IRDA Published annual report for 2014-15. So let us analyze the IRDA Claim Settlement Ratio 2014-15 and understand which is best life insurance company.

First, let us understand the IRDA Claim Settlement Ratio 2014-15 and identify where your insurance companies stand for.

Note-Refer latest report at “IRDA Claim Settlement Ratio 2015-16 | Best Life Insurance Company in 2017“.

What is Claim Settlement Ratio?

It shows you the number of claims settled by a life insurance company during the particular year. It is calculated as the total number of claims received by the total number of claims settled. Let us say, Life Insurance Company received 100 claims and among that it settled 98 means 98% claim settlement ratio.

You notice that this ratio not differentiate of which types of products, life insurance companies settled. It may be term insurance, endowment plans, or ULIPs. Therefore, it is hard to judge the data perfectly. Even recent clarification and changes to Section 45 of IRDA rules clearly indicates that claim settlement ratio is not the biggest criteria.

Hence, I always suggest that claim settlement ratio is just an indicator but not the sole criteria to select an insurance company. This, I suggest to those who are looking for term insurance. I explained the same in my earlier post “Top 5 Best Online Term Insurance Plans in India-2016“.

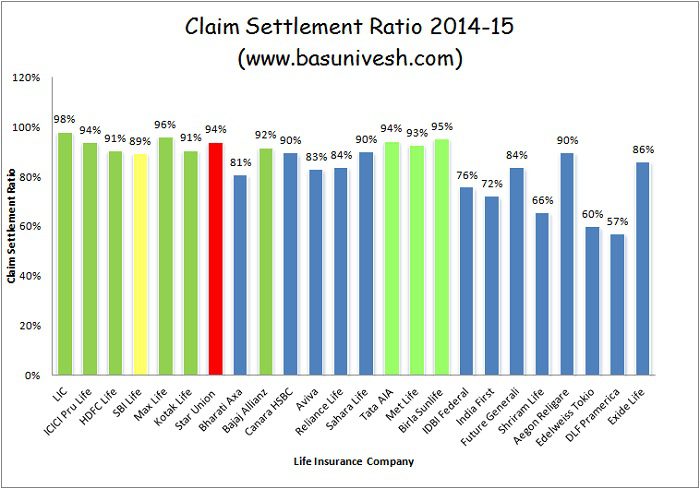

Below is the chart of IRDA Claim Settlement Ratio 2014-15.

You notice that Star Union being a new company managed to settle around 94% of claims. At the same time, SBI Life’s claim settlement ratio decreased below 90%.

I indicated with yellow colour for those companies, whose ratio stands above 90%.

As usual, LIC stands topper with 98% of claim and next to it is Max Life and Birla Life. ICICI managed the almost same ratio, while HDFC’s claim ratio declined to previous years.

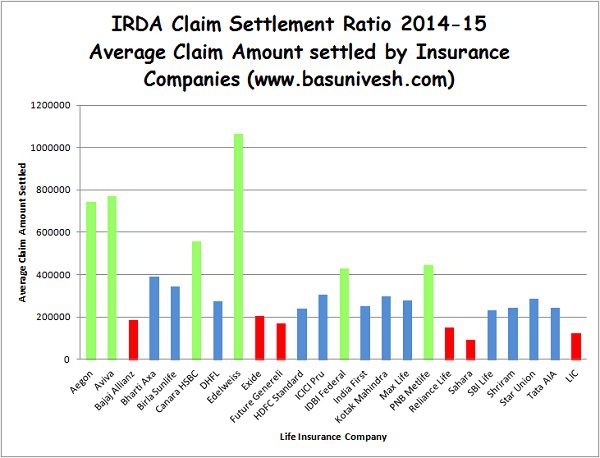

As I said above, it doesn’t classify the product and the amount of the claim it settled. Hence, let us go deeper and identify the average claim settlement amount of these insurance companies. Many fans of LIC may feel it a surprise, but the reality is as below.

Here comes the reality, the average claim settlement of LIC stands below Rs.2,00,000 Sum Assured. That means the claim settlement ratio of LIC mainly includes typical endowment plans.

