private insurers insurance policy before it is launched and before even the premium rates are known.

I agree that one should not mix insurance and investment. But not every person has capacity to distribute his savings in to 2 parts.

I always foloow this author and his analysis is goods but even before the proxy details are out he should have used due caution. Just by giving a disclaimer or saying I have posted this without knowing premium rates does not absolve him of his responsibilities he bear.

He is a fee only consultant/advisor. But more than 90% of people reading his blog are not those who ever pay fee to any one for investment or insurance advice.

Just a simple question if he has such a soft corner for LIC policies only. Why doesn’t he compare the returns that private companies are giving and returns which LIC is giving in terms of Bonus/FAB/LA or any other parameter.

Dear Arpit,

Such comments from few individuals (who associate with LIC), are common to me whenever I wrote such posts 🙂 Now coming back to your points, let me answer one by one.

“I always follow this author and his analysis is goods but even before the proxy details are out he should have used due caution. Just by giving a disclaimer or saying I have posted this without knowing premium rates does not absolve him of his responsibilities he bear.”- Whether at any point of time in the history of my blogging, anything changed in my claim after getting the premium rates?? In whatever way you calculate, the returns from such traditional plans will not cross more than 5% to 6%, then where comes the false claims??

“He is a fee only consultant/advisor. But more than 90% of people reading his blog are not those who ever pay fee to any one for investment or insurance advice.”- Yes, I am a FEE-ONLY FINANCIAL PLANNER. I am not writing this blog with the intention that all the readers will pay me the fee 🙂 Cautioning is my right and avoiding people in miss buying is the idea behind this. When I am not at all associated with any insurance company or financial institution for my earnings, why should I have to defend a particular company?

“Just a simple question if he has such a soft corner for LIC policies only. Why doesn’t he compare the returns that private companies are giving and returns which LIC is giving in terms of Bonus/FAB/LA or any other parameter.”- If you land on my blog when I wrote LIC but not whenever I write, then it is your problem but not my problem. I have written about private players also. For me, if LIC’s Bonus/FAB/LA are high does not mean I have to defend LIC. At the end what matters is, how much returns I am generating (If such plans are considered as INVESTMENT) and how much my family will get in my absence (when I am not here) than have a love affair with LIC or with private players 🙂