EPFO announced EPF Interest Rate FY 2021-22. Let us see the historical EPF interest rates from 1952-53 to 2021-22.

EPF forms one of the most important parts of anyone’s retirement portfolio. It is also one of the attractive debt instruments as its fixed, safe, and tax-free return at retirement. Hence, many try to invest more along with the default option of EPF in the form of VPF.

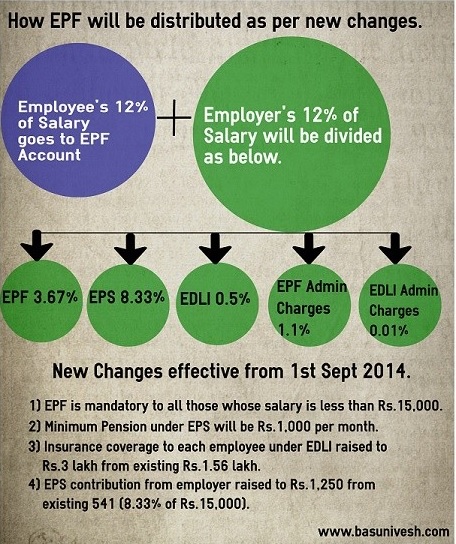

Before proceeding further, first, let us understand how your EPF contribution is divided. I have written a detailed post in this regard earlier (Employee Provident Fund (EPF)-Changed rules from 1st Sept 2014“. However, I will again show you in detail about your and your employer’s EPF contribution being split.

Note:- Now the EDLI is raised from earlier Rs.3 lakh to Rs.7 Lakh (EDLI Scheme 2021 – EPF Life Insurance of Rs. 7 Lakh).

EPF Interest Rate FY 2021-22 – Historical EPF rates 1952 to 2022

EPF Interest Rate for FY 2021-22 is decreased from existing 8.5% to 8.1%. However, let us look into the past 70 years’ data of this rate. Let me divide this 70 years of data into the first 40 years and then 30 years. The charts look like below.

If we look at the historical returns of EPF, in FY 1952-53, it was 3% and gradually increased and during FY 1977-78, it touched the 8% interest rate (which is around the current rate).

From FY 1978-79 to up to 1991-92 it continuously on an uptrend and first 40 years peak was 12%.

From 1992-93 to 1999-00, it was at its peak of 12%. Later on, it is lowering year on year and now it touched to 8.1% for FY 2021-22.

I have mentioned the rates yearwise also from 1952-53 to 2021-22

Year EPF Interest Rate

1952-53 3.0%

1953-54 3.0%

1954-55 3.0%

1955-56 3.5%

1956-57 3.5%

1957-58 3.8%

1958-59 3.8%

1959-60 3.8%

1960-61 3.8%

1961-62 3.8%

1962-63 3.8%

1963-64 4.0%

1964-65 4.3%

1965-66 4.5%

1966-67 4.8%

1967-68 5.0%

1968-69 5.3%

1969-70 5.5%

1970-71 5.7%

1971-72 5.8%

1972-73 6.0%

1973-74 6.0%

1974-75 6.5%

1975-76 7.0%

1976-77 7.5%

1977-78 8.0%

1978-79 8.3%

1979-80 8.3%

1980-81 8.3%

1981-82 8.5%

1982-83 8.8%

1983-84 9.2%

1984-85 9.9%

1985-86 10.2%

1986-87 11.0%

1987-88 11.5%

1988-89 11.8%

1989-90 12.0%

1990-91 12.0%

1991-92 12.0%

1992-93 12.0%

1993-94 12.0%

1994-95 12.0%

1995-96 12.0%

1996-97 12.0%

1997-98 12.0%

1998-99 12.0%

1999-00 12.0%

2000-01 11.0%

2001-02 9.5%

2002-03 9.5%

2003-04 9.1%

2004-05 9.5%

2005-06 8.5%

2006-07 8.5%

2007-08 8.5%

2008-09 8.5%

2009-10 8.5%

2010-11 9.5%

2011-12 8.3%

2012-13 8.5%

2013-14 8.8%

2014-15 8.8%

2015-16 8.8%

2016-17 8.7%

2017-18 8.6%

2018-19 8.7%

2019-20 8.5%

2020-21 8.5%

2021-22 8.1%

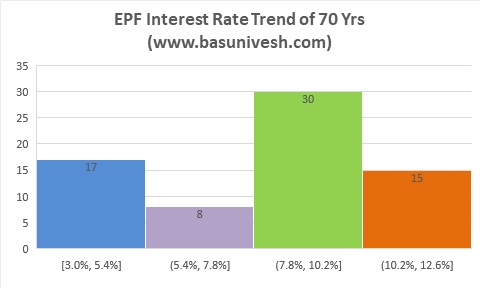

If we draw the histogram chart of these 70 years’ data, then it looks like below.

The majority of the time, the interest rate was within the range of 7.8% to 10.2%. Then the next highest was in the range of 3% to 5.4%.

Hence, the current interest rate change from the existing 8.5% to 8.1% is not new. However, yes it obviously hurts many salaried.

Let us check the EPF contribution history also.

If you check out the historical EPF contribution rate, it increased a lot from around 6.25% in 1956 to currently at 12% of Basic+DA.

Conclusion – The current 8.1% is still better than any other available debt option. Hence, rather than taking it as a negative way, continue your EPF and VPF contribution as usual.

Sir,

I am a regular reader of your articles and it is very informative.

I need your inputs on the Long term capital gains w.r.t site sale proceedings.

My query:

1. How to calculate long term capital gains for both shares and site sale.

2. Can we sell a site and purchase another site or flat or house to avoid long term capital gains

3. There are some accounts where we can park the sale proceedings for a certain period to avoid long term capital gains tax.

Request you to please elaborate and help me understand the above.

Regards

Sridhar

Dear Sridhar,

1) It is bit lengthy process and hard for me to explain the same in comment. You can refer ITR website for a detailed explaination on this.

2) Yes

3) Yes, capital gain savings bonds are there.

very informative. thank you

Dear Chari,

My pleasure 🙂

Appreciate the same Basavaraj. Although you had a separate story on this in relation to budge proposal where if one invest more than Rs 250000/- towards EPF+VPF if one were to be in 30/20% tax bracket the tax will get levied on a yearly basis and tax will get levied for the previous year where the investment is higher. You mentioned it is up to oneself whether they want continue investing or not. Having said as financial expert in these difficult times is it adviseable considering NPS is simply unattractive and basically blocks one’s money and only other option is PPF where the rates are lower compared to EPF. Do advise as a middle class person who does not lot of investments or money what is the best and safe way to ensure principal is safe and you get return which i understand is far less than real consumer inflation.

Dear AG,

Thanks. Even though interest rates are falling in both EPF and PPF, I still prefer these two debt products for retirement over NPS.

Thanks Basavaraj for the response. I know it is one’s choice to decide based on risk appetite as well as taxation would you advise investment over 250000 in EPF over PPF if possible definitely not NPS.

Dear AG,

Yes, if the amount is more than Rs.2,50,000 in EPF and exhausted PPF, then my choice is not NPS. Instead, in debt space, I search for Gilt Funds.