This is the reason I say don’t rely too much on claim settlement ratio. Understand your requirement, product feature, comfort with company, and the budget.

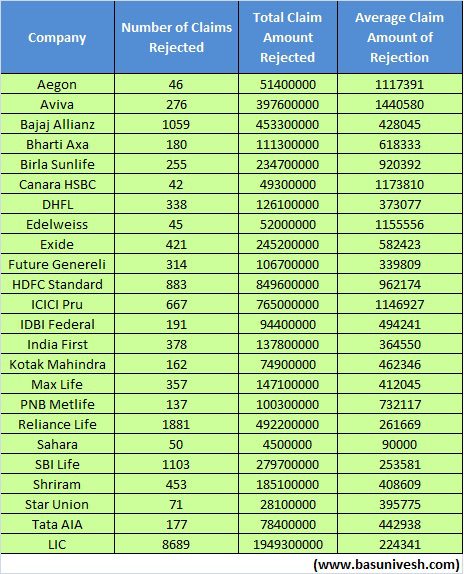

Let us go deeper into this IRDA Claim Settlement Ratio 2014-15. Now we see how much is the claim settlement rejection and what is the average sum assured of these policies.

You notice the difference between average claim settlement amount to average rejection amount. You will find that average rejection size is more to all companies. Definitely, it indicates that they are cautious in settling the claims when it comes to higher sum assured.

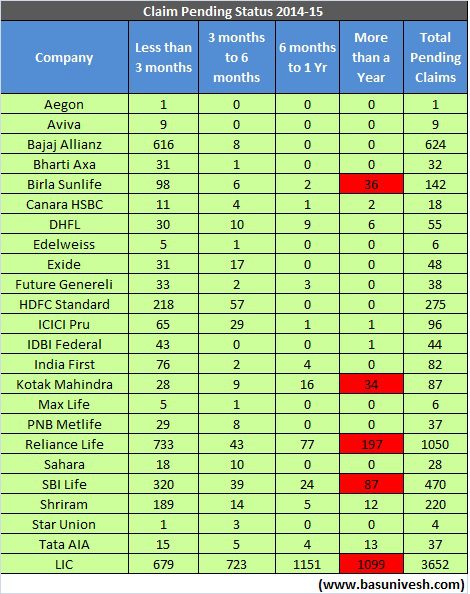

Below data shows the pending claims of all life insurance companies. Along with that it shows since how long they kept them pending. There may be many reasons for it. Some due to insurance companies fault or lethargic attitude or some due to not providing sufficient documents or information by insured or nominees of insured.

You notice that few companies holding the claims for more than a year. I marked them in red colour.

Hope above data will help you to understand what is claim settlement ratio and how much you can rely on this raw data.

Source-IRDA Annual Report-2014-15.

96 Responses

Hello Baswaraj,

I am 38 and almost decided on ICICI Pru i SMART Protect Lumpsum Plan of Rs.1 Cr. But I am now rethinking and considering HDFC Protect Plus as it has a ACCIDENTAL DISABILITY RIDER OF 1% SA / Month for 10 years.

Now, I am suggested by some of my good friends, that all the riders are of no use and go for base plan of TERM Insurance.

Also, how good are these TERMINAL and CRITICAL ILLNESS benefits. Are they practical in any way and will be really useful in the event of unfortunate incident.

But then there is no other plan where in I can get a Accidental Disability cover of close to 1 Cr.

Pl suggest and help. I am now confused

RAvi-Go ahead as per your friend and buy accidental and critical plans from general insurers.

Hello Basavaraj, But I could not find PA Plan which is providing a disability cover for 1 Cr or any where close to that amount. Can tyou suggest few.

It will be very helpful.

Ravi-Check properly. Many insurers provide this.

Hi Basavaraj,

I am Prashant, currently working with pvt company. I want to buy term plan for me which include all. I have good salary.

in Which company should I go? my age is 29yrs.

Thanks,

Prashant

Prashant-Refer my post “Top 5 Best Online Term Insurance Plans in India-2016“.

Mr basu I’m having health insurance with united india health insurance .I spoke to grievance officer he is not helping me and advising me to take your claim from court.he said that more and more case we will move towards court as we are facing losses in health sector.taking claim from court is a lot of time consuming issue.

Sneha-Raise the issue with IRDA first, then move to consumer court.

Mr basu consumer forum takes around 3 to 4 years of time.it is very difficult and time consuming.why there is not some supportive authority to resolve grievance at earliest.

Sneha-I know it is hard but try your luck before that by knocking the door of IRDA.

Sir kindly start working as consumer activist instead of selling policies.

Sneha-Who is selling policies???

I am 42 years old, NRI, working in Oman. I have taken an online

term policy from Max Life insurance last year when I was in India

on my annual leave.

As I am pre-diabetic and taking oral medication, I have disclosed

my health factors sincerely in my proposal form. Even though

my medical examination results were normal, I have been asked

to pay an extra premium @ 50% based on my health declaration.

Now, I came to know that the Max Life Insurance company will

be merged with HDFC Life within an year and the policy will be

serviced by HDFC Life thereafter.

As you are aware, Max Life is having a CSR of 96.2% and the

claims pending for more than 3 months are only few with them.

Where as HDFC Life’s CSR is only 95% and they have more

than 280 claims pending with them for more than 3 months.

Based on the above facts only, many people decided to choose

Max Life as their preferred life insurance partner. However, more

than 75 lakhs policy holders of Max Life are now going to be taken

over by an insurance company with lower CSR.

In current market scenario, merger can happen between any

private insurers in India, in accordance with the acceptance of

respective Board of Directors. But what will be the consequences

to be faced by the policy holders in such corporate consolidations.?

Can I expect to continue with the same kind of quality treatment

and policy contract after the merger of these companies.? Is there

any regulation by IRDA to protect the interest of policy holders in

such mergers.? Being honest in every aspect, can I continue to pay

the premium and go ahead with my existing insurance contract.?

Expecting your valuable comments.

Babu-Please continue, no need to worry. The same rules and regulations continue.

please comment on cigna ttk medical insurance company since it is new in the market.premium is low compared to other insurance companies.

Subramanyam-The data is available in above post.

Hi Basu,

I am confused between Kotak Preferred e-term plan and max online term plan. Please suggest me which one to go for.

Yash-What is your confusion?

Which of the two would be a better choice? The premium is almost the same in both the plans. However, Max would be giving me 50 lacs SA while Kotak only 40 lacs as per the annual income. Max has a higher claim settlement ratio as compared to Kotak.

So please suggest which one would be ideal.

I have L&T Insurance Medisure Classic Plan for me and Apollo Munich Optima Restore for my family. Can tell about claim settlement ratio, Are these genuine companies or creating trouble for customers

Bhatt-Data is available in above post.

Dear Mr. Basu,

It is very nice information shared by you…. Thanks for the same.

I am also associated with Both Life as well as non life insurers.

I really wonder as how IRDA is publishing its data about all these companies

so lately i.e. we have ended up with FY 2015-16 by one quarter and we have to submit

our Tax returns by 31st of July every year.

Don’t you think in today’s IT era IRDA need to improve its late responding in disclosing

data of all the companies available in the market.

Regards

Vishnu Agarwal

9422202863

Vishnu-Yes your points are valid. But we have to accept the regulators also 🙂

Thank you for sharing valuable information. It’s a great work.

I had purchase edelweiss e-term but its settlement rate is very low should i continue with it.

Rakesh-Yes, continue.

My mother in law she is a self employed her age is 41,annual income is 270000 in ITR.she is below 10 standard. Which company term plan is suitable for her.

Donvan-Refer my post “Top 5 Best Online Term Insurance Plans in India-2016“.

Dear sir

To add my agent also informed that as per irda guidelines all claims have to be honored after 3 years

Is it true

Dear sir,

I have taken a term policy with lic for 25 lakhs in 2011

However I missed to declare a ulip policy with reliance which I have closed in 2014

Will it create a problem

Please help

Sai-No need to worry as the ULIP is already closed.

Hello Basavaraj ,

I am 35 years old,would like to buy term insurance for 1cr upto 35yrs.

Please let me know witch is the bast way to by “Term Insurance Plan” online or offline.

what is the different between online and offline.

Please give me right company to bay term plan.

Maxlife

PNB Metlife mera term

ICICI PrudentialiProtect Smart – Life

HDFC Life Click 2 Protect Plus

Can you please suggest to chose,or any other option

Thanks

Vamsi-Online is best if you want to handle on your own and ready to save few agents commission. Otherwise, go for offline. All mentioned companies are best. Chose the one based on your comfort.

Pnb metlife and sbi e shield which is preferable

Donvan-Both are best.

Hi ,

You are doing a great job. really helpful

Well m 30 years and not married, self employed

i plan to buy a health insurance. i was hospitalized 4-5 years back regarding a dislocated knee joint. but it a was minor incident.

now i want to know if i should go for individual or family floater plan. also i think a cover of 7.5 – 8 lac will be good as the costs is increasing year by year.

also i need to buy a term plan as well. m earning 12 lac per annum , self employed

Himanshu-You can go with family floater. Buy term plan to the tune of at least 15-20 times of your yearly income.

Dear Sir,

My dob is 21.07.1980. I have applied online for term plan from lic on dated 03/01/2016, for rs 25.00 lacs for 25 years, after undergoing medical tests two times, and submitting all documents, lic has delayed for 05 months, and on 02nd june i have got mail from LIC that as your age is increased to 36 years, please pay rs.500/-more for issuing policy, it it worth taking policy from LIC, when the delay is from LIC, how can they ask for extra premium, also i have doubt that whether LIC will settle the claim after my death. Please suggest whether i should pay extra premium and go with lic, or choose some other company.

Ratnesh-Frist understand whether Rs.25 lakh worth for you? Second thing, do you feel LIC is the only insurer in India?

Hi Basu,

Very Nice article, Can you please give me a suggestion.

Im earning 8L p.a, I want to take a Term Plan of 1.5 Cr for 30-40 years. Companys include multiple option n riders, Accidental, CI, extra life, monthy income etc. I got confused here.

Wheter its good to go for it.

Or if i take 75 Lac Term plan and 75 lac some investment plan. if so please suggest some company to go for it.

I think HDFC life, ICICI Pru life, MAx life, Bajaj Alianz, which one to go for from your view point.

Pradeep-Buy term insurance without any riders and payment as lump sum at the death of policy holder.

Hi Basu,

Could you please eloborate why do we need to choose a plan without riders?

Best Regards,

Pradeep

Pradeep-Instead of riders, if you opt for individual insurance from general insurers then the features will be higher than the limited features of riders with life insurance.

HI

Basu

Please let me know witch is the bast way to by “Term Insurance Plan” online or offline.

what is the different between online and offline.

I am planing to bay max life 1.5 CR term plan. (how to bay online or offline)

If Required, Please give me right company to bay term plan.

Your prompt and affirmative reply will be highly appreciated.

Thanks & Warmest Regards & Respect,

Virendrakumar Masani

+91 9998454221

[email protected]

Viru-Online is best and cost effective. You can go ahead with Max Life. No issues.

Hi Basu,

Thanks for all the research and analysis report.

I am 40 years old and planning for 2 crore term policy from max life insurance along with increasingly monthly income. What is your comment on this policy ?

Also, What if there is an unfortunate demise of nominee ? Can we change the nominee from wife to children ?

Krishna-Yes, you can go ahead with MaxLife. In case of nominee death, the maturity will be payable based on legal heir laws. Yes, you can change the nominee at any point of time.

sir ,pl confirm health insurance claim settle date 2014-2015

Vinod-It is available at “Best Health Insurance Company in India-Based on IRDA 2014-15 Incurred Ratio“.

I am a 27 year old and have been thinking of buying term insurance with some accidental covers. What options do you suggest? Looking for a cover of 1-1.5 crores.

Kush-Refer my earlier post “Top 5 Best Online Term Insurance Plans in India-2016“.

Hello Basavaraj ,

I am 37 years old,would like to buy term insurance for 1cr upto 35yrs.

PNB Metlife mera term

ICICI PrudentialiProtect Smart – Life

HDFC Life Click 2 Protect Plus

Can you please suggest to chose,or any other option

Thanks

Hello sir,

I want to know that which insurance plan is best of which comp for retirement benefit and also include death and accidental claim and how much money and time period optain we have to choose for better result

My age is 33

Vini-Sadly NONE. Because insurance meant for to protect your life but not for investment.

Hello Sir,

What are the most common reasons for claim rejection?

Regards,

Praveen

Praveen-There are million reasons for one’s death. So there are million reasons for claim settlement. But to simplify, any hidden truths by policyholder during policy buying leads to rejection. A common and wide answer.

LIC pay claims to nominee. when there is no clear nominee the

claim will be kept pending. some times disputes among family

members may cause delay.

Krishnaiah-It is same with others also. What is special with LIC alone?

dear sir,

but lic settled 742243 death claims last year. out of which 1000 out standing for more than year is negligable %. isn’t it sir

Krishnaiah-True but still why such delay?

Basu, awsome article. Thank you for working hard to collect data and present us with these insights. i have one question if you can give me a name or point me to right direction then it will be very much helpfull to me.

i am looking for family floater plan between 5L to 10L, i want no room caping and maximum coverage for most of the deceases. if room caping is removed then bill automatically gets accepted as that is the biggest point to reject a claim or to settle for less money and rest you may have to pay, i may be wrong on this but this is what one of the hospital staff told me.

can you help ? these online comparison sites confuses me more and and once you read terms and conditions you will never trust these representatives.

Sarang-Check Religare Care.

Dear sir,

lic is strong in selling in conventional endowment plans but not term insurance. you analyze how many term insurance plans did lic sold? in 2014-2015. what is the source of pending claims information?

Krishnaiah-I agree that LIC is not a big contender when it comes to selling Term Insurance. This I already showed in above average amount of claims settled by LIC. But sadly no such separate data is available.

Sir,

After viewing and analyzing all that data I wonder if it would be a good idea to not getting any insurance at all and rather put my money in some investment product. At least whatever amount that I will save by not investing in these insurance product will be 100% of my family.

Thanks.

Anil-Insurance is not an investment but risk mitigating strategy. Let us say your income is Rs.10 lakh and you have surplus cash of Rs.2 Cr to Rs.2.5 Cr (which is around 20 times of your yearly income), the you DON”T NEED INSURANCE. If not, then you must have. Also, remember that this Rs.2 Cr must be accessible to your nominees and must know where to invest in your absent. Hope by these words you might understood the importance of insurance 🙂

sir,

what should be the ideal term (in years) of any term plan??

my age is 27 – Male

Arun-It is up to your retirement age. Means, if your age is 27 years and you are plainning for retirement at 60 years, then term of insurance must be 33 years.

I feel IRDA should take strong action against the Insurance companies with low claim settlement. And if their is an issue from Customer side then basis some score , one should become ineligible for insurance.

Sameer-We may hope these points in action in future.

Dear sir I my name is Rakesh Bhardwaj and I am business associate in Tata AIA Life. One of my advisor had sold a Term plan of 1 crore to a Customer of age 31 in August 2015 . The Customer met an accident one and half month before purchase good that policy. We didn’t declared the accident in his proposal form. He had got fractured his left leg and a metal rod was installed in his leg. He has gone through medical test conducted by company and was fine. All his reports were good. Now after reading your article on claims I am worried about him. So please tell me that can this thing be a reason in his claim rejection. What should I do now in this case.

Rakesh-Such accident may not lead to death threatening. Hence, no such issues arised during medical examination. However, there is a declaration clause in proposal (I hope Tata AIA Life also follow the same as that of LIC), that whether you hospitalized for certain days before certain months before applying for this proposal or what. If they prove that proposer mentioned NO wrongly, then it MIGHT create problem. But the possibility of rejection on this is minimal.

Is there any option to declare this now. As the policy is issued only 5 months ago.

Rakesh-You can write it directly to Insurance Company.

Hello Sir,

Being a laymen in thinking to safeguard my family with insurances, i am worried the way lic’s performance and trustability.

Also, in addition to icici pru, I see from your article, aegon and aviva also good players in term insurances. What do you think on my view?

Navin-If LIC worries you, then don’t go for it. At the same time, all insurance companies are equal to me.

CLAIM REAJECTION AMOUNT MOST OF PRIVATE PLAYERS AVG 9 LA BUT LIC 2 LAKS ONLY IN RS WISE HIGH WHY?

Sainath-Good question. Because LIC’s individual policy size mainly constitute endowment plans. The same is also can be presumed from average acceptance amount of claims.

Very good article with updated information. Appreciating your helpful mentality by blogging such nice articles.

After reading this article, got a bit confused. Actually i was planning to go for a Term Plan of 1.5Crore. But after reading the higher amount claims are declining/ squeezing by Insurance Companies, what is your opinion to go for 2 companies with 75L each or 3 companies with 50L each. Can you suggest your thoughts…. If go for multiple companies what are the procedures / declarations etc ?

Loyit.

Loyit-There is no logic in splitting. What if in future all insurance companies centralized their data system (exactly like in Europe countries). Every insurance details, claim details and even the new proposal approved or rejected will be known to one and all insurers. Also what is the guarantee that by splitting you get a claim of at least one company? Probability is also there that all may reject. So don’t do that. Stick to one.

Buy buying multiple insurance, you are complicating your nominee life 🙂

Thank you Basavaraj……..

i want to study CFP ,Kindly give some input

Chandra-First understand about CFP course by visiting FPSB India portal. If you want to pursue, then contact me. My door is always open to help 🙂

You are such a selfless soul!!! May your tribe increase on this earth!!! HIS blessings always be with you. HE will never fail you!! mark my words………

Bless you Basu…..

Satish-Woow..thanks for your kind words Satish 🙂

Nice analysis! But I have few doubts. I am not a fan boy of any insurance company, but after reading your article I want to know few more things. What is the ratio of pending cases amd policy issued? What is the ratio of term insurance claim rejection? Because this where most big settlements have to be done.

I just wondering looking at the market size LIC serves. If you try to get the ratios out of it I guess LIC will not be a villain.

Bharay-Pending cases to policy issued ratio? What it indicates? Sadly there is no such data of product wise claim settlement ratio.

Firstly thanks for all the analysis, however, what I have learnt from your post is that absolute numbers of pending claims (just like any other data) can not be compared. Hence, the ratio of pending claims to the total no. of claims raised will put things in perspective.

Shishir-True but I gave this much only as for public and private sector companies, we don’t have data specific to health insurance. Hence, was just cautious to publish. Sometime readers may interpret in different way.

Thanks for the comprehensive statistics Basavarj, the performance of LIC, which is considered as the safest , is indeed frightening .

Sreerkha-True and hope it enlighten our GUANRATEED INVESTORS.

Nice articulation but somehow the conclusion is missing, maybe you didnot wanted to say it openly 🙂 … but oh man, look at the pending cases of LIC …Definitely no one wants their family to stand in queue, roam around buildings and wait for more than a year to settle the claims .. !

Considering these factors – ICICI Pru or HDFC Life seems to be a safe bet. Your thoughts on this?

Sandeep-You are rightly pointed my intentions 🙂 Look at the average ticket size of the claim LIC settled. It wonders to believe on this.

Thank you for valuable and analytic information

Sir its an nice post with nice explanation. Can you suggest which is best company for general insurance interms of cashless claim and maximum coverage 🙂

Also can you suggest what are things to consider before renewal of existing car insurance 🙂

TIA.

Vishwanath-Your question is wide. I can’t specify names. What are your doubts regarding car insurance renewal? Can you be specific to reply about that doubt?